ABSTRACT

Working conditions in slaughterhouses as well as the accommodation of the employees are regarded as reasons for the specific susceptibility of the slaughterhouse and meat processing sector for coronavirus infections. After massive breakouts in German meat plants, work processes and work places had to be adjusted in order to reduce infection risks. Some slaughterhouses – among them the biggest in Germany – were even temporarily closed until they had developed and implemented an appropriate and administratively approved concept for risk reduction. Currently (November 2020), the German pig meat sector in particular, is affected by the Corona pandemic, while the impact on cattle and poultry is low. The adaption of slaughtering and meat cutting processes to the COVID-19 risk situation resulted in an estimated capacity reduction of about 15% compared to the pre-coronavirus period. As a consequence, slaughtering and meat cutting is a new and limiting bottleneck in the pig meat value chain. Reduction of imports and an increase of exports of live animals could reduce, but, not eliminate a surplus of live pigs. In October 2020, the number of pigs waiting to be slaughtered is estimated at approximately 500,000 to 630,000. Due to the surplus of live animals, pig prices in Germany dropped by about 12%. But farmers do not only face the price drop: Pigs ready for slaughter have to remain on farms leading to additional feeding costs. Moreover, farmers face additional price cuts if pigs exceed the ideal weight and lose profits because they cannot use their stables for further production. The COVID-19 effects were intensified by the outbreak of African swine fever in Germany and the subsequent export restrictions. This led to an additional price cut of 13% and aggravated the situation of German producers of fattening pigs and piglets. However, a short term adjustment of production quantity to prices is not possible, as present supply is determined by the insemination of sows about a year ago. As a result, it will take until the mid and late 2021 before the low prices can result in lower supply. Currently no sectoral strategy is implemented to deal with the inevitable oversupply of live pigs ready to be slaughtered.

Keywords: COVID-19, Slaughterhouse Sector, Pig Value Chain.

INTRODUCTION

The coronavirus pandemic confronts Germany’s supply systems for fast moving consumer goods (FMCG) with major challenges. In general, these challenges were met without relevant gaps in consumer supply. Retailers and processors re-organized their sourcing and adjusted production volumes. As a result, just toilet paper and flour packages for household use were temporarily scarce.

While the coronavirus pandemic hardly impacted the availability of FMCG, some food value chains were severely affected.

• Fruit and vegetable value chains: These chains deal with perishable goods and goods with an optimal harvesting time. Therefore, they are dependent on a smooth functioning of the production and processing chain in order to realize their value creation potential. Once the production is started, frictions in value chains can hardly be balanced by holding up or accelerating the process. The pandemic especially affected the availability of workforces during harvest time. In normal years, a considerable share of the staff for harvesting is hired in Eastern European countries because the German labor market does not provide a sufficient number of workers willing to carry out these jobs at the given payment. However, in 2020, just a limited number of migrant workers were available due to travel restrictions. As a consequence parts of fruits and vegetables were not picked.

• Meat value chains: In a similar way meat value chains are prone to disturbances because live animals loose quality and value if they are not slaughtered at the optimal time. Moreover, delays in slaughtering leads to additional costs because the animals have to be fed and block stable capacity for further production. In the coronavirus pandemic the slaughtering and cutting turned out to be the bottleneck in the value chain because of a high number of infections.

This paper deals with the impact of COVID-19 on the meat value chain in Germany. It is concentrated on the pigs as the pandemic by now does not have considerable impact in the area of cattle and poultry. It describes the specific susceptibility of slaughterhouses for infections, the impact of risk reducing measures on the slaughter capacity and the resulting effects on the upstream sector.

Expert interviews as well as statistics and reports in specialized agricultural and food media form the basis of the analysis. Expert interviews are necessary to point to relevant effects, to explain the consequences, to make sense of statistics and to fill gaps that are not covered by statistics. Moreover, adjustments of the legal framework are planned and not entered into force so that the effects can only be estimated. However, we recognize that experts may have vested interests. That is why we tried to substantiate their statements by cross validating them through the help of other experts, through our own expertise and through available statistics.

SOME BACKGROUND INFORMATION

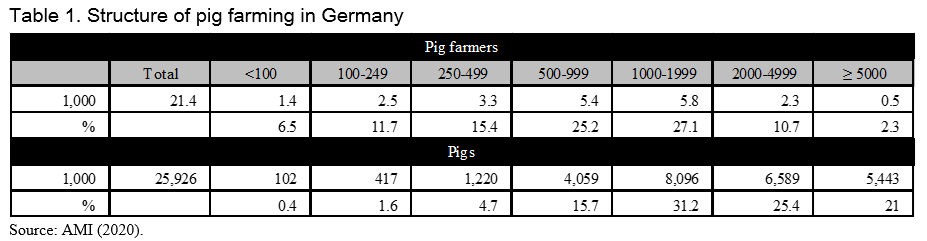

In total, Germany’s 21,400 pig farmers kept about 26 million pigs and produced about 51.8 million slaughter pigs in 2019. Nearly half of the animals are kept on farms with more than 2,000 pigs while the share of the respective pig farmers amounts for less than 15% (Table 1). These farms are especially dependent on pig production and the development of the pig market.

