ABSTRACT

People’s Business Credit (KUR) is a financing scheme for working capital and investment provided to prospective beneficiaries who have productive and viable businesses, including agricultural businesses, but do not have additional collateral or the additional insufficient collateral. This paper aims to describe the performance and challenges in implementing the KUR program, especially in Indonesia’s agricultural sector. The main objective of the KUR program is to increase access to financing for productive businesses, to improve the competitiveness of micro, small and medium enterprises (MSMEs), and to promote economic growth and employment. The scope of the program covers MSMEs in all economic sectors. The implementation of KUR program in the agricultural sector in the last three years has always exceeded the target which reached 100.4%. The challenges were related to aspects of socialization, suitability of the program with agricultural business characteristics, and monitoring the use of credits by farmer beneficiaries. The involvement of extension workers is needed so that the process of socialization, assessment of prospective beneficiaries, and monitoring of the utilization of KUR farmers can run optimally. Hence, there is a need to manage the KUR program to facilitate investments in agricultural equipment and machinery.

Keywords: people’s business credit (KUR), SMEs, agriculture, development, policy, Indonesia

INTRODUCTION

Background

Economic growth is the target of every country as well as an important indicator of the national economy. This economic growth requires the simultaneous operations of all economic sectors in terms of consumption, investments, government spending, and international trade. However, exclusive economic growth will encourage social inequality in society, where the rich are getting richer and the poor are getting poorer. This social inequality can spur social conflict which will eventually lead to an economic downturn.

Inclusive economic growth is highly expected where economic improvement occurs evenly across all levels of society. For this reason, productive activities in Micro, Small, and Medium-sized Enterprises (MSMEs) are expected to develop to attract the economy to the lower middle layers of society. The number of MSMEs in Indonesia is very large and its development in the last five years has continued to grow. The Ministry of Cooperatives, Micro, Small and Medium-sized Enterprises (MoCMSMEs, 2022) noted that the number of MSMEs in Indonesia in 2019 was 65.47 million units or a share of 99.99% of the total businesses in the country that involving 123.37 million people or about 46.24% of the total population of the country with a share of Gross Domestic Product (GDP) at current prices of 60.51%. From 2015 to 2019, the average growth in the number of MSMEs was 2.53% per year. It notes that Indonesia’s experience in the 1998 economic crisis when the Rupiah exchange rate against the US dollar fell proves that MSMEs were able to withstand the storm of the crisis. Not only surviving, but even MSMEs that are export-oriented with raw materials sourced from domestic commodities have also actually experienced a large increase in profits (Widyaningrum, 2020).

As an agricultural country with a population of more than 250 million people, Indonesia is serious in promoting inclusive economic growth through policy support for the national development. Agriculture is an essential one since its businesses are generally driven by MSMEs. This sector has a good resilience in times of economic stress due to the COVID-19 pandemic. During the implementation of large-scale social restriction policy, about 98% of micro level businesses had a negative impact of this pandemic. Almost all economic sectors experienced a decline in GDP, except for the agricultural sector. Since the COVID-19 pandemic in 2020, Indonesia’s GDP decreased by 2.97% year-over-year (Akhmad, 2022), but the agricultural sector experienced an increase in GDP by 2.19% year-over year (MoA, 2022a).

The government of Indonesia (GoI) has provided supporting policies for the developments of MSMEs in general and agricultural sector in the form of a low-interest financing program called People’s Business Credit (Kredit Usaha Rakyat/KUR) program involving the private sector (especially banking institutions). The uncertain conditions due to the conflict of Russia-Ukraine, the stress of climate change, and the recovery process related to the COVID-19 pandemic, the allocation of the state budget has become problematic. Therefore, the development of financing programs such as KUR is expected to increase. The GoI (in this case the Ministry of Agriculture/MoA) continues to encourage farmers, farmer groups, and all MSMEs agricultural business actors to take full advantage of this program.

This paper aims to describe the performance of the KUR program, and specifically how it is implemented to support agricultural development including the perspectives and challenges in Indonesia. In the end, it closes with conclusions and policy recommendations for optimizing the KUR program for the agricultural sector in the country.

PEOPLE’S BUSINESS CREDIT (KUR) PROGRAM

Rationale of KUR

MSMEs ranked as the largest part of Indonesian economic activities, starting from farmers, fishermen, miners, craftsmen, traders, and providers of various services. The number of MSMEs in 2019 was recorded at 65.47 million business units, an increase of 13.07% from 57.90 million units in 2013 (MoCMSME, 2022). The number of workers involved in MSMEs reached 123.37 million people in 2019, an increase of 8.12% from 114.10 million people in 2013. MSMEs are also one of the solutions to reduce inequality and the income gap of the Indonesian people since this sector has high economic resilience. Therefore, the GoI generates and supports a people-based economic empowerment program through KUR to enhance access to financing sources for MSMEs to improve national economic growth.

KUR was launched in November 2007 based on Presidential Instruction Number 6/2007 (GoI, 2007). It aims to expand access for MSMEs to obtain banking credit and increase production in the real sector [1]in Indonesia. This program is intended to strengthen capital capacity in the context of implementing policies to accelerate real sector development and empower MSMEs to increase Indonesia’s economic growth. KUR is sourced from bank funds provided for working capital and investment purposes and is channeled to individual MSME actors and/or business groups in cooperatives, which have feasible but not bankable businesses.

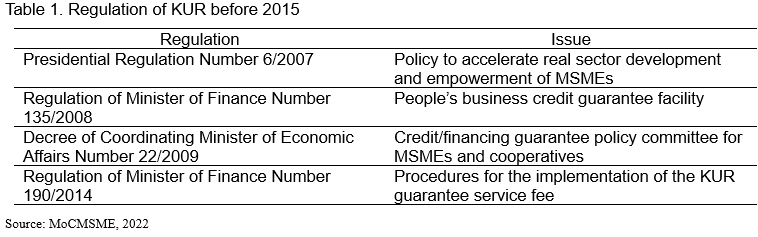

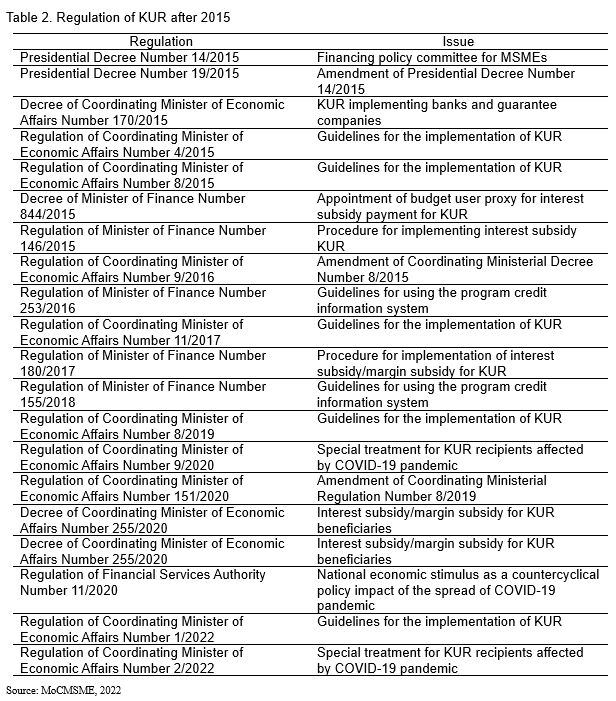

There are certain regulations related to the implementation of the KUR program that has dynamically changed in line with the economic policy direction in Indonesia. First, before 2015 (from 2007 to 2014), KUR was implemented through the guarantee service return mechanism as a service fee for credit/financing companies to MSMEs distributed by implementing banks (Table 1). Second, since 2015 KUR has transformed into interest/margin subsidy scheme since the implementation of guarantee service return mechanism was not on target (Table 2).

