ABSTRACT

The Philippine sugarcane industry is contributing an annual revenue of about PhP 70 billion (IS$1.3billion). Close to 700,000 Filipinos are directly employed in sugar production and about 5-6 million more are indirectly employed (SRA, 2019). It can be found in many regions covering about 422,500 hectares with average annual yield of 57 tons/ha. The sugar yield of 5.1 tons/ha, however, is lower than other producing countries such as Columbia, Australia, Brazil, Guatemala, and Thailand. Low productivity is considered as the major issue besetting the industry. This can be attributed to production issues such as variety of planting materials, soil fertility, and irrigation. Also, the effects of climate change such as higher temperatures and drier conditions is contributed to low yield. These concerns can be addressed through improvement in the varieties of planting materials, establishment of sugarcane high yielding variety nurseries, improved fertilizer use and efficiency and improved irrigation systems. Policies also affect the sugar industry. Specifically, the recent policy on trade liberalization has potential major impacts to various stakeholders. It is seen to potentially affect local producers negatively. The domestic market might be flooded with imported sugar. This may cause potential labor displacement among farmers and workers in the sugar industry. The sugar industry liberalization would possibly affect 84,000 farmers and 720,000 industry workers as well as their families, resulting in a potential negative impact on the livelihood of up to five million Filipinos in over 20 provinces. On the other hand, positive effects are envisioned for the consumers at all levels, as they will benefit from lower prices of sugar. The competitiveness study funded by PCAARRD indicated that the country’s sugar is import and export competitive. However, the industry needs further support, which have to be provided before any serious consideration of liberalizing trade. Among the policies, PCAARRD fully supports RA 10659 or the Sugarcane Industry Development Act (SIDA). SIDA law, though enacted in 2015, is still in its infancy stage. Before the government gets into exporting of sugar, the industry needs to be more competitive through investments and to make sure that allocated funds really reaches the farmers. What can be done by the government is to fully implement the SIDA law to further strengthen the industry and solve the underspending of funds allocated under the Sugar Law and eventually prioritize the improvement of planting materials and the irrigation systems to increase yield.

INTRODUCTION

Looking at the Philippine Sugar Industry: Historical Background

Historically, sugar was the most important agricultural export of the Philippines, not only because of the foreign exchange earnings, but also because sugar was the source of wealth of the Filipino elite called the “hacienderos” or the landlords, owner of large area of farms. The major sugarcane-growing region in the Philippines is the Western Visayas or the Negros Island. In the 1950s up to 1960s, sugar accounted for more than 20% of Philippine exports. However, in the 1970s its share declined to half then down to only 7% in the 1980s. The main culprit was the depressed market for sugar. An increase in the world price of sugar had occurred in 1974 until 1976 where prices fell again and remained low for a few years before moving upward again toward the end of the decade. Sugar prices fell again in the early 1980s, bottoming in May 1985. In early 1990s, prices had recovered.

The Philippines was protected to a certain degree from fluctuations of the world price of sugar by the country's access to a protected and subsidized United States market. In 1913, the US Congress established free trade with Philippines, providing Filipino sugar producers unlimited access to the American market. In 1934, a quota system on sugar was enacted and remained in force until 1974. Although Philippine sugar exports to the United States were restricted during this period, the country continued to enjoy a relatively privileged position. Philippine quotas for the United States in the early 1970s accounted for 25% to 30% of the total market. After the quota law terminated in 1974, Philippine sugar was sold on the open market, generally to unrestricted destinations. On May 5, 1982, the United States reestablished a quota system for the importation of sugar. Allocations were based on a country's share in sugar trade with the United States during the 1975-81 period, the period during which Philippine sugar exports to the United States had dwindled. The Philippine allotment was 13.5%.

As a consequence, shipments to the United States declined. The decline of the sugar industry was complicated by the monopolization that took place during the martial law period and the persistent market failures. In response to declining price in sugar, then President Ferdinand Marcos ordered the establishment of the Philippine Sugar Commission (PHILSUCOM) in 1976 by virtue of Presidential Decree No. 388 and amended by Presidential Decree Nos. 775 and 1192. The Commission was given the sole power to buy and sell sugar, to set prices paid to planters and millers, and to purchase companies connected to the sugar industry. To minimize the impact of world sugar prices fluctuations during those periods, PHILSUCOM then established a protective pricing policy and entered into a four-year, long-term contracts to sell 50% of exported sugar at an average price of $US 23.5 cents per pound although the prevailing world prices were then above $US 30 cents per pound. In May 1978, the Republic Planters Bank was established to provide adequate and timely financing to the sugar industry. After the Marcos regime, President Corazon Aquino established the Sugar Regulatory Authority (SRA) in 1986.