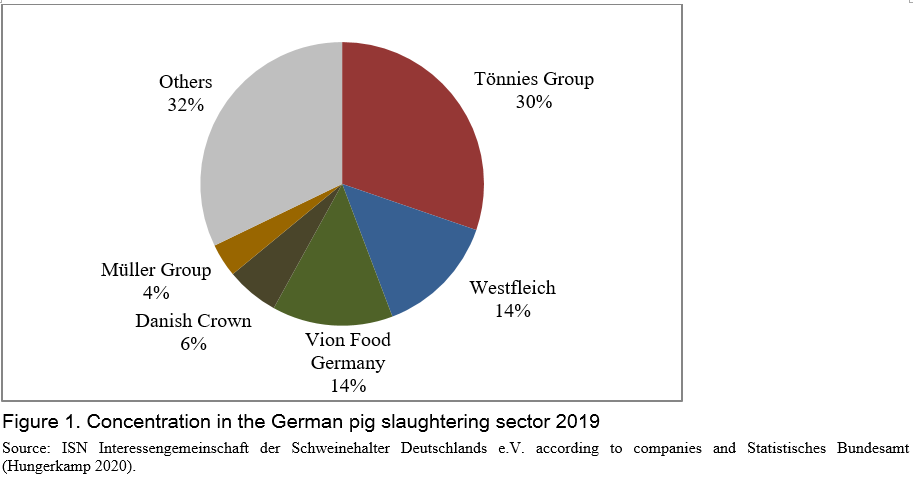

The German pig slaughtering sector is highly concentrated with a concentration rate of the three most relevant companies (CR3) close to 60%. The biggest company, the Tönnies Group, accounts for about a third of overall slaughtering (Figure 1). The big companies are integrated downstream that combine slaughtering, meat cutting and meat processing. They run big slaughterhouses and the shut-down of one individual slaughterhouse can have severe impact on the whole market.

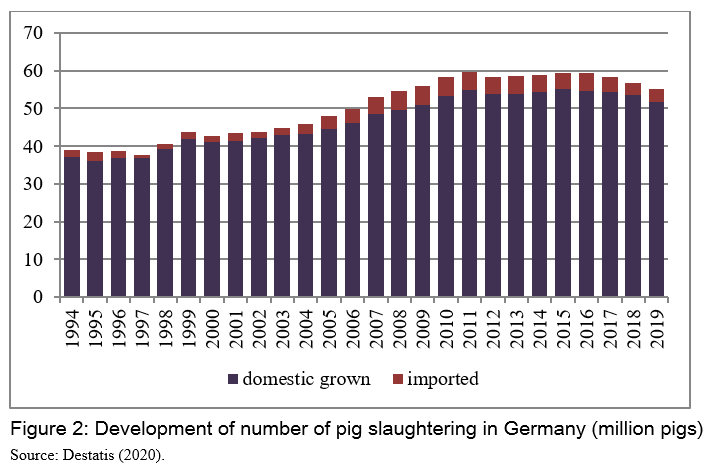

In the 1990s, the German slaughter sector faced a severe crisis. Overcapacities resulted in intense price competition and as a consequence several companies faced serious financial situations. Against this background, a structural crisis cartel was prepared in order to reduce capacities by joint action (Bongaerts 2001). However, the structural crisis cartel did not enter into force and the slaughterhouse sector recovered based on company takeovers, mergers, closure of unprofitable sites and on an increase of German pig production and imports of slaughter pigs. Within 25 years, more precisely between 1994 and 2019, the number of pig slaughtering in Germany increased from about 37m to 52m by approximately 40% (Figure 2).

Slaughter capacity before the coronavirus pandemic was assumed by experts to be slightly above 100%. Therefore slaughter companies competed for pigs and hardly had buyer power. Moreover, possible market power of slaughterhouse companies was balanced because many farmers are organized in producer organizations.

The competitiveness of the German meat sector is among others based on the efficiency of labor organization. Meat companies state that they do not find enough work forces in Germany and have to rely on migrant workers especially from Eastern Europe. Special agencies and labor intermediates recruit workers on behalf of German subcontracting companies. Subcontracting companies in turn employ the workers and offer service to the meat industry.

Subcontracting offers flexibility and low administrative burden for service demanding companies. They just buy the service they need. Subcontracting companies can shift their workforces from one company to another to balance out peaks and reduced workloads within a sector as well as between different sectors. The European Federation of Food Agriculture and Tourism Tarde Unions (EFFAT) estimates that approximately 80% of the labor in Germany's meat industry is carried out by migrant workers from Eastern Europe (EFFAT 2020).

Workers unions complain that the subcontracting system leads to lower costs in the meat industry because of an exploitation of migrant workers. Examples are wage disparities with workers directly employed, a higher number of working hours which even can exceed the legal limits or unpaid overtime. In addition, recruiting agencies would charge inappropriate recruiting fees and travel costs. Moreover, workers unions put poor accommodation in the context of the service contract system. Employees shared rooms and bathrooms and the hygienic status of the dwelling places are regarded as very poor. Subcontracting companies would directly or indirectly act as landlords and charge excessive rents for the poor accommodation (EFFAT 2020). A report on the results of a surveillance operation conducted by the occupational health and safety administration of the Federal state North-Rhine Westphalia provides empirical evidence for these complains (MAGS, 2019). Still it is contentious whether or not the results are representative and to what extent the meat industry and/or the subcontractors benefit from the system.

