ABSTRACT

Coconut remains to be one of the most important crops and a major export of the Philippines. However, despite the continued boom of coconut exports, there has been no significant improvement in the coconut industry for the past years. A factor that has considerably affected the industry is the controversies surrounding the coconut levy fund. In February 2019, Pres. Rodrigo Duterte vetoed the consolidated bill creating the Coconut Farmers and Industry Trust Fund and the bill strengthening the Philippine Coconut Authority (PCA). These bills are deemed to address the stagnant growth of the coconut industry especially that these will provide funds for developmental programs, improvement of coconut farmer’s income, and improvement of the farms’ productivity, among others. However, given the current state of the industry and the veto of the coconut levy bills, other issues should be acted upon in relation to positioning of the coconut industry. A strategic direction could be the continued development of coconut while also encouraging the development of oil palm. Another is to focus investments in producing and/or developing other coconut products such as coconut water, coconut sugar, virgin coconut oil, coconut flour, and coco coir, among others."

INTRODUCTION

Current status of the coconut industry

Coconut, also known as the “tree of life”, is one of the most important crops in the Philippines. It is considered a major export, contributing 3.6% of the country’s gross value-added (GVA) in agriculture, next to banana, corn and rice. Indeed, the country remains to be a top producer and exporter of coconut worldwide (PSA 2019, Lapina and Andal 2017).

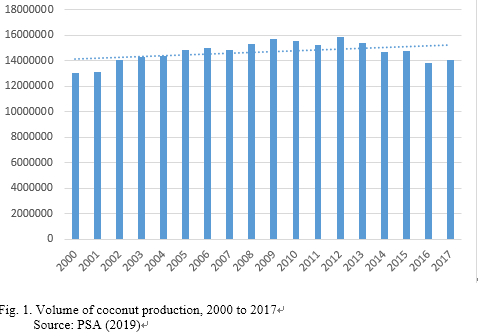

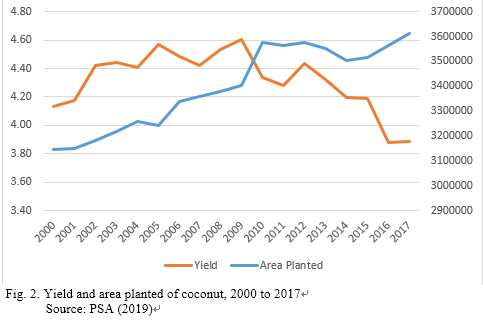

Generally, the coconut production had been stagnant from 2000 to 2017 (Fig. 1). There had been no significant increase in the production’s growth rate. The production has started to slow down in 2010 and 2013 mainly due to the infestation of the coconut scale insects and the occurrence of major typhoons, which destroyed huge number of coconut trees. Evidently, the yield has declined significantly since 2010. On the other hand, the area planted had generally increased from 2000 to 2017, which also caused the production growth in the recent years. The area planted accounted for almost 26% of the total agricultural land in 2015 that covers 68 provinces in the Philippines (Fig. 2) (PSA 2019, PCA 2019, Lapina and Andal 2017).

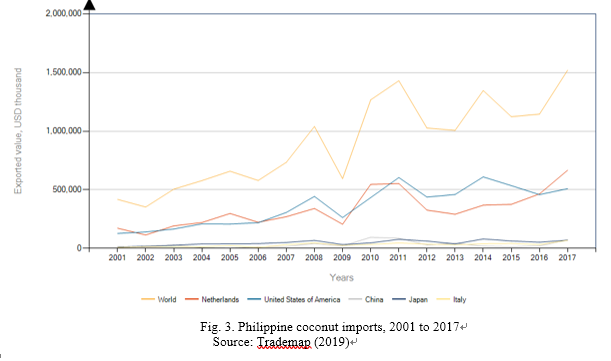

In terms of trade, the country continues to export huge amount of coconut products, about 70% of the country’s total coconut production. Among the coconut products exported include coconut oil (CNO), desiccated coconut (DCN), copra meal, and oleo chemicals (Ani and Aquino 2016). In 2017, the total export amounted to US $ 1, 519,639 (in thousands) with Netherlands and US as the top importing countries (Fig. 3) (Trademap 2019).

