ABSTRACT

The most used natural fiber in making clothing is cotton. Cotton also produces cottonseed oil which is used in cooking, baked goods, and salad dressing, and meals and hulls which are used for livestock, fish feed and fertilizer. Cotton is one of the major industrial crops that is widely grown in the Central Dry Zone of Myanmar. This study explores all the stakeholders in the cotton value chain process in Meiktila district, Mandalay region. The research particularly looks to the cost and benefit of cotton production farmers, marketing activities, and opportunities and constraints of the stakeholders. This study was conducted through face-to-face interviews with 278 stakeholders (221 farmers, 18 brokers, 9 wholesalers, 5 ginners, 4 cotton seed oil millers and 21 weaving enterprises) by using a simple random sampling method, in April 2022. Descriptive analysis and SWOT analysis were used. The result indicated that Shwe Daung-10, Shwe Daung-8 and the hybrid variety Raka were the most commonly cultivated varieties in the study area. Among the three varieties, Shwe Daung-10 gained the highest profit. The main strengths of cotton production for farmers were climate change resistance, low water requirements and low production cost. The main constraints were lack of setting up a floor price and insufficient money loan for cotton production. Cotton traders mainly bought long staple cotton and short staple cotton directly from farmers. Long staple cotton price (US$0.51/kg) was higher than short staple cotton price (US$0.43/kg). Prices were also different depending on the cotton quality. The quality is normally tested by visual and physical. The main strengths of cotton production for traders were easy to sell at a high price and purchase directly from farmers. The main constraints were low cotton quality due to buying without grading cotton quality and high transportation costs. The domestic spinning industries produce cotton yarns (40/1, 32/1 and 20/1). The domestic cotton yarns were used as weft and imported cotton yarns were used as warp. Most of the weaving enterprise and textile industries in Myanmar mainly produced bottom-wearing (Longyi) by using the business meter. The main strength of the textile industries was having huge market demand in domestic. The main constraints were increasing the price of raw materials, electricity interruption, high price of meter fees and skill labor scarcity. Furthermore, investment in new technologies and upgrades of the existing machinery are needed to improve the production of the textile industry.

Keywords: cotton value chain, cost and benefit, marketing activities, strengths and weaknesses, Meiktila

INTRODUCTION

Cotton is a leading cash crop in the world. Although the world cotton production remained stable over the last few years with the production amount of 26.2 million metric tons (MT) in 2020, the world cotton market share increased from 24% in 2018-2019 to 30% in 2019-2020 (Textile Exchange, 2021). The major cotton producing country in the world is China with a production volume of 5.88 MT, followed by India with 5.33 MT and the United States with 3.82 MT, respectively. The top cotton export country in the world is the United States with the export amount of 3.22 MT, followed by Brazil with 1.72 MT and India with 0.87 MT, respectively (Statista, 2022).

Cotton is one of the most important fiber crops and plays a major role in the textile industries and the economy of Myanmar. Cotton is widely cultivated in the Central Dry Zone (CDZ) areas of Myanmar. Both short staple cotton, Mahlaing-5 and Wagyi and long staple cotton, Ngwe Chi-6, Shwe Daung-8, Ngwe Che-9, Shwe Daung-10 and Ngwe Chi-11 are grown in Sagaing, Mandalay, Magway and Bago Regions, Nay Pyi Taw council area and Southern Shan State. The total sown area of cotton in Myanmar was 168,000 ha with an average yield of 1.75 T/ha and the total production was about 294,000 T in the 2019-2020 fiscal year (MOALI, 2020). In the comparison of short staple and long staple cotton production, the total production amount of long staple cotton (279,118 T) was higher than the short staple cotton (10,281 T) in 2019-2020 (CSO, 2021).

In Myanmar, there are about 18 large spinning and weaving factories and three textile factories under Myanmar Textile Industry (MTI), MI (1). Moreover, the power looms and a huge number of small-scale handlooms are operating in the cooperative and private sectors. About 90% of textile industries are in Mandalay Region and 9% in Sagaing Region. Furthermore, there is also two large scale army owned textile factories in Myanmar (San Thein, 2006). After 2003, cotton was freely traded in the domestic market. In the trading process, the harvested cotton is collected by brokers and sent to the cotton ginning industry, textile factories, and oil mills (Swe Zin Theik, 2018).

