ABSTRACT

Rubber production is central in economic development and it is also the second most agricultural export item followed by beans and pulses. Natural rubber production, consumption information of world rubber market and Myanmar rubber sector are done by desk review and conceptual frame work is formulated to cover the current situation and alternative forward policies by stakeholder participation approach. By comparing world production and consumption of natural rubber (NR) and synthetic rubber (SR,) there is slightly higher production than consumption in most of the years of the last decade. Therefore, it could be assumed that world rubber production was surplus NR in the last five years and shortage SR in five years of current decades and these surpluses and shortages were balanced in the current world rubber consumption. Myanmar became the 6th largest rubber producers in the world rubber market in 2018. NR consumption will be projected to grow by 5% per year through 2025 by the World Bank. In the future, World NR demand will be accelerated again as a result of increasing demand in lower and middle-income countries and sustained demand of China, India, the United States, and Japan while with the movement away from rubber production in Malaysia and Singapore and limited scope for rubber expansion in Indonesia, Myanmar could become an important rubber exporter in the rubber producing countries. However, the national average yield of Myanmar rubber was much lower than other rubber producing countries with many constraints and limitations of stakeholders along the value chain. Regarding Myanmar’s natural rubber sector development, the rubber related institutes and professional government organizations need to develop as the result of the policy context and rubber law. These institutes would became powerful and the most responsible units for rubber industry transformation. Moreover, revisions of laws and acts are needed several times to transform the rubber industry. Development of the rubber sector would be done by implementing capacity building and human resource management programs for all stakeholders and revising the rubber related laws and acts. In case of the transformation, this should be performed by the powerful institutions to implement the rubber development forward policy in Myanmar.

Keywords: policy, rubber, key stakeholder, participatory, export, world market

INTRODUCTION

Natural rubber industry in Myanmar

Myanmar’s agricultural sector dominates the economy, contributing 25.6% of gross domestic product (GDP), and employing more than 60% of the workforce (National Export Strategy, 2019). Among several crop productions in Myanmar, rubber production is central in economic development and it is also the second most agricultural export item followed by beans and pulses. Therefore, the rubber industry has been chosen as one of the priority sectors in Myanmar’s export strategies. Moreover, Myanmar's geographic position and climate make a potential driver for growth and development of rubber production. It is also important for economic development because the rural people from rubber growing areas have made their living from downstream and upstream sector of the rubber industry (National Export Strategy, 2015-2019).

Myanmar’s rubber industry had about 0.65 million hectares plantation area which employed about 400,000 workers and had experienced huge natural rubber market demand from neighboring countries (Department of Agriculture, 2019). Therefore, Myanmar became one of the largest rubber producers around the world. However, the national average yield per area was about 780 kg/ha and lower than that of other rubber producing countries (1,450 kg/ha- Malaysia and 1,417 Thailand) (ANRPC, 2019). And it also produced poor quality rubber with the low market price.

Rubber production in Myanmar is centered in Mon State. It is bounded by Bago Region to the north, Kayin to the east, and Tanintharyi to the south. It also shares a short southeastern border with Thailand. Mon State is one of the small States in Myanmar, but, with a population of two million inhabitants, so that it is relatively densely populated. The high population density makes it an economically important region. The central part of the state has the greatest concentration of the rubber industry. There are also various types of rubber markets and market participants, from brokers to exporters. Moreover, different farm sizes of rubber farmers are found in Mon State. Additionally, different kinds of rubber processing industries like Technical Specified Rubber (TSR) factories and value-added processing like rubber rings and balloons factories can be found (Van et al., 2017).

Objectives of the study

- To review the world natural rubber production, consumption, export and import data

- To find the export potential based on the Myanmar rubber production and export data

- To formulate Myanmar’s natural rubber development forward policies

METHODOLOGY

Natural rubber production, consumption information of world rubber market and Myanmar rubber sector are collected from desk reviews and various data sources. Conceptual frame work is formulated to cover the current situation and alternative forward policies by stake holder participation approach.

World natural and synthetic rubber production, consumption and export

In 1888 onwards, the mass production of automobiles created the increased demand for pneumatic tyres, which were made exclusively of NR and it was considered a golden age in terms of demand for NR. Before World War II, rubber products used 100% of NR. At that time, when the word rubber was mentioned, most people associated it with NR. Even latter-days, around 60% of NR was used in the production of tires. Although this might have been appropriate before World War II, synthetic rubber (SR) had grown since then to assume an important position.

During World War II, Japan’s occupation in most of the countries of Southeast Asia blockaded the supply of NR to industrial requirement from the West. It was a cause for concern and these countries responded vigorously, by investigating and searching SR for NR on a large-scale basis. Therefore, the development of SR, which was initiated politically and was strategically motivated, emerged as the most serious threat to NR, although SR production technology was intensive and less dependent on a skill-labor force. Its payment was also high compared to the production of NR latex on estates (Chan et al., 2013).

The production of SR was prompted by cheap and relatively constant supplies of petrochemical feedstock. However, it could not compete with NR’s capacity because the NR has good tensile, strength, friction, abrasion resistance and renounces properties of NR which override to SR. According to its modified qualities, NR cannot be replaced with other substances (Ferreira, Moreno, Gonçalves, & Mattoso, 2002). Moreover, the increase in demand for NR over SR is related to widespread concerns about global warming, deteriorating ecosystems and depleting sources of fossil fuels. In global environmental point of view, the rubber tree is capable of fixing ca. 1 MT of CO2 during its 30-year economic life cycle and therefore, within a hectare of rubber having over 300 trees, a minimum of 300 MT of CO2 is available for trade (Lakshman Rodrigo & Enoka Munasinghe, 2011). Additionally, it has renewable natural value with its premium quality because in the case of tire (passenger car, truck, bus etc.) production, there are certain amounts NR required, with each rubber type performing specific functions (Matthew Harder, 2018).

