Nik Rozana Nik Mohd Masdek*, Tengku Mohd Ariff Tengku Ahmad* and Abu Kasim Ali*

*Economic and Technology Management Research Centre, MARDI Headquarters, Malaysia

e-mail: nrozana@mardi.gov.my

ABSTRACT

This paper evaluated the prospects of further agricultural trade liberalization for Malaysia and the world in general. It traced agricultural trade trends and performance over the last three decades and discussed their association with trade liberalization. Analyses showed that in recent times, developing countries' agricultural trade had become more significant and grew at a much faster rate as compared to the developed countries although the latter still dominated global agricultural trade. Key agricultural trade indicators for Malaysia showed relatively better performance as compared to regional and global performances. In conclusion this paper recommended for Malaysia to continuously pursue for a more liberalized global market while at the same time liberalized its own agricultural market taking into considerations the sensitivities it faced and the flexibilities it needed.

Keywords: Malaysia, agricultural trade liberalization, trade performance, sensitivities

Introduction

Agricultural products are the most sensitive products across all global initiatives to liberalize trade. It was not until the Uruguay Round (UR Round), which started in 1986 that agricultural products were on the table for multilateral negotiations to be liberalized under GATT. After eight years of negotiations (1986 - 1994), the UR Round was successfully concluded. This led to the formation of the World Trade Organisation (WTO) to replace GATT. One of the important agreements that the UR Round had successfully negotiated was the "Agreement on Agriculture" (AoA). Under this Agreement, WTO member countries agreed to reduce trade distorting support and protection in the three main "pillars" consisting of domestic support, market access and export competition. However, post WTO analyses showed that agricultural markets across the world remained highly distorted despite the cuts in protective measures under the AoA. Subsidies in developed countries remain high and market access from developing countries into developed country markets for important agricultural products remain restricted. Developing countries in return are hesitant to further lower the high tariffs and relax other borders measures to liberalize their import regimes. This led to a stalemate in the current Doha Round Negotiations (launched by WTO Ministers in 2001), a around that is supposed to further liberalize world trade and improve the terms of agreements for developing countries.

Despite the "less than expected" cuts in the trade distorting support resulting from the UR Round Agreement and the stalemate of the Doha Round, analyses showed that, trade performance, especially that of developing countries markedly improved in the 1990s and 2000s. Developing countries' total merchandize export shares increased from 30.3% in 1980 to 58.5% in year 2010, surging from a low of 24.1% in 1990 (Michalopoulos and Ng, 2013). The same analysis also showed impressive gains in South-South trade and better integration of the developing economies after the UR Round in world trade (as measured by the ratio of total trade and GNP). It cannot be denied that trade liberalization initiatives significantly contributed to better world trade performance. According to Taylor and Fairchild (2000), one of the main factors that influenced trade in agriculture, especially that of fruits and vegetables was the "change in trade policies resulting from the AoA and regional preferential trading arrangements". Although the Doha Round talks of the WTO had stalled, but the fact that it had stalled, led to a proliferation of plurilateral and bilateral free trade agreements (FTAs). Governments just cannot wait for a comprehensive multilateral trade deal anymore. As reported by the WTO, currently there is a total of 575 FTAs that were notified to the WTO of which 379 are in force. Many of these FTAs are signed after 1995. This in itself is evidence of the bullish expectations by governments across the world on the benefits of freer trade. As shall be shown in this paper, the overall scenario and prospects would be similar for Malaysia which had from the early days depended on international trade for growth and prosperity.

Global Trends and the Role of Developing Countries in World Trade

World agricultural trade exhibited strong growth during the last decade, expanding from US$488.4 billion in year 2000 to more than US$2181 billion in year 2010, registering an annual growth rate of around 10%. This was a much higher rate as compared to 3.3% and 2.2% respectively for the 1980 - 1990 and 1990 - 2000 periods (FAOSTATS). One of the important factors contributing to this growth had been the “acceleration of globalization" which was characterized by a rapid decline in international trading costs, developments in ICT and reductions in government distortions in agricultural trade (Anderson, 2010). World agriculture before the reforms was typified by huge subsidies and protection by developed countries as well as “market insulations” by developing countries. Though these remained high today, significant cuts in subsidies and protection as a result of trade agreements had led to relatively freer market. This freer market had in turn stimulated higher trade in agricultural products and consequently resulted in better integration of the developing economies into the international trading system.

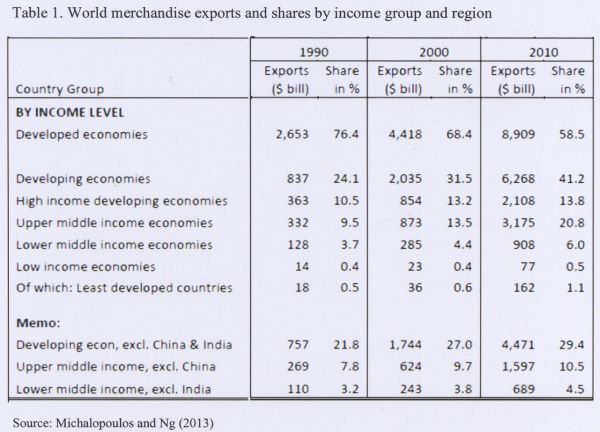

Michalopoulos and Ng (2013) showed that overall export shares of developing economies increased from 24.1% in 1990 to 41.2% in 2010, an increase of over 70 percentage points over the 20-year period. Meanwhile the share of the developed countries dropped from 76.4% to 58.5% during the same period (Table 1). Similar trends could also be observed or imports albeit at lower rates as compared to exports.

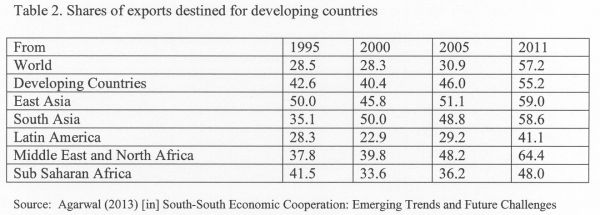

It was also noted for the period that the share of developing countries' exports to other developing countries had also been expanding significantly from 42.6% of total exports in 1995 to over 55% in 2010 (Table 2). Proportionately the share of developing countries exports to developed countries has decreased.

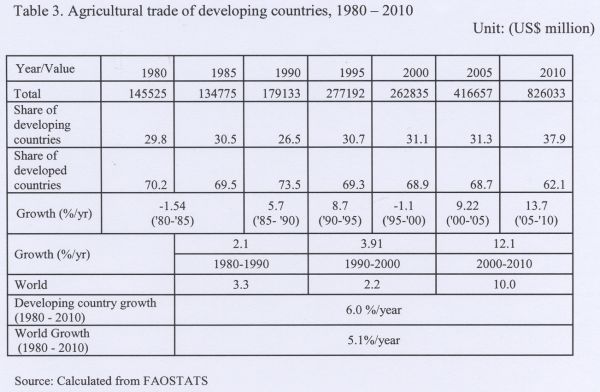

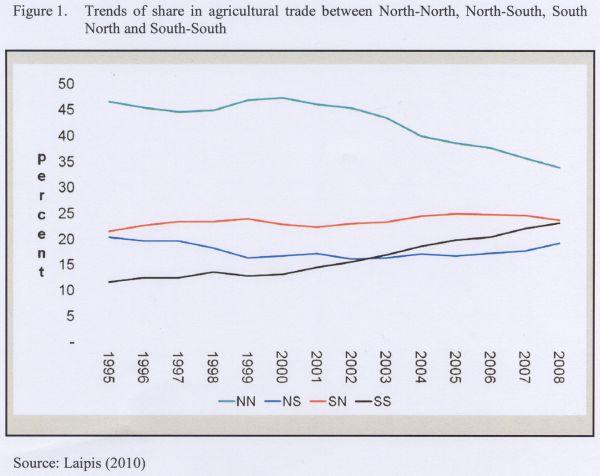

Growth in trade for agricultural products for developing countries was also higher than the overall global growth. The rate in growth was also highest for the 2000 - 2010 decade where expansion in growth in agricultural products for developing countries grew at more than 12% (Table 3). Corresponding with the faster rate of growth registered by developing countries, the share of developing country trade in world agricultural products also rose by more than 11% from its low of about 26.5% in 1990 to more than almost 38% in 2010 (Table 3). Analyses by Laipis (2010) also showed developing country markets were getting increasingly diversified as compared to before. He also showed that trade among developing countries or more popularly known as South-South was not only expanding and was increasingly South-South. On the other hand, the share of North-North trade in agricultural products was getting lower while that of North-South trade has almost stagnated (Figure 1).

Malaysia’s Agricultural and Trade Policy

Agricultural policies were generally designed to balance the economic, social and political objectives of the State that saw a combination of fairly liberal policies for many of the agricultural industries while instituting some protectionist measures for some industries. In this section Malaysia's agricultural and trade policies are briefly described to provide an understanding the evolution of the country's policy from the early days since independence till the present day. One could then relate this to Malaysia's economic development as well its integration into the international trading system. Most of this section had been described and taken from Tengku Ariff (2010).