Despite the continued boom of exports, there has been no significant improvement in the coconut industry. In fact, the industry is still considered an “orphan” in the country’s agriculture due to poor investments. Also, high poverty incidence still prevails among millions of Filipino coconut farmers (Ani and Aquino 2016).

Among the identified problems in the industry are the unorganized supply chain, vulnerability of coconut to world price fluctuations, low farm productivity, which roots from infestations of cocolisap, the aging of current crop of coconut trees and poor nutrition, inadequate infrastructure support and poor farm to market roads, low allocation on research and development (R&D), and presence of corruption and bureaucracy. Another is the controversies surrounding the coconut levy fund (Ani and Aquino 2016, Lapina and Andal 2017).

This paper provides an overview of the status of the Philippine coconut industry, the policies that governed the coco levy fund and some strategic directions for its development. The first section provides the current situation of the coconut productivity. The second section provides a theoretical construct on the economic implications of levies and taxes while the third section discusses the coco levy policies and the current status of the coco levy proposed utilization policies. The last section presents some key strategic areas for the development of the coconut industry.

THE INEFFICIENCY OF TAXATION: A THEORETICAL CONSTRUCT

The economics of taxation

This section provides a theoretical construct on the implication of tax or levy policies on economic welfare. The important role of the government in providing foundation for the environment where tax or levy policies operate is also highlighted. It serves as basis in the analysis of how the coconut levy in the Philippines was established and how governance and administration directed the fate of this landmark tax or levy policy in the country.

Tax or levy system is primarily established to provide revenue for the government to finance essential expenditures on goods and services (Myles, 2009). For developing countries like the Philippines, tax provides the means to boost public expenditures on productivity-enhancing services such as infrastructure, research and development, public education and health care. However, while taxation and the related policies on it are viewed important in developing an economy, a central concern on public finance is the inefficiency due to distortions created by taxation or levies imposed.

The effects of taxation in an economy can be viewed through its impacts on economic welfare. Economic theory posits that economic welfare is the total benefit available to society provided by various economic transaction and situation (Economic Online, 2014). Economic welfare can be evaluated through consumer surplus and producer surplus. Consumer surplus is defined as the difference between the amount that the consumers are willing and able to pay for a good or service (as indicated by the demand curve) and the total amount they actually pay (as indicated by the market price). Producer surplus, on the other hand, captures the difference between the amount that the producer is willing to supply for a good or service (as indicated by the supply curve) and the actual amount received when he makes trade (as indicated by the market price).

Figure 4 shows the effect of taxation on economic welfare. Graphically, prior to the imposition of tax or any levy on a commodity or good, economic welfare is represented by area ABCDEF. This also denotes the total amount of the consumer surplus (Area ABC) and producer surplus (Area DEF). At this point, the level of economic welfare is determined by market forces. The quantity demanded and produced as well as the price paid and received are at equilibrium level of Q* and P*, respectively.

On the other hand, given the imposition of tax or levy, government policy intervention is injected in the scenario. Tax or levy imposed a two-pronged effect on prices of the commodity. Tax increases the price of commodity or good paid by the consumers (Pc) while it reduces the amount received by the producers (Ps). At the same time because of tax, quantity produced and demanded is reduced from Q* to QT. With the new level of prices and quantity of goods due to the additional cost from tax or levy, the consumer surplus and producer surplus are reduced to areas A and F, respectively. Portion of the reduction in the consumer and producer surpluses is transformed into tax revenues remitted to the government (Area BD). Tax revenues, represented by area BD, is considered part of the total economic welfare since the government use them to fund national programs and projects. However, the reduction in consumer and producer surpluses due to the imposition of taxes or levies is not entirely transmitted to the government in the form of tax or levy revenues. The total economic welfare is reduced by area CE which represents the deadweight loss or excess burden attributable to the inefficiency accompanying market distortions of taxation.

.PNG)

Levies, rents and corruption

Levies, enacted through policies and regulations, are temporary taxes collected and state-enforced non-voluntary contributions which are purposively allocated to a sector. Unlike income taxes, levies are not reverted to the government to form part of the national funds for redistribution to the entire economy (Taylor, 2012 and Ramos, 2013). In this sense, levies are considered funds that is sectoral in nature. Hence, in the case of coconut levies, property rights over the use of funds belong to the coconut industry.