Establishment of the Sugar Regulatory Administration (SRA)

On May 28, 1986, Executive Order No. 18 established the current Sugar Regulatory Administration (SRA). The SRA was mandated to carry out the following functions:

- To institute an orderly system in sugarcane production for the stable, sufficient and balanced production of sugar for local consumption, exportation and strategic reserve;

- To establish and maintain such balanced relation between production and requirement of sugar and such marketing conditions that will ensure stabilized prices at a level reasonably profitable to producer and fair to consumers;

- To promote the effective merchandising of sugar and its products in the domestic and foreign markets so that those engaged in the sugar industry will be placed on a basis of economic viability; and

- To undertake such relevant studies as may be needed in the formulation of policies and in the planning and implementation of action programs required in attaining the purposes and objectives set forth under Executive Order No. 18.

Current state of the Philippine sugar industry

The Philippine sugarcane industry is contributing an annual revenue of about PhP 70 billion (US$1.37billion). Close to 700,000 Filipinos are directly employed in sugar production and about 5-6 million more are indirectly employed (SRA, 2019). The total land area devoted to sugarcane plantation in the Philippines is about 422,500 hectares with average yield posted at 57 tons/ha. Majority have landholdings of less than 5 hectares while very few have more than 100 hectares.

Sugarcane is grown in 17 provinces in the country, distributed in eight regions from northern Luzon (Isabela, Cagayan) to Mindanao (Bukidnon, Cotabato, Davao). The largest producer is Western Visayas, contributing 1.44 million metric tons or 55% share to the total sugarcane production. Northern Mindanao and Central Visayas followed with shares of 14.9% and 13.4%, respectively. The main players in the sugar industry are the big landlords, millers, distillers, and refineries. Victorias Milling in Negros Occidental is the largest producer of sugar in the country and one of the largest sugar millers and refineries in Asia. It supplies about 30% of the county’s daily need for refined sugar (Victoria Milling, 2019).

The 28 sugar mills operate at 66% capacity, giving an average recovery of 1.8 bags/ton cane (one bag=50 kilograms), which is low considering the sugar recovery of 2.4 bags in more efficient mills. About 43% (12) of these operating mills are located in Negros, Panay, Leyte and Cebu which produce 56% of the raw sugar in the country. Tarlac and Batangas contribute 20% while Bukidnon produces 24% of the raw sugar. There are also 14 sugar refineries with a combined capacity of 8,000 metric tons of refined sugar per day operating at 70% of mill capacity and four bioethanol distilleries producing 25% of the mandated ethanol market.

In terms of sugar yield, the Philippines has a lower sugar yield at 5.1 tons sugar/ha compared to other major producing countries such as Columbia with 2.38 times more sugar/ha; Australia with 2.15 times; Brazil with 1.88 times; Guatemala with 1.74 times; and Thailand, with 22% more. With respect to sugar recovery per ton of milled cane, Brazil recovers 58% more; Australia, 45%; China, 36.5%; and Thailand, 15% than the Philippines.

Almost all sugar produced in the country is consumed locally. Around 50% of domestic consumption is accounted for by industrial users, 32 % by households, and the remaining 18 % by institutions (e.g., restaurants, bakeries, and hospitals).. The largest Philippine sugar export market is the United States, as prices under the U.S. tariff rate quota system are normally higher than world market prices but lower than domestic prices (USDA, 2019).

In terms of prices, domestic sugar prices are typically higher compared to world prices. November 2019 retail prices of raw sugar in Metro Manila, as published in the Sugar Regulatory Administration (SRA), ranged from PhP 42.00 (US$ 0.08) 2to PhP 56.00 (US$1.10) per kilogram. On the other hand, world market prices, as published by the World Bank “pink sheet” or commodity-price data, showed that sugar prices are at $US 27 cents (or around PhP 13.56) per kilogram. Given the wide disparities in prices, even including transport and marketing costs, sugar in the world market could still be drastically cheaper compared domestically.

Like any other agricultural commodity, low productivity is one key issues that beset the sugar industry. Comparing Philippines with other Southeast Asian countries such as Thailand (sugarcane production is 100 ton canes per hectare), the country has low productivity which is estimated at 60 ton canes per hectare. This could be attributed to production issues such as variety of planting materials, soil fertility, and irrigation. Also, the effects of climate change such as higher temperatures and drier conditions (WWF, 2019) contributed to low yield. These concerns can be addressed through improvement in the varieties of planting materials, establishment of nurseries, improve fertilizer use and efficiency and improved irrigation systems.

