INTRODUCTION

Traditionally, agriculture is generally regarded as a high-risk industry because of its nature of being highly dependent on the climate and crop yields being easily influenced by adverse weather conditions (e.g., typhoons and rainstorms) and climate-associated damage (e.g., cold weather). The risk of agriculture management is not only related to production, but also related to price uncertainties. This is further heightened by economic and trade liberalization. The continuing tariffs reduction under trade liberalization has resulted in the increase of imports and increased the risk of declining and fluctuating prices of agricultural products. Hence, the main risks in agriculture are production and price risks. Production risk is associated with weather conditions leading to uncertainty in yield and quality, whereas price risk is due to price fluctuations as a result of the market economy. The revenue of farmers is affected by production and price. With the long-term trend of climate change and agricultural trade liberalization, the risks faced by farmers are likely to increase in the future.

In the past, most countries adopted market price support measures and input factor subsidies to protect farmer incomes and to stabilize their farming revenue. However, the use of these intervention policies has led to various adverse effects such as market mechanism distortions and resource allocation inefficiencies. Therefore, the amber box subsidies which will stimulate agriculture production are regulated in the Agriculture Agreement of the World Trade Organization (WTO) and resulted in the reduction of the aggregate measurement of support for agricultural production.

Market price support mechanisms could not be a permanent policy. Since Japan and South Korea have abolished the rice price support policy, Taiwan is also considering to reform its rice price support policy, which has been relied on to safeguard rice farmers' revenue. The green box subsidies are however not regulated to cut. These subsidies include government financial support for income insurance and income safety-net programs as well as natural disaster relief. These green box subsidies should provide alternative ways to ensuring farmers’ revenue.

In recent years, global climate change has become more extreme, resulting in more risks in agricultural production. It is insufficient to depend on government budgets for natural disaster relief because this approach has been unable to protect farmers’ production revenue or make up for natural disaster losses. Many countries, such as the United States, Japan, and China, have already implemented agricultural insurance mechanisms to maintain a satisfactory level of income from agricultural production. In the event of a catastrophe, such mechanisms can prevent having to mainly rely on government funding for recovery, which would pose a serious threat to the stability of the government’s finances. By virtue of this system, farmers’ awareness of disaster prevention and the risks involved in farm operations can be enhanced so that agricultural production can be adapted to local conditions. It would be an advancement to predevelop disaster management strategies to alleviate the negative impacts of disasters on rural economic life and stabilize the supply and demand of essential livelihood resources. However, the downside price risk of the agricultural product market receives less insurance coverage under traditional agricultural insurance policies, while the instability and downturn of agricultural product prices are crucial concerns of both farmers and policymakers, particularly after the signing of a free trade agreement, which will increase the downside price risk. Under this context, Korea began implementing a pilot agricultural revenue insurance scheme in 2015, and Japan is actively planning to implement an insurance scheme by 2018. This development demonstrates the necessity of agricultural revenue insurance.

Compared with other countries, Taiwan is lagging behind in the implementation of an effective crop insurance policy, although a pilot agricultural revenue insurance scheme for sugar apples has been in effect in 2017. The details of the scheme and operational model are innovative and comprehensive and thus could serve as a reference for other countries and for policy adjustments. Therefore, the pilot scheme is introduced and analyzed in this article.

STRUCTURE OF REVENUE INSURANCE PROGRAM

Role of insurance in the safety net

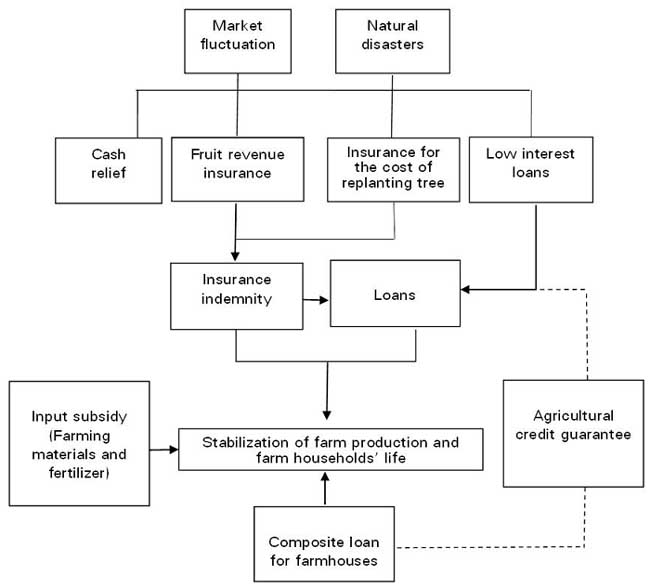

Insurance is an instrument for protecting income security. In Taiwan, the government currently provides a natural disaster relief system, policy-oriented loans, and input subsidies, and these polices are mutually reinforcing. Therefore, cash relief, low-interest loans, composite loans for farmhouse, and agricultural revenue insurance were integrated to construct Taiwan’s crop revenue safety net against the production risk from natural disasters and the price risk from market fluctuations. The aim of these policies is to ensure farm production and farmers’ life stability during periods of replanting growing and to manage the various risks that affect the stabilization of income; such risks include a lack of income during the period of replanting, natural disasters during growth period, and postharvest price collapses. The revenue safety net structure for sugar apples is depicted in Fig. 1.