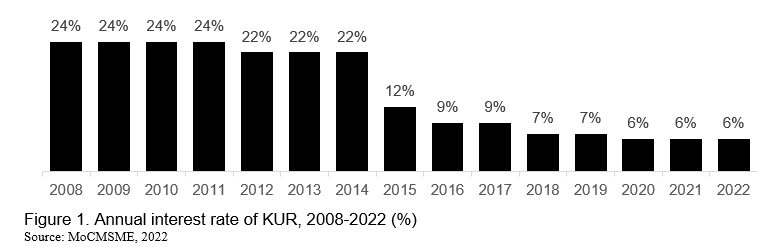

The interest subsidy scheme is the portion of interest borne by the government in the amount of the difference between the interest rate received by the credit/financing provider and the interest rate charged to the beneficiaries. Meanwhile, margin subsidy is the margin portion that is borne by the government in the amount of the difference between the margin received by credit/financing providers and the margin charged to beneficiaries in the sharia[2] financing scheme. The provision of interest/margin subsidies causes the interest rate for KUR to be very low compared to commercial banking. The interest rate continued to decline from 24% in 2008 to 6% in 2022 (Figure 1).

Since sharia principle does not recognize and employ interest rate in credit scheme, based on Decree of Coordinating Ministry of Economic Affairs Number 6/2019, the sharia KUR has been expanded from cost-plus financing (murabaha[3]) contract to sharia contract[4]. From the total of 46 KUR distributors in 2021, four of them (8.70%) were classified as Sharia KUR distributors.

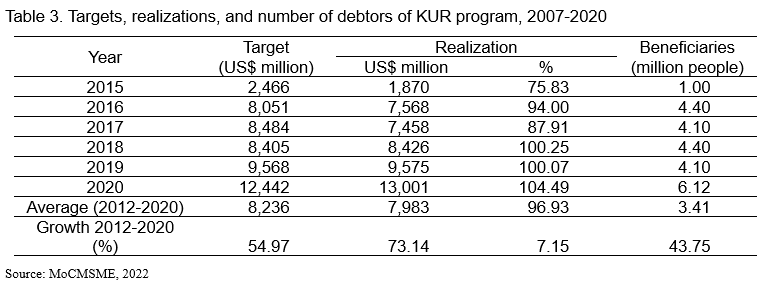

The performance of KUR in the last six years (2015 to 2020) was very good. It was measured by the level of realization of the target loan disbursement and the number of target beneficiaries of the program. KUR targets were set at the beginning of the year taking into account the number of MSMEs and their development. Meanwhile, the realization of KUR distribution was measured by how much money can be distributed by banks that distribute the KUR program to MSMEs. The average KUR target was US$8,236 million, or growing about 36.82% per year. KUR realization also shows good progress, namely US$7,983 million (97% of the target). The average growth of KUR realization was 73.14% per year. The number of KUR beneficiaries also continued to grow, from one million people in 2007 to 6.12 million people in 2020. The average growth of the number of beneficiaries within these periods was 43.75% per year (Table 3).

Scope of KUR

There are several parties involved in implementing the KUR program. They are government and supervisors, guarantors, distributors, and beneficiaries (MoCMEA, 2022).

Government and supervisors

The government has a task in planning and providing the necessary policy support, especially about the implementation of KUR in every economic sector. It comprises of 14 ministries/institutions, namely: (1) Coordinating Ministry for the Economic Affairs which establishes general policies for the implementation of the KUR program; (2) Ministry of Finance; (3) Ministry of Cooperatives and SMEs; (4) Ministry of Industry; (5) Ministry of Trade; (6) Ministry of Manpower; (7) Ministry of Agriculture; (8) Ministry of Maritime Affairs and Fisheries; (9) Ministry of State-Owned Enterprises; (10) Ministry of Home Affairs; (11) Ministry of Tourism; (12) Cabinet Secretary; (13) Indonesian Migrant Workers Protection Agency; and (14) Ministry of National Development Planning. Fourteen ministries/institutions plus the Financial and Development Supervisory Agency (as coordinator) and the Financial Services Authority carry out supervision for the KUR program at least once in six months.

Guarantors

KUR guarantors are guarantee companies and other companies appointed to provide KUR guarantees. The KUR guarantor works based on a cooperation agreement with the KUR distributor, one of which contains the guarantee fee. The guarantee fee is a component of the interest/margin subsidy. In 2021, there were 10 guarantee companies, namely: (1) PT Penjaminan Kredit Indonesia; (2) PT Asuransi Kredit Indonesia; (3) Regional credit guarantee companies in the provinces of Riau, West Sumatra, South Sumatra, Bangka Belitung, Central Java, and DKI Jakarta; and (4) Sharia guarantee companies (PT Penjaminan Jamkrindo Syariah and PT Penjaminan Financing Askrindo Syariah).

Distributors

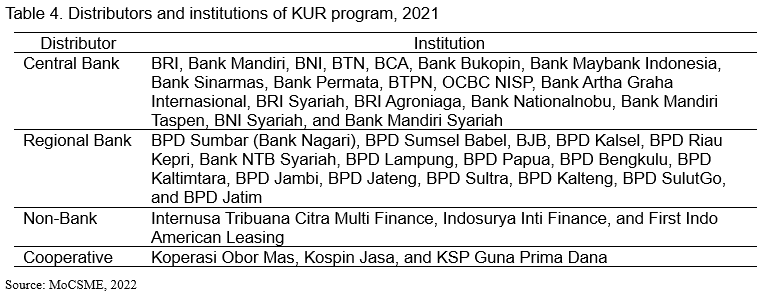

KUR distributors are financial institutions or cooperatives appointed to distribute KUR from banks or financial institutions. It distributes based on a database of the Program Credit Information System compiled by the Ministry of Finance. In 2021, the total KUR distributors were 46 financial institutions and cooperatives consisting of 18 central banks, 22 regional banks, three non-banks, and three cooperatives (Table 4).

Beneficiaries

KUR beneficiaries are individuals, business groups, or business entities that carry out productive businesses. KUR financing is in the form of funds for working capital and investments needs that are channeled to individual MSME actors, business entities, and/or business groups that have productive and viable businesses but do not have additional collateral, or in other words feasible but not yet bankable. In groups or business entities that apply for KUR, the financing agreement is still carried out by each group member with the KUR distributor. However, if there is a failure to pay the financing installments, it will be jointly and severally borne by members of the group/business entity. KUR beneficiaries are MSMEs from: (1) Family members of employees who earn a fixed income or work as Indonesian Migrant Workers; (2) Indonesian migrant workers and prospective apprentices abroad; (3) Workers in border areas with other countries; (4) Retired civil servants, national army/police; (5) Workers affected by the termination of employment; (6) Business groups; (7) Combination of farmer and fisherman groups; and (8) Housewives.

