ABSTRACT

Crop insurance in South Korea has played an important role for stable farm management since 2001 with two crops, apple and pear, as an initial demonstration of insurance. It has been expanded to fifty crops as of 2016. As the number of crops which is covered by agricultural insurance is increasing, the interest of claim adjustment of crop insurance is also expanding. NongHyup Property & Casualty Insurance Co,. Ltd which is the only crop insurance company in South Korea focuses on the improvement of the claim adjustments to builds the prompt and fare claim adjustment system. There are a lot of loss assessments methods for its crops and natural disasters. To provide farmers with direct helps, NongHyup Property & Casualty Insurance is trying to develop claim adjustment system and educate loss adjusters regularly for professional knowledge and skills. In this paper, the claim adjustment of Korea’s crop insurance will be generally explained with the definition of the claim adjustments’ system, human resources, field loss assessment, the examples of loss assessments, and handling civil complaint.

Keywords : Crop Insurance, Loss Adjusters, Natural Disaster, Loss Assessment, Named Peril, Multi-Peril.

1. INTRODUCTION

The development of Korea’s crop insurance has proceeded at an unprecedented pace. It was founded in 2001 with the 2 crops of apple and pear, and now its assuring crops are expanded to 50 crops as of 2016. Besides the types of crop, it has shown a rapid advancement in all area, such as a total amount insured, an insured area, and the number of insured farms, etc. But, it also experienced a dark side. In 2002 when the second year of crop insurance’s introduction, the loss ratio was greater than 400% because of the typhoon ‘Rusa’. Next year, 2003, the re-insurance companies decided to withdraw from crop insurance. Therefore, the insurer NongHyup had to manage the crop insurance without re-insurance. In 2005, the government decided to introduce the National Re-insurance System which covers damage over the loss ratio of 150% and the re-insurance companies take part into crop insurance again. Also, in 2012, four typhoons and three huge hails caused over 350% loss ratio and the payment of 410 million dollars. As the examples mentioned above, it is impossible to estimate the loss ratio and loss amount in the crop natural disaster insurance because the damage could be too big. Also, to prepare for the event of huge natural disaster, it is required to establish a prompt and fare claim adjustment system. The insurer Nonghyup focuses on strengthening ability of loss adjustment and tries to preserve farmers’ income from catastrophe.

2. ORGANIZATION AND HUMAN RESOURCES

The organization of loss adjustment system is composed of Agricultural Insurance Claims Department and sixteen Local Headquarters. The agricultural Insurance Claims Department is located in the head office, Seoul, with two teams and sixteen people. The local headquarters are located around the whole country. The loss adjustment human resources are composed of three loss adjuster groups, farmers, loss adjusters and surveyors corporations, and the korea association of agricultural & fishery insurance on natural disaster (simply called ‘association’).

Agricultural Insurance Claims Department is in charge of managing and training loss adjustment human resources. It educates the loss adjusters every year for professional skills and knowledge about the loss assessment of crop. The education covers all crops which are included in the crop insurance and it is for all loss adjusters around the country. The new farmer loss adjuster must complete the loss adjustment education. The existing loss adjusters have to take the loss adjustment education more than once in three years to maintain their qualification. The loss adjusters are able to perform an accurate and fare crop loss assessment by learning knowledge and skills and taking regular training.

In the event of natural huge catastrophe, Agricultural Insurance Claims Department makes task force team to manage a stable operation of loss adjustment system. The natural catastrophe defines an unexpected natural disaster that causes great suffering or damage to the farm management. Because crop insurance covers damage from natural disaster to crops alive, prompt damage assessment is required for an accurate rate of damage. So the insurer organizes task force and prepares for huge natural catastrophe. In the task force team, members analyze when typhoons occur frequently and which route typhoon often blows, and they practice assigning loss adjusters for prompt loss assessment.

Local Headquarters which are located across the country are in charge of supporting Claims Department. For instance, in the term of claim adjustment education, they make a reservation for training places and guide the general progress to the loss adjusters. In addition, when the loss adjusters visit the damaged farms for claim adjustments, local headquarters’ staff accompanies and supports them.

The loss adjusters consist of three groups : farmers, loss adjusters and surveyors corp, and adjusters in the association. Among them, the number of farmer adjusters is the highest. The number of farmer adjusters is about 12,700 and the number of assigned case to the farmer adjusters is about 80,000 at the end of last year, 2015. The farmer adjusters also have their own farm and are still farming, so they have specialized knowledge about crops. They are educated regularly about claim adjustments and crop insurance. In addition, they can conduct damage assessment anytime because they stay around insured area. For these reasons, the farmer adjusters have contributed to the greater development of Korea’s crop insurance. The farmer adjusters are divided into 3 detailed groups : advanced farmer adjuster, farmer adjuster, and farmer adjuster supporter. The advanced farmer adjusters lead the adjustment team that usually consists of three adjusters. In the past, the advanced farmer adjusters are appointed by the recommendation of crop insurance manager in the local branch. The crop insurance manager reviews farmer adjusters’ past career for recommendation. To apply more objective criteria when selecting advanced farmer adjusters, however, the insurer started to manage each adjuster’s past claims. So, starting from 2015, advanced farmer adjusters are appointed by their claim points. The farmer adjusters occupy most of adjusters. They make a loss assessment team with advanced farmer adjusters and farmer adjuster supporters. The farmer adjuster supporters usually support farmer adjusters. Their role and responsibilities are smaller than other adjusters.

The loss adjusters and surveyors corporations also participate in the claim adjustments. The number of adjusters is about 300 as of 2015. They are in charge of professional claim, such as green house or agricultural facilities. The adjusters in corporation have deeper understanding about insurance than farmer adjusters and they have experienced damage assessment capabilities. In 2016, the insurer has 34 loss adjusters and surveyors corporations under contracts for loss assessment of crop insurance. They are required to complete loss assessment education regularly and get feedback from the insurer to grow their capabilities.