Fig. 1. The revenue safety net structure of sugar apple

Design of sugar apple revenue insurance

In order to ensure the stabilization of farm production and farm households’ life for sugar apple farmers during periods of replanting after natural disasters or postharvest, the policy structure is designed to consist of two parts. First, fruit revenue insurance is the main insurance contract, in which the premium and indemnity are calculated referring to the methods used in by the United States and Korea, and using those that are available in Taiwan. Second, insurance for the cost of replanting tree is the subordinate insurance and is designed to ease the financial burden associated with replanting due to crops having been completely destroyed by a natural disaster, and this design is based on the experiences of Japan. In summary, the objectives of the sugar apple revenue insurance scheme are as follows:

< >To stabilize sugar apple farmers’ revenue during the period of growing including harvest;

To stabilize sugar apple farmers’ income during replanting after crops have been completely destroyed by a natural disaster; and

To understand how much the farmers’ perceive the revenue insurance and have willingness to pay toward the revenue insurance.According to the scheme of fruit revenue insurance and insurance for the cost of replanting trees, the structure of sugar apple insurance can be constructed as depicted in Fig. 2.

.jpg)

Fig. 2. The structure of sugar apple insurance

CONTENT OF SUGAR APPLE INSURANCE

Fruit revenue insurance for sugar apples

The basic concept of revenue insurance is that if the actual revenue falls below the base revenue, then the indemnity can be obtained. Because revenue is calculated on the basis of yield multiplied by price, the crucical things are as follows: (a) the data source for the yield and price, (b) the method for identifying the data, and (c) the baseline for determining the base price. Concurrently, the principle of the calculation is also important. It is that the measurement of the indemnity and premium must use the same definition and data source and maintain consistency in the computations.

Sugar apple harvests can be considered profitable for 15 years; thus, the calculation of the pure premium considers the losses caused by natural disasters during the 2001–2015 period, and the main goal of the revenue insurance is to maintain an appropriate income for this period.

In the calculation process, the yield of sugar apples produced by each farmer is difficult to calculate; therefore, it is necessary to combine the government’s open data on the yield of sugar apples from the Agricultural Statistics Yearbook in Taiwan and the data of yield per hectare disclosed by the unit of township. There are two main reasons for using the yield data at the township level. First, there are positive reasons for encouraging the promotion of risk management. If highly effective approaches to disaster prevention and cultivation management are implemented by individual farmers, any disaster would be mitigated and the farmers would receive a larger indemnity. Second, there are also negative reasons for avoiding the promotion of risk management, such as the problem of moral hazard. Furthermore, if there is lack of disaster prevention measures, farmers who are actually affected by a disaster cannot receive a larger indemnity.

Price data are mainly derived from Taipei Second Fruits and Vegetables Wholesale Market prices. Because the data are open and objective, inquiring about the data can be convenient and can reduce controversy. Because the data are not the selling prices offered by individual farmers, there are positive reasons for encouraging farmers to improve the quality of their goods and sell them at a fair price.

The actual revenue is the actual yield per hectare of each township in the current year multiplied by the weighted annual average wholesale price of the Taipei Second Fruits and Vegetables Wholesale Market. The base revenue is the base yield multiplied by the base price, where the base yield and base price are the simple average of the previous 3 years’ values rather than the Olympic average of the previous 5 years’ values, and the main purpose is to reflect the extreme weather and climate change in recent years. Outliers are incorporated into the calculation of the base value to narrow the gap between the base value and actual value, which can reduce the indemnity.

In addition, based on the weighted average original premium for each township, the insurance is designed to adopt a single rate to avoid the conflict of different premiums in different townships. In the future, if detailed data on individual farmers can be established, the premium will be adjusted according to the insurance status of the individual or township.

As mentioned, the basic definitions of revenue insurance indemnity and calculation of premium are summarized as follows:

1. Base revenue formula:

Base revenue per hectare = base price × base yield per hectare × insurance coverage;

Four levels of insurance coverage can be designed (85%, 90%, 95%, and 100% coverage) to represent the degree of revenue protection. The ranges of insurance coverage in the United States and Korea are 50%–85% and 60%–90%, respectively. For each country, the insurance is designed such that the ratio of the risk deductible should be selected by farmers to avoid moral hazard. However, the data used in this article do not correlate with individual farmers, and to ensure that revenues can be fully protected, the insurance coverage of 100% is listed as an option. Basically, farmers understand the corresponding principle that the higher the degree of revenue protection, the higher the premium will be.