Distribution of KUR

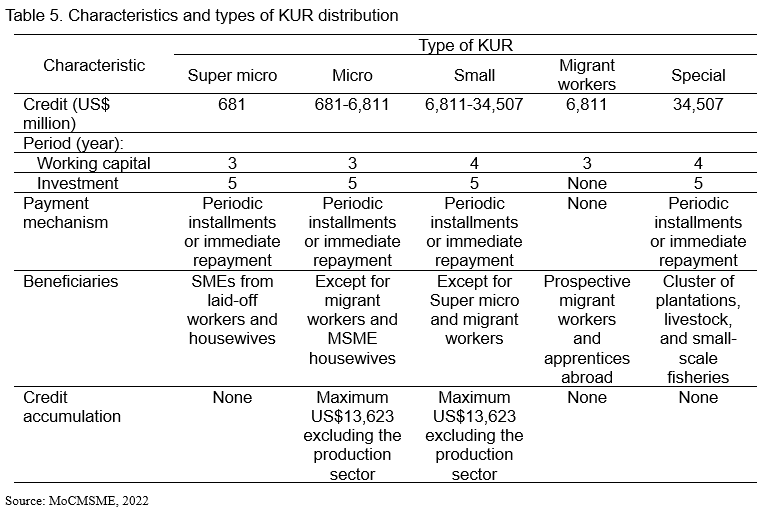

KUR distribution has developed from time to time. During the interest/margin subsidy scheme in 2015, the distribution of KUR consisted of Micro KUR, Retail KUR, and KUR for the placement of Indonesian workers (MoCMSME, 2015). In its development, the distribution of KUR underwent changes and additions. Referring to the Coordinating Ministerial Regulation Number 15/2020 (MoCMSME, 2020), the expansion of KUR distribution to workers affected by layoffs as a result of the COVID-19 pandemic and groups of housewives, Super Micro KUR distribution has been determined. Currently, the distribution of KUR consists of: (1) Super Micro KUR; (2) Micro KUR; (3) Small KUR; (4) KUR for the placement of Indonesian migrant workers; and (5) Special KUR (MoCMSMEs, 2022). The distribution of KUR is prioritized to eight main sectors, namely: (1) Agriculture, hunting, and forestry; (2) Marine and fishery; (3) Manufacturing industry; (4) Construction; (5) People’s salt mining; (6) Tourism; (7) Production services; and (8) Other production sectors.

Super micro KUR

Super micro KUR is a type of distribution with the lowest credit, namely US$681 per beneficiary, but not limited to the total accumulated ceiling credit. The term of the super micro KUR is a maximum of three years for working capital and a maximum of five years for investment. Super micro KUR payments can be made in periodic installments or all at once by the agreement between the beneficiaries’ recipient and the KUR distributors. Super micro KUR is intended for MSMEs from workers affected by layoffs and from housewives. Prospective super micro KUR beneficiaries can receive credit simultaneously with current collectibility. It also includes new business actors who participate in mentoring and entrepreneurship training, join business groups, or have family members who already have productive and viable businesses.

Micro KUR

Micro KUR has a ceiling credit from US$681 to US$6,811 per beneficiary. The term and payment mechanism of micro KUR are the same as the super micro KUR. This micro KUR is intended for all KUR beneficiaries except for prospective Indonesian migrant workers who work abroad, prospective apprentices abroad, as well as MSMEs from housewives. Prospective beneficiaries of micro KUR must have a productive business that is feasible to finance and has been running for at least six months. Prospective KUR beneficiaries can receive a maximum of US$6,811 per planting season or livestock cultivation season (for the agricultural sector) or per production cycle until they produce goods/services (for the production sector). Micro KUR recipients in the production sector are not only limited to the total accumulated ceiling credit, but also to beneficiaries outside the production sector up to US$13,623.

Small KUR

Small KUR has ceiling credit ranging from US$6,811 to US$34,057 per beneficiary. The term of small KUR is a maximum of four years for working capital and a maximum of five years for investment. The payment mechanism is also the same as micro KUR and super micro KUR. Small KUR is intended for all KUR recipients except for prospective Indonesian migrant workers who work abroad, prospective apprentices abroad, as well as MSMEs from workers affected by the termination of employment, and from housewives. Prospective recipients of micro-KUR must have business and taxpayer identification numbers. Small KUR recipients can only receive small KUR with a total accumulated ceiling credit maximum of US$34,057.

KUR for the placement of Indonesian migrant workers

The KUR for the placement of Indonesian migrant workers has a maximum credit limit of US$6,811 per beneficiary with the period is the same as the work contract period and not more than three years. This KUR is intended for prospective Indonesian migrant workers who work abroad and prospective apprentices abroad. The disbursement is carried out in stages from the beginning of the document processes for the placement of Indonesian migrant workers.

Special KUR

Special KUR is given to groups that are managed jointly in the form of a cluster using business partners for smallholders’ plantation commodities, livestock, fisheries, MSME industries, or other productive sectors. It has a ceiling credit starting at a maximum of US$34,057 per beneficiary of group member per planting season or livestock cultivation season (for the agricultural sector) or per production cycle until they produce goods/services (for the production sector). The maximum financing period is four years for working capital and five years for investment. The payment mechanism can be done in periodic installments or all at once according to the agreement between beneficiaries and distributors. Prospective KUR beneficiaries must have a productive business that is feasible to finance and has been running for at least six months as well as business and taxpayer identification numbers. It is specifically implemented in the production sector that is not limited to the total accumulated special KUR ceiling credit. For instance, in the case of smallholders’ oil palm commodity that have received funds from the Palm Oil Plantation Fund Management Agency, they can be financed with the special KUR minus rejuvenation costs.

The distribution of KUR program can be seen in Table 4. It is implemented based on super micro, micro, migrant workers, and special types of KUR as well as characteristics of this program (Table 5).

PEOPLE’S BUSINESS CREDIT (KUR) PROGRAM IN AGRICULTURE

Implementation

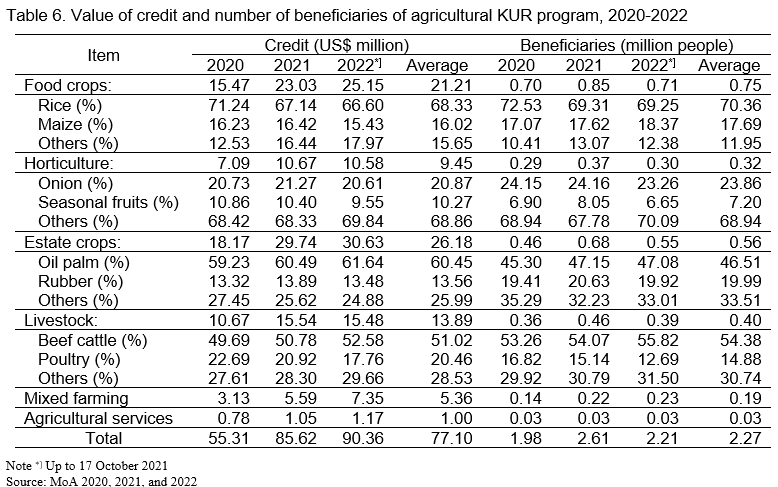

In general, the realization of KUR in the agricultural sector shows positive performance. From 2020 to 2022 (until 17 October 2022), the average realization of KUR in this sector reached 111.11% per year (Table 6). From 2020 to 2021 the realization increased by 10.57%, and in 2022 the realization achievement as of 17 October 2022 has exceeded the target of US$5,593 million or 100.4%. The number of KUR beneficiaries in the agricultural sector from 2020 to 2022 was an average of 2.27 million people. From 2020 to 2021, there was an increase in the number of KUR recipients by 32.06%, and on 17 October 2022 as many as 2.21 million people. This increased in the number of beneficiaries was accompanied by the achievement of non-performing credits of 0%. The high achievement of KUR realization in the agricultural sector reflects the enthusiasm of farmers in accessing credit for their businesses. This is in line with the government’s mandate to reduce the number of development programs sourced from the state budget.

Based on sub-sectors, the highest realization of KUR in 2020 to 2022 was achieved by the estate crops sub-sector with an average of US$1,687 million or 112.55% annually. It was followed by the horticulture sub-sector (111.49% annually), the livestock sub-sector (98.01% annually), and the food crops sub-sector (96.53% annually). The highest realization of KUR was in the estate crops sub-sector, namely US$2,986 per beneficiary. This amount was almost twice as large as the food crops sub-sector which only achieved US$1,812 per beneficiary.

In the estate crop sub-sector, the contribution of oil palm farmers was very large to the realization achievement, which was an average of 60.45% per year or equivalent to US$1,020 million with a total recipient of 0.26 million people. The next plantation commodity was rubber with an average realization of 13.56% per year or equivalent to US$229 million, with a total of 0.11 million recipients. The main orientation of using KUR in palm oil commodity was for the rejuvenation of smallholders’ palm oil with a target of 180,000 hectares in 2021, out of a total of 2.78 million hectares of oil palm plantations aged over 25 years (Tami, 2021). Through the distribution of special KUR with a ceiling credit of US$34,057 and a period of up to five years, it is sufficient to finance the rejuvenation of smallholder palm oil as well as to start other businesses as a “buffer” for farmers’ household income when palm oil cannot be harvested.