Annual world NR latex consumption gradually increased from 170,000 tons to 300,000 tons between 1960 and 1980. In the mid-1980s, total demand for NR latex took off, subsequently growing exponentially. This was the critical juncture of the transition of NR latex industries from the West to East countries. The NR demand take-off was also precipitated by the prevention of transmission of the human immunodeficiency virus (HIV) and hepatitis B with the increase in the use of NR latex gloves (Chan et al., 2013).

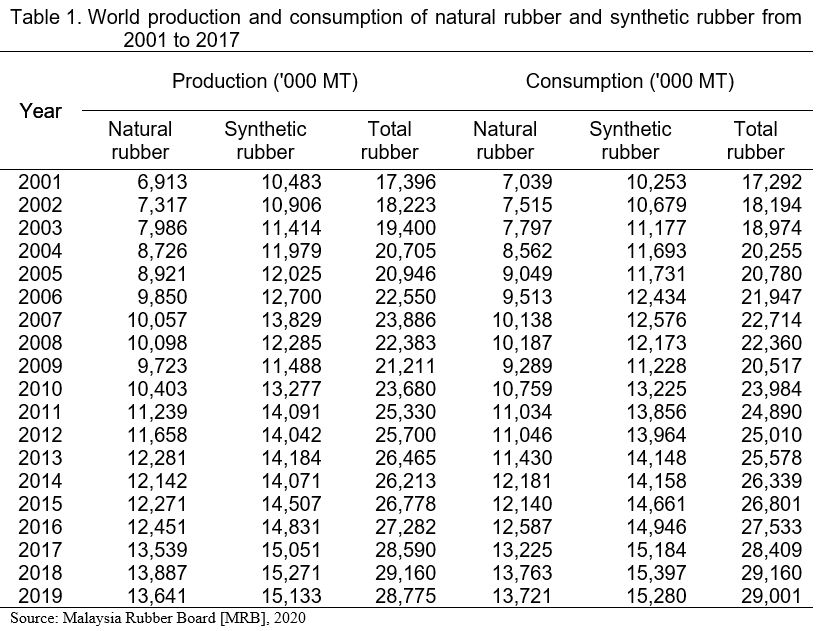

World production and consumption of NR and SR from 2001 to 2017 are summarized in Table 1. By comparing world production and consumption of NR and SR, there is slightly higher production than consumption in most of the years of last decade. Therefore, it could be assumed that world rubber production over the last five years and shortage of SR in five years of current decades and these surpluses and shortages balanced the current world rubber consumption.

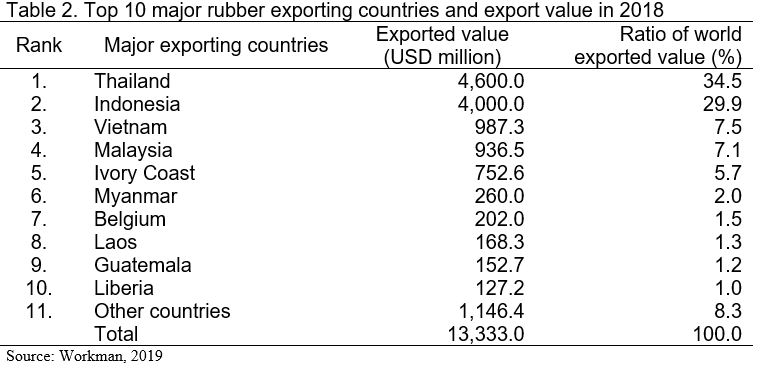

According to the 10 important countries that exported the highest dollar value worth of natural rubber during 2018, Thailand and Indonesia are the top one and two respectively with high proportion as over 60% (Table 2). Among the top ten exporting countries, Myanmar became one of the largest rubber producers around the world which makes it the 6th exporting country in the world rubber market in 2018.

Future world natural and synthetic rubber production and consumption

Although world NR production was slightly higher than NR consumption in several years as shown in Table 1, the global NR consumption is expected to grow at 3.6 % to 14.7 million tons and projected to grow by 5% per year through 2025 ( Global Rubber Market, 2019 and World Bank, 2016). The sector had faced reduced demand in recent years (2012-2016), compared with the previous period (2008-2011) which is shown in Table 1.

In the future, World NR demand will be accelerated again as a result of increasing demand in lower and middle-income countries and sustained demand of China, India, the United States, and Japan. At the same time, with the movement away from rubber production in Malaysia and Singapore and limited scope for rubber expansion in Indonesia, Myanmar could become an important rubber exporter in the rubber producing countries (Van, Htoo, & Dorosh, 2017).

Natural rubber industry in Myanmar’s economy

The commercial planting of rubber in Myanmar started since 1905, and it gradually increased in area to 4,000 hectares in 1909, 29,000 hectares in 1920, and 46,575 hectares in 1940 respectively. Then, in 1960, it reached 56,000 hectares. In particular, Myanmar became a large exporter of natural rubber among the NR producing countries by following the gradual liberalization of the agriculture sector in the 1990s and a surge in rubber prices in international markets in the 2000s and increase in investments of smallholder rubber farmers.

Additionally, a 30-year Master Plan of Ministry of Agriculture, Livestock and Irrigation (MOALI) for the Agriculture Sector (2000 - 2001 to 2030 - 2031) aims to convert 10 million acres (4.46 million ha) of ‘wasteland’ for private industrial agricultural production. The period between 2000 and 2010 was an epoch-making period for the rubber industry policy by the government. Myanmar government increasingly supported the development of the rubber sector. In 2004, the government also liberalized the rubber export policy by allowing both growers and dealers to export without first fulfilling the quota to Myanmar Perennial Crops Enterprise (MPCE) (Woods, 2012). Alternatively, it was estimated that the sector employed between only 350,000 and 400,000 workers, mainly in the plantation or upstream sector linked to planting and production of raw natural rubber. Therefore, the development of the sector, more particularly of its industry, could have high socio-economic impacts and become a driver of job creation.