In any case, working and accommodation conditions fostered the spreading of the virus in the meat sector. According to our research especially the following factors are relevant:

• Low temperature and ventilation systems in the meat cutting and processing areas of factories;

• Little distance between workplaces especially in the meat cutting sections;

• Sending workers of the same accommodation to different plants;

• Using mini buses for transport between accommodations and workplace that do not allow for the necessary minimal distance between the employees; and

• Poor hygienic conditions in accommodations and lack of opportunities for social distance.

Moreover it is assumed that subcontractors put pressure on workers so that they do not stay home even if they feel ill and thus infected persons with a low level of symptoms spread the virus during working hours.

THE HISTORY

The high infection risk becomes evident through Corona outbreaks in the meat sector. Relevant events can be summarized as follows:

• Calendar week 19/2020: a massive COVID-19 outbreak in a slaughterhouse of the Westfleisch Company with a capacity of about 55,000 pigs per week led to a shut-down. After about 10 days, the plant reopened with a reduced capacity in the initial phase. The shut-down did not lead to lasting disturbances on the market due to the limited time span and the ability of neighboring premises to take on additional slaughtering;

• Calendar week 25/2020: Germany’s biggest slaughterhouse with a capacity of about 130,000 pigs a week was closed because of corona outbreaks. This single plant of the Tönnies Group covers about 15% of the total German pig slaughter capacity. After about four weeks it was put into operation again and slowly increased the number of slaughtering. In October 2020, the official permit was still limited to about 90,000 pigs a week which is 40,000 pigs or 30% less than before the crisis. The capacity loss could and cannot be offset by other of slaughterhouses; and

• From calendar week 40/2020 onwards outbreaks in two other slaughterhouses further reduced the slaughter capacity in Germany by about 80,000 pigs a week.

Hygiene concepts had to be developed for all slaughterhouses and had to be approved by health authorities. Concepts are specific for every plant, however measures to reduce the infection risk are comparable: widening the space between employees and/or installing Plexiglas shields and a high density of testing is mandatory. While a minimum of two tests a week is prescribed by law, the Westfleisch company requires the conduct of daily tests for people working in the slaughtering and meat areas. The Tönnies Group has installed high performance HEPA filter in the plant that had been closed in May in order to prevent the spreading of the virus through the ventilation system.

According to expert opinions, capacities in the slaughterhouses not mentioned above had to be reduced by about 4% to 5% or about 30,000 pigs a week to meet the hygienic requirements. Altogether, Germany’s pig slaughtering capacity in October 2020 is estimated to be about 150,000 pigs a week of 15% lower compared to the pre-corona period.

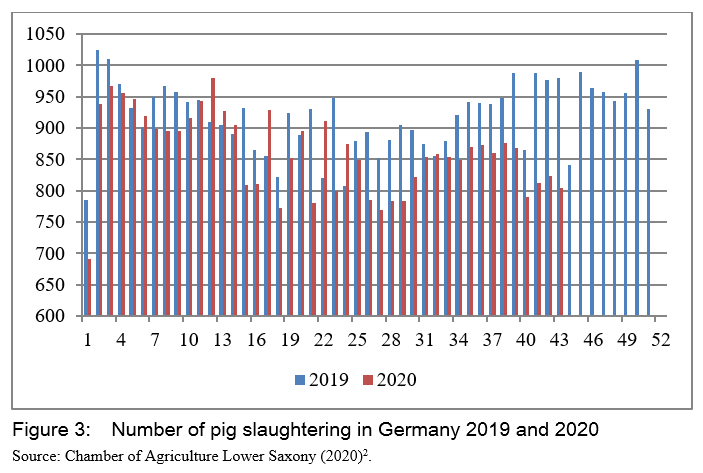

Figure 3 compares the number of slaughtering in Germany in 2019 and 2020. It gives evidence of the reduced potential of the sector.

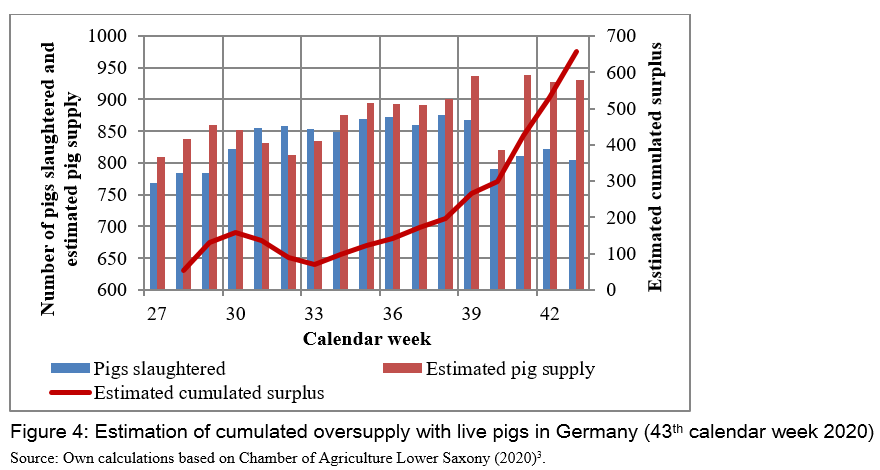

Due to stock reduction, indigenous production in Germany is estimated to be lower than in 2019. Moreover, imports of live animals decreased and exports increased. However, these developments did not balance the reduction of the slaughter capacity, so that a so called “pig-jam” emerged (see Figure 4). The exact extent of the “pig-jam” is currently unknown because no reliable data regarding import and export of live animals and indigenous production are available. Estimations differ between about 500,000 and 630,000 pigs (calendar week 43/2020)