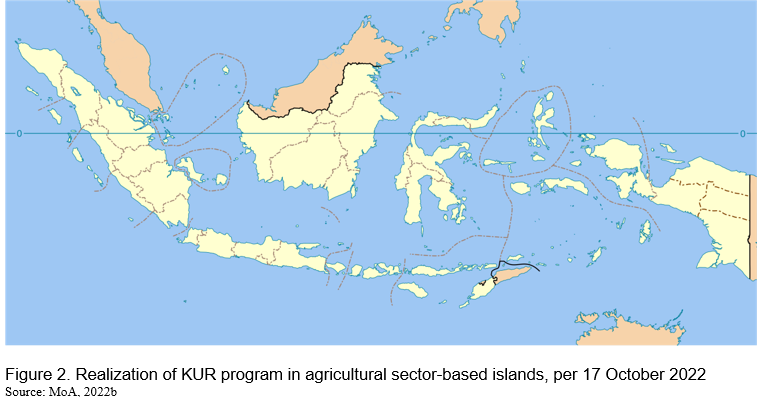

The realization of KUR in the agricultural sector by the island in 2022 (updated 17 October 2022) is shown in Figure 2. The highest KUR realization was in Java at 151.2% of the target set. The provinces of East Java and Central Java, which are the centers of agricultural production (both food crops and livestock), were included in the top five provinces with the highest realizations of 207.30% and 166.20%, respectively. Sumatra was the second island with the highest realization of 133.3%. Riau, Jambi, and North Sumatra were provinces on the island of Sumatra which are classified as the five provinces with the highest achievements. The three provinces on this island are oil palm production centers that are currently massively rejuvenating smallholders’ palm oil. The next realization achievements were Sulawesi (68.8%), Bali and Nusa Tenggara Island (41.6%), Kalimantan (39.6%), and Maluku and Papua Islands (25.5%). The realization achievement in Maluku and North Maluku provinces was the lowest, namely at 16% and 8.9%, respectively. These two provinces are not the centers of agricultural production, but the central producing area of fishery.

Challenges

Based on agricultural KUR data from 2020 to 2022, the average realization achievement per beneficiary was only US$2,191. In general, it can be seen that the use of KUR was more intended as working capital than as an investment. Investments in the agricultural sector were generally in the form of procurement of agricultural equipment and machinery. Limanseto (2022) noted that the realization of KUR for agricultural equipment and machinery as of September 2022 was only US$4.4 million (0.09% of the total KUR realization in the agricultural sector). The number of KUR beneficiaries who use agricultural equipment and machinery was only 272 people. This condition illustrates the importance of the government’s role in encouraging the modernization of agriculture in Indonesia as mandated by the Ministry of Agriculture, so that this sector can be advanced, independent, and modern.

Even though the use of KUR were not fully allocated for working capital, field findings by Ilham et.al (2020) stated that the utilization of credit was 70.7% for on-farm businesses, 3.17% for off-farm businesses, 5.11% for non-farm businesses, and even 18.5% for household consumption needs, while farmers and other uses were only about 2.52%. The use for non-farm businesses and consumption was getting bigger in the food crops and horticulture sub-sector farmers. The role of agricultural extension workers is needed not only in the process of program socialization but also to provide information and recommendations for prospective beneficiary farmers and also to monitor the optimal utilization of KUR. Monitoring the use of KUR is very important so that depraved credits do not occur due to the dominant use of KUR funds for consumptive needs that are not related to agricultural businesses.

CONCLUSION AND RECOMMENDATION

Conclusion

KUR program aims to strengthen capital capacity in the context of implementing policies to accelerate real sector development and empower MSMEs to increase Indonesia’s economic growth. The main parties involved in the KUR are distributors and beneficiaries. KUR distributors are financial institutions or cooperatives appointed to distribute this program. KUR beneficiaries are from: (1) Family members of employees who earn a fixed income; (2) Retired civil servants, Indonesian national army/police or who have entered the retirement preparation period; (3) Non-state civil apparatus; (4) Workers affected by the termination of employment; (5) Business group; (6) Combination of farmer and fisherman groups; (7) Housewives; (8) Workers at border areas with other countries; and (9) Indonesian migrant workers who work abroad and prospective apprentices abroad. There are five types of KUR distribution, namely super micro, micro, small, migrant worker, and special KUR. Each type of KUR distribution has a different ceiling credit, repayment period, payment mechanism, and policy.

The implementation of the KUR in the agricultural sector has shown excellent performance in the last three years. The program achievement was an average of 111.11% per year and the number of beneficiaries was 2.27 million people annually. The challenge in the implementation of the KUR program is the use of credit by beneficiaries who are oriented to working capital. In addition, there are still farmers who use KUR credit for activities outside the agricultural business.

Recommendations

It is necessary to manage several aspects of the KUR program so that the use of credit can lead to increased financing for agricultural investments, especially in the procurement of agricultural equipment and machinery. First, additional interest/margin subsidy of 3% so that farmers can use the KUR facility to provide agricultural equipment and machinery. Second, classify investment credit for agricultural equipment and machinery into a special KUR scheme so that beneficiaries are not subject to the accumulation of ceiling credit policy. Third, advances for the purchase of agricultural equipment and machinery can be reduced from the original 30% to 10%.

There is a need to involve field agricultural extensionists in the implementation of the KUR program through regulation for the implementation guideline of KUR in the agricultural sector. The essential roles of field agricultural extensionists include: (1) Promoting the program to suit the needs and concerns of farmers; (2) Providing information and recommendations for prospective beneficiary farmers; and (3) Monitoring the utilization of credit by beneficiaries toward optimizing agricultural business purposes.

REFERENCES

Akhmad T. 2022. Pertumbuhan Ekonomi Indonesia di masa Pendemi COVID-19 (Indonesia’s Economic Growth during the COVID-19 Pandemic). Muttaqien: Indonesian Journal of Multiciplinary Islamic Studies Muttaqien, Vol. 3 (1): 67-77. Purwakarta.

GoI, 2008. Undang-Undang Nomor 21 Tahun 2008 tentang Perbankan Syariah (Law Number 21/2008 on Sharia Banking). Government of Indonesia. Jakarta.

GoI. 2007. Instruksi Presiden Nomor 6 Tahun 2007 tentang Kebijakan Percepatan Pengembangan Sektor Riil dan Pemberdayaan Usaha Mikro Kecil dan Menengah (Presidential Instruction Number 6/2007 on Policies for Accelerating Real Sector Development and Empowerment of Micro, Small and Medium Enterprises). Government of Indonesia. Jakarta.

Ilham N, M. Syukur, E. Gunawan, S. M. Pasaribu, S. Wahyuni, J. F. Sinuraya, S. H. Suhartini. 2020. Pengoptimalan Pemanfaatan Kredit Usaha Rakyat mendukung Peningkatan Produksi Pangan (Optimizing the Utilization of People’s Business Credit to support Food Production Increase). Research Report. Indonesian Center for Agriculture Socio Economic and Policy Studies (ICASEPS). Bogor.

Limanseto H. 2022. Dorong Produktivitas Pertanian, Pemerintah dukung Modernisasi Taksi Alat dan Mesin Pertanian melalui Penyaluran Kredit Usaha Rakyat (Encourage Agricultural Productivity, Government Supports Modernization of Agricultural Equipment Taxis and Machinery through the Distribution of People’s Business Credit). Retrieved from: https://www.ekon.go.id/publikasi/detail/4628/dorong-produktivitas-hasil-... (2022 October 24). Indonesian Coordinating Ministry of Economic Affairs. Jakarta.