2. Actual revenue formula:

Actual revenue = actual price × actual yield per hectare;

3. Insurance indemnity formula:

Indemnity = (base revenue per hectare − actual revenue per hectare) × insured area;

4. Trial calculation simulation:

Depending on the insurance rate, insurance coverage, sources of price data, and whether cash relief for climatic disasters is included in the actual revenue, various premium and insurance indemnity amounts can be obtained.

In the aforementioned definitions, the key variables and parameters for the calculation of the premium and indemnity must be repeatedly considered, including the yield, price, average value, insurance rate, and insurance coverage.

The per-hectare premiums for sugar apple revenue insurance are NT$52,303, NT$31,244, NT$20,700, and NT$13,424 for 100%, 95%, 90% and 85% insurance coverage, respectively. Depending on the financial burden and degree of revenue protection, farmers can select the most suitable premium for their needs. This would be an effective approach to building an insurance concept. To reduce the burden on farmers, the premium subsidy ratio could be 55% (50% provided by the central government, 5% paid by the local government), only the remaining 45% is paid by farmers, and it would be of great advantage for farmers to purchase insurance.

Revenue insurance differs from natural disaster insurance. Depending on the degree of damage caused by natural disasters (such as typhoons and rainstorms) over the years, the per-hectare premium for natural disaster insurance can reach NT$57,459 for 100% coverage. The premium for natural disaster insurance, however, is significantly higher than that for revenue insurance, mainly because a decrease in yield leads to an increase in price; hence, the loss of actual revenue is less than the loss of yield. Hence, revenue insurance has a lower premium and accounts for the price risk; thus, promoting this type of insurance in the future would be invaluable for protecting farmer incomes.

Insurance for the cost of replanting trees (tree cost insurance) for sugar apples

Tree cost insurance is a type of property insurance specifically designed to provide a guaranteed income for farmers in replanting periods following a natural disaster. It is also considered a form of attached insurance intended to provide insurance coverage for trees. However, each plant must be registered, which requires detailed data on plant growth and management. To avoid moral hazard, the data should be established at least when the plants are first insured.

The rule of tree cost insurance is that it is a form of attached insurance for revenue insurance, meaning that revenue insurance is the main insurance contract and tree cost insurance can be selected as an insurance rider. The qualification for indemnity is that the sugar apple trees are completely collapsed and dead and must be replanted because they have been destroyed by natural disaster. The premium and insurance amount are measured by NT$51 million per hectare on the basis of the total cost of replanting trees over a 3-year period.

Suppose that the replanted area of sugar apple trees following a natural disaster is 5%, in addition to 15% for operating costs; the annual premium per hectare is then calculated to be NT$5,000. The annual loss adjustment expense is NT$8.5 million for 3 consecutive years, but must be annually attached in a fruit revenue insurance policy for sugar apples for the indemnity to be obtained.

Planning the operational model

The government has a critical role in providing public support; because of the considerable management costs and insurance indemnity for systemic risk in agricultural insurance, the private sector is deterred from participating in it. The government can play an active role in providing reinsurance, subsidizing farmers’ insurance premiums, subsidizing management costs for the private sector, establishing public–private partnerships, and assisting in establishing and providing information. Therefore, the revenue insurance is provided with the features of government-sponsored insurance.

The Agricultural Development Act of Taiwan notes the following:

The government shall initiate an agricultural insurance program to secure farmers' income, to stabilize rural communities and to make full use of agricultural resources. Before the agricultural insurance program is enacted into law, the central competent authority shall establish regulations in accordance with which agricultural insurance program by districts, categorization and stage may be implemented on a trial basis. All farmers within the same district and business operation line may participate in the program. Farmers' organizations may be commissioned to handle the said insurance program. The commissioned farmers’ organization handling the insurance program shall receive rewards and have the assistance or support from the government. (Article 58)