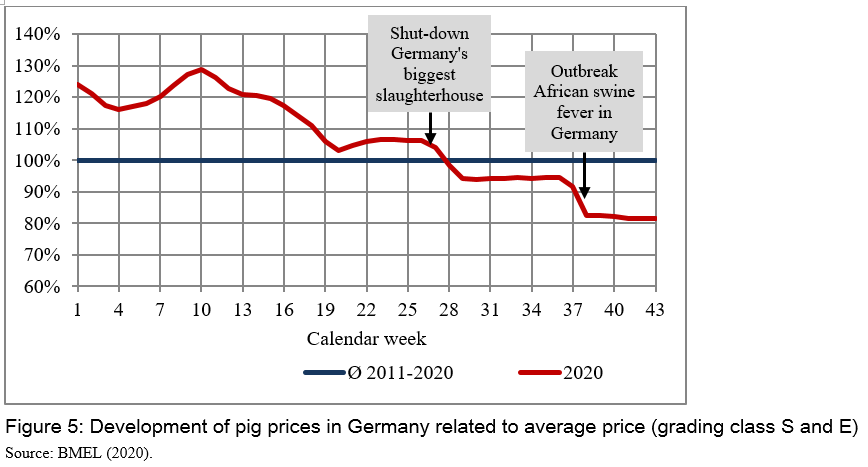

After the shut-down of Germany’s biggest slaughterhouse, the surplus of live animals resulted in a drop of pig prices by about 12% (compare Figure 5). For farmers it became increasingly difficult to sell their pigs as – compared to the slaughterhouse capacity – the market is oversupplied.

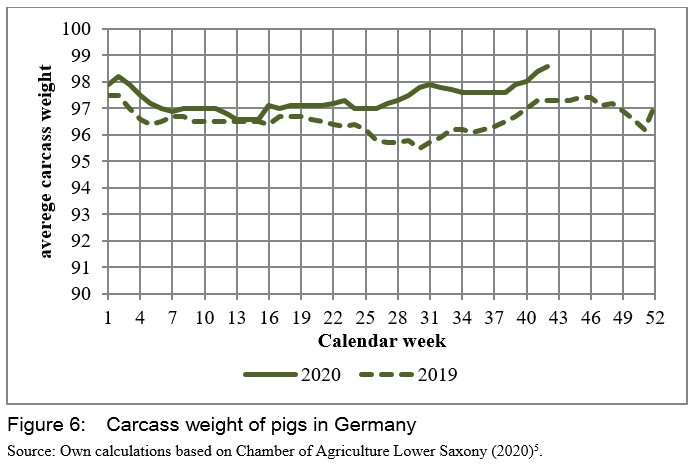

In addition to the price fall for a standardized quality, experts guess that farmers were confronted with a downgrading of the carcass quality because of increasing weight (Figure 6) and the actual price cut is even higher.

But farmers do not only face price drops: Pigs ready for slaughter have to remain on farms leading to additionally feeding costs. Moreover, the pigs block stables which cannot be used for further production with a loss of profits as a consequence. Pig producers having long term delivery contracts with slaughterhouse companies are not affected by delivery problems as slaughterhouses comply with the contract and the obligation to take over the pigs. This in turn means that producers without contracts alone have to bear the adverse consequences resulting from delayed deliveries.

The COVID-19 effects were intensified by the outbreak of African swine fever in Germany and the subsequent export restrictions especially to Asian countries. This led to an additional price cut of 13% and aggravated the situation of farmers (Figure 5).

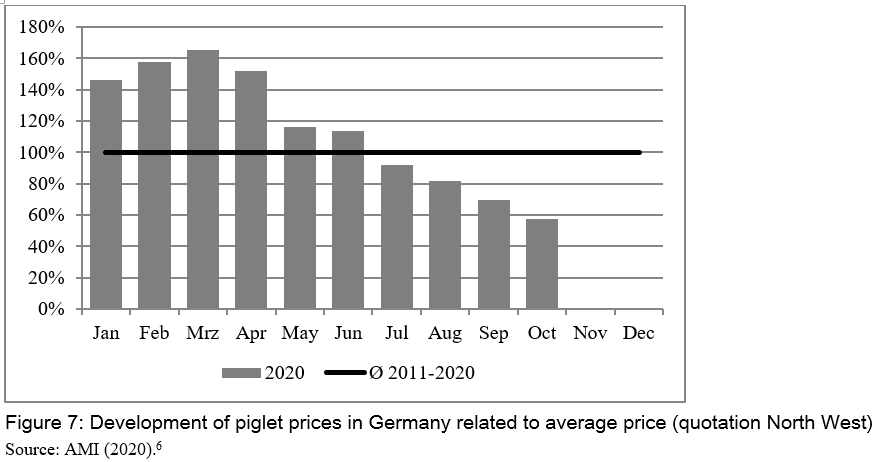

Falling prices for slaughter pigs led to a price cut for piglets to an even greater extent. In total piglet prices fell between June and October 2020 from about 15% above average to more than 40% below (Figure 7).