Earlier policies

The legacy of plantation crops such as rubber and oil palm started very early during the British era before independence. Since then, this subsector has been the pillar of Malaysian agriculture. Relative to other subsectors, plantation crops received more emphasis in terms of budget allocation, development programs as well as other government support during the early phases of agricultural development. The only other crop that received attention is rice. Being the staple and a "poor man's crop" it has a unique status in society as a strategic crop for food security with embedded programs to enhance farm income and alleviate poverty among its producers.

Policies and programs in the early stages of development mainly addressed to enhance income of agricultural producers in order to reduce the incidence of poverty in agriculture and to minimize inter-sectoral disparity and inequity between agriculture and non-agriculture. Hence, agricultural development strategies in the 1960s and 1970s mainly focused on the objectives of reducing poverty, providing rural employment and enhancing agricultural incomes. They were also export oriented to earn foreign exchange. Plantation crops for exports mainly rubber, oil palm and cocoa were actively promoted while a number of the food subsectors were protected to mainly insulate producers and save foreign exchange in line with the import substitution strategy during this period. A few of these support and protection are still in existence until this day though many of them had been dismantled in line with liberalization. These liberalization initiatives mainly started with the introduction of the first National Agricultural Policy (NAP, 1984). Productivity, efficiency and competitiveness were the main focus of the policy. Development efforts in the sector were consequently then geared towards modernization and commercialization. Downstream and value-added agricultural industries were emphasized and encouraged by providing highly attractive incentives such as tax breaks and export rebates. Tariffs on agricultural products were reduced and many were abolished to make imports of raw materials cheaper to reduce input costs for the downstream industries. This move was also to prepare the sector for increased competitiveness by allowing the “discovery” of specialized agricultural product niches through comparative and competitive advantages.

This was followed by the National Agricultural Policy 2 (NAP2), 1992 - 2010 which basically continued and further strengthened the policies in NAP 1. During this period of the 1990s, when the global economy was in a “bull-run” spurred by manufacturing demand from developed countries, Malaysia’s share of manufactured exports rapidly rose from 58.8 % in 1990 to almost 80% in 1995, where it remained in the 2000s. Share of agriculture meanwhile dropped from 22.3 % to just 13.1% during the period, and to 7% in 2005. It was during this period that many developing country governments, Malaysia included neglected agricultural development. Budgetary allocation, human resource and infrastructural development as well as other important requisites for agricultural growth were no longer given emphasis. This period of the “roaring nineties” as described by Stiglitz (2003), had made Malaysia complacent on the importance of growing one’s own food. The popular mantra was that “we can always buy what we want”.

Recent policy development

The Asian Financial Crisis (AFC) of 1998 was a wake-up call for the government on the importance of not being too dependent on imports for food. Domestic food prices escalated resulting from higher import costs as the domestic currency seriously depreciated. Riots in a neighboring country due to food shortages and unaffordable prices led to the fall of the Government. In Malaysia, social discontent was rising. This development led the Malaysian Government to review the second National Agricultural Policy. This gave birth to the Third National Agricultural Policy (1998 – 2010).

The Third National Agricultural Policy (1998 – 2010)

In the NAP3, as it is popularly known, policies, strategies and initiatives to transform and revitalized the sector were specified. The importance of food production and SSL was re-emphasized and “meeting national food requirements” was the first of the five strategic thrusts of the NAP3. Another important strategy was to enhance and strengthen the requisite foundation of agricultural development, especially for the food subsector. This include among others, physical infrastructure, finance, human resource and technology.

Malaysia's trade policy

Trade policies in Malaysia follow closely the sectoral development policies where national development agendas were embedded.

Main components of Malaysia’s agricultural trade policy

Being a trade oriented economy, external trade is of great importance to the development of the Malaysian economy and Malaysia places high importance on a strong, open and viable trading system (GATT, 1993).

The overall trade-related policy’s aim is to promote and safeguard Malaysia's interests in the international trade arena, to spur the development of industrial activities, and to further enhance Malaysian economic growth towards becoming a developed nation by year 2020 (Vision 2020). Specifically, Malaysia's trade policies are intended to: improve market access for goods and services; promote the global competitiveness of its exports; expand and diversify trade with existing trade partners; and explore new markets (WTO, 2010). At the same time, as was earlier mentioned, Malaysia supported a number of agricultural industries for strategic and socio-economic reasons including for food security, rural development and alleviation of poverty. The “infant industry” argument was also used to justify some of this support.

The trade regime for agriculture Overall, Malaysia has a liberal trade regime with low tariffs for most products. The simple average applied MFN tariff was 7.4% in 2009 while more than 60% of the products are duty free. As early as 1985, FAO observed that even for the so-called “protected subsectors” in Malaysian agriculture, such as the tropical fruit industry, which attracted a tariff of RM661 per ton for many imported fruit types, the tariff was still among the lowest in the region (FAO, 1985). Present tariffs on agricultural imports are generally low, averaging at 2.8% in 2009 (WTO, 2010), down from 3.2 % in 2005 and from 10.4 % in 1993. The lowering of the tariffs was in fact a necessity that benefits downstream agricultural value adding activities through the imports of cheaper raw materials and intermediate agricultural products.

Other industries that are still accorded policy support are paddy and rice, specific livestock subsectors, tobacco and tropical fruits, coffee and cabbages. It is in these sub-sectors that most of the non-ad valorem tariffs are still maintained and non tariff measures still in place. However, of late, many of these fixed tariffs had been done away with except for some of the sensitive products such as alcoholic beverages. With the ASEAN Free Trade Area, the import tariffs on most of these products are now down to only 5% within ASEAN, though TRQs are still in place for a small number of products.

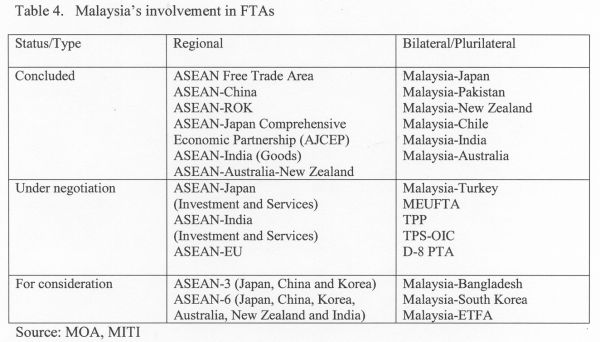

Malaysia's involvement in Free Trade Agreements

Malaysia joined GATT (General Agreement on Tariff and Trade) in 1957, the immediate year it obtained independence from the British. It was one of the earlier members to join the organization, underscoring the importance of international trade accorded by the founding government of the country. This policy remains till this day. GATT itself was formed in 1948 to oversee the multilateral trading system. During GATT, governments that signed GATT were called "GATT Contracting Parties". Upon conclusion of the UR Agreement these Parties became members of the WTO which was formed in 1995 to replace GATT. Being a GATT member, Malaysia became one of the 128 founding members when the WTO was formed. Its membership had since increased to 159 countries while another 24 countries are negotiating to accede and become members of the WTO.

While Malaysia continues to accord high priority to the rule-based multilateral trading system under the WTO, the country also pursued plurilateral, regional and bilateral trading arrangements to complement the multilateral approach to trade liberalization. Free Trade Agreements (FTAs) are generally aimed at providing the means to achieve quicker and higher levels of liberalization that would create effective market access between the participants of the FTA. Table 4 below presents Malaysia’s involvement in FTAs (further details can be seen in Appendix A).

The continued involvement and pursuance of Malaysia in free and preferential trade agreements proved the commitment of the country for freer trade. It also underlined the belief and importance of outward looking policies in achieving national, regional and global growth and firmly supports the fact that international trade is a fundamental requisite that formed one of the critical foundations of the economy.

Malaysia's overall agricultural trade performance

Malaysia has consistently maintained its position as one of the top 20 trading nations in the world. Since 1998, Malaysia reported consistent trade surpluses. Total trade for 2012 surpassed the one trillion ringgit mark with a value of RM1.31 trillion compared with RM1.27 trillion recorded in 2011.

The balance of trade as reported by the Malaysian Department of Statistics recorded a trade surplus of RM5,080 million, as of March 2013. Historically, from 1970 until 2013, Malaysia’s balance of trade averaged RM2,820 million, reaching the highest point of RM15,767 million in May 2008 and the lowest point of a deficit of RM2,881 million in June 1997. The main exports consisted of electrical and electronic products, palm oil, petroleum products, liquefied natural gas, timber and natural rubber. Malaysia also sends abroad chemicals, machinery, appliances and manufactures metals. Meanwhile, the country’s main imports consist of machinery and transport equipment, manufactured goods, fuel and chemicals.