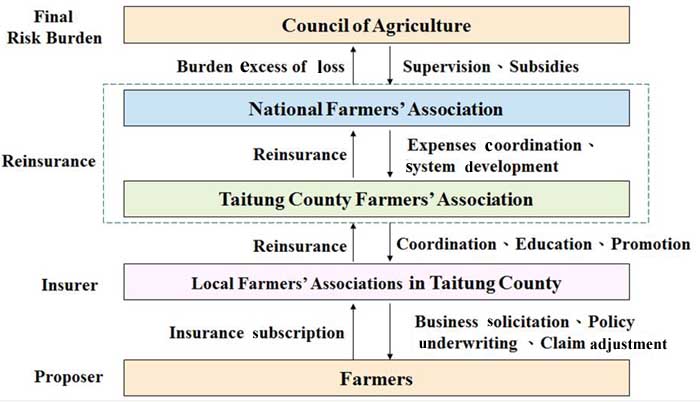

Furthermore, the Farmers Association Act of Taiwan prescribes that farmers’ associations are authorized to “accepting commissioned requests to handle farming insurance business” (Article 4, Subparagraph 12). Therefore, with the support of the law, the coverage, underwriting, and indemnity of sugar apple revenue insurance designed in this article are based on the system of the Farmers’ Association, which is organized into three levels (township, county, and national), and the risk-sharing mechanism of the government. This means that the indemnity is shared by the three levels of the Farmers’ Associations with a loss ratio of less than 100%, where 60% is shared by township-level Farmers’ Associations, while the remaining 40% is transferred to county- and national-level Farmers’ Associations and divided equally between them. The indemnity is transferred to the government, which shoulders the final burden with a loss ratio of more than 100%. Ten percent of the insurance premium is allocated to cover the operating expenses of the Farmers’ Associations, but the loss ratio that must be shared is 100%, and that is expressed as 10% of the risk being shared by the Farmers’ Associations. Meanwhile, the role of county- and national-level Farmers’ Associations is to provide reinsurance—but not coinsurance—because the roles of these institutions are noninsurers. The operational model is depicted in Fig. 3.

Fig. 3. The operation model of sugar apple revenue insurance

Farmers’ Associations are distributed throughout Taiwan, and these institutions tend to interact closely with farmers and would thus have a channel advantage. Therefore, the Farmers’ Associations assist in the promotion of agricultural insurance, coverage, disaster reporting, disaster survey coordination, insurance indemnity, and communication with farmers, and the farmers can purchase insurance or apply for indemnity at the nearest Farmers’ Association. The Council of Agriculture (COA) is the competent authority for enforcing agricultural insurance, and it is responsible for supervising and managing the agricultural insurance fund. The sources of funds would be as follows: (a) The COA compiles the annual budget support for premium subsidies, which are included in the agricultural insurance fund; (b) the insurance premiums paid by the farmers, where after the management expenses and all costs for the current year have been deducted, the entire balance is to be deposited as a reserve, and rapidly accumulating reserves are to be used for future compensations.

It suggests that the agriculture insurance fund should be the core of agricultural insurance operating mechanisms in the future, which is in response to the premium pricing, insurance policy design, catastrophic underwriting, domestic and overseas reinsurance, and insurance indemnity. Moreover, the risk diversification mechanism should be established for coinsurance, reinsurance, and transferring the indemnity to the government when losses exceed the risk-assumption limits of the agriculture insurance fund.

Features of revenue insurance

Basically, the insurance indemnity and premium are determined by the difference between the base revenue and actual revenue, where the price data are wholesale market prices, and the yield data are from the Agricultural Statistics Yearbook. The data for calculating the insurance indemnity and insurance premium should have consistency, transparency, and credibility. The various insurance coverage rates are considered to provide different options for farmers.

In summary, the features of revenue insurance designed in this scheme are as follows:

1. Completeness of vision: the design could be a response to the trend of climate change, agricultural trade liberalization and the traditional subsidy policy, which has been transformed to conform to WTO regulations, as well as foresights regarding policy implications.

2. Government-sponsored insurance: the design does not follow the model of commercial insurance, and the agricultural insurance is piloted by Taiwan’s Farmers’ Associations on the basis of the Agricultural Development Act. In line with the model of livestock insurance, insurance coverage is provided by the Farmers’ Associations at all three levels, the insurance premium is subsidized by the government, and the final excess loss is undertaken by the government.

3. Financial stabilization: the design is based on the economic life of sugar apple plants being 15 years from planting, and on maintaining long-term financial balance.

4. Complete protection: regardless of the price decline or impaired yield of sugar apples, the design would be aimed at guaranteeing the final revenue.

5. Reducing the cost of insurance: the design avoids the cost and disruption of exploration.

6. Locally identified yields: the design considers regional yields and open market prices and is not necessary aimed at filling in the individual actual yields and sales prices. This would contribute to production management and quality improvement.

7. The main insurance contract and attached insurance: in addition to the main contract of fruit revenue insurance, tree cost insurance, which is an attached insurance, can be offered during the replanting period.

8. Various options: different options for protection insurance premiums or base revenues can be provided to farmers, such as different levels of insurance coverage and whether the insurance is included in the natural disaster relief.

9. Information disclosure: the information is transparent and thus can reduce controversy. This would be convenient for underwriting and insurance indemnity calculations, and can be inquired and insured by using a software application (e.g., a mobile phone app).

10. Premium feedback: a dividend discount mechanism for the premium can be used to encourage farmers to purchase insurance.