OUTLOOK

Regarding pig production, short term adjustment of quantity to prices is not possible, as present supply is determined by the insemination of sows about a year ago. As a result it will take until the mid and late 2021 before the low prices can result in lower supply.

Increasing the speed of the slaughter belts to the extent before the crisis is currently impeded by the restricted capacity in the meat cutting sections of the plants due to additional hygienic requirements. To increase capacity the Tönnies Group installed additional cutting belts in a building once used for cattle. However, currently the new capacities are not approved by the administration and the slaughter capacity in Germany’s biggest slaughterhouse is still restricted.

Increasing the number of slaughtering and processing by working on Sundays is technically possible, but experts assume a lack of work forces because of the COVID-19 crisis and an intended change in working conditions for the meat industry. The coronavirus pandemic and the infections in slaughterhouses fueled the public discussion about working and accommodation conditions and increased pressure on politicians to adjust the legal framework. The government reacted and announced a new law (Arbeitsschutzkontrollgesetz, Working Conditions Control Act). Service contracts shall be forbidden and the subcontracting system shall be abolished in the meat industry from 2021 onwards, because they are supposed to contribute to inappropriate working conditions and accommodation. The consultation process between the different ministries is not finalized and the exact legal rules are not known yet. Still the meat industry already reacted in advance and committed not to rely on service contracts from 2021 onwards. Experts mentioned several reasons why this development can lead to a shortage of workers in the meat industry:

• Service providing companies react on the danger of losing their business basis by withdrawing their workforce from the meat industry and offering service to other sectors;

• The meat industry has to yet develop its own system of recruiting labor forces;

• Stricter control of working hours may not be in the interest of all workers. Given that staying in Germany means staying away from family and friends their might be rather interested in earning as much money as possible in a given period of time and therefore look for other working opportunities; and

• Travel restrictions due to the coronavirus pandemic hamper recruiting workforce in East European countries.

In addition, working conditions in the meat industry are harsh and it might be assumed that the infection risk is higher than in other sectors so that there is an incentive for changing.

In total there seem to be two limiting factors in the meat sector: (1) the slaughter and meat cutting capacity and (2) a shortage of labor. By now, no strategy has been developed to solve the problem. The fear is that the surplus of pigs adds up to more than 1,000,000 pigs at the end of 2020 (Figure 8).

In the context of the coronavirus pandemic and the breakout of the African swine fever piglet prices dropped corresponding to pig prices, but to a greater extent. The fall in price coincides with a change in the legal framework for keeping sows and piglets which leads to an increase in animal welfare standards and requires additional investments in stables. Against the background of low piglet prices and high investments it is assumed that a relevant share of piglet producers will leave the sector and by that threaten the basis of German pig production. One expert called the COVID-19 impact a contribution to a severe violation of the backbone of the German pig production and processing.

REFERENCES

AMI, Agrarmarkt Informations-Gesellschaft (2020). AMI Markt Bilanz. Vieh und Fleisch 2020. Daten | Fakten | Entwicklungen. Deutschland | EU | Welt.

BMEL Bundesministerium für Ernährung und Landwirtschaft / Federal Ministry of Food and Agriculture ((2020). Schlachtpreise für Schweine (https://www.bmel-statistik.de/fileadmin/daten/PMT-0100501-2011.xlsx; Accessed 13 November 2020).

Bongaerts, R. (2001). Verbesserung der Schlachthofstruktur in der Bundesrepublik Deutschland: unter besonderer Berücksichtigung eines Strukturkrisenkartells. Lang.

Destatis Deutsches Statistisches Bundesamt / German Federal Statistical Office (2020). Statistisches Bundesamt. Genesis online (https://www-genesis.destatis.de/genesis/online); Accessed 13 November 2020).

EFFAT European Federation of Food Agriculture and Tourism Tarde Unions (2020). Covid-19 outbreaks in slaughterhouses and meat processing plants EFFAT Report (2020) (https://effat.org/wp-content/uploads/2020/06/EFFAT-Report-Covid-19-outbr... Accesses 13 November 2020).

Hungerkamp, M. (2020). Schlachtbranche - ISN-Schlachthofranking: Tönnies baut Marktmacht weiter aus (https://www.agrarheute.com/management/agribusiness/isn-schlachthofrankin... Accessed 13 November 2020);

MAGS Ministerium für Arbeit, Gesundheit und Soziales des Landes Nordrhein-Westfalen / Ministry for Labour, Helath and Social Affairs of North Rhine-Westphalia (2019). Überwachungsaktion. „Faire Arbeit in der Fleischindustrie“. Abschlussbericht https://www.mags.nrw/sites/default/files/asset/document/191220_abschluss... Accessed 12 November 2020.