The adjusters in the association are small part of current claim adjustment system. But, in the event of great disaster, they are also assigned for loss assessment and contribute to prompt claim adjustments.

3. OPERATION AND SYSTEM

The operation of loss assessment in crop insurance is started by the notice of the insurance contractor. In the event of disaster, the contractor visits the local Nonghyup branch and reports the case. In the local branch, crop insurance manager inputs the information about the case into the computing system. The Claim Department in the Head Office checks the reported case in real time and makes a plan for assigning loss adjusters considering the types of disaster, crop, and region, etc. The loss adjusters make an adjusting team that consists of two or three adjusters and visit the damaged area for loss assessment. When they complete the loss assessment, they let the insurance contractor and the crop insurance manager in the local branch the result of loss adjustment. In the local branch, the crop insurance manager input the result of loss assessment into the computing system. In the head office, the manager checks the loss ratio in real time and conduct an inspection in the region of showing unusually high damage ratio for its disaster. When the whole process of calculating payment is finished and the damage exceeds the deductible ratio established in the policy, the insurer compensates the contractor for payment in 7 days.

4. EXAMPLE

The claim adjustment in Korea’s crop insurance differs from the types of disaster and crop. It could be classified into seven types : Named peril fruit tree, Before Thinning Out Multi Peril fruit tree, Multi peril fruit tree, field crops, rice, Agricultural facility and green house product.

4-1. Named Peril

The named peril crop insurance means that it only provides coverage on loss incurred on the insured crops from the disaster named on the policy. The named peril crop insurance includes an apple, a pear, a sweet persimmon, an astringent persimmon, and a tangerine. In this policy, it only covers the damage from the disaster of spring frost, typhoon, strong wind, hail, fall frost, and heavy rain. The typhoon, strong wind, and hail are the main contract and the others, such as spring frost and fall frost, are the option. The claim adjustment of the named peril is largely divided into the before thinning out and after thinning out. To thin out is done usually on June or July to reduce the superfluous fruits. The typical example of the disaster which is covered before thinning out is spring frost. The spring frost means that the damage incurred on a flower or a flower bud by freezing temperature. The spring frost contract is valid until May 31. When the spring frost damage is reported to the head office, the manager in the claim department checks the weather information and assigns the loss assessment team to the damaged area. The loss assessment team visits the damaged area and investigates the claim. The first step of the loss assessment is to select the three sample trees in the field. In the sample trees, select the four branches on each tree and check if the flowers or flower buds are damaged with naked eyes. If the damaged ratio is over 5%, the insurer recognizes the damage on the unit and compensates for the contractor.

In case of hail, the loss assessment differs from the occurred period. If the hail occurs before thinning out, the loss adjusters visit the damaged area and begin to investigate the hit ratio of young fruit by hail. The hit ratio of young fruits is a sample test that examines the ratio of non-damaged young fruit or flower bud to the damaged young fruit or flower bud. The sample trees are selected according to the sample tree table that shows an adequate number of trees for each crop. In the case of hail that occurs after thinning out, the loss adjuster examines the falling of fruit in the field by hail. The loss adjuster counts the number of fallen fruits and reflects it to the final loss ratio. After all, when hail occurs to the insured area, the insurer begins to investigate the damaged area with two way ; hit ratio of young fruits and counting of fallen fruits. In addition to these two loss assessments, the insurer will investigate the damage ratio of fruits right before harvest to the all damaged area by hail. It is because that even if the loss adjuster could not catch the damage by hail, as time passes the damage on the fruits gets bigger when the harvest time is closer. No matter how many cases reported to the insurer by hail, the investigation of damaged fruits before harvest will be done just once on one unit. The loss adjuster selects the three sample trees and picks the all fruits hanging on the trees. All fruits are categorized based on the damage ratio of 100%, 80%, 50%, and non-damaged fruits. 100% damaged fruit means that it could not be used or sold at all in any way. 80% damaged fruit means that it could not be sold to the market but could be used in a processed good like a jam or a juice. 50% damaged fruit means that it could be sold to the market with half price because it has some crack or flaw on its face. With this standard, the loss adjuster evaluates the quality of the fruits and reflects the result to the final loss ratio.

Fall frost refers to the damage incurred on a fruit or a leaf by freezing temperature from September to the time of harvest. When the fall frost damage is reported, the head office assigns the loss adjuster team to the damaged area. The loss adjusters select the three sample trees and pick the all fruits on the trees. They categorize the all fruits based on the damage ratio of 100%, 80%, 50%, and non-damaged fruits. Just like the case of hail, the loss adjuster evaluates the quality of the fruits and reflects the result to the final loss ratio.

In the case of typhoon or gale, the loss assessment is divided into two ways ; before thinning out and after thinning out. Before thinning out, the loss adjuster investigates the damaged trees. Usually before thinning out, the damage by typhoon or gale is little because the fruit is small. So, in the case of typhoon or strong wind before thinning out, the loss adjuster counts the number of the trees that is dead or is not possible to produce fruits. In the event of typhoon or gale after the thinning out, the loss adjuster counts the all fallen fruits. After counting the fallen fruits, the loss adjuster selects at least 100 fruits out of the all fallen fruits and categorizes them based on the damaged ratio, 100%, 80%, 50%, and non-damaged fruits. The loss product is calculated by multiplying the damage ratio from the sample 100 fruits and the number of the fallen fruits. Plus, to get the final loss product, multiply 107% to the product just mentioned above. Whenever the typhoon or gale occurs, the same investigation will be conducted and the loss number of the fruits will be accumulated until the harvest time.