MoA. 2020. Realisasi Kredit Usaha Rakyat (KUR) Sektor Pertanian Tahun 2020 (Nasional) Update per tanggal 3 Juli 2021 (Realization of People’s Business Credit (KUR) for Agriculture Sector 2020 (National) Update as of July 3, 2021). Directorate of Agriculture Financing. Indonesian Ministry of Agriculture. Jakarta.

MoA. 2021. Realisasi Kredit Usaha Rakyat (KUR) Sektor Pertanian Tahun 2021 (Nasional) Update per tanggal 1 Januari 2022 (Realization of People’s Business Credit (KUR) in the Agricultural Sector in 2021 (National) Update as of January 1, 2022). Directorate of Agriculture Financing. Indonesian Ministry of Agriculture. Jakarta.

MoA. 2022a. FAO: Pertanian Indonesia Luar Biasa (FAO: Amazing Indonesian Agriculture). Retrieved from: https://www.pertanian.go.id/home/?show=news&act=view&id=4796#:~:text=Sel...) (2022 October 23). Indonesian Ministry of Agriculture. Jakarta.

MoA. 2022b. Realisasi Kredit Usaha Rakyat (KUR) Sektor Pertanian Tahun 2022 (Nasional) Update per tanggal 17 Oktober 2022 (Realization of People’s Business Credit (KUR) in the Agriculture Sector in 2022 (National) Update as of October 17, 2022). Directorate of Agriculture Financing. Indonesian Ministry of Agriculture. Jakarta.

MoCMEA. 2015. Peraturan Menteri Koordinator Bidang Perekonomian Nomor 8 Tahun 2015 tentang Pedoman Pelaksanaan Kredit Usaha Rakyat (Regulation of Indonesian Coordinating Ministry of Economic Affairs Number 8/2015 on Guideline of People’s Business Credit. Indonesian Coordinating Ministry of Economic Affairs. Jakarta.

MoCMEA. 2022. Peraturan Menteri Koordinator Bidang Perekonomian Nomor 1 Tahun 2022 tentang Pedoman Kredit Usaha Rakyat (Regulation of Coordinating Ministry of Economic Affairs Number 1/2002 on Guideline of People’s Business Credit). Indonesian Coordinating Ministry of Economic Affairs. Jakarta.

MoCMSME. 2022. Data UMKM (Small, Micro, and Medium-sized Enterprises Data). Retrieved from: https://kemenkopukm.go.id/data-umkm (2022 October 23). Indonesian Ministry of Cooperatives and Small and Medium-sized Enterprises . Jakarta.

Tami. 2021. Pekebun sawit bisa mendapatkan bantuan 30 juta: ini syaratnya (Oil palm smallholders can get 30 million in aid: this is the condition). Retrivied from: https://www.google.com/search?q=translate&oq =&aqs=chrome.0.35i39i362l8.29839272j0j15&sourceid=chrome&ie=UTF-8 (2022 October 24). Mutu Institut. Jakarta.

Widyaningrum N. 2020. UMKM Indonesia tahan banting pada Krisis 1998 dan 2008, tapi tidak saat Pandemi (Indonesian MSMEs were resilient in the 1998 and 2008 crises, but not during the pandemic). Retrieved from: https://theconversation.com/umkm-indonesia-tahan-banting-pada-krisis-199... (2022 October 23). The Conversation. Jakarta.

[1] Real sector is economic activities that involve transactions of goods or services, not just financial transactions (financial sector)

[2] Sharia carries out business activity based on the principles of Islamic law in banking based-fatwas issued by the Indonesian Ulema Council (GoI, 2008)

[3] A murabaha contract is a sale and purchase contract with an acquisition price plus profit, the determination of profit in a murabaha contract is determined at the beginning of the contract by agreement.

[4] A sharia contract is a cooperation contract between capital owners and business actors who have the ability to manage business productively and halal. The return on the sharia contract from the business will be shared between the investor and the perpetrator after knowing the results of the business.

People’s Business Credit (KUR) Program Supporting Agricultural Development in Indonesia

ABSTRACT

People’s Business Credit (KUR) is a financing scheme for working capital and investment provided to prospective beneficiaries who have productive and viable businesses, including agricultural businesses, but do not have additional collateral or the additional insufficient collateral. This paper aims to describe the performance and challenges in implementing the KUR program, especially in Indonesia’s agricultural sector. The main objective of the KUR program is to increase access to financing for productive businesses, to improve the competitiveness of micro, small and medium enterprises (MSMEs), and to promote economic growth and employment. The scope of the program covers MSMEs in all economic sectors. The implementation of KUR program in the agricultural sector in the last three years has always exceeded the target which reached 100.4%. The challenges were related to aspects of socialization, suitability of the program with agricultural business characteristics, and monitoring the use of credits by farmer beneficiaries. The involvement of extension workers is needed so that the process of socialization, assessment of prospective beneficiaries, and monitoring of the utilization of KUR farmers can run optimally. Hence, there is a need to manage the KUR program to facilitate investments in agricultural equipment and machinery.

Keywords: people’s business credit (KUR), SMEs, agriculture, development, policy, Indonesia

INTRODUCTION

Background

Economic growth is the target of every country as well as an important indicator of the national economy. This economic growth requires the simultaneous operations of all economic sectors in terms of consumption, investments, government spending, and international trade. However, exclusive economic growth will encourage social inequality in society, where the rich are getting richer and the poor are getting poorer. This social inequality can spur social conflict which will eventually lead to an economic downturn.

Inclusive economic growth is highly expected where economic improvement occurs evenly across all levels of society. For this reason, productive activities in Micro, Small, and Medium-sized Enterprises (MSMEs) are expected to develop to attract the economy to the lower middle layers of society. The number of MSMEs in Indonesia is very large and its development in the last five years has continued to grow. The Ministry of Cooperatives, Micro, Small and Medium-sized Enterprises (MoCMSMEs, 2022) noted that the number of MSMEs in Indonesia in 2019 was 65.47 million units or a share of 99.99% of the total businesses in the country that involving 123.37 million people or about 46.24% of the total population of the country with a share of Gross Domestic Product (GDP) at current prices of 60.51%. From 2015 to 2019, the average growth in the number of MSMEs was 2.53% per year. It notes that Indonesia’s experience in the 1998 economic crisis when the Rupiah exchange rate against the US dollar fell proves that MSMEs were able to withstand the storm of the crisis. Not only surviving, but even MSMEs that are export-oriented with raw materials sourced from domestic commodities have also actually experienced a large increase in profits (Widyaningrum, 2020).

As an agricultural country with a population of more than 250 million people, Indonesia is serious in promoting inclusive economic growth through policy support for the national development. Agriculture is an essential one since its businesses are generally driven by MSMEs. This sector has a good resilience in times of economic stress due to the COVID-19 pandemic. During the implementation of large-scale social restriction policy, about 98% of micro level businesses had a negative impact of this pandemic. Almost all economic sectors experienced a decline in GDP, except for the agricultural sector. Since the COVID-19 pandemic in 2020, Indonesia’s GDP decreased by 2.97% year-over-year (Akhmad, 2022), but the agricultural sector experienced an increase in GDP by 2.19% year-over year (MoA, 2022a).

The government of Indonesia (GoI) has provided supporting policies for the developments of MSMEs in general and agricultural sector in the form of a low-interest financing program called People’s Business Credit (Kredit Usaha Rakyat/KUR) program involving the private sector (especially banking institutions). The uncertain conditions due to the conflict of Russia-Ukraine, the stress of climate change, and the recovery process related to the COVID-19 pandemic, the allocation of the state budget has become problematic. Therefore, the development of financing programs such as KUR is expected to increase. The GoI (in this case the Ministry of Agriculture/MoA) continues to encourage farmers, farmer groups, and all MSMEs agricultural business actors to take full advantage of this program.