COVID-19 – Impact on the Meat Sector in Germany

ABSTRACT

Working conditions in slaughterhouses as well as the accommodation of the employees are regarded as reasons for the specific susceptibility of the slaughterhouse and meat processing sector for coronavirus infections. After massive breakouts in German meat plants, work processes and work places had to be adjusted in order to reduce infection risks. Some slaughterhouses – among them the biggest in Germany – were even temporarily closed until they had developed and implemented an appropriate and administratively approved concept for risk reduction. Currently (November 2020), the German pig meat sector in particular, is affected by the Corona pandemic, while the impact on cattle and poultry is low. The adaption of slaughtering and meat cutting processes to the COVID-19 risk situation resulted in an estimated capacity reduction of about 15% compared to the pre-coronavirus period. As a consequence, slaughtering and meat cutting is a new and limiting bottleneck in the pig meat value chain. Reduction of imports and an increase of exports of live animals could reduce, but, not eliminate a surplus of live pigs. In October 2020, the number of pigs waiting to be slaughtered is estimated at approximately 500,000 to 630,000. Due to the surplus of live animals, pig prices in Germany dropped by about 12%. But farmers do not only face the price drop: Pigs ready for slaughter have to remain on farms leading to additional feeding costs. Moreover, farmers face additional price cuts if pigs exceed the ideal weight and lose profits because they cannot use their stables for further production. The COVID-19 effects were intensified by the outbreak of African swine fever in Germany and the subsequent export restrictions. This led to an additional price cut of 13% and aggravated the situation of German producers of fattening pigs and piglets. However, a short term adjustment of production quantity to prices is not possible, as present supply is determined by the insemination of sows about a year ago. As a result, it will take until the mid and late 2021 before the low prices can result in lower supply. Currently no sectoral strategy is implemented to deal with the inevitable oversupply of live pigs ready to be slaughtered.

Keywords: COVID-19, Slaughterhouse Sector, Pig Value Chain.

INTRODUCTION

The coronavirus pandemic confronts Germany’s supply systems for fast moving consumer goods (FMCG) with major challenges. In general, these challenges were met without relevant gaps in consumer supply. Retailers and processors re-organized their sourcing and adjusted production volumes. As a result, just toilet paper and flour packages for household use were temporarily scarce.

While the coronavirus pandemic hardly impacted the availability of FMCG, some food value chains were severely affected.

• Fruit and vegetable value chains: These chains deal with perishable goods and goods with an optimal harvesting time. Therefore, they are dependent on a smooth functioning of the production and processing chain in order to realize their value creation potential. Once the production is started, frictions in value chains can hardly be balanced by holding up or accelerating the process. The pandemic especially affected the availability of workforces during harvest time. In normal years, a considerable share of the staff for harvesting is hired in Eastern European countries because the German labor market does not provide a sufficient number of workers willing to carry out these jobs at the given payment. However, in 2020, just a limited number of migrant workers were available due to travel restrictions. As a consequence parts of fruits and vegetables were not picked.

• Meat value chains: In a similar way meat value chains are prone to disturbances because live animals loose quality and value if they are not slaughtered at the optimal time. Moreover, delays in slaughtering leads to additional costs because the animals have to be fed and block stable capacity for further production. In the coronavirus pandemic the slaughtering and cutting turned out to be the bottleneck in the value chain because of a high number of infections.

This paper deals with the impact of COVID-19 on the meat value chain in Germany. It is concentrated on the pigs as the pandemic by now does not have considerable impact in the area of cattle and poultry. It describes the specific susceptibility of slaughterhouses for infections, the impact of risk reducing measures on the slaughter capacity and the resulting effects on the upstream sector.

Expert interviews as well as statistics and reports in specialized agricultural and food media form the basis of the analysis. Expert interviews are necessary to point to relevant effects, to explain the consequences, to make sense of statistics and to fill gaps that are not covered by statistics. Moreover, adjustments of the legal framework are planned and not entered into force so that the effects can only be estimated. However, we recognize that experts may have vested interests. That is why we tried to substantiate their statements by cross validating them through the help of other experts, through our own expertise and through available statistics.

SOME BACKGROUND INFORMATION

In total, Germany’s 21,400 pig farmers kept about 26 million pigs and produced about 51.8 million slaughter pigs in 2019. Nearly half of the animals are kept on farms with more than 2,000 pigs while the share of the respective pig farmers amounts for less than 15% (Table 1). These farms are especially dependent on pig production and the development of the pig market.

The German pig slaughtering sector is highly concentrated with a concentration rate of the three most relevant companies (CR3) close to 60%. The biggest company, the Tönnies Group, accounts for about a third of overall slaughtering (Figure 1). The big companies are integrated downstream that combine slaughtering, meat cutting and meat processing. They run big slaughterhouses and the shut-down of one individual slaughterhouse can have severe impact on the whole market.

In the 1990s, the German slaughter sector faced a severe crisis. Overcapacities resulted in intense price competition and as a consequence several companies faced serious financial situations. Against this background, a structural crisis cartel was prepared in order to reduce capacities by joint action (Bongaerts 2001). However, the structural crisis cartel did not enter into force and the slaughterhouse sector recovered based on company takeovers, mergers, closure of unprofitable sites and on an increase of German pig production and imports of slaughter pigs. Within 25 years, more precisely between 1994 and 2019, the number of pig slaughtering in Germany increased from about 37m to 52m by approximately 40% (Figure 2).

Slaughter capacity before the coronavirus pandemic was assumed by experts to be slightly above 100%. Therefore slaughter companies competed for pigs and hardly had buyer power. Moreover, possible market power of slaughterhouse companies was balanced because many farmers are organized in producer organizations.