Policies affecting the sugarcane industry

In the Philippines, sugar policy is generally controlled by the SRA specifically trade and domestic prices. Moreover, SRA, oversees and controls the domestic supply and demand of sugar every year. They control the supply under the “Quedan System”, which allocates what percentages of local production should be supplied to domestic market mainly to the US market and the international market. The Quedan System was established primarily to protect local sugarcane farmers from unstable prices by controlling the supply of sugar. During the start of each crop year, the SRA issues a central policy on production and marketing of sugar for the country, which allocates how much production goes to the domestic, export markets and reserves. These orders are adjusted as the season progresses.

The Biofuels Act

Republic Act (RA) 9367 or the Biofuels Act was signed on January 2007 making the Philippines the first Southeast Asian country to have biofuels policy in place (USDA, 2019). The Biofuels Act envisions less dependence on imported fuel, countryside development, shielding of the environment from toxic and greenhouse gases emitted by vehicles, and protection of food reserves and biodiversity.

However, the country was not able to comply with the goals set forth by the Act while other countries with biofuel programs continued to raise biofuel penetration (blending) rates in transport fuels. Similarly, a study conducted by FAO on the assessment of biofuels in the country showed that the mandates cannot be achieved sustainably such that there is not enough feedstock available to produce the ethanol required by the mandates and coconut oil has many more lucrative uses. However, from a farmers’ point of view, the mixed option to produce sugar and ethanol is best as the farmers receive a higher price for the product. But from the mill’s point of view, profit margins are lower. Despite of this, it is important to observe that the results are dependent on the price of oil and its effect on ethanol and gasoline prices. When the price of oil increases, producing ethanol becomes more lucrative, nevertheless feedstock availability would still be a constraint. Findings also showed that biodiesel production in the Philippines is not economical under current biodiesel prices. Biodiesel would be competing with pure coconut oil which is a valuable product with many uses in food and oleochemical industries (detergents, toothpaste, soap).

The sugar industry development act

The competitiveness study funded by PCAARRD indicated that the country’s sugar is import and export competitive. However, the industry needs further support, which have to be provided before any serious consideration of liberalizing trade. Among the policies, PCAARRD fully supports RA 10659 or the Sugarcane Industry Development Act (SIDA).

SIDA was approved on April 2015. The law mandates that the government provide PhP 2 billion (US$393,000) to the industry allocated as follows: (a) 15% for grants to block farms under the Block Farm Program; (b) 15% for socialized credit under the Farm Support and Farm Mechanization Programs; (c) 15% for research and development (R&D), capability building and technology transfer activities, extension, human resources development, and farm support programs; (d) 5% for scholarship grants to be provided to human resources development; and (e) 50% for infrastructure support programs.

SIDA primarily aims to enhance the competitiveness of the sugarcane industry and maximize the utilization of sugarcane resources, and improve the incomes of farmers/ farm workers, through improved productivity, product diversification, job generation, and increased efficiency of sugar mills. Under the law, SRA, the Department of Agriculture, the Department of Agrarian Reform and other concerned government agencies shall provide common service facilities such as farm machineries and implements, grants or start-up funding for the needed production inputs, technology adoption, livelihood and skills training and other development activities for the block farm and its members, and other support activities that may be identified.

The impact of climate change in the sugarcane areas is also felt in sugarcane producing areas. Hence, to solve this concern, improvement on the varieties of planting materials, establishment of nurseries, improve fertilizer use efficiency and improved irrigation systems should be considered.

SIDA law, though enacted in 2015, is still in its infancy stage. Before the government gets into exporting of sugar, the industry needs to be more competitive, through investments and to make sure that the allocated funds really reaches the farmers. What can be done by the government is to fully implement the SIDA law to further strengthen the industry and solve the underspending of funds allocated under the 2015 sugar law. What should be prioritized now is the improvement of planting materials and the irrigation systems to eventually increase yield.

Liberalization of sugar trade

The proposed liberalization of sugar imports foremost will bring cheaply produced sugar by more efficient and high sugar-yielding countries like Australia, Brazil and Thailand. The Philippine government has initiated moves to liberalize sugar imports in the country for the first time. In 2018, the Sugar Regulatory Administration (SRA) decided to allow the importation of a large volume of refined and raw sugar (up to 200,000 metric tons) at one instance. In the recent months, it also allowed additional importation of 100,000 metric tons of sugar. As a result, sugar prices have declined slightly from PhP 65.00 (US$1.28) per kilogram for refined quality sugar to around PhP 59.00 (US$1.16) per kilogram in March.

According to SRA, the government will liberalize sugar imports while maintaining tariff at around 40%. The planned liberalization of the sugar imports would benefit a greater number of consumers specifically the confectionary industry. According to the Philippine Confederation of Sugar Producers Associations, Inc. (CONFED), sugar liberalization will lower the price of sugar in the market making it beneficial to Filipino consumers. Figure 1 shows the percentage distribution of sugar by major consumers.