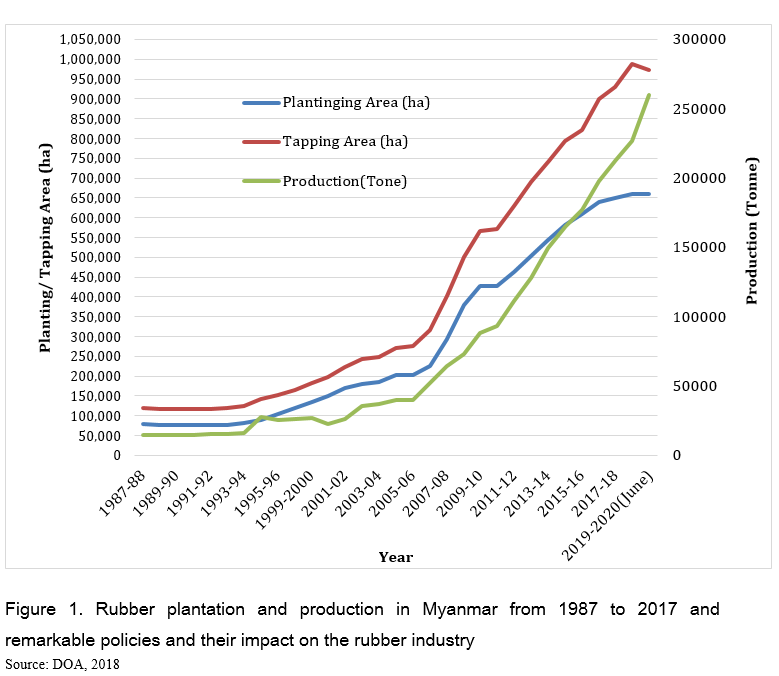

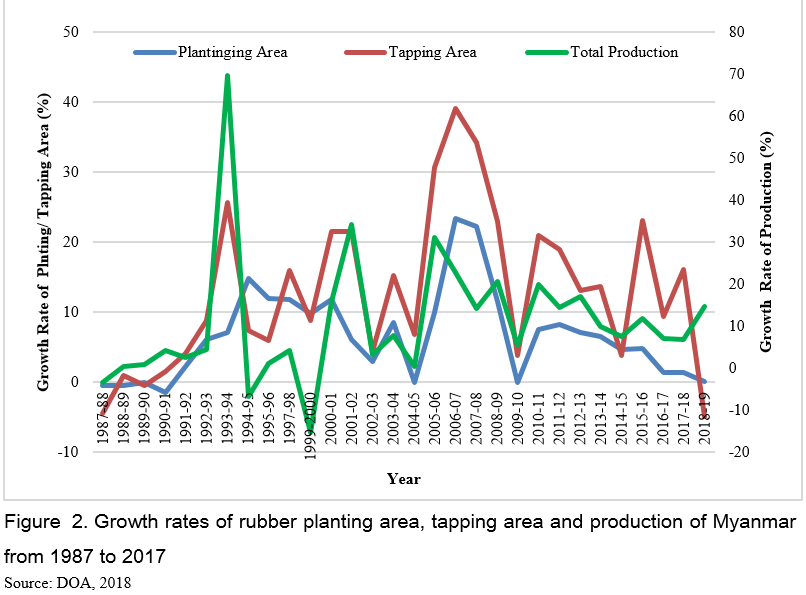

The rubber plantation areas were instantaneously increased after 1994-1995 as a consequence of Open Door policy (1989) and the establishment of MPCE, focal institute of rubber industry in 1994 as shown in Figure 1. There was also a significant increase in rubber export after 2006-2007 because the government had liberalized the rubber export policy by allowing both growers and dealers to export without any restrictions. Thereafter, rubber plantation areas, tapping areas and production were steadily increased until present time. Figure 2 presented growth rate of rubber planting areas, tapping areas and production. Therefore, national policy context for rubber industry was vital for further development.

Rubber production in Myanmar is centered in Mon and Kayin States. The central part of the Mon State has the greatest concentration of rubber trees and rubber products. There are also various types of rubber markets and market participants, from brokers to exporters. Moreover, different farm sizes of rubber farmers are found in Mon and Kayin States. Additionally, different kinds of rubber processing industries like Technical Specified Rubber (TSR) factories, Ribbed Smoked Sheet (RSS) factories and value-added processing like rubber ring and balloons factories can be found (Van et al., 2017).

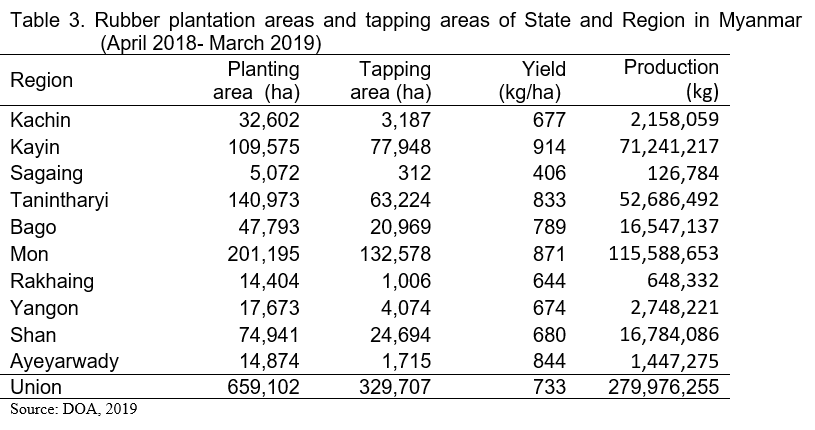

Moreover, Myanmar's geographic position and climate make a potential driver for growth and development of rubber production throughout the country. Table 3 presented rubber plantation areas and tapping areas of States and Regions in Myanmar. Among them, Mon State and Kayin State occupied about 50% of rubber planting areas and potential areas for investing in rubber related business.