4-2. BTO MPCI

BTO MPCI which is standing for Before Thinning Out Multi Peril Crop Insurance covers multi perils only before thinning out and convers after thinning out disaster only named on the policy just like named peril insurance. The crops in BTO MPCI are an apple, a pear, and a sweet persimmon. For example, the farmer who is farming an apple can have a choice which insurance system to choose between Named Peril system and BTO Multi Peril system. The multi perils which are covered before thinning out are natural disaster, fire, and damage by birds and mammals. The natural disaster means all disaster except the damage by disease and insects. After thinning out, the process and principle of loss assessment are totally same as the named peril insurance mentioned above.

4-3. Multi-Peril

Multi peril crop insurance includes a grape, a peach, a plum, a mulberry, a kiwi, a jujube, a Japanese apricot, and chestnut. It covers natural disaster, fire, and damage by birds and mammals in the insurance contract period.

4-4. Rice

The rice crop insurance covers natural disaster, fire, damage by birds and mammals, and disease and insects. The rice crop’s cover types are composed of four ; transplanting cover, re-transplanting cover, unproductive cover, and decreased yield cover.

The investigation of transplanting cover is conducted after 31st July, when the insurer considers that transplanting is not possible anymore. If the contractor cannot transplant rice because of the natural disaster, he or she asks for the investigation of transplanting cover contract and the loss adjuster visits the damaged area for checking whether or not insured. The insurer checks the result of loss assessment and compensates the payment. The payment is 10% of amount insured and the contract terminates.

The investigation of re-transplanting cover is for the contractor who wants to keep farming rice. In the event of disaster after transplanting rice, the contractor asks for the investigation of re-transplanting to keep farming. The term of the contract is from the time of transplanting to 31st July. If the damaged ratio exceeds the deductible ratio, the insurer compensates the payment which is 25% of the amount insured. In this case, the insurance contract is not terminated and still valid and the contractor keeps rice farming.

The unproductive cover contract which begins after transplanting rice is the contract which covers if the damaged ratio of rice is over 70% and the contractor asks for the premium. In this case, the contractor has a choice to choose the unproductive cover contract or the decrease in harvest cover contract. If the contract wants the unproductive cover, the insurer decides to compensate and the contract will be terminated.

The last one is the investigation of decreased yield cover. When the contractor reports the damage, the loss adjuster measures the yield when harvesting and calculates the decreased yield. The decreased yield cover has three types of investigation methods. The first one is to investigate the ratio of ripen rice. It is conducted 14 days before and after harvest time. The loss adjuster select six sample section and check the ripen ratio of the sample rice. The second one is to measure yield of sample section. The loss adjuster selects the sample area according to the sample area table which is made up by the insurer. The last one is to measure all yield of the insured area. It is conducted at harvesting time.

4-5. Field Crop

The field crop insurance includes a garlic, a bean, a potato, a corn, an onion, a sweet potato, and a tea. The principle of the field crop insurance is same as the rice crop insurance. In the event of the natural disaster that is covered by the contract, the contractor visits the local NongHyup branch to report the damage fact. The crop insurance manager in the head office assigns the loss adjuster to the damaged area. The loss adjuster visits the damaged field to see if the damage is from the disaster that covered by the contract. When it’s harvesting time, the loss adjusters measure yield and compare the measured yield with the expected yield. The insurer will compensate the decreased yield. The field crop insurance also has the unproductive cover contract except the tea crop. Just like rice crop insurance, when the loss adjuster checks the damage which is happened by the covered disaster, the loss adjuster measures the damaged area and compares it with the insured area to calculate the damage ratio. If it exceeds 70%, the insurer compensates the contractor for the insurance and the contract terminates. The investigation of yield is conducted to all field crop insurance. Except the bean crop, the sample test can be used for investigating yield. About the bean crop, the loss adjuster have to investigate all yield of the field.

4-6. Examples

Now the examples of the payment’s whole process by crop and disaster will be explained.

Let’s suppose the apple in the named peril which is damaged by spring frost before thinning out. In the named peril fruit tree insurance, the number of fruit is the standard for compensating the payment. So, in this case, suppose the standard number of apple is 10,000, the number of after thinning out is 6,000, the recognized loss ratio of the spring frost is 50%, the deductible ratio is 20%, and the amount insured is 10,000 dollars. About the natural disaster before thinning out, the named peril insurance compensates the decreased number of standard number of fruit and the number of fruit after thinning out. The standard number of fruit is decided by the past yield number of the fruit in the area. When the loss by spring frost is reported to the local Nonghyup branch, the loss adjuster visits the damaged area and checks the fact of the damage. The loss adjuster selects the three sample trees in the field and investigates the frost damage of a flower or a flower bud. When the loss adjuster recognizes the loss, the insurer considers the decreased number of the fruit as the loss. So, the final loss number of the fruit is calculated to 2,000. (10,000 – 6,000) ⅹ 50% = 2,000.

The insurance contractor can choose between 50% and 70% for the recognized loss ratio in the spring frost contract when purchasing the crop insurance.

The example of compensating the apple in the named peril by typhoon after thinning out is explained. Suppose that the number of standard fruit is 10,000, the number of fruit after thinning out is 10,000, the deductible rate is 20%, the amount insured is 10,000 dollars. When the contractor reports the damage to the local Nonghyup branch, the loss adjuster visits the damaged field. The loss adjuster counts all fallen fruits in the field. Among the all fallen fruits, the loss adjuster extracts 100 fruits at random and categorizes them into 100%, 80%, 50%, and non-damaged fruits based on the damage ratio. Suppose the number of the all fallen fruits is 5,000. The result of categorized 100 fruits is that the number of 100% damaged fruits is 20, 80% damaged fruits is 30, 50% damaged fruits is 30, and the non-damaged fruits is 20. The processed result is like this. 100% ⅹ 20 + 80% ⅹ 30 + 50% ⅹ 30 + 0% ⅹ 20 = 59. The loss ratio of this typhoon is calculated to 59% and the decreased number of fruits is 2,950 (5,000 ⅹ 59%). The final loss ratio is 9.5% ( 2,950 / 10,000 – 20%) and the final insurance payment will be 950 dollars. In the case of typhoon, the decreased number of fruits is accumulated every time a typhoon occurs until the termination of the contract. So, if another typhoon occurs at the same field, the loss adjuster will conduct the same investigation. In the event of gale or strong wind, the same investigation that is used for typhoon will be conducted.