The industrial users benefit the most from liberalization of the sugar trade. It should be noted that the household consumers only comprised 13% of the total sugar consumption. Annually, each household only consumes 7-8 kilograms of sugar. The Philippine Confectionery Biscuit and Snack Association (PCBSA) indicated that liberalizing sugar imports would help the industry to further grow, as it will gain more savings from the cheaper price of sugar. These savings can be invested instead to boost their operations. The confectionary industry is a heavy user of sugar, as it constitutes 50-70% of confectionery items.

On the other hand, the planned liberalization of sugar imports is seen to potentially affect local producers negatively. The domestic market might be flooded with imported sugar. This may cause potential labor displacement among farmers and workers in the sugar industry. According to Mendoza (2019), for every 3 tons of sugar produced, one worker is directly employed and about seven are indirectly employed.

Further, the sugar industry liberalization would possibly affect 84,000 farmers and 720,000 industry workers as well as their families, resulting in a potential negative impact on the livelihood of up to five million Filipinos in over 20 provinces. Among these provinces are Cagayan, Isabela, Tarlac, Pampanga, Batangas, Cavite, Camarines Sur, Cebu, Leyte, Iloilo, Cadiz, Antique, Negros Occidental, Negros Oriental, North Cotabato, Davao Del Sur, Bukidnon, and Sultan Kudarat (Zubiri, 2019).

CONCLUSIONS AND WAYS FORWARD

Sugar is one of the most important traditional commodities in the Philippines which supports millions of farmers and farm workers as well as various manufacturing industries. While liberalization may provide cheaper sugar in the domestic market, pros and cons of this policy should be carefully weighed as it could potentially affect local farmers. Services and technologies are provided to support the primary production of sugarcane. PCAARRD has funded the development of a technology, NutrioTM, a foliar biofertilizer that makes the plant grow healthy and boost the yield of sugarcane. It also reduces chemical fertilizer usage, thereby reducing the cost of production. NutrioTM has been tested in the in Tarlac, Philippines and was found to increase the yield to 156 tons of cane per hectare. Based on the results of the research, NutrioTM is best used in combination with half recommendation of inorganic or chemical fertilizers. Two (2kg) of NutrioTM is applied twice per cropping season of sugarcane every two months and three to four months of planting. The use of the product will result to greener and healthier plants and reduced chemical fertilizer usage. Thus, increased in crop yield and profit. Further, it has been observed that by applying NutrioTM in combination with inorganic fertilizers or farmers practice will increase the yield by 19 % and 37 % in terms of monetary value in comparison with the full inorganic application. The application using the full recommendation of the product in comparison with full recommendation of inorganic fertilizers according to the results is almost comparable. In terms of addition of labor, this will be an added cost for the spraying of chemicals to crops. However, despite the increase in the labor cost, it will not still be as high as compared to the use inorganic fertilizers alone. The Council has also invested in improving the mechanization of sugar production. Among the outputs of that investment is the technology on automated furrow irrigation systems which seeks to provide irrigation with lesser labor.

REFERENCES

Food and Agriculture Organization. Meeting the mandates set for liquid biofuels for transport in the Philippines http://www.fao.org/3/CA2642EN/ca2642en.pdf

Mendoza, T. C. 2019. Multiple threats to PH sugar industry. https://opinion.inquirer.net/119717/multiple-threats-to-ph-sugar-industry

Philippine News Agency. 2019. Who benefits the most from sugar import liberalization? Retrieved: https://www.pna.gov.ph/articles/1060647

Sugar Regulatory Administration. 2019. Retrieved from: https://www.sra.gov.ph/

United States Department of Agriculture (USDA). 2019. https://www.fas.usda.gov/data/philippines-sugar-annual-3

Victoria Milling Company, Inc. Retrieved from: http://www.victoriasmilling.com/about_us/business_segments/power

World Bank. 2019. Retrieved from: http://pubdocs.worldbank.org/en/169031559692506553/CMO-Pink-Sheet-June-2019.pdf

World Wide Fund. 2019. Philippines Study Suggests New Planting Season, Farming Practices for Sugar Cane in the Face of Changing Climates. https://wwf.org.ph/resource-center/story-archives-2019/climate-change-ef...