Myanmar natural rubber production and export during 2006-2019

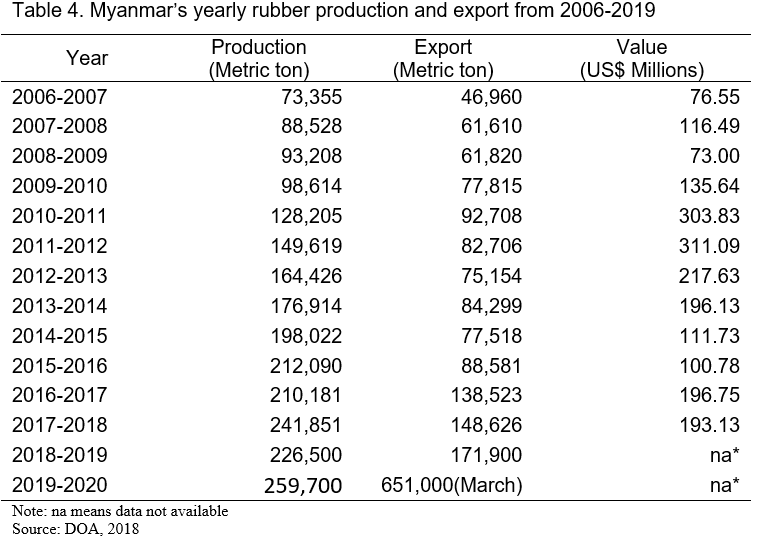

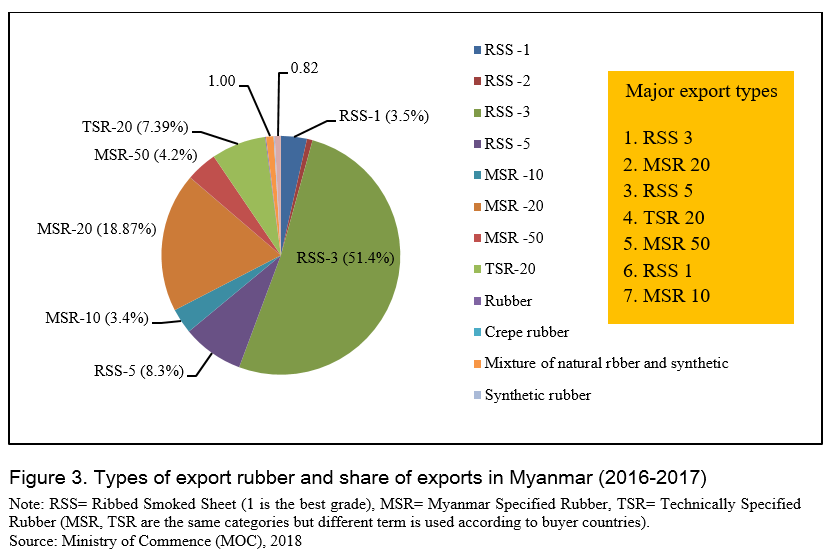

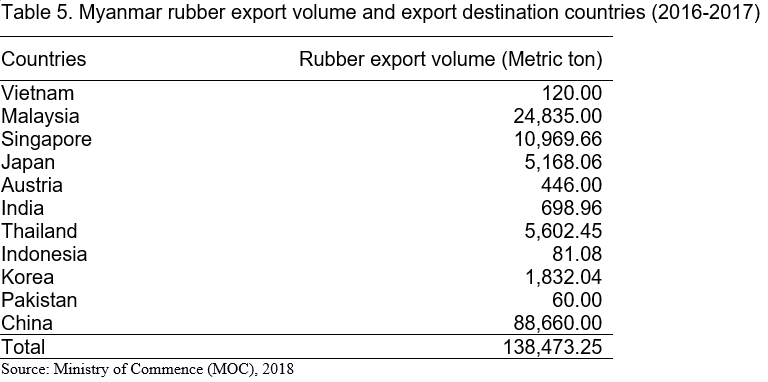

Myanmar’s yearly rubber production and export from 2006 to 2017 are presented in Table 4. Production and export volume are gradually increasing trend during 2006-2019 while earning value was fluctuated based on the world rubber price changes. Rubber production was 226,500 MT and export was 171,900 MT in 2018-2019. The different types of export rubber and share of export destinations were also described in Figure 3. Myanmar rubber export volume by export destination countries in the year 2016-2017 was show in Table 5. China is the main buyer of Myanmar rubber in 2016-17.

Way forward Policy on natural rubber development in Myanmar

The major role of government in every country is proper planning or policymaking to develop their country. Therefore, the government and their policies become a crucial ingredient in any meaningful development. The rubber sector development has relied on government policy issues and Myanmar’s government had a long support for rubber as a strategic export crop to earn foreign income.

According to the country’s economic reform, State Law and Order Restoration Council (SLORC) government launched an Open Door policy in 1989 and the production of perennial crops was partially liberalized from the control in regulations, although it was still limited in routine. However, the rise of domestic rubber price was accelerated as the country opened its economy for the private sector and foreign investments. By mid-1990s, smallholders re-engaged themselves in the rubber production sector.

In 1994, Myanmar Perennial Crop Enterprise (MPCE) was established and the government gave more attention to the rubber industry. Another major new driver of rubber plantation area expansion was the government's policies that had been emphasized on industrial crop development. Since 2010, Myanmar’s economic policy is following market-oriented reforms and substantially has been increasing its integration into the world economy. The government conjectured that the rubber industry could be a major source of capital for modern economic growth.

Additionally, the strategy of rubber products sector held significant promise in terms of contributing to the export performance of Myanmar, while also driving improvements across the sector’s export value chain. The rubber products sector also had the potential to develop as a key industry to support the automobile industry in Myanmar in the future (Odaka, 2015).

Myanmar’s rubber industry has a huge market as a high demand for NR around neighboring countries. The neighboring countries such as China utilized 37% of world NR for their industrialization and India for 9% and South East Asian countries for 17% respectively (Markit, 2017). Therefore, Myanmar’s natural rubber export destination target would be set up by the strategic action for key stakeholders in rubber sector.