Now, the example of damage by hail will be explained. Suppose the hail occurs before thinning out to an apple crop insurance, the standard number of fruits is 100,000, and the number of fruits after thinning out is 60,000. When the contractor reports the damage to the local Nonghyup branch, the crop insurance manager assigns a loss adjuster to the field. The loss adjuster visits the field and investigates the hit ratio of young fruit. The loss adjuster selects the sample trees in accordance with the sample tree table. The sample tree table by crops shows the proper number of sample tree. The loss adjuster selects four branches on each sample trees and extracts over 5 young fruits or flower buds on each selected branches. On one tree, total 20 young fruits or flower buds will be searched. If the loss adjuster selects 10 sample trees, total 200 young fruits or flower buds will be investigated. If 100 out of 200 young fruits get damaged by hail, the hit ratio of the young fruits is 50%. So, the final decreased number of fruits by hail before thinning out will be 28,571.

Calculated detail : 50% ⅹ 10/7 ⅹ 40,000 (decreased number of fruits : 100,000 – 60,000) = 28,571

All claims by hail will conduct an additional investigation of damage right before harvest. When the young fruit is too small to see the flaw or crack by hail, the damage is not recognized by the loss adjuster. As the tree grows, however, the fruits get damaged cracks or flaw on its face. So, the loss adjuster will investigate the damage ratio of the fruits right before harvest. The loss adjuster selects the three sample trees and extracts all fruits on the trees. And then categorizes the extracted fruits into 100% damaged, 80% damaged, 50% damaged, and non-damaged fruits. From this process, the loss adjuster gets the loss rate and calculates the final loss number by multiplying the loss rate by the number of final harvest fruits.

The example of multi peril crop insurance is explained. Suppose that the crop is jujube, the amount insured is 15,000 dollars, the standard harvest weight is 1,600kg, the deductible rate is 20%, and the number of the jujube trees is 350. If the typhoon occurs, the contractor visits the local Nonghyup branch for reporting the claim. The insurer assigns the loss adjusting team to the damaged area. The loss adjuster visits the field and checks the damage. Multi peril crop insurance system does not count the number of fallen fruits. Instead, the loss adjuster just checks the types of natural disaster. When its harvest time, the loss adjuster visits the field and measures harvest weight. To measure the weight, the loss adjuster selects the sample trees in accordance with the sample tree table. And then, the loss adjuster picks all apples and weights them. The loss adjuster divides the measured weight by the number of used trees and it gives us the weight of harvest jujubes from one trees. Let’s suppose that the harvest weight of one jujube tree is 1,250g. So, the total measured harvest weight could be estimated to 437.5kg(1,250g ⅹ 350). The loss rate would be 72.7%(1 - 437.5 / 1,600) and the final loss rate would be 52.7% which reflects deductible rate(20%). So, the insurance payment would be 7,905 dollars(15,000 ⅹ 52.7%).

The representative loss assessments examples in Korea’s agricultural insurance are explained above. There are much more loss assessments methods by the types of crop, disaster, and period. NongHyup property and casualty insurance corporation is trying to improve claim adjustment system to provide direct help for farmers. But, sometimes the contractor files a civil complaint about the process of loss assessment or insurance payment. In this case, the contractor files a civil complaint through a phone call, mail, the internet, visiting directly to the head office, or using Financial Supervisory Service. When the civil complaint is reported, the crop insurance manager in the head office examines the case with the loss adjuster that was in charge of the case in the past. The crop insurance manager compares the civil complaint with the past similar cases or requests an investigation about the crop and disaster to the related institution or professor who researches the agricultural field. When the crop insurance managers finish the all examination about the case, the insurer gives notice to the contractor about the result. The insurer puts forth a multilateral effort to reduce an incidence of civil complaint.

5. CONCLUSION

Korea’s agricultural insurance has grown rapidly in a short time. It covers 50 crops as of 2016 and the insurer plans to expand crops steadily. In addition, the insurer will improve the agricultural insurance from the covering decreased amount to the covering decreased income for famers. Currently, the insurer applies ‘Revenue Protection’ which preserves the farmer’s decreased income to some crops as a pilot project. The insurer will expand the Revenue Protection to more crops and improve the insurance system. Also, the insurer tries to keep stable loss assessment system of crop insurance. So, with this system, even if a huge natural catastrophe occurs in South Korea, the farmer could keep stable farming management.

Table 1. Farmer adjuster’s loss assessment training

|

Year

|

Trainees

|

Training

|

|

2014

|

2,930

|

30

|

|

2015

|

4,548

|

32

|

|

2016

|

3,688

|

28

|

|

Totals

|

11,166

|

90

|

Table 2. Farmer adjusters in 2015

|

|

Number

|

%

|

|

Advanced

|

294

|

2.2

|

|

Farmer

|

12,757

|

94.9

|

|

Supporter

|

393

|

2.9

|

Fig 1. The picture of damaged flower and flower bud by spring frost

Fig 2. The picture of damaged pear field by typhoon

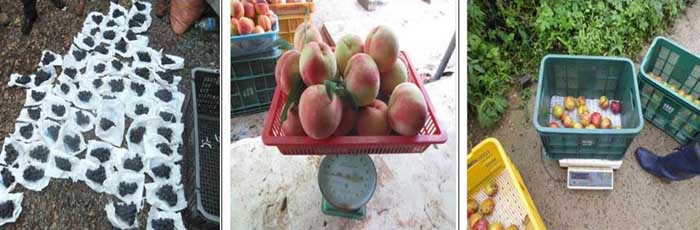

Fig 3. The picture of damaged young fruit by hail

Fig 4. The picture of the weighing multi peril fruits(grape, peach, plum)

| Submitted as a country paper for the FFTC-RDA International Seminar on Implementing and Improving Crop Natural Disaster Insurance Program, June 14-16, 2016, Jeonju, Korea |