CONCLUSION

In Taiwan, agricultural insurance has been a topic of discussion since 1956; however, the implementation of this type of insurance did not begin until the insurance policy for top-grafting sand pears was implemented in 2015, and its insurance rate remains low (less than 1% of planted areas) because it continues to follow the commercial insurance model. In 2016, a series of typhoons caused large-scale agricultural disasters. Following the presidential inauguration on May 20, 2016, and active reformation of the agricultural policy, the revenue insurance for sugar apples was designed and finalized. The implementation of revenue insurance for sugar apples is expected to be successful, but it is necessary to consider the number and arrangement of current policies, such as price support for each product, factor subsidies, the relief of production and marketing imbalances, natural disaster relief, and rules for redressing damage to farmers from agricultural imports, and to avoid the problems of overlapping subsidies and inequality. Clarifying the relationship between agricultural insurance and these subsidy policies would also be helpful. Such clarification could avoid placing a heavy financial burden on the government.

|

Date submitted: April 21, 2017

Reviewed, edited and uploaded: June 26, 2017

|

Design and Operation of Agricultural Revenue Insurance in Taiwan: The Case of Sugar Apple

INTRODUCTION

Traditionally, agriculture is generally regarded as a high-risk industry because of its nature of being highly dependent on the climate and crop yields being easily influenced by adverse weather conditions (e.g., typhoons and rainstorms) and climate-associated damage (e.g., cold weather). The risk of agriculture management is not only related to production, but also related to price uncertainties. This is further heightened by economic and trade liberalization. The continuing tariffs reduction under trade liberalization has resulted in the increase of imports and increased the risk of declining and fluctuating prices of agricultural products. Hence, the main risks in agriculture are production and price risks. Production risk is associated with weather conditions leading to uncertainty in yield and quality, whereas price risk is due to price fluctuations as a result of the market economy. The revenue of farmers is affected by production and price. With the long-term trend of climate change and agricultural trade liberalization, the risks faced by farmers are likely to increase in the future.

In the past, most countries adopted market price support measures and input factor subsidies to protect farmer incomes and to stabilize their farming revenue. However, the use of these intervention policies has led to various adverse effects such as market mechanism distortions and resource allocation inefficiencies. Therefore, the amber box subsidies which will stimulate agriculture production are regulated in the Agriculture Agreement of the World Trade Organization (WTO) and resulted in the reduction of the aggregate measurement of support for agricultural production.

Market price support mechanisms could not be a permanent policy. Since Japan and South Korea have abolished the rice price support policy, Taiwan is also considering to reform its rice price support policy, which has been relied on to safeguard rice farmers' revenue. The green box subsidies are however not regulated to cut. These subsidies include government financial support for income insurance and income safety-net programs as well as natural disaster relief. These green box subsidies should provide alternative ways to ensuring farmers’ revenue.

In recent years, global climate change has become more extreme, resulting in more risks in agricultural production. It is insufficient to depend on government budgets for natural disaster relief because this approach has been unable to protect farmers’ production revenue or make up for natural disaster losses. Many countries, such as the United States, Japan, and China, have already implemented agricultural insurance mechanisms to maintain a satisfactory level of income from agricultural production. In the event of a catastrophe, such mechanisms can prevent having to mainly rely on government funding for recovery, which would pose a serious threat to the stability of the government’s finances. By virtue of this system, farmers’ awareness of disaster prevention and the risks involved in farm operations can be enhanced so that agricultural production can be adapted to local conditions. It would be an advancement to predevelop disaster management strategies to alleviate the negative impacts of disasters on rural economic life and stabilize the supply and demand of essential livelihood resources. However, the downside price risk of the agricultural product market receives less insurance coverage under traditional agricultural insurance policies, while the instability and downturn of agricultural product prices are crucial concerns of both farmers and policymakers, particularly after the signing of a free trade agreement, which will increase the downside price risk. Under this context, Korea began implementing a pilot agricultural revenue insurance scheme in 2015, and Japan is actively planning to implement an insurance scheme by 2018. This development demonstrates the necessity of agricultural revenue insurance.

Compared with other countries, Taiwan is lagging behind in the implementation of an effective crop insurance policy, although a pilot agricultural revenue insurance scheme for sugar apples has been in effect in 2017. The details of the scheme and operational model are innovative and comprehensive and thus could serve as a reference for other countries and for policy adjustments. Therefore, the pilot scheme is introduced and analyzed in this article.