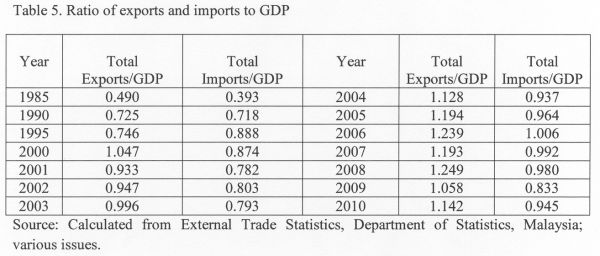

Increased liberalization of the world trade environment, coupled with the increased opening of the Malaysian market, had made international trade more important to the Malaysian economy. Over the 1985-1995 period, the ratio of total exports to total GDP increased from 0.49 to 0.75 (Table 5). The ratio of imports to GDP also exhibited a similar trend, rising from about 39% of GDP to 88% during the period. These ratios further increased in the 2000 - 2010 decade from 1.05 to 1.14, reaching a high of 1.25 in 2008 for exports and from 0.87 to 0.95 for imports. These increasing ratios showed how well integrated the economy is in the international trading system as well as the growing importance of external trade to the Malaysian economy.

Agricultural trade

Total trade for Malaysian agricultural products showed steady growth for the past two decades. Total agricultural trade grew at the rate of almost 9.8% per annum for the period 1991 - 2010. Both imports and exports grew the same rate of also 9.8% per annum during the period. However, the 2001 - 2010 period saw a period of distinct growth in agricultural trade for Malaysia. Exports of Malaysian agriculture grew at almost 19% per annum from US$5.5 billion to almost US$26.0 billion, edging imports which grew at 15% per annum, from US$4.0 billion to US$14.0 billion (Table 6). This is despite the Global Financial Crisis (GFC) of 2007 - 2008 that hit both Europe and America. The robustness of Malaysian agricultural exports once again demonstrated the resilience of Malaysian agriculture to external shocks as was the case during the Asian Financial Crisis (AFC) of 1997 - 1998.

This AFC witnessed the melt down of Asian currencies including the Malaysian Ringgit and resulted in lower export earnings. This explained the slow growth in agricultural trade during the 1991 - 2000 period, which only grew at the rate of only 3.9% per annum. Table 6 also showed that exports slowed down to only 3.1% during the period. Lower value of the Ringgit caused imports to grow faster than exports, at 5.2% per year. Both average imports and exports between the two periods jumped by 2.2 times in trade value. This better performance of international trade by Malaysia in the later decade is most likely a result of increased trade liberalization between Malaysia's important trading partners such as the ASEAN FTAs and its bilaterals (Table 6).

The increasing importance of agricultural trade to the Malaysian economy can be seen in Table 7. The ratio of total agricultural trade to agricultural GDP had steadily increased form 1.19 in the year 2000 to 1.60 in 2010. This indicated that Malaysian agriculture has become more trade oriented. If one was to separate the overall agricultural trade ratio into ratios of exports and imports to agricultural GDP, it is shown that the ratio of agricultural exports to agricultural GDP were consistently higher than the ratio of agricultural imports to agricultural GDP. This indicated that the sector was more export oriented than import oriented. It export orientation has also been increasing over the 2000s from a ratio of 0.72 in year 2000 to more than 1 in 2010 (Table 8). Since 2003 the ratio of exports to GDP has always been above 0.9 while starting 2008 the ratio has been consistently at about 1.0. These stronger export GDP ratios as compared to import GDP ratios could also indicate the competitiveness of Malaysian agricultural exports and hence, overall should be able to continue to benefit from increased agricultural trade liberalization world wide.

Direction of Agricultural Trade

A study by Tengku Ariff (1998) for the period of 1985-1996, observed that Japan, the USA the EU and ASEAN, particularly Singapore, were among the major markets for Malaysia products. Together they accounted for more than 75% of Malaysian exports for the previous two decades. Singapore, USA and Japan together have consistently accounted for more than 50% of total exports. Thus, the Malaysian export market remained highly concentrated with limited progress being made in market diversification. The direction of imports was also similar, with Japan, Singapore, USA and the EU being the major source of Malaysia’s imports. The trend showed that there was also an increased concentration in the sources of Malaysia’s imports. The study, on the other hand, showed that trade in agriculture was more successful in terms of diversification. The 10 major export destinations for Malaysian agricultural products were Japan, Singapore, USA, China, Hong Kong, Korea, the Netherlands, Thailand, Taiwan and Pakistan. There was a decrease in concentration of exports to these countries from 64% of total agricultural exports in 1985 to 54% in 1995. For agricultural products, the Asian market became increasingly important with China and Pakistan displacing USA in the top five export destinations. The sources of agricultural imports also became less concentrated.

.jpg)

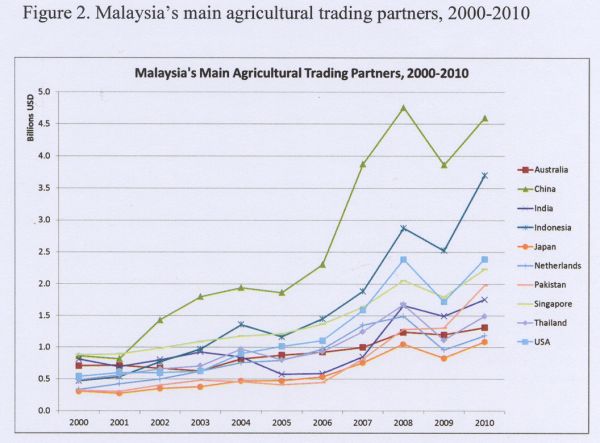

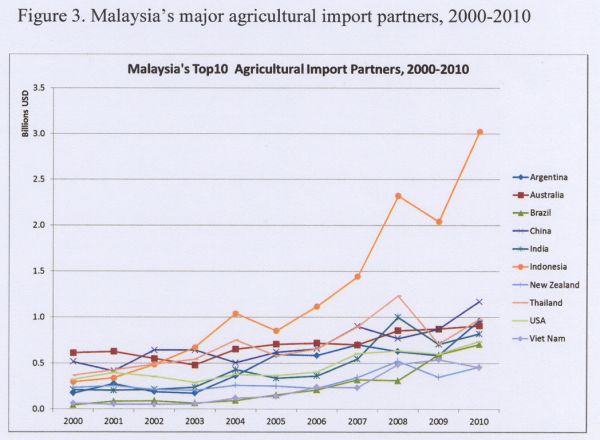

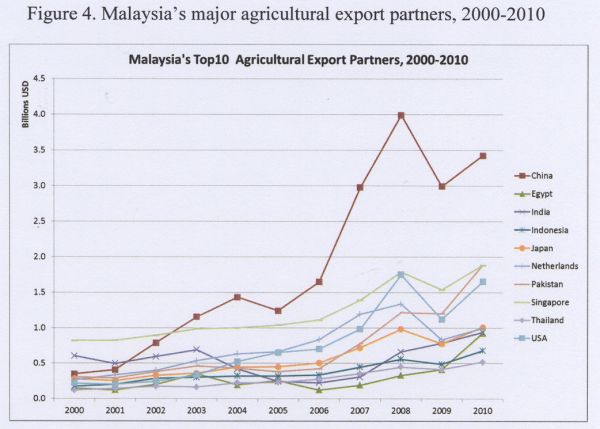

Meanwhile, observing the more recent trend for the year 2000-2010 (Figure 2), the country’s top 10 agricultural trading partners are China, Indonesia, Singapore, Thailand, the US, Australia, India, Japan, the Netherlands, and Pakistan. Figure 3 exhibits the nation’s agricultural import trend for the same period. Starting from 2003, Indonesia became a leading source for Malaysian agricultural imports, and it continues to show tremendous increase until recently. On the other hand, in the early years from 2000, Singapore was Malaysia’s leading agricultural export destination (Figure 4). Eventually, China took over as Malaysia’s major agricultural export destination from 2003 onwards, maintaining the increasing importance of the Asian market in the top five export destinations. This trend again signifies the importance of developing country market expansion, the South-South trade, for exports from developing countries. Malaysian agricultural exports certainly benefited from their expanding import demand.

Malaysia’s agricultural trade vis-à-vis ASEAN and the world

This section further analyzed the growth trends of Malaysia’s agricultural trade as compared to ASEAN and the world for the 1986 – 2010 period. The period were divided into five-year-periods as in Table 9. A simple comparative analysis was made to indicate the trends and levels of trade that took place before and after WTO and AFTA came into force. For this purpose, the periods were divided into two, pre-WTO and AFTA (1986-1995) and post-WTO and AFTA (1996-2010).

.jpg)

Malaysia’s total trade during the 1986-1990 periods averaged US$ 6.1 billion, with growth of around 8.6% which is comparable to ASEAN and the world’s growth. However, the following five-year periods (1991-1995) prior to coming into force of WTO/AFTA, its total trade recorded a trade average of US$ 8.8 billion and growth of 14.4%. The nation’s trade growth was slightly higher than ASEAN’s and well above the worlds’ average.