Zubiri, J.M. 2019. Sponsorship speech of Senate Resolution No. 213, Senate of the Philippines

Initiatives and Implications of Philippine Sugar Liberalization

ABSTRACT

The Philippine sugarcane industry is contributing an annual revenue of about PhP 70 billion (IS$1.3billion). Close to 700,000 Filipinos are directly employed in sugar production and about 5-6 million more are indirectly employed (SRA, 2019). It can be found in many regions covering about 422,500 hectares with average annual yield of 57 tons/ha. The sugar yield of 5.1 tons/ha, however, is lower than other producing countries such as Columbia, Australia, Brazil, Guatemala, and Thailand. Low productivity is considered as the major issue besetting the industry. This can be attributed to production issues such as variety of planting materials, soil fertility, and irrigation. Also, the effects of climate change such as higher temperatures and drier conditions is contributed to low yield. These concerns can be addressed through improvement in the varieties of planting materials, establishment of sugarcane high yielding variety nurseries, improved fertilizer use and efficiency and improved irrigation systems. Policies also affect the sugar industry. Specifically, the recent policy on trade liberalization has potential major impacts to various stakeholders. It is seen to potentially affect local producers negatively. The domestic market might be flooded with imported sugar. This may cause potential labor displacement among farmers and workers in the sugar industry. The sugar industry liberalization would possibly affect 84,000 farmers and 720,000 industry workers as well as their families, resulting in a potential negative impact on the livelihood of up to five million Filipinos in over 20 provinces. On the other hand, positive effects are envisioned for the consumers at all levels, as they will benefit from lower prices of sugar. The competitiveness study funded by PCAARRD indicated that the country’s sugar is import and export competitive. However, the industry needs further support, which have to be provided before any serious consideration of liberalizing trade. Among the policies, PCAARRD fully supports RA 10659 or the Sugarcane Industry Development Act (SIDA). SIDA law, though enacted in 2015, is still in its infancy stage. Before the government gets into exporting of sugar, the industry needs to be more competitive through investments and to make sure that allocated funds really reaches the farmers. What can be done by the government is to fully implement the SIDA law to further strengthen the industry and solve the underspending of funds allocated under the Sugar Law and eventually prioritize the improvement of planting materials and the irrigation systems to increase yield.

INTRODUCTION

Looking at the Philippine Sugar Industry: Historical Background

Historically, sugar was the most important agricultural export of the Philippines, not only because of the foreign exchange earnings, but also because sugar was the source of wealth of the Filipino elite called the “hacienderos” or the landlords, owner of large area of farms. The major sugarcane-growing region in the Philippines is the Western Visayas or the Negros Island. In the 1950s up to 1960s, sugar accounted for more than 20% of Philippine exports. However, in the 1970s its share declined to half then down to only 7% in the 1980s. The main culprit was the depressed market for sugar. An increase in the world price of sugar had occurred in 1974 until 1976 where prices fell again and remained low for a few years before moving upward again toward the end of the decade. Sugar prices fell again in the early 1980s, bottoming in May 1985. In early 1990s, prices had recovered.

The Philippines was protected to a certain degree from fluctuations of the world price of sugar by the country's access to a protected and subsidized United States market. In 1913, the US Congress established free trade with Philippines, providing Filipino sugar producers unlimited access to the American market. In 1934, a quota system on sugar was enacted and remained in force until 1974. Although Philippine sugar exports to the United States were restricted during this period, the country continued to enjoy a relatively privileged position. Philippine quotas for the United States in the early 1970s accounted for 25% to 30% of the total market. After the quota law terminated in 1974, Philippine sugar was sold on the open market, generally to unrestricted destinations. On May 5, 1982, the United States reestablished a quota system for the importation of sugar. Allocations were based on a country's share in sugar trade with the United States during the 1975-81 period, the period during which Philippine sugar exports to the United States had dwindled. The Philippine allotment was 13.5%.

As a consequence, shipments to the United States declined. The decline of the sugar industry was complicated by the monopolization that took place during the martial law period and the persistent market failures. In response to declining price in sugar, then President Ferdinand Marcos ordered the establishment of the Philippine Sugar Commission (PHILSUCOM) in 1976 by virtue of Presidential Decree No. 388 and amended by Presidential Decree Nos. 775 and 1192. The Commission was given the sole power to buy and sell sugar, to set prices paid to planters and millers, and to purchase companies connected to the sugar industry. To minimize the impact of world sugar prices fluctuations during those periods, PHILSUCOM then established a protective pricing policy and entered into a four-year, long-term contracts to sell 50% of exported sugar at an average price of $US 23.5 cents per pound although the prevailing world prices were then above $US 30 cents per pound. In May 1978, the Republic Planters Bank was established to provide adequate and timely financing to the sugar industry. After the Marcos regime, President Corazon Aquino established the Sugar Regulatory Authority (SRA) in 1986.

Establishment of the Sugar Regulatory Administration (SRA)

On May 28, 1986, Executive Order No. 18 established the current Sugar Regulatory Administration (SRA). The SRA was mandated to carry out the following functions:

Current state of the Philippine sugar industry

The Philippine sugarcane industry is contributing an annual revenue of about PhP 70 billion (US$1.37billion). Close to 700,000 Filipinos are directly employed in sugar production and about 5-6 million more are indirectly employed (SRA, 2019). The total land area devoted to sugarcane plantation in the Philippines is about 422,500 hectares with average yield posted at 57 tons/ha. Majority have landholdings of less than 5 hectares while very few have more than 100 hectares.