Cotton provides not only fiber for the textile industry but also cottonseed oil, meals and hulls. The cottonseed oil is used for cooking oil, baked goods, and salad dressing, and the remained meal and hulls are used for livestock, poultry, fish feed, fertilizer, etc. (Dinesh K. A. et al., 2003). The cotton textile industries in Myanmar produce cotton fabrics, poplin, cotton shirt, mosquito net, cotton yam, vests, towel, longyi, shirts, garments, monk’s robes, etc. (CSO, 2021). Most of the cotton produced in Myanmar is consumed locally. The majority of finished textiles and garments were sold in the wholesale and retail markets, mostly around Mandalay. The volume of raw cotton fiber exported to China through the border has remarkably increased. However, it remains small as compared to local use (Smart Power Myanmar, 2021).

The high yielding and good quality long staple cotton varieties are needed to grow to increase the production of high-quality cotton fibers in Myanmar’s cotton sector. Moreover, the domestic garment, textile industry and other industries which are involved in the cotton value chain sector require setting up stable market prices. Therefore, this study was conducted to know the cotton production, cost and benefit, market price, and market information. In addition, the garment and textile industries, weaving enterprises and all other stakeholders who are related in the cotton value chain process were asked about their activities and attitude for the cotton sector development.

Objectives of the study

- To investigate the cost and benefit and marketing activities of cotton value chain process in Meiktila district, Mandalay Region

- To know the opportunities and constraints of the cotton value chain process in Meiktila district, Mandalay Region

METHODOLOGY

Selection of the study area

Mandalay region consists of seven districts namely Mandalay, Pyin Oo Lwin, Kyaukse, Myingyan, Nyaung U, Yame`thin, and Meiktila. It is situated between north latitude 21 ̊ 57' and east longitudes 96 ̊ 5'. The four focus townships of the study area in Meiktila district, Mandalay region are Thazi, Meiktila, Mahlaing and Wundwin. These townships were chosen due to the major cotton production areas of Myanmar.

Data collection and analysis

This survey was conducted by collaborating with the Cotton and Allied Fibre Crops Division, Department of Agriculture and Department of Agricultural Economics, Yezin Agricultural University from the Ministry of Agriculture, Livestock and Irrigation in April 2022. Data were collected from different stakeholders through personal interviews with a structured questionnaire. In this survey, a total of 278 stakeholders (221 farmers, 18 brokers, 9 wholesalers, 5 ginners, 4 cotton seed oil millers and 21 weaving enterprises) were interviewed using a simple random sampling method. Moreover, key informant interviews (KIIs) were carried out before and during the preparation and implementation of the questionnaire for the interviews to improve the quality of information access. KIIs were asked cotton value chain experts by using face-to-face and distance interviewing. In addition, a focus group discussion (FGD) was carried out to know the different stakeholders’ perspectives and opinions on the cotton value chain process. The different stakeholders’ perception was collected through face-to-face group meeting. The main stakeholders consulted for the FGD were cotton farmers, cotton middlemen, ginners, textile technicians, and weavers.