Conversely, in the early years after WTO and AFTA were in place, there was a major drop in Malaysia’s trade growth rate, registering a negative growth of -5.97% per annum. ASEAN and the worlds’ trade growth were also negative, albeit not as bad as Malaysia’s. This demonstrated that being a trading nation, the years during global recession really affected our economy. However, this period could be considered an “abnormal period”, a period of the Asian Financial crisis, where as pointed earlier, the Malaysian Ringgit fell by as much 50% during the peak of the crisis in 1998 before the government instituted the fixed exchange rate of RM3.80 to the US dollar. Nevertheless, when the economy is thriving, Malaysia recovered better in terms of its trade growth. Recent years saw a notable improvement in the country’s total agricultural trade from about US$ 16.7 billion in 2005 to almost US$ 40.0 billion in 2010, registering a growth of 17.48%. Despite the short-term external shocks such as the AFC and the GFC the Malaysian agricultural trade registered a robust long term growth of more than 9.4 percent year for the 1986 – 2010 period. Also, during the period Malaysia’s agricultural trade market share increased from 0.95% to 1.83% of world agricultural trade, while its five-year average trade increased by almost 8.7 times for the 1986 - 90 period as compared to the 2006 - 2010 period. Most of this increase in share could be atributed to its exports rather than imports.

ASEAN fared almost similarly at the same rate as Malaysia. Its total agricultural trade increased during the pre-liberalization era from an average of US$ 24.5 (1986-1990) to US$ 38.8 (1991-1995). There was then the same drop whereby ASEAN’s trade growth slowed down to -5.37% per annum during 1996-2000, although the average trade for that period did register an increase. The later decade after the liberalization initiatives saw ASEAN’s trade expanded from US$57.3 billion to US$125.9 billion, an improvement of more than twice the worlds’ average.

The "Offensive" and "Defensive" perspectives

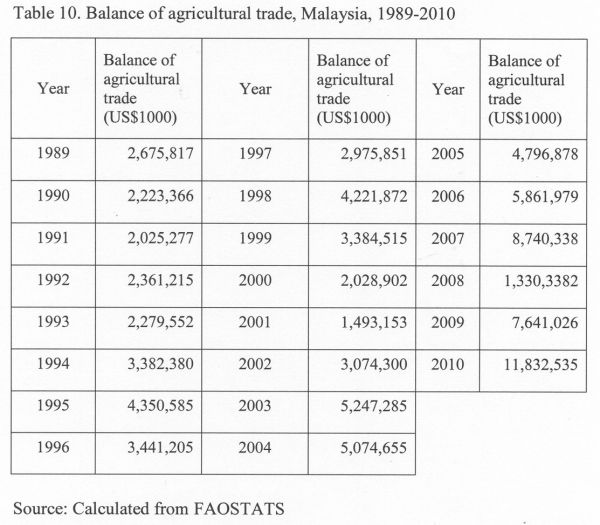

The trends and indicators for Malaysian agricultural trade conducted in the preceding sections all indicated that Malaysia has benefited from a more liberal agricultural trade regime world-wide. Its agriculture had become more trade oriented in nature, its growth in agricultural trade had surpassed that of the region and the world and more importantly, its agricultural balance of trade (BOT) was not only consistently positive but had widely increased over time. Since 1989, the BOT had increased by nearly 4.5 folds, from RM2,676 million to RM11,833 million, growing at an average rate of 7.3% per annum (Table 10). A better liberalized world, as such, holds a promise of a better agricultural economy for Malaysia. On this premise, Malaysia has been a strong advocator of freer trade in agriculture. Opening of agricultural markets seemed highly beneficial to Malaysia.

However, policymakers had been more cautious in pushing "too much" liberalization in agriculture lately due to the reciprocal response it has to similarly undertake. Although the agricultural trade BOT had been positive and increasing for the last 30 years, this positive BOT was mainly accounted by a narrow based agricultural export, led mainly by palm oil and rubber. Malaysia is still a net importer of food (discounting palm oil). Figures released by the Department of Statistics, Malaysia showed that the deficit in food trade has increased from RM5.3 billion in 2000 to RM7.5 billion in 2005 and further widened to more than RM12.0 billion in 2010. Major food group deficits in 2010 came from feedstuffs (RM3.70 billion), cereals (RM2.80 billion), sugars and preparations (RM1.92 billion), vegetables (RM1.68 billion), meat and meat products (RM1.3 billion), fruits (RM722 million) and milk and milk products (RM662 million). Hence while Malaysia has a strong offensive interests in its commodity exports, it also has defensive interests in its food sector. Furthermore, producers in the food sector in Malaysia are primarily smallholders where socio-economic considerations such as income, poverty alleviation, food security as well as rural development objectives need to be balanced with economic growth and trade. This is more so in the rice subsector, where national food security considerations usually take priority.

.jpg)

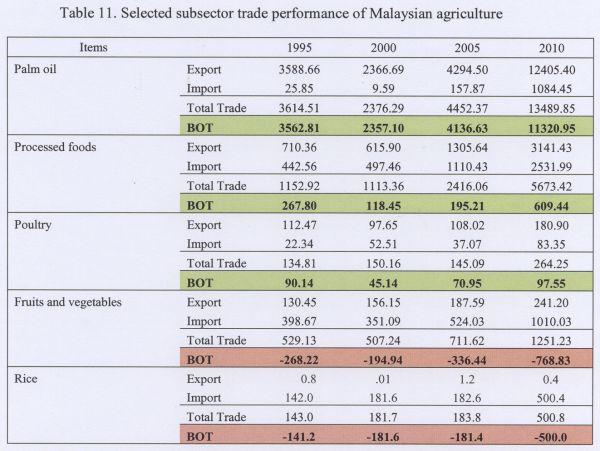

Table 11 shows the import and export performances of five subsectors in agriculture with three of them registering positive BOTs while two of the subsectors exhibiting negative BOTs. Of the five selected agricultural products, it can be clearly seen that palm oil constituted the largest BOT. During the 15 year period its BOT increased from RM3.6 billion to more than RM11.3 billion. Obviously the dominance of palm oil exports is the main factor that resulted in the overall positive BOT for agriculture.

The poultry and processed food subsector both reported a positive BOT during 1995 until 2010 (Table 11). However, comparing between 1995 and 2000, there was a slight decrease in each of the respective total exports. Meanwhile, between 2005 and 2010, both subsectors saw a commendable increase in its total trade, from US$ 145 million to US$ 264 million, and from US$ 2416 million to US$ 5673 million, respectively. While Malaysia is moving rapidly towards industrialization, processed food production will continue to become more important. Processed food demand including for both domestic consumption and exports are expected to expand as consumer preference changes and incomes and standard of living increases.

The exports of fruits and vegetables increased at a steady rate. However, it registered a negative BOT throughout the observed period, due to the fact that Malaysia still depends heavily on imported fruits and vegetables, especially for the temperate types. As the data shows, the country’s dependency on imports of fruits and vegetables increased profoundly from US$ 524 million in 2005 to almost double, valued at around US$ 1,010 million in 2010. The imports of rice, the staple food also increased significantly, resulting in expanding trade deficits from US$141 million to US$500 million during the same period. These higher imports remained a sensitive public and political issue as Malaysia continues to grapple to find an appropriate and feasible ratio balance of national self-sufficiency and imports for rice. Producer prices are supported as part of the "small producer income enhancement" program to allow them to stay in rice farming and face cheaper imports, which are also regulated by the government.

The future of agricultural trade

The conclusion of the UR Round of negotiations that led to the formation of the WTO in 1995 was welcomed all around the world. Expectations were high. This was more so for the developing countries. For the first time in history, policy limits and ground rules for global trade in agriculture were established. Trade distortions were to be reduced over eight

years for developing countries and six years for developed countries. There were huge cuts expected in agricultural subsidies in developed countries which had for years displaced farmers in the developing countries. At the same time, developing countries were also committed to open new market opportunities for products from the developed countries by reducing import tariffs, quantitative restrictions and other non-tariff barriers. Trade was then to be the main vehicle for global growth and prosperity. However during the implementation period of the WTO, developing country members realized that they were ill equipped in many aspects to enjoy the benefits of the WTO and that protection, support and agricultural subsidies remained high in the developed countries. The playing field remained unlevelled.

Return to protectionism?

As the above weaknesses were uncovered, the first post WTO multilateral negotiating round was launched in 2001 to negotiate a new and improved terms for all members. The Doha Round as it is known, was to be a "development round", a round to give better terms for the developing countries, especially for agriculture. After 12 years, this Round is almost "dead" with no conclusion foreseen in the near future. The stalemate of the Doha Round has placed doubts on the ability of the WTO and the multilateral trading system to enforce a truly fair global trading based on the rules-based system. Many developing country governments and even members of advance economies such as the G10 Group1/ in the WTO seemed to be reverting back "protectionist positions" on the negotiating table. The failure of the Doha Round can primarily be attributed to this hard stand on agriculture. Issues regarding food security and poverty, rural development, the welfare of small farmers as well as the demands of the big agricultural exporters for deeper access to markets of the developing economies held back the progress of the Doha Round. The protectionist sentiments were further exacerbated by the food and fuel crisis in 2008 that again fuelled riots and social discontent in many developing countries. It will be unfortunate if the world would revert back to the protectionist measures of the past that would negatively affect international trade and agriculture and overall economic growth. This would a loss to global economic welfare affecting both developing and developed countries.