STRUCTURE OF REVENUE INSURANCE PROGRAM

Role of insurance in the safety net

Insurance is an instrument for protecting income security. In Taiwan, the government currently provides a natural disaster relief system, policy-oriented loans, and input subsidies, and these polices are mutually reinforcing. Therefore, cash relief, low-interest loans, composite loans for farmhouse, and agricultural revenue insurance were integrated to construct Taiwan’s crop revenue safety net against the production risk from natural disasters and the price risk from market fluctuations. The aim of these policies is to ensure farm production and farmers’ life stability during periods of replanting growing and to manage the various risks that affect the stabilization of income; such risks include a lack of income during the period of replanting, natural disasters during growth period, and postharvest price collapses. The revenue safety net structure for sugar apples is depicted in Fig. 1.

Fig. 1. The revenue safety net structure of sugar apple

Design of sugar apple revenue insurance

In order to ensure the stabilization of farm production and farm households’ life for sugar apple farmers during periods of replanting after natural disasters or postharvest, the policy structure is designed to consist of two parts. First, fruit revenue insurance is the main insurance contract, in which the premium and indemnity are calculated referring to the methods used in by the United States and Korea, and using those that are available in Taiwan. Second, insurance for the cost of replanting tree is the subordinate insurance and is designed to ease the financial burden associated with replanting due to crops having been completely destroyed by a natural disaster, and this design is based on the experiences of Japan. In summary, the objectives of the sugar apple revenue insurance scheme are as follows:

< >To stabilize sugar apple farmers’ revenue during the period of growing including harvest;

To stabilize sugar apple farmers’ income during replanting after crops have been completely destroyed by a natural disaster; and

To understand how much the farmers’ perceive the revenue insurance and have willingness to pay toward the revenue insurance.According to the scheme of fruit revenue insurance and insurance for the cost of replanting trees, the structure of sugar apple insurance can be constructed as depicted in Fig. 2.

Fig. 2. The structure of sugar apple insurance

CONTENT OF SUGAR APPLE INSURANCE

Fruit revenue insurance for sugar apples

The basic concept of revenue insurance is that if the actual revenue falls below the base revenue, then the indemnity can be obtained. Because revenue is calculated on the basis of yield multiplied by price, the crucical things are as follows: (a) the data source for the yield and price, (b) the method for identifying the data, and (c) the baseline for determining the base price. Concurrently, the principle of the calculation is also important. It is that the measurement of the indemnity and premium must use the same definition and data source and maintain consistency in the computations.

Sugar apple harvests can be considered profitable for 15 years; thus, the calculation of the pure premium considers the losses caused by natural disasters during the 2001–2015 period, and the main goal of the revenue insurance is to maintain an appropriate income for this period.

In the calculation process, the yield of sugar apples produced by each farmer is difficult to calculate; therefore, it is necessary to combine the government’s open data on the yield of sugar apples from the Agricultural Statistics Yearbook in Taiwan and the data of yield per hectare disclosed by the unit of township. There are two main reasons for using the yield data at the township level. First, there are positive reasons for encouraging the promotion of risk management. If highly effective approaches to disaster prevention and cultivation management are implemented by individual farmers, any disaster would be mitigated and the farmers would receive a larger indemnity. Second, there are also negative reasons for avoiding the promotion of risk management, such as the problem of moral hazard. Furthermore, if there is lack of disaster prevention measures, farmers who are actually affected by a disaster cannot receive a larger indemnity.

Price data are mainly derived from Taipei Second Fruits and Vegetables Wholesale Market prices. Because the data are open and objective, inquiring about the data can be convenient and can reduce controversy. Because the data are not the selling prices offered by individual farmers, there are positive reasons for encouraging farmers to improve the quality of their goods and sell them at a fair price.

The actual revenue is the actual yield per hectare of each township in the current year multiplied by the weighted annual average wholesale price of the Taipei Second Fruits and Vegetables Wholesale Market. The base revenue is the base yield multiplied by the base price, where the base yield and base price are the simple average of the previous 3 years’ values rather than the Olympic average of the previous 5 years’ values, and the main purpose is to reflect the extreme weather and climate change in recent years. Outliers are incorporated into the calculation of the base value to narrow the gap between the base value and actual value, which can reduce the indemnity.

In addition, based on the weighted average original premium for each township, the insurance is designed to adopt a single rate to avoid the conflict of different premiums in different townships. In the future, if detailed data on individual farmers can be established, the premium will be adjusted according to the insurance status of the individual or township.

As mentioned, the basic definitions of revenue insurance indemnity and calculation of premium are summarized as follows:

1. Base revenue formula:

Base revenue per hectare = base price × base yield per hectare × insurance coverage;

Four levels of insurance coverage can be designed (85%, 90%, 95%, and 100% coverage) to represent the degree of revenue protection. The ranges of insurance coverage in the United States and Korea are 50%–85% and 60%–90%, respectively. For each country, the insurance is designed such that the ratio of the risk deductible should be selected by farmers to avoid moral hazard. However, the data used in this article do not correlate with individual farmers, and to ensure that revenues can be fully protected, the insurance coverage of 100% is listed as an option. Basically, farmers understand the corresponding principle that the higher the degree of revenue protection, the higher the premium will be.