RESULTS AND DISCUSSION

Cotton farmers

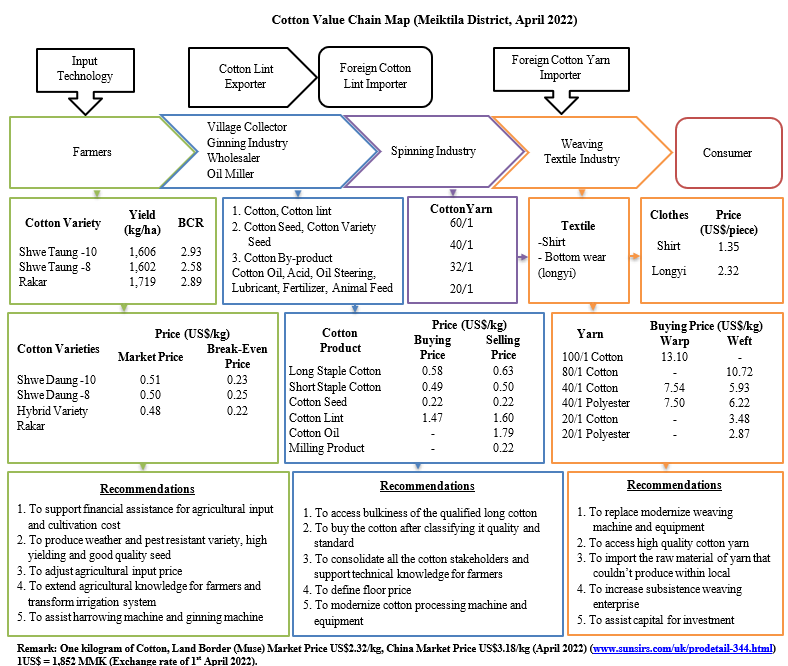

The selected cotton farmers in the study area cultivated seven types of cotton varieties. However, the three main types of cotton varieties grown by the farmers in Meiktila district were Shwe Daung-10, Shwe Daung-8, and hybrid variety Raka. The highest yield variety was Raka with an average amount of 1,719 kg/ha, followed by Shwe Daung-10 with 1,606 kg/ha and Shwe Daung-8 with 1,602 kg/ha. In the comparison of the benefit and cost ratio (BCR) of the farmers' cultivated cotton varieties, Shwe Daung-10 had the highest BCR ratio with 2.93. The second highest BCR ratio variety was the hybrid variety Raka with 2.89 and Shwe Daung-8 had the lowest BCR ratio with 2.58. The bigger the BCR values, the more profit the farmers received. Therefore, among the three varieties, Shwe Daung-10 earned the highest profit. The highest market price variety was Shwe Daung-10 with US$0.51/kg, followed by Shwe Daung-8 with US$0.50/kg and the hybrid variety Raka with US$0.48/kg. The Break-even price was the price that can cover the total variable cost at the current yield of cotton production. The hybrid variety Raka was the lowest break-even price with US$0.22/kg. The second lowest variety was Shwe Daung-10 with US$0.23/kg and Shwe Daung-8 (US$0.25/kg) was the highest break-even price.

Concerning the strengths of cotton crop production, one of the major strengths was climate change resilience. Consequently, getting higher benefits compared to other crops and the availability of good quality cotton seed were the major strengths of the cotton production that helps to extend the cultivation area. In addition, low water requirements, low production cost, low labor requirements, and market stability compared to other crops were the strengths of cotton production.

As weaknesses, one of the major constraints of cotton production was the lack of setting up floor prices that guarantee farmers' income. In addition, cotton farmers faced higher input costs, insufficient credit, and labor shortages during the peak season time that impact cotton production improvement. One of the main suggestions to improve the cotton sector is to support agricultural input such as cottonseeds and fertilizers. Moreover, high yielding, pest and disease resistance and climate change resilience varieties are needed to produce and distribute to farmers. In addition, cultivation technology sharing and balancing agricultural input prices are important for farmers. Furthermore, irrigation water and tractors are needed to support farmers to improve the cotton production area.

Cotton traders

Cotton brokers, millers, wholesalers, and cottonseed oil millers are included in the cotton trading process. Cotton products were sold in both domestic and foreign countries. Both short staple and long staple cotton were directly purchased from the farmers in Thazi, Meiktila, Mahlaing, and Wundwin townships. The price of cotton products was different depending on the type of cotton and buying and selling processes. They bought the long staple and short staple cotton with the average price of US$0.58/kg and US$0.49/kg and then sold with the average price of US$0.63/kg and US$0.59/kg. However, the average buying and selling prices of cottonseeds were the same at US$0.22/kg. The buying and selling prices of cotton lint were different. They bought the cotton lint at US$1.47/kg and then sold it at US$1.60/kg. The average selling price of cottonseed oil was US$1.79/kg and cotton oilcake, the byproduct of cottonseed, was US$0.22/kg.

In the purchasing of cotton, specific quality standards are needed to meet. These quality standards would include quantifiable standards such as strength and dimensional stability of the fabric, abrasion and moisture content, and color fastness and cleanliness. These qualities are normally tested in visual and physical. Most traders sold the purchased cotton without storage due to financial requirements, fire risk concerns, price risk, weight losses, and cotton discoloration. However, 40/1, 32/1, and 20/1 cotton yarns were produced in the domestic industries, and 40/1 cotton yarn, 32/1 polyester yarn, and 20/1 polyester yarn were imported from foreign countries, China and India. The main reason for purchasing imported thread abroad was for its quality. Moreover, it makes a profit due to getting a cheaper price as compared to domestic threads.

Regarding strength, one of the main strengths of cotton trading was easy to sell and getting a higher price. In addition, cotton can be purchased directly from farmers for good communication. As weaknesses, one of the main weaknesses of cotton trading was low cotton quality. Furthermore, without having sufficient good quality cotton seeds and buying without grading the cotton quality were the major constraints of the cotton sector to produce good quality products. The other constraints were price instability and high transportation costs. The main opportunity for cotton trading was having an export market that can export without classifying cotton standards.

The main suggestions to improve the cotton sector are to provide good quality cotton seeds to access a sufficient amount of good quality cotton and to purchase the cotton at different prices depending on the cotton quality standards. In addition, it is needed to distribute knowledge by cooperating with the cotton stakeholders and cotton technicians. Furthermore, setting floor prices and upgrading the existing machinery are needed to produce standard cotton products.