Without concrete research, it is not known how much more liberalization of agricultural trade have taken place as a result of the numerous FTAs that have been signed world-wide that is over and above the WTO, the so called WTO plus measures. Nevertheless, our suspicion it was not much. Most of these FTAs are not comprehensive and many agricultural lines were still excluded to cater for individual sensitivities. Furthermore, in most FTAs, only border measure issues were mainly addressed while domestic and export subsidies and other support that badly distort trade were not negotiated. These issues could only be tackled at the multilateral level.

A discussion on policy and trade prospects for Malaysian agricultural trade

Malaysia is a small trading nation that has depended on trade for its growth and prosperity. It needs to continue to depend on trade to accelerate further economic growth and generate higher incomes for society. It needs a viable and open global trading system which is predictable. The Government need to realize that as we desire increased openness and accessibility of markets from our trading partners, the same expectation is required of us. However, despite the need for more open markets, no nation including Malaysia can brush aside sensitivities be it socio-economics, religious and or political; or even just the sentiments of the majority. These sensitivities need to be carefully managed with proper "buffers" and safety nets, if appropriate. Longer adjustment periods and temporary exclusions that can be renegotiated are some of the possible options.

For Malaysia, the defensive interests in the agricultural sector that have been described earlier are important to be accorded some flexibility, some less and some more. In the rice subsector, for example, which can be considered as the most sensitive crop in agriculture due to host of sensitive elements, the most flexible liberalization process would be needed to provide comfort to all stakeholders. During the food and fuel crisis of 2008 Malaysia faced difficulties in sourcing its rice due to abrupt export bans and constrains imposed by Malaysia's "traditional rice trading partners". This has reignited the scepticism that "nations can depend on the international trading system at all times to deliver its need for food". It has been proven otherwise.

Other sensitivities including religious ones, such as liberalizing trade for wine and liquor as well as tobacco products (viewed as "sin products") also need to be extensively considered and understood by our policymakers as well as Malaysia's trading partners in designing future initiatives for freer trade. It is within this framework that we think the future of Malaysia's trade policies would continue to evolve. It would be beyond reason for Malaysia to fall back to inward looking and further protectionist policies that would pull back economic progress social prosperity that have been derived from international trade thus far.

CONCLUSION

The enthusiasm shown by governments towards freer trade as well as the come into force of numerous plurilateral and bilateral FTAs across political ideologies around the world showed the confidence they have in the benefits of freer trade. The WTO started with 128 founding members. Today its membership is up to 159 countries, and even as the Doha Talks stalled, there still more than 20 countries that are applying and awaiting accession to join the WTO. Almost every nation seems to believe freer markets is the way forward for global prosperity. The common issue that confronts them is how to get there as smooth as possible and to minimize the "negative shocks" to those affected by the new rules and measures. For Malaysia, there should be no looking back but to continue to promote and pursue fairer and freer trade among nations. With a merchandize trade to GDP ratio of almost 140%, Malaysia's capability to spur growth from within would be relatively more difficult and the economic backlash of a slowdown in international trade would be deep. Even the big domestic economies such as the USA and China with merchandize trade to GDP ratios of around 25% and 50% respectively, would experience the consequences of a global slowdown in international trade.

A more liberalized world trading environment is expected to be continuously sought by nations in their search for better economic welfare for their people. Being a small nation, Malaysia, more so, needs to persistently progress with this approach and outlook. To be economically secured as the trading order becomes more liberalized, it has no other option rather than to increase productivity and competitiveness of its industries, including agriculture. No food security assurance can be more assured than the competitiveness to produce and export one's own food. The importance of trade in assuring the liberty and self-security of a nation cannot be more reflected in the belief of the liberals that, "nations that trade do not go to war with each other".

REFERENCES

Anderson, Kym. 2010. "Globalization's effects on world agricultural trade, 1960-2050". Discussion Paper No. 1011, Centre for International Economic Studies, University of Adelaide, Adelaide, Australia. Retrieved from http://pandora.nla.gov.au/pan/20110418-1451 /www.adelaide.edu.au/cies/publications/present/CIES_DP1011.pdf

Agarwal, M. 2013. "South-South Economic Cooperation: Emerging Trends and Future Challenges". Background research paper Submitted to the High Level Panel on the Post-2015 Development Agenda. Retrieved from http://www.post2015hlp.org/wp-content/uploads/2013/05/Agarwal_South-Sout...

FAO. 1985. ‘Situation and Prospects of International Trade in Fruits and Vegetables in ASEAN countries’, RAPA Monograph 3185, Bangkok, Thailand.

FAOSTATS. 2013. Website http://faostat.fao.org/site/535/default.aspx

GATT. 1993. ‘An Analysis of the Proposed Uruguay Round Agreement, with Particular Emphasis on Aspects of Interest to Developing Economies’, Geneva.

Liapis, Peter S, 2010. Trends in Agricultural Trade. Presentation at the Joint ICTSD-FAO Expert Meeting, Geneva, Switzerland.

Michalopoulos, Constantine and Francis Ng. 2013. "Trends In Developing Country Trade

1980–2010". Policy Research Working Paper 6334, The World Bank Development Research Group, Trade and Integration Team. Retrieved from http://papers.ssrn.com/sol3/papers.cfm ...

Ministry of International Trade and Industry, Malaysia (MITI). 2008. Developments in the Implementation of the CEPT Scheme for ASEAN Free Trade Area. Retrieved June 10, 2013, from http://www.miti.gov.my/cms/content.jsp?id=com.tms.cms.article.Article_b5...

Stiglitz, J. 2003. The Roaring Nineties – Seeds of Destruction, London: Penguin Books Limited.

Taylor, Timothy G. and Gary F. Fairchild. 2000. "Competition and Trade in Fresh Fruits and Vegetables in the New Millennium". Paper prepared for presentation at the conference on Global Agricultural Trade in the New Millennium, New Orleans, Louisiana: May 25-26,

Tengku Ariff Tengku Ahmad. 2010. "Dimensions of Food and Livelihood Security of Agricultural Trade: The Case of Malaysia". Paper presented at The Multi-Country Research Dialogue on Emerging Economies In The New World Order: Promises, Pitfalls And Priorities, The The Indian Council for Research on International Economic Relations (ICRIER), New Delhi, India.

Tengku Mohd Ariff, T.A. 1998. Effects of Trade Liberalization on Agriculture in Malaysia: Institutional and Structural Aspects. Working Paper Series No. 34, CGPRT Centre, Bogor, Indonesia.

The World Bank Data. 2013. Website: http://data.worldbank.org

UN Comtrade. 2013. Retrieved from http://unstats.un.org/unsd/comtrade

World Trade Organisation 2001. “WTO Agriculture Negotiations: The Issues, and Where Are Now.”, Geneva, Switzerland.

World Trade Organisation (WTO). 2005. Trade Policy Review Body. Trade Policy Review Report by Malaysia, 1-11. Retrieved from http://www.fdi.net/documents/WorldBank/ databases/malaysia/Trade_Policy_Review_Malaysia.pdf

1/ Group consisting of Chinese Taipei, Rep. Korea, Iceland, Israel, Japan, Liechtenstein, Mauritius, Norway, Switzerland that call for agriculture to be treated as diverse and special because of non-trade concerns which effectively translates to cautious liberalization in agricultural trade

Appendix A:

Malaysia’s involvement in free trade agreements (FTAs) are briefly described d below:

a) Malaysia-European Union Free Trade Agreement (MEUFTA) - Malaysia and EU commenced the first round of negotiations on 6 Dec 2010 in Brussels, Belgium. A total of 13 Working Groups have been established to negotiate on various issues. In 2011, total trade between Malaysia and the EU amounted to RM132 billion, recording an increase by 7.4 per cent with exports valued at RM72 billion (an increase by 4.7%) and imports accounted for RM60 billion (an 11.0% increase).

b) Malaysia-Turkey Free Trade Agreement (MTFTA) - established on 8 November 2007 and came into force on 1 January 2008. The MPCEPA encompasses liberalisation in trade in goods and services, investment, as well as bilateral technical cooperation and capacity building in areas such as SPS measures, intellectual property protection, construction, tourism, healthcare and telecommunications. Under MPCEPA, both Malaysia and Pakistan will progressively reduce or eliminate tariffs on their respective industrial and agricultural products.

c) Malaysia-New Zealand FTA (MNZFTA) - Malaysia and New Zealand commenced negotiations on the bilateral FTA in May 2005. The MNZFTA negotiations were concluded on 30 May 2009 at the 10th round of negotiations in Kuala Lumpur and entered into force on 1 August 2010, with areas of cooperation in the sectors of education, forestry, health, manufacturing and biotechnology.

d) Malaysia-Chile Free Trade Agreement (MCFTA) – negotiations were concluded in May 2010, signed on 13 November 2010 and came into force on 25 February 2012. This is Malaysia's fifth bilateral and the first FTA with a Latin American country. The Agreement outlines commitments from both countries on liberalization of trade in goods. Malaysia and Chile will progressively reduce or eliminate tariffs on their respective industrial and agricultural products.