Sugarcane is grown in 17 provinces in the country, distributed in eight regions from northern Luzon (Isabela, Cagayan) to Mindanao (Bukidnon, Cotabato, Davao). The largest producer is Western Visayas, contributing 1.44 million metric tons or 55% share to the total sugarcane production. Northern Mindanao and Central Visayas followed with shares of 14.9% and 13.4%, respectively. The main players in the sugar industry are the big landlords, millers, distillers, and refineries. Victorias Milling in Negros Occidental is the largest producer of sugar in the country and one of the largest sugar millers and refineries in Asia. It supplies about 30% of the county’s daily need for refined sugar (Victoria Milling, 2019).

The 28 sugar mills operate at 66% capacity, giving an average recovery of 1.8 bags/ton cane (one bag=50 kilograms), which is low considering the sugar recovery of 2.4 bags in more efficient mills. About 43% (12) of these operating mills are located in Negros, Panay, Leyte and Cebu which produce 56% of the raw sugar in the country. Tarlac and Batangas contribute 20% while Bukidnon produces 24% of the raw sugar. There are also 14 sugar refineries with a combined capacity of 8,000 metric tons of refined sugar per day operating at 70% of mill capacity and four bioethanol distilleries producing 25% of the mandated ethanol market.

In terms of sugar yield, the Philippines has a lower sugar yield at 5.1 tons sugar/ha compared to other major producing countries such as Columbia with 2.38 times more sugar/ha; Australia with 2.15 times; Brazil with 1.88 times; Guatemala with 1.74 times; and Thailand, with 22% more. With respect to sugar recovery per ton of milled cane, Brazil recovers 58% more; Australia, 45%; China, 36.5%; and Thailand, 15% than the Philippines.

Almost all sugar produced in the country is consumed locally. Around 50% of domestic consumption is accounted for by industrial users, 32 % by households, and the remaining 18 % by institutions (e.g., restaurants, bakeries, and hospitals).. The largest Philippine sugar export market is the United States, as prices under the U.S. tariff rate quota system are normally higher than world market prices but lower than domestic prices (USDA, 2019).

In terms of prices, domestic sugar prices are typically higher compared to world prices. November 2019 retail prices of raw sugar in Metro Manila, as published in the Sugar Regulatory Administration (SRA), ranged from PhP 42.00 (US$ 0.08) 2to PhP 56.00 (US$1.10) per kilogram. On the other hand, world market prices, as published by the World Bank “pink sheet” or commodity-price data, showed that sugar prices are at $US 27 cents (or around PhP 13.56) per kilogram. Given the wide disparities in prices, even including transport and marketing costs, sugar in the world market could still be drastically cheaper compared domestically.

Like any other agricultural commodity, low productivity is one key issues that beset the sugar industry. Comparing Philippines with other Southeast Asian countries such as Thailand (sugarcane production is 100 ton canes per hectare), the country has low productivity which is estimated at 60 ton canes per hectare. This could be attributed to production issues such as variety of planting materials, soil fertility, and irrigation. Also, the effects of climate change such as higher temperatures and drier conditions (WWF, 2019) contributed to low yield. These concerns can be addressed through improvement in the varieties of planting materials, establishment of nurseries, improve fertilizer use and efficiency and improved irrigation systems.

Policies affecting the sugarcane industry

In the Philippines, sugar policy is generally controlled by the SRA specifically trade and domestic prices. Moreover, SRA, oversees and controls the domestic supply and demand of sugar every year. They control the supply under the “Quedan System”, which allocates what percentages of local production should be supplied to domestic market mainly to the US market and the international market. The Quedan System was established primarily to protect local sugarcane farmers from unstable prices by controlling the supply of sugar. During the start of each crop year, the SRA issues a central policy on production and marketing of sugar for the country, which allocates how much production goes to the domestic, export markets and reserves. These orders are adjusted as the season progresses.

The Biofuels Act

Republic Act (RA) 9367 or the Biofuels Act was signed on January 2007 making the Philippines the first Southeast Asian country to have biofuels policy in place (USDA, 2019). The Biofuels Act envisions less dependence on imported fuel, countryside development, shielding of the environment from toxic and greenhouse gases emitted by vehicles, and protection of food reserves and biodiversity.