This paper aims to describe the performance of the KUR program, and specifically how it is implemented to support agricultural development including the perspectives and challenges in Indonesia. In the end, it closes with conclusions and policy recommendations for optimizing the KUR program for the agricultural sector in the country.

PEOPLE’S BUSINESS CREDIT (KUR) PROGRAM

Rationale of KUR

MSMEs ranked as the largest part of Indonesian economic activities, starting from farmers, fishermen, miners, craftsmen, traders, and providers of various services. The number of MSMEs in 2019 was recorded at 65.47 million business units, an increase of 13.07% from 57.90 million units in 2013 (MoCMSME, 2022). The number of workers involved in MSMEs reached 123.37 million people in 2019, an increase of 8.12% from 114.10 million people in 2013. MSMEs are also one of the solutions to reduce inequality and the income gap of the Indonesian people since this sector has high economic resilience. Therefore, the GoI generates and supports a people-based economic empowerment program through KUR to enhance access to financing sources for MSMEs to improve national economic growth.

KUR was launched in November 2007 based on Presidential Instruction Number 6/2007 (GoI, 2007). It aims to expand access for MSMEs to obtain banking credit and increase production in the real sector [1]in Indonesia. This program is intended to strengthen capital capacity in the context of implementing policies to accelerate real sector development and empower MSMEs to increase Indonesia’s economic growth. KUR is sourced from bank funds provided for working capital and investment purposes and is channeled to individual MSME actors and/or business groups in cooperatives, which have feasible but not bankable businesses.

There are certain regulations related to the implementation of the KUR program that has dynamically changed in line with the economic policy direction in Indonesia. First, before 2015 (from 2007 to 2014), KUR was implemented through the guarantee service return mechanism as a service fee for credit/financing companies to MSMEs distributed by implementing banks (Table 1). Second, since 2015 KUR has transformed into interest/margin subsidy scheme since the implementation of guarantee service return mechanism was not on target (Table 2).

The interest subsidy scheme is the portion of interest borne by the government in the amount of the difference between the interest rate received by the credit/financing provider and the interest rate charged to the beneficiaries. Meanwhile, margin subsidy is the margin portion that is borne by the government in the amount of the difference between the margin received by credit/financing providers and the margin charged to beneficiaries in the sharia[2] financing scheme. The provision of interest/margin subsidies causes the interest rate for KUR to be very low compared to commercial banking. The interest rate continued to decline from 24% in 2008 to 6% in 2022 (Figure 1).

Since sharia principle does not recognize and employ interest rate in credit scheme, based on Decree of Coordinating Ministry of Economic Affairs Number 6/2019, the sharia KUR has been expanded from cost-plus financing (murabaha[3]) contract to sharia contract[4]. From the total of 46 KUR distributors in 2021, four of them (8.70%) were classified as Sharia KUR distributors.

The performance of KUR in the last six years (2015 to 2020) was very good. It was measured by the level of realization of the target loan disbursement and the number of target beneficiaries of the program. KUR targets were set at the beginning of the year taking into account the number of MSMEs and their development. Meanwhile, the realization of KUR distribution was measured by how much money can be distributed by banks that distribute the KUR program to MSMEs. The average KUR target was US$8,236 million, or growing about 36.82% per year. KUR realization also shows good progress, namely US$7,983 million (97% of the target). The average growth of KUR realization was 73.14% per year. The number of KUR beneficiaries also continued to grow, from one million people in 2007 to 6.12 million people in 2020. The average growth of the number of beneficiaries within these periods was 43.75% per year (Table 3).

Scope of KUR

There are several parties involved in implementing the KUR program. They are government and supervisors, guarantors, distributors, and beneficiaries (MoCMEA, 2022).

Government and supervisors

The government has a task in planning and providing the necessary policy support, especially about the implementation of KUR in every economic sector. It comprises of 14 ministries/institutions, namely: (1) Coordinating Ministry for the Economic Affairs which establishes general policies for the implementation of the KUR program; (2) Ministry of Finance; (3) Ministry of Cooperatives and SMEs; (4) Ministry of Industry; (5) Ministry of Trade; (6) Ministry of Manpower; (7) Ministry of Agriculture; (8) Ministry of Maritime Affairs and Fisheries; (9) Ministry of State-Owned Enterprises; (10) Ministry of Home Affairs; (11) Ministry of Tourism; (12) Cabinet Secretary; (13) Indonesian Migrant Workers Protection Agency; and (14) Ministry of National Development Planning. Fourteen ministries/institutions plus the Financial and Development Supervisory Agency (as coordinator) and the Financial Services Authority carry out supervision for the KUR program at least once in six months.

Guarantors

KUR guarantors are guarantee companies and other companies appointed to provide KUR guarantees. The KUR guarantor works based on a cooperation agreement with the KUR distributor, one of which contains the guarantee fee. The guarantee fee is a component of the interest/margin subsidy. In 2021, there were 10 guarantee companies, namely: (1) PT Penjaminan Kredit Indonesia; (2) PT Asuransi Kredit Indonesia; (3) Regional credit guarantee companies in the provinces of Riau, West Sumatra, South Sumatra, Bangka Belitung, Central Java, and DKI Jakarta; and (4) Sharia guarantee companies (PT Penjaminan Jamkrindo Syariah and PT Penjaminan Financing Askrindo Syariah).

Distributors

KUR distributors are financial institutions or cooperatives appointed to distribute KUR from banks or financial institutions. It distributes based on a database of the Program Credit Information System compiled by the Ministry of Finance. In 2021, the total KUR distributors were 46 financial institutions and cooperatives consisting of 18 central banks, 22 regional banks, three non-banks, and three cooperatives (Table 4).

Beneficiaries

KUR beneficiaries are individuals, business groups, or business entities that carry out productive businesses. KUR financing is in the form of funds for working capital and investments needs that are channeled to individual MSME actors, business entities, and/or business groups that have productive and viable businesses but do not have additional collateral, or in other words feasible but not yet bankable. In groups or business entities that apply for KUR, the financing agreement is still carried out by each group member with the KUR distributor. However, if there is a failure to pay the financing installments, it will be jointly and severally borne by members of the group/business entity. KUR beneficiaries are MSMEs from: (1) Family members of employees who earn a fixed income or work as Indonesian Migrant Workers; (2) Indonesian migrant workers and prospective apprentices abroad; (3) Workers in border areas with other countries; (4) Retired civil servants, national army/police; (5) Workers affected by the termination of employment; (6) Business groups; (7) Combination of farmer and fisherman groups; and (8) Housewives.

Distribution of KUR

KUR distribution has developed from time to time. During the interest/margin subsidy scheme in 2015, the distribution of KUR consisted of Micro KUR, Retail KUR, and KUR for the placement of Indonesian workers (MoCMSME, 2015). In its development, the distribution of KUR underwent changes and additions. Referring to the Coordinating Ministerial Regulation Number 15/2020 (MoCMSME, 2020), the expansion of KUR distribution to workers affected by layoffs as a result of the COVID-19 pandemic and groups of housewives, Super Micro KUR distribution has been determined. Currently, the distribution of KUR consists of: (1) Super Micro KUR; (2) Micro KUR; (3) Small KUR; (4) KUR for the placement of Indonesian migrant workers; and (5) Special KUR (MoCMSMEs, 2022). The distribution of KUR is prioritized to eight main sectors, namely: (1) Agriculture, hunting, and forestry; (2) Marine and fishery; (3) Manufacturing industry; (4) Construction; (5) People’s salt mining; (6) Tourism; (7) Production services; and (8) Other production sectors.

Super micro KUR

Super micro KUR is a type of distribution with the lowest credit, namely US$681 per beneficiary, but not limited to the total accumulated ceiling credit. The term of the super micro KUR is a maximum of three years for working capital and a maximum of five years for investment. Super micro KUR payments can be made in periodic installments or all at once by the agreement between the beneficiaries’ recipient and the KUR distributors. Super micro KUR is intended for MSMEs from workers affected by layoffs and from housewives. Prospective super micro KUR beneficiaries can receive credit simultaneously with current collectibility. It also includes new business actors who participate in mentoring and entrepreneurship training, join business groups, or have family members who already have productive and viable businesses.