Moreover, Odaka (2015) pointed out that the national average yield was much lower than other rubber producing countries. Additionally, the problems in Myanmar are numerous and not confined to the low yield level. Moreover, it appears as a very complicated issue. The authors assumed that currently the major problems for the rubber industry in Myanmar would be:

- Land tenure;

- Outdated recommended clones;

- Scarcity of skilled labor ;

- Limited access to improved technology;

- Impact of climate change;

- Lack of quality product market and quality control;

- Weak correlation with world rubber price;

- Poor bargaining power of farmer; and

- Inefficient transportation facilities

However, all the problems were listed without surveying and analyzing the related factors. To date, it has become necessary to survey key predicaments, analyze the structure of the problem and find out intervention areas to improve competitiveness for further developments of Myanmar rubber industry by key stakeholder participation. The empirical researches can provide understanding to policymakers for the priority and policies that can protect the livelihood of stakeholders and the way forward to enhance competitiveness of the rubber industry.

CONCLUSION

Myanmar’s rubber sector is chosen by the state priority for export promotion strategy. By comparing the world production and consumption of natural rubber (NR) and synthetic rubber (SR,) it is assumed that the world rubber production had a surplus NR in the last five years and a shortage SR in five years of current decades and these surpluses and shortages were balanced in the current world rubber consumption. Myanmar became the 6th largest rubber producer in the world rubber market in 2018. World bank studies estimated future World NR demand will be accelerated again as a result of increasing demand in lower and middle-income countries and sustained demand of China, India, the United States, and Japan while with the movement away from rubber production in Malaysia and Singapore and limited scope for rubber expansion in Indonesia, Myanmar could become an important rubber exporter in the rubber producing countries. Therefore, Myanmar’s rubber sector would compete with other rubber producing countries by overcoming current constraints and limitations of stakeholders along the value chain.

Regarding Myanmar’s natural rubber sector development, it would have the effective rubber law and act according to relevant development policies in time. Moreover, the rubber related institutes and professional government organizations need to develop as the result of the policy context and rubber law as other neighboring rubber producing countries. These institutes would became powerful and the most responsible units for rubber industry development. The institute would provide valuable research results not only in terms of technical outputs which would provide technical knowledge and adoption of high yielding varieties for increasing yield in Myanmar but also economic and market demand and supply estimation of value chain development for future.

Moreover, a vital move would be to transform institutional structures. Development of rubber production by implementing capacity building and human resources management programs for all stakeholders and revising the rubber related law and act. Enforcing implementation of rubber development policy including these programs for human resource development might give positive impact for Myanmar’s natural rubber industry. Although Myanmar adopted the institutional development and transformation policy, it needed to follow the experiences and transformation model as other rubber producing countries to gain competitiveness of the rubber industry. The transformation in Myanmar rubber industry, would all depend on the performances of the country’s powerful institutions to implement the rubber development forward policy.

REFERENCES

ANRPC, 2019. "Natural Rubber Trends Statistics", August - December 2019, Association of Natural Rubber Production Countries.

Chan, C., Joy, J., Maria, H. J., & Thomas, S. 2013. Natural rubber-based composites and nanocomposites: state of the art, new challenges and opportunities. Nat. Rubber Mater. Chapter, 1, 2.

Depatment of Agriculture. 2018. Situation of Myanmar Rubber Industry and Progress Report, Office No.50, Nay Pyi Taw, Perennial Crop Division, Department of Agriculture, Ministry of Agricultre, Livestock and Irrigation.

Depatment of Agriculture. 2019. Supply and demand modelling of natural rubber for Myanmar, Presentation on Workshop on Supply, Demand and Modelling of Natural Rubber Industry. Hotel Dawei, Dawei City. Tanintharyi Region, Myanmar.

Dr. Lakshman Rodrigo & Dr. Enoka Munasinghe, 2011. Business Times, Rubber tree should not only be for latex but for carbon trading too!, http://www.sundaytimes.lk/110710/ BusinessTimes/bt08.html http://

Ferreira, M., Moreno, R. r. M., Gonçalves, P. S., & Mattoso, L. H. 2002. Evaluation of natural rubber from clones of Hevea brasiliensis.

Global Rubber Market, 2019. No revival of Natural Rubber prices until 2025: Rubber expert, https://globalrubbermarkets.com/141343/no-revival-of-natural-rubber-pric...

Malaysia Rubber Board. 2018. Natural Rubber Statistics, Unit Kajian Kemajuan Pasaran, Bahagian Ekonomi dan Pasaran Getah: Malaysian Rubber Board. pp 2-6.

Markit, I. 2017. Chemical Economics Handbook, Rubber, Natural. from https://ihsmarkit.com/products/natural-rubber-chemical-economics-handbook.html.

Matthew Harder, 2018. Natural Rubber Vs Synthetic Rubber – The price relationship and demand switch ability, https://www.halcyonagri.com/ natural-rubber-vs-synthetic-rubber-the-price-relationship-and-demand-switchability/

MOC. (Ministry of Commence) 2015. National Export Strategy Rubber Sector Strategy 2015-2019, Ministry of Commence MOC.). Nay Pyi Taw.

National Export Strategy (2019). Rubber Sector Strategy, 2015-2019. Retrieved form https://www.myantrade .org/ files/.

Odaka, K. 2015. Setting the Conditions for Stable Economic Development- Reflections on the Outcomes of an Economic Policy Support Project for Myanmar. The Program for Economic Development in Myanmar, FINAL REPORT, pp 21-43.

Van Asselt, J., Htoo, K., & Dorosh, P. A. 2017. Prospects for the Myanmar rubber sector: an analysis of the viability of smallholder production in Mon State (Vol. 1610): Intl Food Policy Res Inst.

World Bank. 2016. Commodity Markets Data. Retrieved from www.worldbank. org/en/research/commodity-markets.

Woods, K. 2012. The political ecology of rubber production in Myanmar: an overview. Global Witness, Yangon, Myanmar.

Workman, D. 2019. Natural Rubber Exports by Country. Retrieved from http:// www.worldstopexports.com/natural-rubber-exports-country.

Myanmar’s Natural Rubber Forward Policy: How to do it?