However, the country was not able to comply with the goals set forth by the Act while other countries with biofuel programs continued to raise biofuel penetration (blending) rates in transport fuels. Similarly, a study conducted by FAO on the assessment of biofuels in the country showed that the mandates cannot be achieved sustainably such that there is not enough feedstock available to produce the ethanol required by the mandates and coconut oil has many more lucrative uses. However, from a farmers’ point of view, the mixed option to produce sugar and ethanol is best as the farmers receive a higher price for the product. But from the mill’s point of view, profit margins are lower. Despite of this, it is important to observe that the results are dependent on the price of oil and its effect on ethanol and gasoline prices. When the price of oil increases, producing ethanol becomes more lucrative, nevertheless feedstock availability would still be a constraint. Findings also showed that biodiesel production in the Philippines is not economical under current biodiesel prices. Biodiesel would be competing with pure coconut oil which is a valuable product with many uses in food and oleochemical industries (detergents, toothpaste, soap).

The sugar industry development act

The competitiveness study funded by PCAARRD indicated that the country’s sugar is import and export competitive. However, the industry needs further support, which have to be provided before any serious consideration of liberalizing trade. Among the policies, PCAARRD fully supports RA 10659 or the Sugarcane Industry Development Act (SIDA).

SIDA was approved on April 2015. The law mandates that the government provide PhP 2 billion (US$393,000) to the industry allocated as follows: (a) 15% for grants to block farms under the Block Farm Program; (b) 15% for socialized credit under the Farm Support and Farm Mechanization Programs; (c) 15% for research and development (R&D), capability building and technology transfer activities, extension, human resources development, and farm support programs; (d) 5% for scholarship grants to be provided to human resources development; and (e) 50% for infrastructure support programs.

SIDA primarily aims to enhance the competitiveness of the sugarcane industry and maximize the utilization of sugarcane resources, and improve the incomes of farmers/ farm workers, through improved productivity, product diversification, job generation, and increased efficiency of sugar mills. Under the law, SRA, the Department of Agriculture, the Department of Agrarian Reform and other concerned government agencies shall provide common service facilities such as farm machineries and implements, grants or start-up funding for the needed production inputs, technology adoption, livelihood and skills training and other development activities for the block farm and its members, and other support activities that may be identified.

The impact of climate change in the sugarcane areas is also felt in sugarcane producing areas. Hence, to solve this concern, improvement on the varieties of planting materials, establishment of nurseries, improve fertilizer use efficiency and improved irrigation systems should be considered.

SIDA law, though enacted in 2015, is still in its infancy stage. Before the government gets into exporting of sugar, the industry needs to be more competitive, through investments and to make sure that the allocated funds really reaches the farmers. What can be done by the government is to fully implement the SIDA law to further strengthen the industry and solve the underspending of funds allocated under the 2015 sugar law. What should be prioritized now is the improvement of planting materials and the irrigation systems to eventually increase yield.

Liberalization of sugar trade

The proposed liberalization of sugar imports foremost will bring cheaply produced sugar by more efficient and high sugar-yielding countries like Australia, Brazil and Thailand. The Philippine government has initiated moves to liberalize sugar imports in the country for the first time. In 2018, the Sugar Regulatory Administration (SRA) decided to allow the importation of a large volume of refined and raw sugar (up to 200,000 metric tons) at one instance. In the recent months, it also allowed additional importation of 100,000 metric tons of sugar. As a result, sugar prices have declined slightly from PhP 65.00 (US$1.28) per kilogram for refined quality sugar to around PhP 59.00 (US$1.16) per kilogram in March.

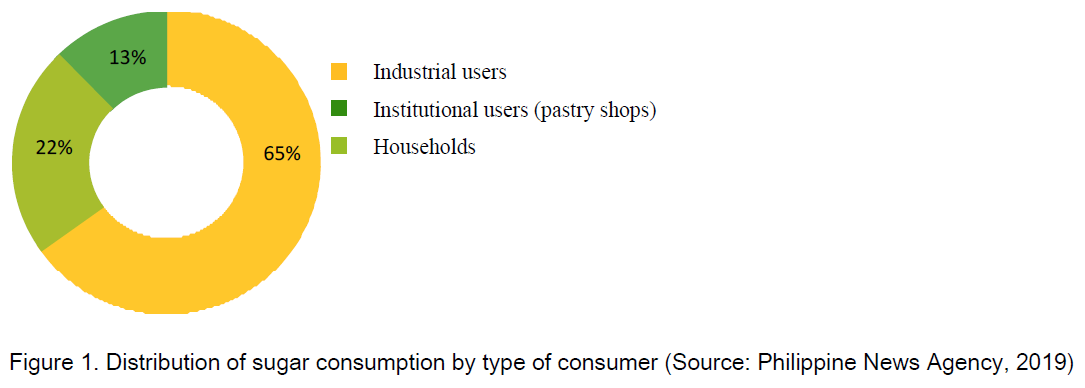

According to SRA, the government will liberalize sugar imports while maintaining tariff at around 40%. The planned liberalization of the sugar imports would benefit a greater number of consumers specifically the confectionary industry. According to the Philippine Confederation of Sugar Producers Associations, Inc. (CONFED), sugar liberalization will lower the price of sugar in the market making it beneficial to Filipino consumers. Figure 1 shows the percentage distribution of sugar by major consumers.