e) Malaysia-India Comprehensive Economic Cooperation Agreement (MICECA) – established on 24 September 2010 and came into force on 1 July 2011. It is a comprehensive agreement that value-adds to the benefits shared from ASEAN-India Trade in Goods Agreement (AITIG). Under MICECA, both Malaysia and India will progressively reduce or eliminate tariffs on their respective industrial and agricultural products whereby the commitments by both countries are reflected in its Schedule of Commitments.

f) Malaysia-Australia Free Trade Agreement (MAFTA) – concluded negotiations on MAFTA on 30 March 2012, and entered into force on 1 January 2013. It is a comprehensive agreement, which comprises 21 chapters encompassing trade in goods, services and investment as well as economic cooperation. MAFTA marks another important milestone in Malaysia – Australia economic relations, complementing the already established ASEAN-Australia-New Zealand FTA (AANZFTA).

g) Malaysia-Japan Economic Partnership Agreement (MJEPA) – established on 13 December 2005 and came into force on 13 July 2006. MJEPA is Malaysia's first comprehensive Agreement covering: trade in industrial and agricultural goods, trade in services, investment, rules of origin, customs procedures, standards and conformance, intellectual property, competition policy, enhancement of business environment, safeguard measures and dispute settlement.

h) Developing Eight (D-8) Preferential Tariff Agreement (PTA) – comprises eight Islamic countries, namely, Bangladesh, Indonesia, Iran, Malaysia, Egypt, Nigeria, Pakistan and Turkey. All eight (8) member countries signed the D-8 PTA at the Fifth D8 Summit on 13 May 2006 in Bali, Indonesia. Malaysia ratified the D-8 PTA on 20 July 2006. The PTA is designed to gradually reduce tariffs and other barriers to trade on specific goods in order to promote intra-trade among D-8 members.

i) Trade Preferential System - Organisation of the Islamic Conference (TPS-OIC) - implementation of TPS-OIC would enable Malaysian exporters to gain preferential tariff treatment for selected products in the markets of the participating countries and enable exporters to gain competitive advantage over similar products originating from non-participating countries.

| Submitted as a country paper for the FFTC.NACF International Seminar on Threats and Opportunities of the Trade Agreements in the Asian Region, Sept. 29-Oct. 3, 2013, Seoul, Korea |

Current Status and Future Perspectives of Agricultural Trade: The Case of Malaysia

Nik Rozana Nik Mohd Masdek*, Tengku Mohd Ariff Tengku Ahmad* and Abu Kasim Ali*

*Economic and Technology Management Research Centre, MARDI Headquarters, Malaysia

e-mail: nrozana@mardi.gov.my

ABSTRACT

This paper evaluated the prospects of further agricultural trade liberalization for Malaysia and the world in general. It traced agricultural trade trends and performance over the last three decades and discussed their association with trade liberalization. Analyses showed that in recent times, developing countries' agricultural trade had become more significant and grew at a much faster rate as compared to the developed countries although the latter still dominated global agricultural trade. Key agricultural trade indicators for Malaysia showed relatively better performance as compared to regional and global performances. In conclusion this paper recommended for Malaysia to continuously pursue for a more liberalized global market while at the same time liberalized its own agricultural market taking into considerations the sensitivities it faced and the flexibilities it needed.

Keywords: Malaysia, agricultural trade liberalization, trade performance, sensitivities

Introduction

Agricultural products are the most sensitive products across all global initiatives to liberalize trade. It was not until the Uruguay Round (UR Round), which started in 1986 that agricultural products were on the table for multilateral negotiations to be liberalized under GATT. After eight years of negotiations (1986 - 1994), the UR Round was successfully concluded. This led to the formation of the World Trade Organisation (WTO) to replace GATT. One of the important agreements that the UR Round had successfully negotiated was the "Agreement on Agriculture" (AoA). Under this Agreement, WTO member countries agreed to reduce trade distorting support and protection in the three main "pillars" consisting of domestic support, market access and export competition. However, post WTO analyses showed that agricultural markets across the world remained highly distorted despite the cuts in protective measures under the AoA. Subsidies in developed countries remain high and market access from developing countries into developed country markets for important agricultural products remain restricted. Developing countries in return are hesitant to further lower the high tariffs and relax other borders measures to liberalize their import regimes. This led to a stalemate in the current Doha Round Negotiations (launched by WTO Ministers in 2001), a around that is supposed to further liberalize world trade and improve the terms of agreements for developing countries.

Despite the "less than expected" cuts in the trade distorting support resulting from the UR Round Agreement and the stalemate of the Doha Round, analyses showed that, trade performance, especially that of developing countries markedly improved in the 1990s and 2000s. Developing countries' total merchandize export shares increased from 30.3% in 1980 to 58.5% in year 2010, surging from a low of 24.1% in 1990 (Michalopoulos and Ng, 2013). The same analysis also showed impressive gains in South-South trade and better integration of the developing economies after the UR Round in world trade (as measured by the ratio of total trade and GNP). It cannot be denied that trade liberalization initiatives significantly contributed to better world trade performance. According to Taylor and Fairchild (2000), one of the main factors that influenced trade in agriculture, especially that of fruits and vegetables was the "change in trade policies resulting from the AoA and regional preferential trading arrangements". Although the Doha Round talks of the WTO had stalled, but the fact that it had stalled, led to a proliferation of plurilateral and bilateral free trade agreements (FTAs). Governments just cannot wait for a comprehensive multilateral trade deal anymore. As reported by the WTO, currently there is a total of 575 FTAs that were notified to the WTO of which 379 are in force. Many of these FTAs are signed after 1995. This in itself is evidence of the bullish expectations by governments across the world on the benefits of freer trade. As shall be shown in this paper, the overall scenario and prospects would be similar for Malaysia which had from the early days depended on international trade for growth and prosperity.

Global Trends and the Role of Developing Countries in World Trade

World agricultural trade exhibited strong growth during the last decade, expanding from US$488.4 billion in year 2000 to more than US$2181 billion in year 2010, registering an annual growth rate of around 10%. This was a much higher rate as compared to 3.3% and 2.2% respectively for the 1980 - 1990 and 1990 - 2000 periods (FAOSTATS). One of the important factors contributing to this growth had been the “acceleration of globalization" which was characterized by a rapid decline in international trading costs, developments in ICT and reductions in government distortions in agricultural trade (Anderson, 2010). World agriculture before the reforms was typified by huge subsidies and protection by developed countries as well as “market insulations” by developing countries. Though these remained high today, significant cuts in subsidies and protection as a result of trade agreements had led to relatively freer market. This freer market had in turn stimulated higher trade in agricultural products and consequently resulted in better integration of the developing economies into the international trading system.

Michalopoulos and Ng (2013) showed that overall export shares of developing economies increased from 24.1% in 1990 to 41.2% in 2010, an increase of over 70 percentage points over the 20-year period. Meanwhile the share of the developed countries dropped from 76.4% to 58.5% during the same period (Table 1). Similar trends could also be observed or imports albeit at lower rates as compared to exports.

It was also noted for the period that the share of developing countries' exports to other developing countries had also been expanding significantly from 42.6% of total exports in 1995 to over 55% in 2010 (Table 2). Proportionately the share of developing countries exports to developed countries has decreased.

Growth in trade for agricultural products for developing countries was also higher than the overall global growth. The rate in growth was also highest for the 2000 - 2010 decade where expansion in growth in agricultural products for developing countries grew at more than 12% (Table 3). Corresponding with the faster rate of growth registered by developing countries, the share of developing country trade in world agricultural products also rose by more than 11% from its low of about 26.5% in 1990 to more than almost 38% in 2010 (Table 3). Analyses by Laipis (2010) also showed developing country markets were getting increasingly diversified as compared to before. He also showed that trade among developing countries or more popularly known as South-South was not only expanding and was increasingly South-South. On the other hand, the share of North-North trade in agricultural products was getting lower while that of North-South trade has almost stagnated (Figure 1).

Malaysia’s Agricultural and Trade Policy

Agricultural policies were generally designed to balance the economic, social and political objectives of the State that saw a combination of fairly liberal policies for many of the agricultural industries while instituting some protectionist measures for some industries. In this section Malaysia's agricultural and trade policies are briefly described to provide an understanding the evolution of the country's policy from the early days since independence till the present day. One could then relate this to Malaysia's economic development as well its integration into the international trading system. Most of this section had been described and taken from Tengku Ariff (2010).

Earlier policies

The legacy of plantation crops such as rubber and oil palm started very early during the British era before independence. Since then, this subsector has been the pillar of Malaysian agriculture. Relative to other subsectors, plantation crops received more emphasis in terms of budget allocation, development programs as well as other government support during the early phases of agricultural development. The only other crop that received attention is rice. Being the staple and a "poor man's crop" it has a unique status in society as a strategic crop for food security with embedded programs to enhance farm income and alleviate poverty among its producers.