The competitiveness of the German meat sector is among others based on the efficiency of labor organization. Meat companies state that they do not find enough work forces in Germany and have to rely on migrant workers especially from Eastern Europe. Special agencies and labor intermediates recruit workers on behalf of German subcontracting companies. Subcontracting companies in turn employ the workers and offer service to the meat industry.

Subcontracting offers flexibility and low administrative burden for service demanding companies. They just buy the service they need. Subcontracting companies can shift their workforces from one company to another to balance out peaks and reduced workloads within a sector as well as between different sectors. The European Federation of Food Agriculture and Tourism Tarde Unions (EFFAT) estimates that approximately 80% of the labor in Germany's meat industry is carried out by migrant workers from Eastern Europe (EFFAT 2020).

Workers unions complain that the subcontracting system leads to lower costs in the meat industry because of an exploitation of migrant workers. Examples are wage disparities with workers directly employed, a higher number of working hours which even can exceed the legal limits or unpaid overtime. In addition, recruiting agencies would charge inappropriate recruiting fees and travel costs. Moreover, workers unions put poor accommodation in the context of the service contract system. Employees shared rooms and bathrooms and the hygienic status of the dwelling places are regarded as very poor. Subcontracting companies would directly or indirectly act as landlords and charge excessive rents for the poor accommodation (EFFAT 2020). A report on the results of a surveillance operation conducted by the occupational health and safety administration of the Federal state North-Rhine Westphalia provides empirical evidence for these complains (MAGS, 2019). Still it is contentious whether or not the results are representative and to what extent the meat industry and/or the subcontractors benefit from the system.

In any case, working and accommodation conditions fostered the spreading of the virus in the meat sector. According to our research especially the following factors are relevant:

• Low temperature and ventilation systems in the meat cutting and processing areas of factories;

• Little distance between workplaces especially in the meat cutting sections;

• Sending workers of the same accommodation to different plants;

• Using mini buses for transport between accommodations and workplace that do not allow for the necessary minimal distance between the employees; and

• Poor hygienic conditions in accommodations and lack of opportunities for social distance.

Moreover it is assumed that subcontractors put pressure on workers so that they do not stay home even if they feel ill and thus infected persons with a low level of symptoms spread the virus during working hours.

THE HISTORY

The high infection risk becomes evident through Corona outbreaks in the meat sector. Relevant events can be summarized as follows:

• Calendar week 19/2020: a massive COVID-19 outbreak in a slaughterhouse of the Westfleisch Company with a capacity of about 55,000 pigs per week led to a shut-down. After about 10 days, the plant reopened with a reduced capacity in the initial phase. The shut-down did not lead to lasting disturbances on the market due to the limited time span and the ability of neighboring premises to take on additional slaughtering;

• Calendar week 25/2020: Germany’s biggest slaughterhouse with a capacity of about 130,000 pigs a week was closed because of corona outbreaks. This single plant of the Tönnies Group covers about 15% of the total German pig slaughter capacity. After about four weeks it was put into operation again and slowly increased the number of slaughtering. In October 2020, the official permit was still limited to about 90,000 pigs a week which is 40,000 pigs or 30% less than before the crisis. The capacity loss could and cannot be offset by other of slaughterhouses; and

• From calendar week 40/2020 onwards outbreaks in two other slaughterhouses further reduced the slaughter capacity in Germany by about 80,000 pigs a week.

Hygiene concepts had to be developed for all slaughterhouses and had to be approved by health authorities. Concepts are specific for every plant, however measures to reduce the infection risk are comparable: widening the space between employees and/or installing Plexiglas shields and a high density of testing is mandatory. While a minimum of two tests a week is prescribed by law, the Westfleisch company requires the conduct of daily tests for people working in the slaughtering and meat areas. The Tönnies Group has installed high performance HEPA filter in the plant that had been closed in May in order to prevent the spreading of the virus through the ventilation system.

According to expert opinions, capacities in the slaughterhouses not mentioned above had to be reduced by about 4% to 5% or about 30,000 pigs a week to meet the hygienic requirements. Altogether, Germany’s pig slaughtering capacity in October 2020 is estimated to be about 150,000 pigs a week of 15% lower compared to the pre-corona period.

Figure 3 compares the number of slaughtering in Germany in 2019 and 2020. It gives evidence of the reduced potential of the sector.

Due to stock reduction, indigenous production in Germany is estimated to be lower than in 2019. Moreover, imports of live animals decreased and exports increased. However, these developments did not balance the reduction of the slaughter capacity, so that a so called “pig-jam” emerged (see Figure 4). The exact extent of the “pig-jam” is currently unknown because no reliable data regarding import and export of live animals and indigenous production are available. Estimations differ between about 500,000 and 630,000 pigs (calendar week 43/2020)

After the shut-down of Germany’s biggest slaughterhouse, the surplus of live animals resulted in a drop of pig prices by about 12% (compare Figure 5). For farmers it became increasingly difficult to sell their pigs as – compared to the slaughterhouse capacity – the market is oversupplied.

In addition to the price fall for a standardized quality, experts guess that farmers were confronted with a downgrading of the carcass quality because of increasing weight (Figure 6) and the actual price cut is even higher.