Micro KUR

Micro KUR has a ceiling credit from US$681 to US$6,811 per beneficiary. The term and payment mechanism of micro KUR are the same as the super micro KUR. This micro KUR is intended for all KUR beneficiaries except for prospective Indonesian migrant workers who work abroad, prospective apprentices abroad, as well as MSMEs from housewives. Prospective beneficiaries of micro KUR must have a productive business that is feasible to finance and has been running for at least six months. Prospective KUR beneficiaries can receive a maximum of US$6,811 per planting season or livestock cultivation season (for the agricultural sector) or per production cycle until they produce goods/services (for the production sector). Micro KUR recipients in the production sector are not only limited to the total accumulated ceiling credit, but also to beneficiaries outside the production sector up to US$13,623.

Small KUR

Small KUR has ceiling credit ranging from US$6,811 to US$34,057 per beneficiary. The term of small KUR is a maximum of four years for working capital and a maximum of five years for investment. The payment mechanism is also the same as micro KUR and super micro KUR. Small KUR is intended for all KUR recipients except for prospective Indonesian migrant workers who work abroad, prospective apprentices abroad, as well as MSMEs from workers affected by the termination of employment, and from housewives. Prospective recipients of micro-KUR must have business and taxpayer identification numbers. Small KUR recipients can only receive small KUR with a total accumulated ceiling credit maximum of US$34,057.

KUR for the placement of Indonesian migrant workers

The KUR for the placement of Indonesian migrant workers has a maximum credit limit of US$6,811 per beneficiary with the period is the same as the work contract period and not more than three years. This KUR is intended for prospective Indonesian migrant workers who work abroad and prospective apprentices abroad. The disbursement is carried out in stages from the beginning of the document processes for the placement of Indonesian migrant workers.

Special KUR

Special KUR is given to groups that are managed jointly in the form of a cluster using business partners for smallholders’ plantation commodities, livestock, fisheries, MSME industries, or other productive sectors. It has a ceiling credit starting at a maximum of US$34,057 per beneficiary of group member per planting season or livestock cultivation season (for the agricultural sector) or per production cycle until they produce goods/services (for the production sector). The maximum financing period is four years for working capital and five years for investment. The payment mechanism can be done in periodic installments or all at once according to the agreement between beneficiaries and distributors. Prospective KUR beneficiaries must have a productive business that is feasible to finance and has been running for at least six months as well as business and taxpayer identification numbers. It is specifically implemented in the production sector that is not limited to the total accumulated special KUR ceiling credit. For instance, in the case of smallholders’ oil palm commodity that have received funds from the Palm Oil Plantation Fund Management Agency, they can be financed with the special KUR minus rejuvenation costs.

The distribution of KUR program can be seen in Table 4. It is implemented based on super micro, micro, migrant workers, and special types of KUR as well as characteristics of this program (Table 5).

PEOPLE’S BUSINESS CREDIT (KUR) PROGRAM IN AGRICULTURE

Implementation

In general, the realization of KUR in the agricultural sector shows positive performance. From 2020 to 2022 (until 17 October 2022), the average realization of KUR in this sector reached 111.11% per year (Table 6). From 2020 to 2021 the realization increased by 10.57%, and in 2022 the realization achievement as of 17 October 2022 has exceeded the target of US$5,593 million or 100.4%. The number of KUR beneficiaries in the agricultural sector from 2020 to 2022 was an average of 2.27 million people. From 2020 to 2021, there was an increase in the number of KUR recipients by 32.06%, and on 17 October 2022 as many as 2.21 million people. This increased in the number of beneficiaries was accompanied by the achievement of non-performing credits of 0%. The high achievement of KUR realization in the agricultural sector reflects the enthusiasm of farmers in accessing credit for their businesses. This is in line with the government’s mandate to reduce the number of development programs sourced from the state budget.

Based on sub-sectors, the highest realization of KUR in 2020 to 2022 was achieved by the estate crops sub-sector with an average of US$1,687 million or 112.55% annually. It was followed by the horticulture sub-sector (111.49% annually), the livestock sub-sector (98.01% annually), and the food crops sub-sector (96.53% annually). The highest realization of KUR was in the estate crops sub-sector, namely US$2,986 per beneficiary. This amount was almost twice as large as the food crops sub-sector which only achieved US$1,812 per beneficiary.

In the estate crop sub-sector, the contribution of oil palm farmers was very large to the realization achievement, which was an average of 60.45% per year or equivalent to US$1,020 million with a total recipient of 0.26 million people. The next plantation commodity was rubber with an average realization of 13.56% per year or equivalent to US$229 million, with a total of 0.11 million recipients. The main orientation of using KUR in palm oil commodity was for the rejuvenation of smallholders’ palm oil with a target of 180,000 hectares in 2021, out of a total of 2.78 million hectares of oil palm plantations aged over 25 years (Tami, 2021). Through the distribution of special KUR with a ceiling credit of US$34,057 and a period of up to five years, it is sufficient to finance the rejuvenation of smallholder palm oil as well as to start other businesses as a “buffer” for farmers’ household income when palm oil cannot be harvested.

The realization of KUR in the agricultural sector by the island in 2022 (updated 17 October 2022) is shown in Figure 2. The highest KUR realization was in Java at 151.2% of the target set. The provinces of East Java and Central Java, which are the centers of agricultural production (both food crops and livestock), were included in the top five provinces with the highest realizations of 207.30% and 166.20%, respectively. Sumatra was the second island with the highest realization of 133.3%. Riau, Jambi, and North Sumatra were provinces on the island of Sumatra which are classified as the five provinces with the highest achievements. The three provinces on this island are oil palm production centers that are currently massively rejuvenating smallholders’ palm oil. The next realization achievements were Sulawesi (68.8%), Bali and Nusa Tenggara Island (41.6%), Kalimantan (39.6%), and Maluku and Papua Islands (25.5%). The realization achievement in Maluku and North Maluku provinces was the lowest, namely at 16% and 8.9%, respectively. These two provinces are not the centers of agricultural production, but the central producing area of fishery.

Challenges

Based on agricultural KUR data from 2020 to 2022, the average realization achievement per beneficiary was only US$2,191. In general, it can be seen that the use of KUR was more intended as working capital than as an investment. Investments in the agricultural sector were generally in the form of procurement of agricultural equipment and machinery. Limanseto (2022) noted that the realization of KUR for agricultural equipment and machinery as of September 2022 was only US$4.4 million (0.09% of the total KUR realization in the agricultural sector). The number of KUR beneficiaries who use agricultural equipment and machinery was only 272 people. This condition illustrates the importance of the government’s role in encouraging the modernization of agriculture in Indonesia as mandated by the Ministry of Agriculture, so that this sector can be advanced, independent, and modern.

Even though the use of KUR were not fully allocated for working capital, field findings by Ilham et.al (2020) stated that the utilization of credit was 70.7% for on-farm businesses, 3.17% for off-farm businesses, 5.11% for non-farm businesses, and even 18.5% for household consumption needs, while farmers and other uses were only about 2.52%. The use for non-farm businesses and consumption was getting bigger in the food crops and horticulture sub-sector farmers. The role of agricultural extension workers is needed not only in the process of program socialization but also to provide information and recommendations for prospective beneficiary farmers and also to monitor the optimal utilization of KUR. Monitoring the use of KUR is very important so that depraved credits do not occur due to the dominant use of KUR funds for consumptive needs that are not related to agricultural businesses.