ABSTRACT

Rubber production is central in economic development and it is also the second most agricultural export item followed by beans and pulses. Natural rubber production, consumption information of world rubber market and Myanmar rubber sector are done by desk review and conceptual frame work is formulated to cover the current situation and alternative forward policies by stakeholder participation approach. By comparing world production and consumption of natural rubber (NR) and synthetic rubber (SR,) there is slightly higher production than consumption in most of the years of the last decade. Therefore, it could be assumed that world rubber production was surplus NR in the last five years and shortage SR in five years of current decades and these surpluses and shortages were balanced in the current world rubber consumption. Myanmar became the 6th largest rubber producers in the world rubber market in 2018. NR consumption will be projected to grow by 5% per year through 2025 by the World Bank. In the future, World NR demand will be accelerated again as a result of increasing demand in lower and middle-income countries and sustained demand of China, India, the United States, and Japan while with the movement away from rubber production in Malaysia and Singapore and limited scope for rubber expansion in Indonesia, Myanmar could become an important rubber exporter in the rubber producing countries. However, the national average yield of Myanmar rubber was much lower than other rubber producing countries with many constraints and limitations of stakeholders along the value chain. Regarding Myanmar’s natural rubber sector development, the rubber related institutes and professional government organizations need to develop as the result of the policy context and rubber law. These institutes would became powerful and the most responsible units for rubber industry transformation. Moreover, revisions of laws and acts are needed several times to transform the rubber industry. Development of the rubber sector would be done by implementing capacity building and human resource management programs for all stakeholders and revising the rubber related laws and acts. In case of the transformation, this should be performed by the powerful institutions to implement the rubber development forward policy in Myanmar.

Keywords: policy, rubber, key stakeholder, participatory, export, world market

INTRODUCTION

Natural rubber industry in Myanmar

Myanmar’s agricultural sector dominates the economy, contributing 25.6% of gross domestic product (GDP), and employing more than 60% of the workforce (National Export Strategy, 2019). Among several crop productions in Myanmar, rubber production is central in economic development and it is also the second most agricultural export item followed by beans and pulses. Therefore, the rubber industry has been chosen as one of the priority sectors in Myanmar’s export strategies. Moreover, Myanmar's geographic position and climate make a potential driver for growth and development of rubber production. It is also important for economic development because the rural people from rubber growing areas have made their living from downstream and upstream sector of the rubber industry (National Export Strategy, 2015-2019).

Myanmar’s rubber industry had about 0.65 million hectares plantation area which employed about 400,000 workers and had experienced huge natural rubber market demand from neighboring countries (Department of Agriculture, 2019). Therefore, Myanmar became one of the largest rubber producers around the world. However, the national average yield per area was about 780 kg/ha and lower than that of other rubber producing countries (1,450 kg/ha- Malaysia and 1,417 Thailand) (ANRPC, 2019). And it also produced poor quality rubber with the low market price.

Rubber production in Myanmar is centered in Mon State. It is bounded by Bago Region to the north, Kayin to the east, and Tanintharyi to the south. It also shares a short southeastern border with Thailand. Mon State is one of the small States in Myanmar, but, with a population of two million inhabitants, so that it is relatively densely populated. The high population density makes it an economically important region. The central part of the state has the greatest concentration of the rubber industry. There are also various types of rubber markets and market participants, from brokers to exporters. Moreover, different farm sizes of rubber farmers are found in Mon State. Additionally, different kinds of rubber processing industries like Technical Specified Rubber (TSR) factories and value-added processing like rubber rings and balloons factories can be found (Van et al., 2017).

Objectives of the study

METHODOLOGY

Natural rubber production, consumption information of world rubber market and Myanmar rubber sector are collected from desk reviews and various data sources. Conceptual frame work is formulated to cover the current situation and alternative forward policies by stake holder participation approach.

RESULTS AND DISCUSSION

World natural and synthetic rubber production, consumption and export

In 1888 onwards, the mass production of automobiles created the increased demand for pneumatic tyres, which were made exclusively of NR and it was considered a golden age in terms of demand for NR. Before World War II, rubber products used 100% of NR. At that time, when the word rubber was mentioned, most people associated it with NR. Even latter-days, around 60% of NR was used in the production of tires. Although this might have been appropriate before World War II, synthetic rubber (SR) had grown since then to assume an important position.

During World War II, Japan’s occupation in most of the countries of Southeast Asia blockaded the supply of NR to industrial requirement from the West. It was a cause for concern and these countries responded vigorously, by investigating and searching SR for NR on a large-scale basis. Therefore, the development of SR, which was initiated politically and was strategically motivated, emerged as the most serious threat to NR, although SR production technology was intensive and less dependent on a skill-labor force. Its payment was also high compared to the production of NR latex on estates (Chan et al., 2013).

The production of SR was prompted by cheap and relatively constant supplies of petrochemical feedstock. However, it could not compete with NR’s capacity because the NR has good tensile, strength, friction, abrasion resistance and renounces properties of NR which override to SR. According to its modified qualities, NR cannot be replaced with other substances (Ferreira, Moreno, Gonçalves, & Mattoso, 2002). Moreover, the increase in demand for NR over SR is related to widespread concerns about global warming, deteriorating ecosystems and depleting sources of fossil fuels. In global environmental point of view, the rubber tree is capable of fixing ca. 1 MT of CO2 during its 30-year economic life cycle and therefore, within a hectare of rubber having over 300 trees, a minimum of 300 MT of CO2 is available for trade (Lakshman Rodrigo & Enoka Munasinghe, 2011). Additionally, it has renewable natural value with its premium quality because in the case of tire (passenger car, truck, bus etc.) production, there are certain amounts NR required, with each rubber type performing specific functions (Matthew Harder, 2018).

Annual world NR latex consumption gradually increased from 170,000 tons to 300,000 tons between 1960 and 1980. In the mid-1980s, total demand for NR latex took off, subsequently growing exponentially. This was the critical juncture of the transition of NR latex industries from the West to East countries. The NR demand take-off was also precipitated by the prevention of transmission of the human immunodeficiency virus (HIV) and hepatitis B with the increase in the use of NR latex gloves (Chan et al., 2013).