2. Actual revenue formula:

Actual revenue = actual price × actual yield per hectare;

3. Insurance indemnity formula:

Indemnity = (base revenue per hectare − actual revenue per hectare) × insured area;

4. Trial calculation simulation:

Depending on the insurance rate, insurance coverage, sources of price data, and whether cash relief for climatic disasters is included in the actual revenue, various premium and insurance indemnity amounts can be obtained.

In the aforementioned definitions, the key variables and parameters for the calculation of the premium and indemnity must be repeatedly considered, including the yield, price, average value, insurance rate, and insurance coverage.

The per-hectare premiums for sugar apple revenue insurance are NT$52,303, NT$31,244, NT$20,700, and NT$13,424 for 100%, 95%, 90% and 85% insurance coverage, respectively. Depending on the financial burden and degree of revenue protection, farmers can select the most suitable premium for their needs. This would be an effective approach to building an insurance concept. To reduce the burden on farmers, the premium subsidy ratio could be 55% (50% provided by the central government, 5% paid by the local government), only the remaining 45% is paid by farmers, and it would be of great advantage for farmers to purchase insurance.

Revenue insurance differs from natural disaster insurance. Depending on the degree of damage caused by natural disasters (such as typhoons and rainstorms) over the years, the per-hectare premium for natural disaster insurance can reach NT$57,459 for 100% coverage. The premium for natural disaster insurance, however, is significantly higher than that for revenue insurance, mainly because a decrease in yield leads to an increase in price; hence, the loss of actual revenue is less than the loss of yield. Hence, revenue insurance has a lower premium and accounts for the price risk; thus, promoting this type of insurance in the future would be invaluable for protecting farmer incomes.

Insurance for the cost of replanting trees (tree cost insurance) for sugar apples

Tree cost insurance is a type of property insurance specifically designed to provide a guaranteed income for farmers in replanting periods following a natural disaster. It is also considered a form of attached insurance intended to provide insurance coverage for trees. However, each plant must be registered, which requires detailed data on plant growth and management. To avoid moral hazard, the data should be established at least when the plants are first insured.

The rule of tree cost insurance is that it is a form of attached insurance for revenue insurance, meaning that revenue insurance is the main insurance contract and tree cost insurance can be selected as an insurance rider. The qualification for indemnity is that the sugar apple trees are completely collapsed and dead and must be replanted because they have been destroyed by natural disaster. The premium and insurance amount are measured by NT$51 million per hectare on the basis of the total cost of replanting trees over a 3-year period.

Suppose that the replanted area of sugar apple trees following a natural disaster is 5%, in addition to 15% for operating costs; the annual premium per hectare is then calculated to be NT$5,000. The annual loss adjustment expense is NT$8.5 million for 3 consecutive years, but must be annually attached in a fruit revenue insurance policy for sugar apples for the indemnity to be obtained.

Planning the operational model

The government has a critical role in providing public support; because of the considerable management costs and insurance indemnity for systemic risk in agricultural insurance, the private sector is deterred from participating in it. The government can play an active role in providing reinsurance, subsidizing farmers’ insurance premiums, subsidizing management costs for the private sector, establishing public–private partnerships, and assisting in establishing and providing information. Therefore, the revenue insurance is provided with the features of government-sponsored insurance.

The Agricultural Development Act of Taiwan notes the following:

The government shall initiate an agricultural insurance program to secure farmers' income, to stabilize rural communities and to make full use of agricultural resources. Before the agricultural insurance program is enacted into law, the central competent authority shall establish regulations in accordance with which agricultural insurance program by districts, categorization and stage may be implemented on a trial basis. All farmers within the same district and business operation line may participate in the program. Farmers' organizations may be commissioned to handle the said insurance program. The commissioned farmers’ organization handling the insurance program shall receive rewards and have the assistance or support from the government. (Article 58)

Furthermore, the Farmers Association Act of Taiwan prescribes that farmers’ associations are authorized to “accepting commissioned requests to handle farming insurance business” (Article 4, Subparagraph 12). Therefore, with the support of the law, the coverage, underwriting, and indemnity of sugar apple revenue insurance designed in this article are based on the system of the Farmers’ Association, which is organized into three levels (township, county, and national), and the risk-sharing mechanism of the government. This means that the indemnity is shared by the three levels of the Farmers’ Associations with a loss ratio of less than 100%, where 60% is shared by township-level Farmers’ Associations, while the remaining 40% is transferred to county- and national-level Farmers’ Associations and divided equally between them. The indemnity is transferred to the government, which shoulders the final burden with a loss ratio of more than 100%. Ten percent of the insurance premium is allocated to cover the operating expenses of the Farmers’ Associations, but the loss ratio that must be shared is 100%, and that is expressed as 10% of the risk being shared by the Farmers’ Associations. Meanwhile, the role of county- and national-level Farmers’ Associations is to provide reinsurance—but not coinsurance—because the roles of these institutions are noninsurers. The operational model is depicted in Fig. 3.