Claim Adjustments in Korea’s Crop Natural Disaster Insurance

ABSTRACT

Crop insurance in South Korea has played an important role for stable farm management since 2001 with two crops, apple and pear, as an initial demonstration of insurance. It has been expanded to fifty crops as of 2016. As the number of crops which is covered by agricultural insurance is increasing, the interest of claim adjustment of crop insurance is also expanding. NongHyup Property & Casualty Insurance Co,. Ltd which is the only crop insurance company in South Korea focuses on the improvement of the claim adjustments to builds the prompt and fare claim adjustment system. There are a lot of loss assessments methods for its crops and natural disasters. To provide farmers with direct helps, NongHyup Property & Casualty Insurance is trying to develop claim adjustment system and educate loss adjusters regularly for professional knowledge and skills. In this paper, the claim adjustment of Korea’s crop insurance will be generally explained with the definition of the claim adjustments’ system, human resources, field loss assessment, the examples of loss assessments, and handling civil complaint.

Keywords : Crop Insurance, Loss Adjusters, Natural Disaster, Loss Assessment, Named Peril, Multi-Peril.

1. INTRODUCTION

The development of Korea’s crop insurance has proceeded at an unprecedented pace. It was founded in 2001 with the 2 crops of apple and pear, and now its assuring crops are expanded to 50 crops as of 2016. Besides the types of crop, it has shown a rapid advancement in all area, such as a total amount insured, an insured area, and the number of insured farms, etc. But, it also experienced a dark side. In 2002 when the second year of crop insurance’s introduction, the loss ratio was greater than 400% because of the typhoon ‘Rusa’. Next year, 2003, the re-insurance companies decided to withdraw from crop insurance. Therefore, the insurer NongHyup had to manage the crop insurance without re-insurance. In 2005, the government decided to introduce the National Re-insurance System which covers damage over the loss ratio of 150% and the re-insurance companies take part into crop insurance again. Also, in 2012, four typhoons and three huge hails caused over 350% loss ratio and the payment of 410 million dollars. As the examples mentioned above, it is impossible to estimate the loss ratio and loss amount in the crop natural disaster insurance because the damage could be too big. Also, to prepare for the event of huge natural disaster, it is required to establish a prompt and fare claim adjustment system. The insurer Nonghyup focuses on strengthening ability of loss adjustment and tries to preserve farmers’ income from catastrophe.

2. ORGANIZATION AND HUMAN RESOURCES

The organization of loss adjustment system is composed of Agricultural Insurance Claims Department and sixteen Local Headquarters. The agricultural Insurance Claims Department is located in the head office, Seoul, with two teams and sixteen people. The local headquarters are located around the whole country. The loss adjustment human resources are composed of three loss adjuster groups, farmers, loss adjusters and surveyors corporations, and the korea association of agricultural & fishery insurance on natural disaster (simply called ‘association’).

Agricultural Insurance Claims Department is in charge of managing and training loss adjustment human resources. It educates the loss adjusters every year for professional skills and knowledge about the loss assessment of crop. The education covers all crops which are included in the crop insurance and it is for all loss adjusters around the country. The new farmer loss adjuster must complete the loss adjustment education. The existing loss adjusters have to take the loss adjustment education more than once in three years to maintain their qualification. The loss adjusters are able to perform an accurate and fare crop loss assessment by learning knowledge and skills and taking regular training.

In the event of natural huge catastrophe, Agricultural Insurance Claims Department makes task force team to manage a stable operation of loss adjustment system. The natural catastrophe defines an unexpected natural disaster that causes great suffering or damage to the farm management. Because crop insurance covers damage from natural disaster to crops alive, prompt damage assessment is required for an accurate rate of damage. So the insurer organizes task force and prepares for huge natural catastrophe. In the task force team, members analyze when typhoons occur frequently and which route typhoon often blows, and they practice assigning loss adjusters for prompt loss assessment.

Local Headquarters which are located across the country are in charge of supporting Claims Department. For instance, in the term of claim adjustment education, they make a reservation for training places and guide the general progress to the loss adjusters. In addition, when the loss adjusters visit the damaged farms for claim adjustments, local headquarters’ staff accompanies and supports them.

The loss adjusters consist of three groups : farmers, loss adjusters and surveyors corp, and adjusters in the association. Among them, the number of farmer adjusters is the highest. The number of farmer adjusters is about 12,700 and the number of assigned case to the farmer adjusters is about 80,000 at the end of last year, 2015. The farmer adjusters also have their own farm and are still farming, so they have specialized knowledge about crops. They are educated regularly about claim adjustments and crop insurance. In addition, they can conduct damage assessment anytime because they stay around insured area. For these reasons, the farmer adjusters have contributed to the greater development of Korea’s crop insurance. The farmer adjusters are divided into 3 detailed groups : advanced farmer adjuster, farmer adjuster, and farmer adjuster supporter. The advanced farmer adjusters lead the adjustment team that usually consists of three adjusters. In the past, the advanced farmer adjusters are appointed by the recommendation of crop insurance manager in the local branch. The crop insurance manager reviews farmer adjusters’ past career for recommendation. To apply more objective criteria when selecting advanced farmer adjusters, however, the insurer started to manage each adjuster’s past claims. So, starting from 2015, advanced farmer adjusters are appointed by their claim points. The farmer adjusters occupy most of adjusters. They make a loss assessment team with advanced farmer adjusters and farmer adjuster supporters. The farmer adjuster supporters usually support farmer adjusters. Their role and responsibilities are smaller than other adjusters.