Policies and programs in the early stages of development mainly addressed to enhance income of agricultural producers in order to reduce the incidence of poverty in agriculture and to minimize inter-sectoral disparity and inequity between agriculture and non-agriculture. Hence, agricultural development strategies in the 1960s and 1970s mainly focused on the objectives of reducing poverty, providing rural employment and enhancing agricultural incomes. They were also export oriented to earn foreign exchange. Plantation crops for exports mainly rubber, oil palm and cocoa were actively promoted while a number of the food subsectors were protected to mainly insulate producers and save foreign exchange in line with the import substitution strategy during this period. A few of these support and protection are still in existence until this day though many of them had been dismantled in line with liberalization. These liberalization initiatives mainly started with the introduction of the first National Agricultural Policy (NAP, 1984). Productivity, efficiency and competitiveness were the main focus of the policy. Development efforts in the sector were consequently then geared towards modernization and commercialization. Downstream and value-added agricultural industries were emphasized and encouraged by providing highly attractive incentives such as tax breaks and export rebates. Tariffs on agricultural products were reduced and many were abolished to make imports of raw materials cheaper to reduce input costs for the downstream industries. This move was also to prepare the sector for increased competitiveness by allowing the “discovery” of specialized agricultural product niches through comparative and competitive advantages.

This was followed by the National Agricultural Policy 2 (NAP2), 1992 - 2010 which basically continued and further strengthened the policies in NAP 1. During this period of the 1990s, when the global economy was in a “bull-run” spurred by manufacturing demand from developed countries, Malaysia’s share of manufactured exports rapidly rose from 58.8 % in 1990 to almost 80% in 1995, where it remained in the 2000s. Share of agriculture meanwhile dropped from 22.3 % to just 13.1% during the period, and to 7% in 2005. It was during this period that many developing country governments, Malaysia included neglected agricultural development. Budgetary allocation, human resource and infrastructural development as well as other important requisites for agricultural growth were no longer given emphasis. This period of the “roaring nineties” as described by Stiglitz (2003), had made Malaysia complacent on the importance of growing one’s own food. The popular mantra was that “we can always buy what we want”.

Recent policy development

The Asian Financial Crisis (AFC) of 1998 was a wake-up call for the government on the importance of not being too dependent on imports for food. Domestic food prices escalated resulting from higher import costs as the domestic currency seriously depreciated. Riots in a neighboring country due to food shortages and unaffordable prices led to the fall of the Government. In Malaysia, social discontent was rising. This development led the Malaysian Government to review the second National Agricultural Policy. This gave birth to the Third National Agricultural Policy (1998 – 2010).

The Third National Agricultural Policy (1998 – 2010)

In the NAP3, as it is popularly known, policies, strategies and initiatives to transform and revitalized the sector were specified. The importance of food production and SSL was re-emphasized and “meeting national food requirements” was the first of the five strategic thrusts of the NAP3. Another important strategy was to enhance and strengthen the requisite foundation of agricultural development, especially for the food subsector. This include among others, physical infrastructure, finance, human resource and technology.

Malaysia's trade policy

Trade policies in Malaysia follow closely the sectoral development policies where national development agendas were embedded.

Main components of Malaysia’s agricultural trade policy

Being a trade oriented economy, external trade is of great importance to the development of the Malaysian economy and Malaysia places high importance on a strong, open and viable trading system (GATT, 1993).

The overall trade-related policy’s aim is to promote and safeguard Malaysia's interests in the international trade arena, to spur the development of industrial activities, and to further enhance Malaysian economic growth towards becoming a developed nation by year 2020 (Vision 2020). Specifically, Malaysia's trade policies are intended to: improve market access for goods and services; promote the global competitiveness of its exports; expand and diversify trade with existing trade partners; and explore new markets (WTO, 2010). At the same time, as was earlier mentioned, Malaysia supported a number of agricultural industries for strategic and socio-economic reasons including for food security, rural development and alleviation of poverty. The “infant industry” argument was also used to justify some of this support.

The trade regime for agriculture Overall, Malaysia has a liberal trade regime with low tariffs for most products. The simple average applied MFN tariff was 7.4% in 2009 while more than 60% of the products are duty free. As early as 1985, FAO observed that even for the so-called “protected subsectors” in Malaysian agriculture, such as the tropical fruit industry, which attracted a tariff of RM661 per ton for many imported fruit types, the tariff was still among the lowest in the region (FAO, 1985). Present tariffs on agricultural imports are generally low, averaging at 2.8% in 2009 (WTO, 2010), down from 3.2 % in 2005 and from 10.4 % in 1993. The lowering of the tariffs was in fact a necessity that benefits downstream agricultural value adding activities through the imports of cheaper raw materials and intermediate agricultural products.

Other industries that are still accorded policy support are paddy and rice, specific livestock subsectors, tobacco and tropical fruits, coffee and cabbages. It is in these sub-sectors that most of the non-ad valorem tariffs are still maintained and non tariff measures still in place. However, of late, many of these fixed tariffs had been done away with except for some of the sensitive products such as alcoholic beverages. With the ASEAN Free Trade Area, the import tariffs on most of these products are now down to only 5% within ASEAN, though TRQs are still in place for a small number of products.

Malaysia's involvement in Free Trade Agreements

Malaysia joined GATT (General Agreement on Tariff and Trade) in 1957, the immediate year it obtained independence from the British. It was one of the earlier members to join the organization, underscoring the importance of international trade accorded by the founding government of the country. This policy remains till this day. GATT itself was formed in 1948 to oversee the multilateral trading system. During GATT, governments that signed GATT were called "GATT Contracting Parties". Upon conclusion of the UR Agreement these Parties became members of the WTO which was formed in 1995 to replace GATT. Being a GATT member, Malaysia became one of the 128 founding members when the WTO was formed. Its membership had since increased to 159 countries while another 24 countries are negotiating to accede and become members of the WTO.

While Malaysia continues to accord high priority to the rule-based multilateral trading system under the WTO, the country also pursued plurilateral, regional and bilateral trading arrangements to complement the multilateral approach to trade liberalization. Free Trade Agreements (FTAs) are generally aimed at providing the means to achieve quicker and higher levels of liberalization that would create effective market access between the participants of the FTA. Table 4 below presents Malaysia’s involvement in FTAs (further details can be seen in Appendix A).

The continued involvement and pursuance of Malaysia in free and preferential trade agreements proved the commitment of the country for freer trade. It also underlined the belief and importance of outward looking policies in achieving national, regional and global growth and firmly supports the fact that international trade is a fundamental requisite that formed one of the critical foundations of the economy.

Malaysia's overall agricultural trade performance

Malaysia has consistently maintained its position as one of the top 20 trading nations in the world. Since 1998, Malaysia reported consistent trade surpluses. Total trade for 2012 surpassed the one trillion ringgit mark with a value of RM1.31 trillion compared with RM1.27 trillion recorded in 2011.

The balance of trade as reported by the Malaysian Department of Statistics recorded a trade surplus of RM5,080 million, as of March 2013. Historically, from 1970 until 2013, Malaysia’s balance of trade averaged RM2,820 million, reaching the highest point of RM15,767 million in May 2008 and the lowest point of a deficit of RM2,881 million in June 1997. The main exports consisted of electrical and electronic products, palm oil, petroleum products, liquefied natural gas, timber and natural rubber. Malaysia also sends abroad chemicals, machinery, appliances and manufactures metals. Meanwhile, the country’s main imports consist of machinery and transport equipment, manufactured goods, fuel and chemicals.

Increased liberalization of the world trade environment, coupled with the increased opening of the Malaysian market, had made international trade more important to the Malaysian economy. Over the 1985-1995 period, the ratio of total exports to total GDP increased from 0.49 to 0.75 (Table 5). The ratio of imports to GDP also exhibited a similar trend, rising from about 39% of GDP to 88% during the period. These ratios further increased in the 2000 - 2010 decade from 1.05 to 1.14, reaching a high of 1.25 in 2008 for exports and from 0.87 to 0.95 for imports. These increasing ratios showed how well integrated the economy is in the international trading system as well as the growing importance of external trade to the Malaysian economy.

Agricultural trade

Total trade for Malaysian agricultural products showed steady growth for the past two decades. Total agricultural trade grew at the rate of almost 9.8% per annum for the period 1991 - 2010. Both imports and exports grew the same rate of also 9.8% per annum during the period. However, the 2001 - 2010 period saw a period of distinct growth in agricultural trade for Malaysia. Exports of Malaysian agriculture grew at almost 19% per annum from US$5.5 billion to almost US$26.0 billion, edging imports which grew at 15% per annum, from US$4.0 billion to US$14.0 billion (Table 6). This is despite the Global Financial Crisis (GFC) of 2007 - 2008 that hit both Europe and America. The robustness of Malaysian agricultural exports once again demonstrated the resilience of Malaysian agriculture to external shocks as was the case during the Asian Financial Crisis (AFC) of 1997 - 1998.