World production and consumption of NR and SR from 2001 to 2017 are summarized in Table 1. By comparing world production and consumption of NR and SR, there is slightly higher production than consumption in most of the years of last decade. Therefore, it could be assumed that world rubber production over the last five years and shortage of SR in five years of current decades and these surpluses and shortages balanced the current world rubber consumption.

According to the 10 important countries that exported the highest dollar value worth of natural rubber during 2018, Thailand and Indonesia are the top one and two respectively with high proportion as over 60% (Table 2). Among the top ten exporting countries, Myanmar became one of the largest rubber producers around the world which makes it the 6th exporting country in the world rubber market in 2018.

Future world natural and synthetic rubber production and consumption

Although world NR production was slightly higher than NR consumption in several years as shown in Table 1, the global NR consumption is expected to grow at 3.6 % to 14.7 million tons and projected to grow by 5% per year through 2025 ( Global Rubber Market, 2019 and World Bank, 2016). The sector had faced reduced demand in recent years (2012-2016), compared with the previous period (2008-2011) which is shown in Table 1.

In the future, World NR demand will be accelerated again as a result of increasing demand in lower and middle-income countries and sustained demand of China, India, the United States, and Japan. At the same time, with the movement away from rubber production in Malaysia and Singapore and limited scope for rubber expansion in Indonesia, Myanmar could become an important rubber exporter in the rubber producing countries (Van, Htoo, & Dorosh, 2017).

Natural rubber industry in Myanmar’s economy

The commercial planting of rubber in Myanmar started since 1905, and it gradually increased in area to 4,000 hectares in 1909, 29,000 hectares in 1920, and 46,575 hectares in 1940 respectively. Then, in 1960, it reached 56,000 hectares. In particular, Myanmar became a large exporter of natural rubber among the NR producing countries by following the gradual liberalization of the agriculture sector in the 1990s and a surge in rubber prices in international markets in the 2000s and increase in investments of smallholder rubber farmers.

Additionally, a 30-year Master Plan of Ministry of Agriculture, Livestock and Irrigation (MOALI) for the Agriculture Sector (2000 - 2001 to 2030 - 2031) aims to convert 10 million acres (4.46 million ha) of ‘wasteland’ for private industrial agricultural production. The period between 2000 and 2010 was an epoch-making period for the rubber industry policy by the government. Myanmar government increasingly supported the development of the rubber sector. In 2004, the government also liberalized the rubber export policy by allowing both growers and dealers to export without first fulfilling the quota to Myanmar Perennial Crops Enterprise (MPCE) (Woods, 2012). Alternatively, it was estimated that the sector employed between only 350,000 and 400,000 workers, mainly in the plantation or upstream sector linked to planting and production of raw natural rubber. Therefore, the development of the sector, more particularly of its industry, could have high socio-economic impacts and become a driver of job creation.

The rubber plantation areas were instantaneously increased after 1994-1995 as a consequence of Open Door policy (1989) and the establishment of MPCE, focal institute of rubber industry in 1994 as shown in Figure 1. There was also a significant increase in rubber export after 2006-2007 because the government had liberalized the rubber export policy by allowing both growers and dealers to export without any restrictions. Thereafter, rubber plantation areas, tapping areas and production were steadily increased until present time. Figure 2 presented growth rate of rubber planting areas, tapping areas and production. Therefore, national policy context for rubber industry was vital for further development.

Rubber production in Myanmar is centered in Mon and Kayin States. The central part of the Mon State has the greatest concentration of rubber trees and rubber products. There are also various types of rubber markets and market participants, from brokers to exporters. Moreover, different farm sizes of rubber farmers are found in Mon and Kayin States. Additionally, different kinds of rubber processing industries like Technical Specified Rubber (TSR) factories, Ribbed Smoked Sheet (RSS) factories and value-added processing like rubber ring and balloons factories can be found (Van et al., 2017).

Moreover, Myanmar's geographic position and climate make a potential driver for growth and development of rubber production throughout the country. Table 3 presented rubber plantation areas and tapping areas of States and Regions in Myanmar. Among them, Mon State and Kayin State occupied about 50% of rubber planting areas and potential areas for investing in rubber related business.

Myanmar natural rubber production and export during 2006-2019

Myanmar’s yearly rubber production and export from 2006 to 2017 are presented in Table 4. Production and export volume are gradually increasing trend during 2006-2019 while earning value was fluctuated based on the world rubber price changes. Rubber production was 226,500 MT and export was 171,900 MT in 2018-2019. The different types of export rubber and share of export destinations were also described in Figure 3. Myanmar rubber export volume by export destination countries in the year 2016-2017 was show in Table 5. China is the main buyer of Myanmar rubber in 2016-17.

Way forward Policy on natural rubber development in Myanmar

The major role of government in every country is proper planning or policymaking to develop their country. Therefore, the government and their policies become a crucial ingredient in any meaningful development. The rubber sector development has relied on government policy issues and Myanmar’s government had a long support for rubber as a strategic export crop to earn foreign income.

According to the country’s economic reform, State Law and Order Restoration Council (SLORC) government launched an Open Door policy in 1989 and the production of perennial crops was partially liberalized from the control in regulations, although it was still limited in routine. However, the rise of domestic rubber price was accelerated as the country opened its economy for the private sector and foreign investments. By mid-1990s, smallholders re-engaged themselves in the rubber production sector.

In 1994, Myanmar Perennial Crop Enterprise (MPCE) was established and the government gave more attention to the rubber industry. Another major new driver of rubber plantation area expansion was the government's policies that had been emphasized on industrial crop development. Since 2010, Myanmar’s economic policy is following market-oriented reforms and substantially has been increasing its integration into the world economy. The government conjectured that the rubber industry could be a major source of capital for modern economic growth.

Additionally, the strategy of rubber products sector held significant promise in terms of contributing to the export performance of Myanmar, while also driving improvements across the sector’s export value chain. The rubber products sector also had the potential to develop as a key industry to support the automobile industry in Myanmar in the future (Odaka, 2015).