The loss adjusters and surveyors corporations also participate in the claim adjustments. The number of adjusters is about 300 as of 2015. They are in charge of professional claim, such as green house or agricultural facilities. The adjusters in corporation have deeper understanding about insurance than farmer adjusters and they have experienced damage assessment capabilities. In 2016, the insurer has 34 loss adjusters and surveyors corporations under contracts for loss assessment of crop insurance. They are required to complete loss assessment education regularly and get feedback from the insurer to grow their capabilities.

The adjusters in the association are small part of current claim adjustment system. But, in the event of great disaster, they are also assigned for loss assessment and contribute to prompt claim adjustments.

3. OPERATION AND SYSTEM

The operation of loss assessment in crop insurance is started by the notice of the insurance contractor. In the event of disaster, the contractor visits the local Nonghyup branch and reports the case. In the local branch, crop insurance manager inputs the information about the case into the computing system. The Claim Department in the Head Office checks the reported case in real time and makes a plan for assigning loss adjusters considering the types of disaster, crop, and region, etc. The loss adjusters make an adjusting team that consists of two or three adjusters and visit the damaged area for loss assessment. When they complete the loss assessment, they let the insurance contractor and the crop insurance manager in the local branch the result of loss adjustment. In the local branch, the crop insurance manager input the result of loss assessment into the computing system. In the head office, the manager checks the loss ratio in real time and conduct an inspection in the region of showing unusually high damage ratio for its disaster. When the whole process of calculating payment is finished and the damage exceeds the deductible ratio established in the policy, the insurer compensates the contractor for payment in 7 days.

4. EXAMPLE

The claim adjustment in Korea’s crop insurance differs from the types of disaster and crop. It could be classified into seven types : Named peril fruit tree, Before Thinning Out Multi Peril fruit tree, Multi peril fruit tree, field crops, rice, Agricultural facility and green house product.

4-1. Named Peril

The named peril crop insurance means that it only provides coverage on loss incurred on the insured crops from the disaster named on the policy. The named peril crop insurance includes an apple, a pear, a sweet persimmon, an astringent persimmon, and a tangerine. In this policy, it only covers the damage from the disaster of spring frost, typhoon, strong wind, hail, fall frost, and heavy rain. The typhoon, strong wind, and hail are the main contract and the others, such as spring frost and fall frost, are the option. The claim adjustment of the named peril is largely divided into the before thinning out and after thinning out. To thin out is done usually on June or July to reduce the superfluous fruits. The typical example of the disaster which is covered before thinning out is spring frost. The spring frost means that the damage incurred on a flower or a flower bud by freezing temperature. The spring frost contract is valid until May 31. When the spring frost damage is reported to the head office, the manager in the claim department checks the weather information and assigns the loss assessment team to the damaged area. The loss assessment team visits the damaged area and investigates the claim. The first step of the loss assessment is to select the three sample trees in the field. In the sample trees, select the four branches on each tree and check if the flowers or flower buds are damaged with naked eyes. If the damaged ratio is over 5%, the insurer recognizes the damage on the unit and compensates for the contractor.

In case of hail, the loss assessment differs from the occurred period. If the hail occurs before thinning out, the loss adjusters visit the damaged area and begin to investigate the hit ratio of young fruit by hail. The hit ratio of young fruits is a sample test that examines the ratio of non-damaged young fruit or flower bud to the damaged young fruit or flower bud. The sample trees are selected according to the sample tree table that shows an adequate number of trees for each crop. In the case of hail that occurs after thinning out, the loss adjuster examines the falling of fruit in the field by hail. The loss adjuster counts the number of fallen fruits and reflects it to the final loss ratio. After all, when hail occurs to the insured area, the insurer begins to investigate the damaged area with two way ; hit ratio of young fruits and counting of fallen fruits. In addition to these two loss assessments, the insurer will investigate the damage ratio of fruits right before harvest to the all damaged area by hail. It is because that even if the loss adjuster could not catch the damage by hail, as time passes the damage on the fruits gets bigger when the harvest time is closer. No matter how many cases reported to the insurer by hail, the investigation of damaged fruits before harvest will be done just once on one unit. The loss adjuster selects the three sample trees and picks the all fruits hanging on the trees. All fruits are categorized based on the damage ratio of 100%, 80%, 50%, and non-damaged fruits. 100% damaged fruit means that it could not be used or sold at all in any way. 80% damaged fruit means that it could not be sold to the market but could be used in a processed good like a jam or a juice. 50% damaged fruit means that it could be sold to the market with half price because it has some crack or flaw on its face. With this standard, the loss adjuster evaluates the quality of the fruits and reflects the result to the final loss ratio.

Fall frost refers to the damage incurred on a fruit or a leaf by freezing temperature from September to the time of harvest. When the fall frost damage is reported, the head office assigns the loss adjuster team to the damaged area. The loss adjusters select the three sample trees and pick the all fruits on the trees. They categorize the all fruits based on the damage ratio of 100%, 80%, 50%, and non-damaged fruits. Just like the case of hail, the loss adjuster evaluates the quality of the fruits and reflects the result to the final loss ratio.

In the case of typhoon or gale, the loss assessment is divided into two ways ; before thinning out and after thinning out. Before thinning out, the loss adjuster investigates the damaged trees. Usually before thinning out, the damage by typhoon or gale is little because the fruit is small. So, in the case of typhoon or strong wind before thinning out, the loss adjuster counts the number of the trees that is dead or is not possible to produce fruits. In the event of typhoon or gale after the thinning out, the loss adjuster counts the all fallen fruits. After counting the fallen fruits, the loss adjuster selects at least 100 fruits out of the all fallen fruits and categorizes them based on the damaged ratio, 100%, 80%, 50%, and non-damaged fruits. The loss product is calculated by multiplying the damage ratio from the sample 100 fruits and the number of the fallen fruits. Plus, to get the final loss product, multiply 107% to the product just mentioned above. Whenever the typhoon or gale occurs, the same investigation will be conducted and the loss number of the fruits will be accumulated until the harvest time.