This AFC witnessed the melt down of Asian currencies including the Malaysian Ringgit and resulted in lower export earnings. This explained the slow growth in agricultural trade during the 1991 - 2000 period, which only grew at the rate of only 3.9% per annum. Table 6 also showed that exports slowed down to only 3.1% during the period. Lower value of the Ringgit caused imports to grow faster than exports, at 5.2% per year. Both average imports and exports between the two periods jumped by 2.2 times in trade value. This better performance of international trade by Malaysia in the later decade is most likely a result of increased trade liberalization between Malaysia's important trading partners such as the ASEAN FTAs and its bilaterals (Table 6).

The increasing importance of agricultural trade to the Malaysian economy can be seen in Table 7. The ratio of total agricultural trade to agricultural GDP had steadily increased form 1.19 in the year 2000 to 1.60 in 2010. This indicated that Malaysian agriculture has become more trade oriented. If one was to separate the overall agricultural trade ratio into ratios of exports and imports to agricultural GDP, it is shown that the ratio of agricultural exports to agricultural GDP were consistently higher than the ratio of agricultural imports to agricultural GDP. This indicated that the sector was more export oriented than import oriented. It export orientation has also been increasing over the 2000s from a ratio of 0.72 in year 2000 to more than 1 in 2010 (Table 8). Since 2003 the ratio of exports to GDP has always been above 0.9 while starting 2008 the ratio has been consistently at about 1.0. These stronger export GDP ratios as compared to import GDP ratios could also indicate the competitiveness of Malaysian agricultural exports and hence, overall should be able to continue to benefit from increased agricultural trade liberalization world wide.

Direction of Agricultural Trade

A study by Tengku Ariff (1998) for the period of 1985-1996, observed that Japan, the USA the EU and ASEAN, particularly Singapore, were among the major markets for Malaysia products. Together they accounted for more than 75% of Malaysian exports for the previous two decades. Singapore, USA and Japan together have consistently accounted for more than 50% of total exports. Thus, the Malaysian export market remained highly concentrated with limited progress being made in market diversification. The direction of imports was also similar, with Japan, Singapore, USA and the EU being the major source of Malaysia’s imports. The trend showed that there was also an increased concentration in the sources of Malaysia’s imports. The study, on the other hand, showed that trade in agriculture was more successful in terms of diversification. The 10 major export destinations for Malaysian agricultural products were Japan, Singapore, USA, China, Hong Kong, Korea, the Netherlands, Thailand, Taiwan and Pakistan. There was a decrease in concentration of exports to these countries from 64% of total agricultural exports in 1985 to 54% in 1995. For agricultural products, the Asian market became increasingly important with China and Pakistan displacing USA in the top five export destinations. The sources of agricultural imports also became less concentrated.

Meanwhile, observing the more recent trend for the year 2000-2010 (Figure 2), the country’s top 10 agricultural trading partners are China, Indonesia, Singapore, Thailand, the US, Australia, India, Japan, the Netherlands, and Pakistan. Figure 3 exhibits the nation’s agricultural import trend for the same period. Starting from 2003, Indonesia became a leading source for Malaysian agricultural imports, and it continues to show tremendous increase until recently. On the other hand, in the early years from 2000, Singapore was Malaysia’s leading agricultural export destination (Figure 4). Eventually, China took over as Malaysia’s major agricultural export destination from 2003 onwards, maintaining the increasing importance of the Asian market in the top five export destinations. This trend again signifies the importance of developing country market expansion, the South-South trade, for exports from developing countries. Malaysian agricultural exports certainly benefited from their expanding import demand.

Malaysia’s agricultural trade vis-à-vis ASEAN and the world

This section further analyzed the growth trends of Malaysia’s agricultural trade as compared to ASEAN and the world for the 1986 – 2010 period. The period were divided into five-year-periods as in Table 9. A simple comparative analysis was made to indicate the trends and levels of trade that took place before and after WTO and AFTA came into force. For this purpose, the periods were divided into two, pre-WTO and AFTA (1986-1995) and post-WTO and AFTA (1996-2010).

Malaysia’s total trade during the 1986-1990 periods averaged US$ 6.1 billion, with growth of around 8.6% which is comparable to ASEAN and the world’s growth. However, the following five-year periods (1991-1995) prior to coming into force of WTO/AFTA, its total trade recorded a trade average of US$ 8.8 billion and growth of 14.4%. The nation’s trade growth was slightly higher than ASEAN’s and well above the worlds’ average.

Conversely, in the early years after WTO and AFTA were in place, there was a major drop in Malaysia’s trade growth rate, registering a negative growth of -5.97% per annum. ASEAN and the worlds’ trade growth were also negative, albeit not as bad as Malaysia’s. This demonstrated that being a trading nation, the years during global recession really affected our economy. However, this period could be considered an “abnormal period”, a period of the Asian Financial crisis, where as pointed earlier, the Malaysian Ringgit fell by as much 50% during the peak of the crisis in 1998 before the government instituted the fixed exchange rate of RM3.80 to the US dollar. Nevertheless, when the economy is thriving, Malaysia recovered better in terms of its trade growth. Recent years saw a notable improvement in the country’s total agricultural trade from about US$ 16.7 billion in 2005 to almost US$ 40.0 billion in 2010, registering a growth of 17.48%. Despite the short-term external shocks such as the AFC and the GFC the Malaysian agricultural trade registered a robust long term growth of more than 9.4 percent year for the 1986 – 2010 period. Also, during the period Malaysia’s agricultural trade market share increased from 0.95% to 1.83% of world agricultural trade, while its five-year average trade increased by almost 8.7 times for the 1986 - 90 period as compared to the 2006 - 2010 period. Most of this increase in share could be atributed to its exports rather than imports.

ASEAN fared almost similarly at the same rate as Malaysia. Its total agricultural trade increased during the pre-liberalization era from an average of US$ 24.5 (1986-1990) to US$ 38.8 (1991-1995). There was then the same drop whereby ASEAN’s trade growth slowed down to -5.37% per annum during 1996-2000, although the average trade for that period did register an increase. The later decade after the liberalization initiatives saw ASEAN’s trade expanded from US$57.3 billion to US$125.9 billion, an improvement of more than twice the worlds’ average.

The "Offensive" and "Defensive" perspectives

The trends and indicators for Malaysian agricultural trade conducted in the preceding sections all indicated that Malaysia has benefited from a more liberal agricultural trade regime world-wide. Its agriculture had become more trade oriented in nature, its growth in agricultural trade had surpassed that of the region and the world and more importantly, its agricultural balance of trade (BOT) was not only consistently positive but had widely increased over time. Since 1989, the BOT had increased by nearly 4.5 folds, from RM2,676 million to RM11,833 million, growing at an average rate of 7.3% per annum (Table 10). A better liberalized world, as such, holds a promise of a better agricultural economy for Malaysia. On this premise, Malaysia has been a strong advocator of freer trade in agriculture. Opening of agricultural markets seemed highly beneficial to Malaysia.

However, policymakers had been more cautious in pushing "too much" liberalization in agriculture lately due to the reciprocal response it has to similarly undertake. Although the agricultural trade BOT had been positive and increasing for the last 30 years, this positive BOT was mainly accounted by a narrow based agricultural export, led mainly by palm oil and rubber. Malaysia is still a net importer of food (discounting palm oil). Figures released by the Department of Statistics, Malaysia showed that the deficit in food trade has increased from RM5.3 billion in 2000 to RM7.5 billion in 2005 and further widened to more than RM12.0 billion in 2010. Major food group deficits in 2010 came from feedstuffs (RM3.70 billion), cereals (RM2.80 billion), sugars and preparations (RM1.92 billion), vegetables (RM1.68 billion), meat and meat products (RM1.3 billion), fruits (RM722 million) and milk and milk products (RM662 million). Hence while Malaysia has a strong offensive interests in its commodity exports, it also has defensive interests in its food sector. Furthermore, producers in the food sector in Malaysia are primarily smallholders where socio-economic considerations such as income, poverty alleviation, food security as well as rural development objectives need to be balanced with economic growth and trade. This is more so in the rice subsector, where national food security considerations usually take priority.

Table 11 shows the import and export performances of five subsectors in agriculture with three of them registering positive BOTs while two of the subsectors exhibiting negative BOTs. Of the five selected agricultural products, it can be clearly seen that palm oil constituted the largest BOT. During the 15 year period its BOT increased from RM3.6 billion to more than RM11.3 billion. Obviously the dominance of palm oil exports is the main factor that resulted in the overall positive BOT for agriculture.

The poultry and processed food subsector both reported a positive BOT during 1995 until 2010 (Table 11). However, comparing between 1995 and 2000, there was a slight decrease in each of the respective total exports. Meanwhile, between 2005 and 2010, both subsectors saw a commendable increase in its total trade, from US$ 145 million to US$ 264 million, and from US$ 2416 million to US$ 5673 million, respectively. While Malaysia is moving rapidly towards industrialization, processed food production will continue to become more important. Processed food demand including for both domestic consumption and exports are expected to expand as consumer preference changes and incomes and standard of living increases.