Textiles industry

Cotton fibers were purchased not only from domestic but also from foreign countries. The average buying price of 100/1 warp cotton yarn was US$13.10/kg, and 80/1 weft cotton yarn was US$10.72/kg. Prices were different depending on the types of cotton yarn. While the average price of 40/1 warp cotton yarn was US$7.54/kg, the average price of 40/1 weft cotton yarn was US$5.93/kg. Even though the average price of 40/1 warp polyester yarn was US$7.50/kg, 40/1 weft polyester yarn was US$6.22/kg. However, the average price of 20/1 weft cotton yarn was US$3.48/kg, 20/1 weft polyester yarn was US$2.87/kg. Cotton shirts and traditional longyi were the product of the domestic textile industries. Most of the Weaving enterprise and textile industries mainly produced bottom wearing (Longyi) by using the business meter. The selling price of the cotton shirts was US$1.35/piece and the longyi was US$2.32/piece.

The main strength of the textile industries was having huge domestic market demand that makes a profit. As threats, one of the main threats to the textile industries was the increasing price of cotton fabric and its related raw materials price. Furthermore, electricity interruption and the high price of meter fees were the main constraints for the running of the textile industries. In addition, skill labor scarcity and weakness of labor management were also the main constraints of the textile industries that impact the product quality and quantity. The main suggestions to improve the textile industries are to invest in new technology and upgrade the existing machinery. High quality cotton yarn is important to produce high quality cotton products. Therefore, it is needed to import high-quality cotton yarns that cannot be produced domestically. Furthermore, it is important to support investment funds and encourage subsistence weaving enterprises to improve productivity.

CONCLUSION AND RECOMMENDATION

Farmers mainly cultivate long staple cotton varieties. Among the long staple cotton varieties, Shwe Daung-10 earned the highest benefit in the current situation. Moreover, hybrid varieties' propensity is also good. In cotton trading, it is needed to classify the cotton quality and standard not only in buying but also in ginning to get good quality cotton seeds and lint. Domestic cotton textile and garments which are produced in Wondwin Township, Meiktila district in Myanmar, contribute 70% of the domestic cotton textile and garment market. Domestic cotton yarns are used as weft and imported cotton yarns are used as warp in weaving. Good quality 40/1 warp yarns are also produced domestically. However, to produce 40/1 warp yarns commercially domestically, it is needed to improve not only cotton lint quality but also spinning machinery quality.

In April 2022 cotton market price, the average price of cotton lint in the domestic market was about US$1.31/kg, the price of the land border (Muse) was about US$2.04/kg, and the China market price was about US$2.8/kg. Therefore, domestic cotton traders earned a profit by exporting cotton to China. Systematic trading management and policy are required to fulfill the amount of domestic cotton needed and only the surplus sells to the export market. It is needed to improve the cotton quality and upgrade the machinery of the domestic textile industry to reduce foreign cotton yarns import and foreign currency expenses. The domestic cotton price should be increased depending on the quality of cotton that makes sense to pursuit farmers and cotton traders. Both domestic and foreign demands are needed to be sure and stable to improve the cotton sector sustainably.

In order to improve the current cotton production situation in Myanmar, policy interventions are required. The critical intervention areas for the cotton value chain process are recommended as follows.

- Cotton seed varieties and input

- To produce high-yielding and good-quality cotton seeds by doing a contract farming system.

- To support irrigated water and to hire a harrowing machine and ginning machine with a fair price.

- To support good quality seeds, cultivation technology, and input use management system for farmers.

- To produce hybrid cotton seeds in the cotton research farms and distribute good quality hybrid seeds to farmers.

- Trade and market

- To create a stable market and to purchase cotton by setting up different floor prices depending on the cotton quality.

- To set the price that matches the market price.

- To purchase cotton by grading the cotton quality such as Grade A, B, C, D, etc.

- To purchase cotton separately in accordance with the cotton varieties and store the purchased cotton systematically to maintain the cotton quality.

- To sort separately in ginning of the cotton varieties.

- To upgrade ginning machines, weavings, and textile industry to produce good quality cotton yarns, fabrics, and garments.

- To purchase cotton by measuring the cotton lint length and sell the good quality cotton lint to the domestic spinning industries too.

- To make an incentive with the price gaps to get good quality cotton.

- If the cotton buyers purchase cotton at a low price, the cotton cultivation area can be reduced due to the impact on farmers' income. Therefore, to fulfill the domestic cotton need, avoid buying cotton at the price lower than the market price.

- To estimate the amount of cotton needed for the domestic textile industries and export the surplus depending on the total amount of domestic production, consumption, and surplus.

- To reduce the imported cotton yarns and increase the domestic production of good quality cotton lint.

- To establish a special industrial zone within the Meiktila district for providing a storage facility for cotton lint.

- To hold transparent meetings and discussions with policymakers and stakeholders such as cotton farmers, industrial zone, agricultural technicians, textile and garment and merchants for formulating the pragmatic planning.