4-2. BTO MPCI

BTO MPCI which is standing for Before Thinning Out Multi Peril Crop Insurance covers multi perils only before thinning out and convers after thinning out disaster only named on the policy just like named peril insurance. The crops in BTO MPCI are an apple, a pear, and a sweet persimmon. For example, the farmer who is farming an apple can have a choice which insurance system to choose between Named Peril system and BTO Multi Peril system. The multi perils which are covered before thinning out are natural disaster, fire, and damage by birds and mammals. The natural disaster means all disaster except the damage by disease and insects. After thinning out, the process and principle of loss assessment are totally same as the named peril insurance mentioned above.

4-3. Multi-Peril

Multi peril crop insurance includes a grape, a peach, a plum, a mulberry, a kiwi, a jujube, a Japanese apricot, and chestnut. It covers natural disaster, fire, and damage by birds and mammals in the insurance contract period.

4-4. Rice

The rice crop insurance covers natural disaster, fire, damage by birds and mammals, and disease and insects. The rice crop’s cover types are composed of four ; transplanting cover, re-transplanting cover, unproductive cover, and decreased yield cover.

The investigation of transplanting cover is conducted after 31st July, when the insurer considers that transplanting is not possible anymore. If the contractor cannot transplant rice because of the natural disaster, he or she asks for the investigation of transplanting cover contract and the loss adjuster visits the damaged area for checking whether or not insured. The insurer checks the result of loss assessment and compensates the payment. The payment is 10% of amount insured and the contract terminates.

The investigation of re-transplanting cover is for the contractor who wants to keep farming rice. In the event of disaster after transplanting rice, the contractor asks for the investigation of re-transplanting to keep farming. The term of the contract is from the time of transplanting to 31st July. If the damaged ratio exceeds the deductible ratio, the insurer compensates the payment which is 25% of the amount insured. In this case, the insurance contract is not terminated and still valid and the contractor keeps rice farming.

The unproductive cover contract which begins after transplanting rice is the contract which covers if the damaged ratio of rice is over 70% and the contractor asks for the premium. In this case, the contractor has a choice to choose the unproductive cover contract or the decrease in harvest cover contract. If the contract wants the unproductive cover, the insurer decides to compensate and the contract will be terminated.

The last one is the investigation of decreased yield cover. When the contractor reports the damage, the loss adjuster measures the yield when harvesting and calculates the decreased yield. The decreased yield cover has three types of investigation methods. The first one is to investigate the ratio of ripen rice. It is conducted 14 days before and after harvest time. The loss adjuster select six sample section and check the ripen ratio of the sample rice. The second one is to measure yield of sample section. The loss adjuster selects the sample area according to the sample area table which is made up by the insurer. The last one is to measure all yield of the insured area. It is conducted at harvesting time.

4-5. Field Crop

The field crop insurance includes a garlic, a bean, a potato, a corn, an onion, a sweet potato, and a tea. The principle of the field crop insurance is same as the rice crop insurance. In the event of the natural disaster that is covered by the contract, the contractor visits the local NongHyup branch to report the damage fact. The crop insurance manager in the head office assigns the loss adjuster to the damaged area. The loss adjuster visits the damaged field to see if the damage is from the disaster that covered by the contract. When it’s harvesting time, the loss adjusters measure yield and compare the measured yield with the expected yield. The insurer will compensate the decreased yield. The field crop insurance also has the unproductive cover contract except the tea crop. Just like rice crop insurance, when the loss adjuster checks the damage which is happened by the covered disaster, the loss adjuster measures the damaged area and compares it with the insured area to calculate the damage ratio. If it exceeds 70%, the insurer compensates the contractor for the insurance and the contract terminates. The investigation of yield is conducted to all field crop insurance. Except the bean crop, the sample test can be used for investigating yield. About the bean crop, the loss adjuster have to investigate all yield of the field.

4-6. Examples

Now the examples of the payment’s whole process by crop and disaster will be explained.

Let’s suppose the apple in the named peril which is damaged by spring frost before thinning out. In the named peril fruit tree insurance, the number of fruit is the standard for compensating the payment. So, in this case, suppose the standard number of apple is 10,000, the number of after thinning out is 6,000, the recognized loss ratio of the spring frost is 50%, the deductible ratio is 20%, and the amount insured is 10,000 dollars. About the natural disaster before thinning out, the named peril insurance compensates the decreased number of standard number of fruit and the number of fruit after thinning out. The standard number of fruit is decided by the past yield number of the fruit in the area. When the loss by spring frost is reported to the local Nonghyup branch, the loss adjuster visits the damaged area and checks the fact of the damage. The loss adjuster selects the three sample trees in the field and investigates the frost damage of a flower or a flower bud. When the loss adjuster recognizes the loss, the insurer considers the decreased number of the fruit as the loss. So, the final loss number of the fruit is calculated to 2,000. (10,000 – 6,000) ⅹ 50% = 2,000.

The insurance contractor can choose between 50% and 70% for the recognized loss ratio in the spring frost contract when purchasing the crop insurance.