But farmers do not only face price drops: Pigs ready for slaughter have to remain on farms leading to additionally feeding costs. Moreover, the pigs block stables which cannot be used for further production with a loss of profits as a consequence. Pig producers having long term delivery contracts with slaughterhouse companies are not affected by delivery problems as slaughterhouses comply with the contract and the obligation to take over the pigs. This in turn means that producers without contracts alone have to bear the adverse consequences resulting from delayed deliveries.

The COVID-19 effects were intensified by the outbreak of African swine fever in Germany and the subsequent export restrictions especially to Asian countries. This led to an additional price cut of 13% and aggravated the situation of farmers (Figure 5).

Falling prices for slaughter pigs led to a price cut for piglets to an even greater extent. In total piglet prices fell between June and October 2020 from about 15% above average to more than 40% below (Figure 7).

OUTLOOK

Regarding pig production, short term adjustment of quantity to prices is not possible, as present supply is determined by the insemination of sows about a year ago. As a result it will take until the mid and late 2021 before the low prices can result in lower supply.

Increasing the speed of the slaughter belts to the extent before the crisis is currently impeded by the restricted capacity in the meat cutting sections of the plants due to additional hygienic requirements. To increase capacity the Tönnies Group installed additional cutting belts in a building once used for cattle. However, currently the new capacities are not approved by the administration and the slaughter capacity in Germany’s biggest slaughterhouse is still restricted.

Increasing the number of slaughtering and processing by working on Sundays is technically possible, but experts assume a lack of work forces because of the COVID-19 crisis and an intended change in working conditions for the meat industry. The coronavirus pandemic and the infections in slaughterhouses fueled the public discussion about working and accommodation conditions and increased pressure on politicians to adjust the legal framework. The government reacted and announced a new law (Arbeitsschutzkontrollgesetz, Working Conditions Control Act). Service contracts shall be forbidden and the subcontracting system shall be abolished in the meat industry from 2021 onwards, because they are supposed to contribute to inappropriate working conditions and accommodation. The consultation process between the different ministries is not finalized and the exact legal rules are not known yet. Still the meat industry already reacted in advance and committed not to rely on service contracts from 2021 onwards. Experts mentioned several reasons why this development can lead to a shortage of workers in the meat industry:

• Service providing companies react on the danger of losing their business basis by withdrawing their workforce from the meat industry and offering service to other sectors;

• The meat industry has to yet develop its own system of recruiting labor forces;

• Stricter control of working hours may not be in the interest of all workers. Given that staying in Germany means staying away from family and friends their might be rather interested in earning as much money as possible in a given period of time and therefore look for other working opportunities; and

• Travel restrictions due to the coronavirus pandemic hamper recruiting workforce in East European countries.

In addition, working conditions in the meat industry are harsh and it might be assumed that the infection risk is higher than in other sectors so that there is an incentive for changing.

In total there seem to be two limiting factors in the meat sector: (1) the slaughter and meat cutting capacity and (2) a shortage of labor. By now, no strategy has been developed to solve the problem. The fear is that the surplus of pigs adds up to more than 1,000,000 pigs at the end of 2020 (Figure 8).

In the context of the coronavirus pandemic and the breakout of the African swine fever piglet prices dropped corresponding to pig prices, but to a greater extent. The fall in price coincides with a change in the legal framework for keeping sows and piglets which leads to an increase in animal welfare standards and requires additional investments in stables. Against the background of low piglet prices and high investments it is assumed that a relevant share of piglet producers will leave the sector and by that threaten the basis of German pig production. One expert called the COVID-19 impact a contribution to a severe violation of the backbone of the German pig production and processing.

REFERENCES

AMI, Agrarmarkt Informations-Gesellschaft (2020). AMI Markt Bilanz. Vieh und Fleisch 2020. Daten | Fakten | Entwicklungen. Deutschland | EU | Welt.

BMEL Bundesministerium für Ernährung und Landwirtschaft / Federal Ministry of Food and Agriculture ((2020). Schlachtpreise für Schweine (https://www.bmel-statistik.de/fileadmin/daten/PMT-0100501-2011.xlsx; Accessed 13 November 2020).

Bongaerts, R. (2001). Verbesserung der Schlachthofstruktur in der Bundesrepublik Deutschland: unter besonderer Berücksichtigung eines Strukturkrisenkartells. Lang.

Destatis Deutsches Statistisches Bundesamt / German Federal Statistical Office (2020). Statistisches Bundesamt. Genesis online (https://www-genesis.destatis.de/genesis/online); Accessed 13 November 2020).

EFFAT European Federation of Food Agriculture and Tourism Tarde Unions (2020). Covid-19 outbreaks in slaughterhouses and meat processing plants EFFAT Report (2020) (https://effat.org/wp-content/uploads/2020/06/EFFAT-Report-Covid-19-outbr... Accesses 13 November 2020).

Hungerkamp, M. (2020). Schlachtbranche - ISN-Schlachthofranking: Tönnies baut Marktmacht weiter aus (https://www.agrarheute.com/management/agribusiness/isn-schlachthofrankin... Accessed 13 November 2020);

MAGS Ministerium für Arbeit, Gesundheit und Soziales des Landes Nordrhein-Westfalen / Ministry for Labour, Helath and Social Affairs of North Rhine-Westphalia (2019). Überwachungsaktion. „Faire Arbeit in der Fleischindustrie“. Abschlussbericht https://www.mags.nrw/sites/default/files/asset/document/191220_abschluss... Accessed 12 November 2020.