- To cooperate with all stakeholders who are involved in the cotton value chain process such as agriculture, ministry of commerce, industrial, state-owned textile, private cotton associations, etc.

REFERENCES

Central Statistical Organization (CSO). (2021). Myanmar Statistical Yearbook, Ministry of Planning, Finance and Industry, The Republic of Union of Myanmar.

Dinesh K. A., Phundan S., Mukta C, Shaikh A. J., Gayal S. G. (2003). Cottonseed Oil Quality, Utilization and Processing. Central Institute for Cotton Research Nagpur. Available online at https://www.cicr.org.in/pdf/cottonseed_oil.pdf

Ministry of Agriculture, Livestock and Irrigation (MOALI). (2020). Myanmar Agriculture Sector in Brief, Department of Planning, The Republic of Union of Myanmar.

San Thein (2006). Agro-based Industries in Myanmar: The Long Road to Industrialization. Institute of Developing Economies Japan External Trade Organization (V.R.F, 414). Available online at https://www.ide.go.jp/library/English/Publish/Reports/Vrf/pdf/414.pdf.

SmartPower Myanmar (2021). Energising Agriculture in Myanmar. A Guide to Prioritising Energy Access Investments into Agricultural Value Chains. Available online at https://downloads.ctfassets.net/nvxmg7jt07o2/aw1dQBBaMLxivJ7jRLu4Z/716b0...

Statista (2022). Global cotton production 2021/2022, by country, Available online at https://www.statista.com/statistics/263055/cotton-production-worldwide-b...

Swe Zin Theik (2018). Agricultural Transformation Processes in Myanmar: Farming of Industrial Crops in Bago Region (West), Journal of Myanmar Academy of Arts and Science, XVI (5), pp. 350–374.

Textile Exchange (2021). Preferred Fiber & Materials Market Report. Available online at https://textileexchange.org/wp-content/uploads/2021/08/Textile-Exchange_....

Myanmar Cotton Value Chain: Case Study in Meiktila District, Mandalay Region

ABSTRACT

The most used natural fiber in making clothing is cotton. Cotton also produces cottonseed oil which is used in cooking, baked goods, and salad dressing, and meals and hulls which are used for livestock, fish feed and fertilizer. Cotton is one of the major industrial crops that is widely grown in the Central Dry Zone of Myanmar. This study explores all the stakeholders in the cotton value chain process in Meiktila district, Mandalay region. The research particularly looks to the cost and benefit of cotton production farmers, marketing activities, and opportunities and constraints of the stakeholders. This study was conducted through face-to-face interviews with 278 stakeholders (221 farmers, 18 brokers, 9 wholesalers, 5 ginners, 4 cotton seed oil millers and 21 weaving enterprises) by using a simple random sampling method, in April 2022. Descriptive analysis and SWOT analysis were used. The result indicated that Shwe Daung-10, Shwe Daung-8 and the hybrid variety Raka were the most commonly cultivated varieties in the study area. Among the three varieties, Shwe Daung-10 gained the highest profit. The main strengths of cotton production for farmers were climate change resistance, low water requirements and low production cost. The main constraints were lack of setting up a floor price and insufficient money loan for cotton production. Cotton traders mainly bought long staple cotton and short staple cotton directly from farmers. Long staple cotton price (US$0.51/kg) was higher than short staple cotton price (US$0.43/kg). Prices were also different depending on the cotton quality. The quality is normally tested by visual and physical. The main strengths of cotton production for traders were easy to sell at a high price and purchase directly from farmers. The main constraints were low cotton quality due to buying without grading cotton quality and high transportation costs. The domestic spinning industries produce cotton yarns (40/1, 32/1 and 20/1). The domestic cotton yarns were used as weft and imported cotton yarns were used as warp. Most of the weaving enterprise and textile industries in Myanmar mainly produced bottom-wearing (Longyi) by using the business meter. The main strength of the textile industries was having huge market demand in domestic. The main constraints were increasing the price of raw materials, electricity interruption, high price of meter fees and skill labor scarcity. Furthermore, investment in new technologies and upgrades of the existing machinery are needed to improve the production of the textile industry.

Keywords: cotton value chain, cost and benefit, marketing activities, strengths and weaknesses, Meiktila

INTRODUCTION

Cotton is a leading cash crop in the world. Although the world cotton production remained stable over the last few years with the production amount of 26.2 million metric tons (MT) in 2020, the world cotton market share increased from 24% in 2018-2019 to 30% in 2019-2020 (Textile Exchange, 2021). The major cotton producing country in the world is China with a production volume of 5.88 MT, followed by India with 5.33 MT and the United States with 3.82 MT, respectively. The top cotton export country in the world is the United States with the export amount of 3.22 MT, followed by Brazil with 1.72 MT and India with 0.87 MT, respectively (Statista, 2022).