The example of compensating the apple in the named peril by typhoon after thinning out is explained. Suppose that the number of standard fruit is 10,000, the number of fruit after thinning out is 10,000, the deductible rate is 20%, the amount insured is 10,000 dollars. When the contractor reports the damage to the local Nonghyup branch, the loss adjuster visits the damaged field. The loss adjuster counts all fallen fruits in the field. Among the all fallen fruits, the loss adjuster extracts 100 fruits at random and categorizes them into 100%, 80%, 50%, and non-damaged fruits based on the damage ratio. Suppose the number of the all fallen fruits is 5,000. The result of categorized 100 fruits is that the number of 100% damaged fruits is 20, 80% damaged fruits is 30, 50% damaged fruits is 30, and the non-damaged fruits is 20. The processed result is like this. 100% ⅹ 20 + 80% ⅹ 30 + 50% ⅹ 30 + 0% ⅹ 20 = 59. The loss ratio of this typhoon is calculated to 59% and the decreased number of fruits is 2,950 (5,000 ⅹ 59%). The final loss ratio is 9.5% ( 2,950 / 10,000 – 20%) and the final insurance payment will be 950 dollars. In the case of typhoon, the decreased number of fruits is accumulated every time a typhoon occurs until the termination of the contract. So, if another typhoon occurs at the same field, the loss adjuster will conduct the same investigation. In the event of gale or strong wind, the same investigation that is used for typhoon will be conducted.

Now, the example of damage by hail will be explained. Suppose the hail occurs before thinning out to an apple crop insurance, the standard number of fruits is 100,000, and the number of fruits after thinning out is 60,000. When the contractor reports the damage to the local Nonghyup branch, the crop insurance manager assigns a loss adjuster to the field. The loss adjuster visits the field and investigates the hit ratio of young fruit. The loss adjuster selects the sample trees in accordance with the sample tree table. The sample tree table by crops shows the proper number of sample tree. The loss adjuster selects four branches on each sample trees and extracts over 5 young fruits or flower buds on each selected branches. On one tree, total 20 young fruits or flower buds will be searched. If the loss adjuster selects 10 sample trees, total 200 young fruits or flower buds will be investigated. If 100 out of 200 young fruits get damaged by hail, the hit ratio of the young fruits is 50%. So, the final decreased number of fruits by hail before thinning out will be 28,571.

Calculated detail : 50% ⅹ 10/7 ⅹ 40,000 (decreased number of fruits : 100,000 – 60,000) = 28,571

All claims by hail will conduct an additional investigation of damage right before harvest. When the young fruit is too small to see the flaw or crack by hail, the damage is not recognized by the loss adjuster. As the tree grows, however, the fruits get damaged cracks or flaw on its face. So, the loss adjuster will investigate the damage ratio of the fruits right before harvest. The loss adjuster selects the three sample trees and extracts all fruits on the trees. And then categorizes the extracted fruits into 100% damaged, 80% damaged, 50% damaged, and non-damaged fruits. From this process, the loss adjuster gets the loss rate and calculates the final loss number by multiplying the loss rate by the number of final harvest fruits.

The example of multi peril crop insurance is explained. Suppose that the crop is jujube, the amount insured is 15,000 dollars, the standard harvest weight is 1,600kg, the deductible rate is 20%, and the number of the jujube trees is 350. If the typhoon occurs, the contractor visits the local Nonghyup branch for reporting the claim. The insurer assigns the loss adjusting team to the damaged area. The loss adjuster visits the field and checks the damage. Multi peril crop insurance system does not count the number of fallen fruits. Instead, the loss adjuster just checks the types of natural disaster. When its harvest time, the loss adjuster visits the field and measures harvest weight. To measure the weight, the loss adjuster selects the sample trees in accordance with the sample tree table. And then, the loss adjuster picks all apples and weights them. The loss adjuster divides the measured weight by the number of used trees and it gives us the weight of harvest jujubes from one trees. Let’s suppose that the harvest weight of one jujube tree is 1,250g. So, the total measured harvest weight could be estimated to 437.5kg(1,250g ⅹ 350). The loss rate would be 72.7%(1 - 437.5 / 1,600) and the final loss rate would be 52.7% which reflects deductible rate(20%). So, the insurance payment would be 7,905 dollars(15,000 ⅹ 52.7%).

The representative loss assessments examples in Korea’s agricultural insurance are explained above. There are much more loss assessments methods by the types of crop, disaster, and period. NongHyup property and casualty insurance corporation is trying to improve claim adjustment system to provide direct help for farmers. But, sometimes the contractor files a civil complaint about the process of loss assessment or insurance payment. In this case, the contractor files a civil complaint through a phone call, mail, the internet, visiting directly to the head office, or using Financial Supervisory Service. When the civil complaint is reported, the crop insurance manager in the head office examines the case with the loss adjuster that was in charge of the case in the past. The crop insurance manager compares the civil complaint with the past similar cases or requests an investigation about the crop and disaster to the related institution or professor who researches the agricultural field. When the crop insurance managers finish the all examination about the case, the insurer gives notice to the contractor about the result. The insurer puts forth a multilateral effort to reduce an incidence of civil complaint.

5. CONCLUSION

Korea’s agricultural insurance has grown rapidly in a short time. It covers 50 crops as of 2016 and the insurer plans to expand crops steadily. In addition, the insurer will improve the agricultural insurance from the covering decreased amount to the covering decreased income for famers. Currently, the insurer applies ‘Revenue Protection’ which preserves the farmer’s decreased income to some crops as a pilot project. The insurer will expand the Revenue Protection to more crops and improve the insurance system. Also, the insurer tries to keep stable loss assessment system of crop insurance. So, with this system, even if a huge natural catastrophe occurs in South Korea, the farmer could keep stable farming management.

Table 1. Farmer adjuster’s loss assessment training

Year

Trainees

Training

2014

2,930

30

2015

4,548

32

2016

3,688

28

Totals

11,166

90

Table 2. Farmer adjusters in 2015

Number

%

Advanced

294

2.2

Farmer

12,757

94.9

Supporter

393

2.9

Fig 1. The picture of damaged flower and flower bud by spring frost

Fig 2. The picture of damaged pear field by typhoon

Fig 3. The picture of damaged young fruit by hail

Fig 4. The picture of the weighing multi peril fruits(grape, peach, plum)