The industrial users benefit the most from liberalization of the sugar trade. It should be noted that the household consumers only comprised 13% of the total sugar consumption. Annually, each household only consumes 7-8 kilograms of sugar. The Philippine Confectionery Biscuit and Snack Association (PCBSA) indicated that liberalizing sugar imports would help the industry to further grow, as it will gain more savings from the cheaper price of sugar. These savings can be invested instead to boost their operations. The confectionary industry is a heavy user of sugar, as it constitutes 50-70% of confectionery items.

On the other hand, the planned liberalization of sugar imports is seen to potentially affect local producers negatively. The domestic market might be flooded with imported sugar. This may cause potential labor displacement among farmers and workers in the sugar industry. According to Mendoza (2019), for every 3 tons of sugar produced, one worker is directly employed and about seven are indirectly employed.

Further, the sugar industry liberalization would possibly affect 84,000 farmers and 720,000 industry workers as well as their families, resulting in a potential negative impact on the livelihood of up to five million Filipinos in over 20 provinces. Among these provinces are Cagayan, Isabela, Tarlac, Pampanga, Batangas, Cavite, Camarines Sur, Cebu, Leyte, Iloilo, Cadiz, Antique, Negros Occidental, Negros Oriental, North Cotabato, Davao Del Sur, Bukidnon, and Sultan Kudarat (Zubiri, 2019).

CONCLUSIONS AND WAYS FORWARD

Sugar is one of the most important traditional commodities in the Philippines which supports millions of farmers and farm workers as well as various manufacturing industries. While liberalization may provide cheaper sugar in the domestic market, pros and cons of this policy should be carefully weighed as it could potentially affect local farmers. Services and technologies are provided to support the primary production of sugarcane. PCAARRD has funded the development of a technology, NutrioTM, a foliar biofertilizer that makes the plant grow healthy and boost the yield of sugarcane. It also reduces chemical fertilizer usage, thereby reducing the cost of production. NutrioTM has been tested in the in Tarlac, Philippines and was found to increase the yield to 156 tons of cane per hectare. Based on the results of the research, NutrioTM is best used in combination with half recommendation of inorganic or chemical fertilizers. Two (2kg) of NutrioTM is applied twice per cropping season of sugarcane every two months and three to four months of planting. The use of the product will result to greener and healthier plants and reduced chemical fertilizer usage. Thus, increased in crop yield and profit. Further, it has been observed that by applying NutrioTM in combination with inorganic fertilizers or farmers practice will increase the yield by 19 % and 37 % in terms of monetary value in comparison with the full inorganic application. The application using the full recommendation of the product in comparison with full recommendation of inorganic fertilizers according to the results is almost comparable. In terms of addition of labor, this will be an added cost for the spraying of chemicals to crops. However, despite the increase in the labor cost, it will not still be as high as compared to the use inorganic fertilizers alone. The Council has also invested in improving the mechanization of sugar production. Among the outputs of that investment is the technology on automated furrow irrigation systems which seeks to provide irrigation with lesser labor.

REFERENCES

Food and Agriculture Organization. Meeting the mandates set for liquid biofuels for transport in the Philippines http://www.fao.org/3/CA2642EN/ca2642en.pdf

Mendoza, T. C. 2019. Multiple threats to PH sugar industry. https://opinion.inquirer.net/119717/multiple-threats-to-ph-sugar-industry

Philippine News Agency. 2019. Who benefits the most from sugar import liberalization? Retrieved: https://www.pna.gov.ph/articles/1060647

Sugar Regulatory Administration. 2019. Retrieved from: https://www.sra.gov.ph/

United States Department of Agriculture (USDA). 2019. https://www.fas.usda.gov/data/philippines-sugar-annual-3

Victoria Milling Company, Inc. Retrieved from: http://www.victoriasmilling.com/about_us/business_segments/power

World Bank. 2019. Retrieved from: http://pubdocs.worldbank.org/en/169031559692506553/CMO-Pink-Sheet-June-2019.pdf

World Wide Fund. 2019. Philippines Study Suggests New Planting Season, Farming Practices for Sugar Cane in the Face of Changing Climates. https://wwf.org.ph/resource-center/story-archives-2019/climate-change-ef...

Zubiri, J.M. 2019. Sponsorship speech of Senate Resolution No. 213, Senate of the Philippines