Fig. 3. The operation model of sugar apple revenue insurance

Farmers’ Associations are distributed throughout Taiwan, and these institutions tend to interact closely with farmers and would thus have a channel advantage. Therefore, the Farmers’ Associations assist in the promotion of agricultural insurance, coverage, disaster reporting, disaster survey coordination, insurance indemnity, and communication with farmers, and the farmers can purchase insurance or apply for indemnity at the nearest Farmers’ Association. The Council of Agriculture (COA) is the competent authority for enforcing agricultural insurance, and it is responsible for supervising and managing the agricultural insurance fund. The sources of funds would be as follows: (a) The COA compiles the annual budget support for premium subsidies, which are included in the agricultural insurance fund; (b) the insurance premiums paid by the farmers, where after the management expenses and all costs for the current year have been deducted, the entire balance is to be deposited as a reserve, and rapidly accumulating reserves are to be used for future compensations.

It suggests that the agriculture insurance fund should be the core of agricultural insurance operating mechanisms in the future, which is in response to the premium pricing, insurance policy design, catastrophic underwriting, domestic and overseas reinsurance, and insurance indemnity. Moreover, the risk diversification mechanism should be established for coinsurance, reinsurance, and transferring the indemnity to the government when losses exceed the risk-assumption limits of the agriculture insurance fund.

Features of revenue insurance

Basically, the insurance indemnity and premium are determined by the difference between the base revenue and actual revenue, where the price data are wholesale market prices, and the yield data are from the Agricultural Statistics Yearbook. The data for calculating the insurance indemnity and insurance premium should have consistency, transparency, and credibility. The various insurance coverage rates are considered to provide different options for farmers.

In summary, the features of revenue insurance designed in this scheme are as follows:

1. Completeness of vision: the design could be a response to the trend of climate change, agricultural trade liberalization and the traditional subsidy policy, which has been transformed to conform to WTO regulations, as well as foresights regarding policy implications.

2. Government-sponsored insurance: the design does not follow the model of commercial insurance, and the agricultural insurance is piloted by Taiwan’s Farmers’ Associations on the basis of the Agricultural Development Act. In line with the model of livestock insurance, insurance coverage is provided by the Farmers’ Associations at all three levels, the insurance premium is subsidized by the government, and the final excess loss is undertaken by the government.

3. Financial stabilization: the design is based on the economic life of sugar apple plants being 15 years from planting, and on maintaining long-term financial balance.

4. Complete protection: regardless of the price decline or impaired yield of sugar apples, the design would be aimed at guaranteeing the final revenue.

5. Reducing the cost of insurance: the design avoids the cost and disruption of exploration.

6. Locally identified yields: the design considers regional yields and open market prices and is not necessary aimed at filling in the individual actual yields and sales prices. This would contribute to production management and quality improvement.

7. The main insurance contract and attached insurance: in addition to the main contract of fruit revenue insurance, tree cost insurance, which is an attached insurance, can be offered during the replanting period.

8. Various options: different options for protection insurance premiums or base revenues can be provided to farmers, such as different levels of insurance coverage and whether the insurance is included in the natural disaster relief.

9. Information disclosure: the information is transparent and thus can reduce controversy. This would be convenient for underwriting and insurance indemnity calculations, and can be inquired and insured by using a software application (e.g., a mobile phone app).

10. Premium feedback: a dividend discount mechanism for the premium can be used to encourage farmers to purchase insurance.

CONCLUSION

In Taiwan, agricultural insurance has been a topic of discussion since 1956; however, the implementation of this type of insurance did not begin until the insurance policy for top-grafting sand pears was implemented in 2015, and its insurance rate remains low (less than 1% of planted areas) because it continues to follow the commercial insurance model. In 2016, a series of typhoons caused large-scale agricultural disasters. Following the presidential inauguration on May 20, 2016, and active reformation of the agricultural policy, the revenue insurance for sugar apples was designed and finalized. The implementation of revenue insurance for sugar apples is expected to be successful, but it is necessary to consider the number and arrangement of current policies, such as price support for each product, factor subsidies, the relief of production and marketing imbalances, natural disaster relief, and rules for redressing damage to farmers from agricultural imports, and to avoid the problems of overlapping subsidies and inequality. Clarifying the relationship between agricultural insurance and these subsidy policies would also be helpful. Such clarification could avoid placing a heavy financial burden on the government.

Date submitted: April 21, 2017

Reviewed, edited and uploaded: June 26, 2017