Cotton is one of the most important fiber crops and plays a major role in the textile industries and the economy of Myanmar. Cotton is widely cultivated in the Central Dry Zone (CDZ) areas of Myanmar. Both short staple cotton, Mahlaing-5 and Wagyi and long staple cotton, Ngwe Chi-6, Shwe Daung-8, Ngwe Che-9, Shwe Daung-10 and Ngwe Chi-11 are grown in Sagaing, Mandalay, Magway and Bago Regions, Nay Pyi Taw council area and Southern Shan State. The total sown area of cotton in Myanmar was 168,000 ha with an average yield of 1.75 T/ha and the total production was about 294,000 T in the 2019-2020 fiscal year (MOALI, 2020). In the comparison of short staple and long staple cotton production, the total production amount of long staple cotton (279,118 T) was higher than the short staple cotton (10,281 T) in 2019-2020 (CSO, 2021).

In Myanmar, there are about 18 large spinning and weaving factories and three textile factories under Myanmar Textile Industry (MTI), MI (1). Moreover, the power looms and a huge number of small-scale handlooms are operating in the cooperative and private sectors. About 90% of textile industries are in Mandalay Region and 9% in Sagaing Region. Furthermore, there is also two large scale army owned textile factories in Myanmar (San Thein, 2006). After 2003, cotton was freely traded in the domestic market. In the trading process, the harvested cotton is collected by brokers and sent to the cotton ginning industry, textile factories, and oil mills (Swe Zin Theik, 2018).

Cotton provides not only fiber for the textile industry but also cottonseed oil, meals and hulls. The cottonseed oil is used for cooking oil, baked goods, and salad dressing, and the remained meal and hulls are used for livestock, poultry, fish feed, fertilizer, etc. (Dinesh K. A. et al., 2003). The cotton textile industries in Myanmar produce cotton fabrics, poplin, cotton shirt, mosquito net, cotton yam, vests, towel, longyi, shirts, garments, monk’s robes, etc. (CSO, 2021). Most of the cotton produced in Myanmar is consumed locally. The majority of finished textiles and garments were sold in the wholesale and retail markets, mostly around Mandalay. The volume of raw cotton fiber exported to China through the border has remarkably increased. However, it remains small as compared to local use (Smart Power Myanmar, 2021).

The high yielding and good quality long staple cotton varieties are needed to grow to increase the production of high-quality cotton fibers in Myanmar’s cotton sector. Moreover, the domestic garment, textile industry and other industries which are involved in the cotton value chain sector require setting up stable market prices. Therefore, this study was conducted to know the cotton production, cost and benefit, market price, and market information. In addition, the garment and textile industries, weaving enterprises and all other stakeholders who are related in the cotton value chain process were asked about their activities and attitude for the cotton sector development.

Objectives of the study

METHODOLOGY

Selection of the study area

Mandalay region consists of seven districts namely Mandalay, Pyin Oo Lwin, Kyaukse, Myingyan, Nyaung U, Yame`thin, and Meiktila. It is situated between north latitude 21 ̊ 57' and east longitudes 96 ̊ 5'. The four focus townships of the study area in Meiktila district, Mandalay region are Thazi, Meiktila, Mahlaing and Wundwin. These townships were chosen due to the major cotton production areas of Myanmar.

Data collection and analysis

This survey was conducted by collaborating with the Cotton and Allied Fibre Crops Division, Department of Agriculture and Department of Agricultural Economics, Yezin Agricultural University from the Ministry of Agriculture, Livestock and Irrigation in April 2022. Data were collected from different stakeholders through personal interviews with a structured questionnaire. In this survey, a total of 278 stakeholders (221 farmers, 18 brokers, 9 wholesalers, 5 ginners, 4 cotton seed oil millers and 21 weaving enterprises) were interviewed using a simple random sampling method. Moreover, key informant interviews (KIIs) were carried out before and during the preparation and implementation of the questionnaire for the interviews to improve the quality of information access. KIIs were asked cotton value chain experts by using face-to-face and distance interviewing. In addition, a focus group discussion (FGD) was carried out to know the different stakeholders’ perspectives and opinions on the cotton value chain process. The different stakeholders’ perception was collected through face-to-face group meeting. The main stakeholders consulted for the FGD were cotton farmers, cotton middlemen, ginners, textile technicians, and weavers.