CONCLUSION AND RECOMMENDATION

Conclusion

KUR program aims to strengthen capital capacity in the context of implementing policies to accelerate real sector development and empower MSMEs to increase Indonesia’s economic growth. The main parties involved in the KUR are distributors and beneficiaries. KUR distributors are financial institutions or cooperatives appointed to distribute this program. KUR beneficiaries are from: (1) Family members of employees who earn a fixed income; (2) Retired civil servants, Indonesian national army/police or who have entered the retirement preparation period; (3) Non-state civil apparatus; (4) Workers affected by the termination of employment; (5) Business group; (6) Combination of farmer and fisherman groups; (7) Housewives; (8) Workers at border areas with other countries; and (9) Indonesian migrant workers who work abroad and prospective apprentices abroad. There are five types of KUR distribution, namely super micro, micro, small, migrant worker, and special KUR. Each type of KUR distribution has a different ceiling credit, repayment period, payment mechanism, and policy.

The implementation of the KUR in the agricultural sector has shown excellent performance in the last three years. The program achievement was an average of 111.11% per year and the number of beneficiaries was 2.27 million people annually. The challenge in the implementation of the KUR program is the use of credit by beneficiaries who are oriented to working capital. In addition, there are still farmers who use KUR credit for activities outside the agricultural business.

Recommendations

It is necessary to manage several aspects of the KUR program so that the use of credit can lead to increased financing for agricultural investments, especially in the procurement of agricultural equipment and machinery. First, additional interest/margin subsidy of 3% so that farmers can use the KUR facility to provide agricultural equipment and machinery. Second, classify investment credit for agricultural equipment and machinery into a special KUR scheme so that beneficiaries are not subject to the accumulation of ceiling credit policy. Third, advances for the purchase of agricultural equipment and machinery can be reduced from the original 30% to 10%.

There is a need to involve field agricultural extensionists in the implementation of the KUR program through regulation for the implementation guideline of KUR in the agricultural sector. The essential roles of field agricultural extensionists include: (1) Promoting the program to suit the needs and concerns of farmers; (2) Providing information and recommendations for prospective beneficiary farmers; and (3) Monitoring the utilization of credit by beneficiaries toward optimizing agricultural business purposes.

REFERENCES

Akhmad T. 2022. Pertumbuhan Ekonomi Indonesia di masa Pendemi COVID-19 (Indonesia’s Economic Growth during the COVID-19 Pandemic). Muttaqien: Indonesian Journal of Multiciplinary Islamic Studies Muttaqien, Vol. 3 (1): 67-77. Purwakarta.

GoI, 2008. Undang-Undang Nomor 21 Tahun 2008 tentang Perbankan Syariah (Law Number 21/2008 on Sharia Banking). Government of Indonesia. Jakarta.

GoI. 2007. Instruksi Presiden Nomor 6 Tahun 2007 tentang Kebijakan Percepatan Pengembangan Sektor Riil dan Pemberdayaan Usaha Mikro Kecil dan Menengah (Presidential Instruction Number 6/2007 on Policies for Accelerating Real Sector Development and Empowerment of Micro, Small and Medium Enterprises). Government of Indonesia. Jakarta.

Ilham N, M. Syukur, E. Gunawan, S. M. Pasaribu, S. Wahyuni, J. F. Sinuraya, S. H. Suhartini. 2020. Pengoptimalan Pemanfaatan Kredit Usaha Rakyat mendukung Peningkatan Produksi Pangan (Optimizing the Utilization of People’s Business Credit to support Food Production Increase). Research Report. Indonesian Center for Agriculture Socio Economic and Policy Studies (ICASEPS). Bogor.

Limanseto H. 2022. Dorong Produktivitas Pertanian, Pemerintah dukung Modernisasi Taksi Alat dan Mesin Pertanian melalui Penyaluran Kredit Usaha Rakyat (Encourage Agricultural Productivity, Government Supports Modernization of Agricultural Equipment Taxis and Machinery through the Distribution of People’s Business Credit). Retrieved from: https://www.ekon.go.id/publikasi/detail/4628/dorong-produktivitas-hasil-... (2022 October 24). Indonesian Coordinating Ministry of Economic Affairs. Jakarta.

MoA. 2020. Realisasi Kredit Usaha Rakyat (KUR) Sektor Pertanian Tahun 2020 (Nasional) Update per tanggal 3 Juli 2021 (Realization of People’s Business Credit (KUR) for Agriculture Sector 2020 (National) Update as of July 3, 2021). Directorate of Agriculture Financing. Indonesian Ministry of Agriculture. Jakarta.

MoA. 2021. Realisasi Kredit Usaha Rakyat (KUR) Sektor Pertanian Tahun 2021 (Nasional) Update per tanggal 1 Januari 2022 (Realization of People’s Business Credit (KUR) in the Agricultural Sector in 2021 (National) Update as of January 1, 2022). Directorate of Agriculture Financing. Indonesian Ministry of Agriculture. Jakarta.

MoA. 2022a. FAO: Pertanian Indonesia Luar Biasa (FAO: Amazing Indonesian Agriculture). Retrieved from: https://www.pertanian.go.id/home/?show=news&act=view&id=4796#:~:text=Sel...) (2022 October 23). Indonesian Ministry of Agriculture. Jakarta.

MoA. 2022b. Realisasi Kredit Usaha Rakyat (KUR) Sektor Pertanian Tahun 2022 (Nasional) Update per tanggal 17 Oktober 2022 (Realization of People’s Business Credit (KUR) in the Agriculture Sector in 2022 (National) Update as of October 17, 2022). Directorate of Agriculture Financing. Indonesian Ministry of Agriculture. Jakarta.

MoCMEA. 2015. Peraturan Menteri Koordinator Bidang Perekonomian Nomor 8 Tahun 2015 tentang Pedoman Pelaksanaan Kredit Usaha Rakyat (Regulation of Indonesian Coordinating Ministry of Economic Affairs Number 8/2015 on Guideline of People’s Business Credit. Indonesian Coordinating Ministry of Economic Affairs. Jakarta.

MoCMEA. 2022. Peraturan Menteri Koordinator Bidang Perekonomian Nomor 1 Tahun 2022 tentang Pedoman Kredit Usaha Rakyat (Regulation of Coordinating Ministry of Economic Affairs Number 1/2002 on Guideline of People’s Business Credit). Indonesian Coordinating Ministry of Economic Affairs. Jakarta.

MoCMSME. 2022. Data UMKM (Small, Micro, and Medium-sized Enterprises Data). Retrieved from: https://kemenkopukm.go.id/data-umkm (2022 October 23). Indonesian Ministry of Cooperatives and Small and Medium-sized Enterprises . Jakarta.

Tami. 2021. Pekebun sawit bisa mendapatkan bantuan 30 juta: ini syaratnya (Oil palm smallholders can get 30 million in aid: this is the condition). Retrivied from: https://www.google.com/search?q=translate&oq =&aqs=chrome.0.35i39i362l8.29839272j0j15&sourceid=chrome&ie=UTF-8 (2022 October 24). Mutu Institut. Jakarta.

Widyaningrum N. 2020. UMKM Indonesia tahan banting pada Krisis 1998 dan 2008, tapi tidak saat Pandemi (Indonesian MSMEs were resilient in the 1998 and 2008 crises, but not during the pandemic). Retrieved from: https://theconversation.com/umkm-indonesia-tahan-banting-pada-krisis-199... (2022 October 23). The Conversation. Jakarta.

[1] Real sector is economic activities that involve transactions of goods or services, not just financial transactions (financial sector)

[2] Sharia carries out business activity based on the principles of Islamic law in banking based-fatwas issued by the Indonesian Ulema Council (GoI, 2008)

[3] A murabaha contract is a sale and purchase contract with an acquisition price plus profit, the determination of profit in a murabaha contract is determined at the beginning of the contract by agreement.

[4] A sharia contract is a cooperation contract between capital owners and business actors who have the ability to manage business productively and halal. The return on the sharia contract from the business will be shared between the investor and the perpetrator after knowing the results of the business.