Myanmar’s rubber industry has a huge market as a high demand for NR around neighboring countries. The neighboring countries such as China utilized 37% of world NR for their industrialization and India for 9% and South East Asian countries for 17% respectively (Markit, 2017). Therefore, Myanmar’s natural rubber export destination target would be set up by the strategic action for key stakeholders in rubber sector.

Moreover, Odaka (2015) pointed out that the national average yield was much lower than other rubber producing countries. Additionally, the problems in Myanmar are numerous and not confined to the low yield level. Moreover, it appears as a very complicated issue. The authors assumed that currently the major problems for the rubber industry in Myanmar would be:

However, all the problems were listed without surveying and analyzing the related factors. To date, it has become necessary to survey key predicaments, analyze the structure of the problem and find out intervention areas to improve competitiveness for further developments of Myanmar rubber industry by key stakeholder participation. The empirical researches can provide understanding to policymakers for the priority and policies that can protect the livelihood of stakeholders and the way forward to enhance competitiveness of the rubber industry.

CONCLUSION

Myanmar’s rubber sector is chosen by the state priority for export promotion strategy. By comparing the world production and consumption of natural rubber (NR) and synthetic rubber (SR,) it is assumed that the world rubber production had a surplus NR in the last five years and a shortage SR in five years of current decades and these surpluses and shortages were balanced in the current world rubber consumption. Myanmar became the 6th largest rubber producer in the world rubber market in 2018. World bank studies estimated future World NR demand will be accelerated again as a result of increasing demand in lower and middle-income countries and sustained demand of China, India, the United States, and Japan while with the movement away from rubber production in Malaysia and Singapore and limited scope for rubber expansion in Indonesia, Myanmar could become an important rubber exporter in the rubber producing countries. Therefore, Myanmar’s rubber sector would compete with other rubber producing countries by overcoming current constraints and limitations of stakeholders along the value chain.

Regarding Myanmar’s natural rubber sector development, it would have the effective rubber law and act according to relevant development policies in time. Moreover, the rubber related institutes and professional government organizations need to develop as the result of the policy context and rubber law as other neighboring rubber producing countries. These institutes would became powerful and the most responsible units for rubber industry development. The institute would provide valuable research results not only in terms of technical outputs which would provide technical knowledge and adoption of high yielding varieties for increasing yield in Myanmar but also economic and market demand and supply estimation of value chain development for future.

Moreover, a vital move would be to transform institutional structures. Development of rubber production by implementing capacity building and human resources management programs for all stakeholders and revising the rubber related law and act. Enforcing implementation of rubber development policy including these programs for human resource development might give positive impact for Myanmar’s natural rubber industry. Although Myanmar adopted the institutional development and transformation policy, it needed to follow the experiences and transformation model as other rubber producing countries to gain competitiveness of the rubber industry. The transformation in Myanmar rubber industry, would all depend on the performances of the country’s powerful institutions to implement the rubber development forward policy.

REFERENCES

ANRPC, 2019. "Natural Rubber Trends Statistics", August - December 2019, Association of Natural Rubber Production Countries.

Chan, C., Joy, J., Maria, H. J., & Thomas, S. 2013. Natural rubber-based composites and nanocomposites: state of the art, new challenges and opportunities. Nat. Rubber Mater. Chapter, 1, 2.

Depatment of Agriculture. 2018. Situation of Myanmar Rubber Industry and Progress Report, Office No.50, Nay Pyi Taw, Perennial Crop Division, Department of Agriculture, Ministry of Agricultre, Livestock and Irrigation.

Depatment of Agriculture. 2019. Supply and demand modelling of natural rubber for Myanmar, Presentation on Workshop on Supply, Demand and Modelling of Natural Rubber Industry. Hotel Dawei, Dawei City. Tanintharyi Region, Myanmar.

Dr. Lakshman Rodrigo & Dr. Enoka Munasinghe, 2011. Business Times, Rubber tree should not only be for latex but for carbon trading too!, http://www.sundaytimes.lk/110710/ BusinessTimes/bt08.html http://

Ferreira, M., Moreno, R. r. M., Gonçalves, P. S., & Mattoso, L. H. 2002. Evaluation of natural rubber from clones of Hevea brasiliensis.

Global Rubber Market, 2019. No revival of Natural Rubber prices until 2025: Rubber expert, https://globalrubbermarkets.com/141343/no-revival-of-natural-rubber-pric...

Malaysia Rubber Board. 2018. Natural Rubber Statistics, Unit Kajian Kemajuan Pasaran, Bahagian Ekonomi dan Pasaran Getah: Malaysian Rubber Board. pp 2-6.

Markit, I. 2017. Chemical Economics Handbook, Rubber, Natural. from https://ihsmarkit.com/products/natural-rubber-chemical-economics-handbook.html.

Matthew Harder, 2018. Natural Rubber Vs Synthetic Rubber – The price relationship and demand switch ability, https://www.halcyonagri.com/ natural-rubber-vs-synthetic-rubber-the-price-relationship-and-demand-switchability/

MOC. (Ministry of Commence) 2015. National Export Strategy Rubber Sector Strategy 2015-2019, Ministry of Commence MOC.). Nay Pyi Taw.

National Export Strategy (2019). Rubber Sector Strategy, 2015-2019. Retrieved form https://www.myantrade .org/ files/.

Odaka, K. 2015. Setting the Conditions for Stable Economic Development- Reflections on the Outcomes of an Economic Policy Support Project for Myanmar. The Program for Economic Development in Myanmar, FINAL REPORT, pp 21-43.

Van Asselt, J., Htoo, K., & Dorosh, P. A. 2017. Prospects for the Myanmar rubber sector: an analysis of the viability of smallholder production in Mon State (Vol. 1610): Intl Food Policy Res Inst.

World Bank. 2016. Commodity Markets Data. Retrieved from www.worldbank. org/en/research/commodity-markets.

Woods, K. 2012. The political ecology of rubber production in Myanmar: an overview. Global Witness, Yangon, Myanmar.

Workman, D. 2019. Natural Rubber Exports by Country. Retrieved from http:// www.worldstopexports.com/natural-rubber-exports-country.