RESULTS AND DISCUSSION

Cotton farmers

The selected cotton farmers in the study area cultivated seven types of cotton varieties. However, the three main types of cotton varieties grown by the farmers in Meiktila district were Shwe Daung-10, Shwe Daung-8, and hybrid variety Raka. The highest yield variety was Raka with an average amount of 1,719 kg/ha, followed by Shwe Daung-10 with 1,606 kg/ha and Shwe Daung-8 with 1,602 kg/ha. In the comparison of the benefit and cost ratio (BCR) of the farmers' cultivated cotton varieties, Shwe Daung-10 had the highest BCR ratio with 2.93. The second highest BCR ratio variety was the hybrid variety Raka with 2.89 and Shwe Daung-8 had the lowest BCR ratio with 2.58. The bigger the BCR values, the more profit the farmers received. Therefore, among the three varieties, Shwe Daung-10 earned the highest profit. The highest market price variety was Shwe Daung-10 with US$0.51/kg, followed by Shwe Daung-8 with US$0.50/kg and the hybrid variety Raka with US$0.48/kg. The Break-even price was the price that can cover the total variable cost at the current yield of cotton production. The hybrid variety Raka was the lowest break-even price with US$0.22/kg. The second lowest variety was Shwe Daung-10 with US$0.23/kg and Shwe Daung-8 (US$0.25/kg) was the highest break-even price.

Concerning the strengths of cotton crop production, one of the major strengths was climate change resilience. Consequently, getting higher benefits compared to other crops and the availability of good quality cotton seed were the major strengths of the cotton production that helps to extend the cultivation area. In addition, low water requirements, low production cost, low labor requirements, and market stability compared to other crops were the strengths of cotton production.

As weaknesses, one of the major constraints of cotton production was the lack of setting up floor prices that guarantee farmers' income. In addition, cotton farmers faced higher input costs, insufficient credit, and labor shortages during the peak season time that impact cotton production improvement. One of the main suggestions to improve the cotton sector is to support agricultural input such as cottonseeds and fertilizers. Moreover, high yielding, pest and disease resistance and climate change resilience varieties are needed to produce and distribute to farmers. In addition, cultivation technology sharing and balancing agricultural input prices are important for farmers. Furthermore, irrigation water and tractors are needed to support farmers to improve the cotton production area.

Cotton traders

Cotton brokers, millers, wholesalers, and cottonseed oil millers are included in the cotton trading process. Cotton products were sold in both domestic and foreign countries. Both short staple and long staple cotton were directly purchased from the farmers in Thazi, Meiktila, Mahlaing, and Wundwin townships. The price of cotton products was different depending on the type of cotton and buying and selling processes. They bought the long staple and short staple cotton with the average price of US$0.58/kg and US$0.49/kg and then sold with the average price of US$0.63/kg and US$0.59/kg. However, the average buying and selling prices of cottonseeds were the same at US$0.22/kg. The buying and selling prices of cotton lint were different. They bought the cotton lint at US$1.47/kg and then sold it at US$1.60/kg. The average selling price of cottonseed oil was US$1.79/kg and cotton oilcake, the byproduct of cottonseed, was US$0.22/kg.

In the purchasing of cotton, specific quality standards are needed to meet. These quality standards would include quantifiable standards such as strength and dimensional stability of the fabric, abrasion and moisture content, and color fastness and cleanliness. These qualities are normally tested in visual and physical. Most traders sold the purchased cotton without storage due to financial requirements, fire risk concerns, price risk, weight losses, and cotton discoloration. However, 40/1, 32/1, and 20/1 cotton yarns were produced in the domestic industries, and 40/1 cotton yarn, 32/1 polyester yarn, and 20/1 polyester yarn were imported from foreign countries, China and India. The main reason for purchasing imported thread abroad was for its quality. Moreover, it makes a profit due to getting a cheaper price as compared to domestic threads.

Regarding strength, one of the main strengths of cotton trading was easy to sell and getting a higher price. In addition, cotton can be purchased directly from farmers for good communication. As weaknesses, one of the main weaknesses of cotton trading was low cotton quality. Furthermore, without having sufficient good quality cotton seeds and buying without grading the cotton quality were the major constraints of the cotton sector to produce good quality products. The other constraints were price instability and high transportation costs. The main opportunity for cotton trading was having an export market that can export without classifying cotton standards.

The main suggestions to improve the cotton sector are to provide good quality cotton seeds to access a sufficient amount of good quality cotton and to purchase the cotton at different prices depending on the cotton quality standards. In addition, it is needed to distribute knowledge by cooperating with the cotton stakeholders and cotton technicians. Furthermore, setting floor prices and upgrading the existing machinery are needed to produce standard cotton products.

Textiles industry

Cotton fibers were purchased not only from domestic but also from foreign countries. The average buying price of 100/1 warp cotton yarn was US$13.10/kg, and 80/1 weft cotton yarn was US$10.72/kg. Prices were different depending on the types of cotton yarn. While the average price of 40/1 warp cotton yarn was US$7.54/kg, the average price of 40/1 weft cotton yarn was US$5.93/kg. Even though the average price of 40/1 warp polyester yarn was US$7.50/kg, 40/1 weft polyester yarn was US$6.22/kg. However, the average price of 20/1 weft cotton yarn was US$3.48/kg, 20/1 weft polyester yarn was US$2.87/kg. Cotton shirts and traditional longyi were the product of the domestic textile industries. Most of the Weaving enterprise and textile industries mainly produced bottom wearing (Longyi) by using the business meter. The selling price of the cotton shirts was US$1.35/piece and the longyi was US$2.32/piece.

The main strength of the textile industries was having huge domestic market demand that makes a profit. As threats, one of the main threats to the textile industries was the increasing price of cotton fabric and its related raw materials price. Furthermore, electricity interruption and the high price of meter fees were the main constraints for the running of the textile industries. In addition, skill labor scarcity and weakness of labor management were also the main constraints of the textile industries that impact the product quality and quantity. The main suggestions to improve the textile industries are to invest in new technology and upgrade the existing machinery. High quality cotton yarn is important to produce high quality cotton products. Therefore, it is needed to import high-quality cotton yarns that cannot be produced domestically. Furthermore, it is important to support investment funds and encourage subsistence weaving enterprises to improve productivity.

CONCLUSION AND RECOMMENDATION

Farmers mainly cultivate long staple cotton varieties. Among the long staple cotton varieties, Shwe Daung-10 earned the highest benefit in the current situation. Moreover, hybrid varieties' propensity is also good. In cotton trading, it is needed to classify the cotton quality and standard not only in buying but also in ginning to get good quality cotton seeds and lint. Domestic cotton textile and garments which are produced in Wondwin Township, Meiktila district in Myanmar, contribute 70% of the domestic cotton textile and garment market. Domestic cotton yarns are used as weft and imported cotton yarns are used as warp in weaving. Good quality 40/1 warp yarns are also produced domestically. However, to produce 40/1 warp yarns commercially domestically, it is needed to improve not only cotton lint quality but also spinning machinery quality.

In April 2022 cotton market price, the average price of cotton lint in the domestic market was about US$1.31/kg, the price of the land border (Muse) was about US$2.04/kg, and the China market price was about US$2.8/kg. Therefore, domestic cotton traders earned a profit by exporting cotton to China. Systematic trading management and policy are required to fulfill the amount of domestic cotton needed and only the surplus sells to the export market. It is needed to improve the cotton quality and upgrade the machinery of the domestic textile industry to reduce foreign cotton yarns import and foreign currency expenses. The domestic cotton price should be increased depending on the quality of cotton that makes sense to pursuit farmers and cotton traders. Both domestic and foreign demands are needed to be sure and stable to improve the cotton sector sustainably.

In order to improve the current cotton production situation in Myanmar, policy interventions are required. The critical intervention areas for the cotton value chain process are recommended as follows.

REFERENCES

Central Statistical Organization (CSO). (2021). Myanmar Statistical Yearbook, Ministry of Planning, Finance and Industry, The Republic of Union of Myanmar.

Dinesh K. A., Phundan S., Mukta C, Shaikh A. J., Gayal S. G. (2003). Cottonseed Oil Quality, Utilization and Processing. Central Institute for Cotton Research Nagpur. Available online at https://www.cicr.org.in/pdf/cottonseed_oil.pdf

Ministry of Agriculture, Livestock and Irrigation (MOALI). (2020). Myanmar Agriculture Sector in Brief, Department of Planning, The Republic of Union of Myanmar.

San Thein (2006). Agro-based Industries in Myanmar: The Long Road to Industrialization. Institute of Developing Economies Japan External Trade Organization (V.R.F, 414). Available online at https://www.ide.go.jp/library/English/Publish/Reports/Vrf/pdf/414.pdf.

SmartPower Myanmar (2021). Energising Agriculture in Myanmar. A Guide to Prioritising Energy Access Investments into Agricultural Value Chains. Available online at https://downloads.ctfassets.net/nvxmg7jt07o2/aw1dQBBaMLxivJ7jRLu4Z/716b0...

Statista (2022). Global cotton production 2021/2022, by country, Available online at https://www.statista.com/statistics/263055/cotton-production-worldwide-b...

Swe Zin Theik (2018). Agricultural Transformation Processes in Myanmar: Farming of Industrial Crops in Bago Region (West), Journal of Myanmar Academy of Arts and Science, XVI (5), pp. 350–374.

Textile Exchange (2021). Preferred Fiber & Materials Market Report. Available online at https://textileexchange.org/wp-content/uploads/2021/08/Textile-Exchange_....