In most cases and as practice in other countries, the utilization and management of levy funds are usually lodged to associations of the concerned sector. This institutional framework in managing levies, as claimed by Khan (2000), provides private agents access to income streams which they would have not had without the policy interventions. In this context, Khan defined levies as state-mediated rents that resulted from a politically organized transfers which converted public property into private ones. As such, state policies and regulations on levies give opportunities for possible rent-seeking which refers to all activities that seek to create, maintain and change rights and institutions to which rents are based. This effectively assigns the rights to the economic rent to a privileged portion of society. At worst, the privileged few given access to the funds through political assignments had little or nothing to do with the concerned sector, hence, property rights are attenuated. In the Philippines, Ramos (2013) pointed out that the coconut levy administered during the Marcos regime is considered a rent-allocation under a monopolistic corruption structure.

As cited in Ani and Aquino (2016), innate inefficiencies of coco levy imposition caused welfare loss. It has become disincentive to farmers since it adversely affected farm profitability (Aquino, 1993). Majority of the taxes on coconut products collected at any point along the marketing chain were borne by the farmers (Habito and Inatal, 1988). The farmers’ loss in income because of the coconut levy imposition was further aggravated by poor governance and administration of the levy returns.

The levy funds have become a tool for corruption. Corrupt practices in managing and implementing the coco levy returns allowed for welfare losses. As Taylor (2012) emphasized in his report, tax or levy can be an abused or abusive means resulting to ignoble ends. It has always been associated with extortion and misuse. The situation is a classic “double whammy” case where farmers were grabbed with benefits from the inefficiencies caused by levies or taxation policies and from the corruption that stolen the welfare due to the programs and projects created under the coconut levy funds.

COCONUT LEVY FUND

One of the most controversial issues, which has considerably affected the coconut industry, is the enactment of the coconut levy fund under the administration of former president Ferdinand Marcos in 1971. Coconut levy is the state-enforced tax imposed on coconut products and collected from the coconut farmers to be used supposedly for the development of the coconut industry and improvement of the lives of coconut farmers. However, until now, coconut farmers have not yet fully realized the benefits from this fund, and there were no evidences that the funds were actually utilized for the sector. In fact, only about 33% of the Php 9.68 billion or US$185.37 million (exchange rate at Php 52.22 per US$ 1.00), estimated total amount of levy in 1997, was used to support programs directly benefitting farmers (Ani and Aquino 2016).

The coconut levy fund was imposed through series of major funds, which were enacted between the 1970s and early 1980s, namely Coconut Investment Fund (CIF) levy, Coconut Consumer Stabilization Fund (CCSF), Coconut Industry Development Fund (CIDF), and Coconut Industry Stabilization Fund (CISF). CIF, established in 1971 through Republic Act 6260, was created supposedly to provide medium- and long-term financing for capital investments. CCSF, on the other hand, was used to provide subsidy for coconut-based products, fund investments in processing plants, R&D, and extension services. CIDF was created to establish, operate and manage the hybrid coconut seed farm for the national replanting program, while CISF was designed to support socio-economic and development programs (Ani and Aquino 2016).

After the Marcos regime, recovering the assets and properties, acquired through the coconut levy fund, has been a priority agenda of the next administrations. Through the Presidential Commission on Good Governance, significant amount of assets was recovered, currently amounting to around Php 100 billion or US$ 1.91 billion (PNA 2018). But, still, this recovered fund remains to be unutilized.

Both Senate and House have crafted several bills with regard to developing mechanisms on how to utilize and allocate the said fund. Yet, after almost four decades, there had been no actual law enacted to distribute and return this fund to coconut farmers.

Meanwhile, coconut farmers had high hopes that with the current administration under Pres. Rodrigo Duterte in which he signed a manifesto and committed to return the coco levy fund to farmers (Elemia 2019), things would be better. However, just recently, the President had vetoed the bill creating the coco levy trust fund.

Coconut levy twin bill

The consolidated bill Senate Bill No. 1233/ House Bill No. 5745, titled “An Act Creating the Coconut Farmers and Industry Trust Fund, Providing for its Management and Utilization, and for Other Purposes” and also known as the “Coconut Farmers and Industry Development Trust Fund Act”, aims to consolidate all assets and benefits emanating from the coconut levy, and create a Trust Fund for the benefit of coconut farmers and farm workers. It has the following key provisions (House of Representatives 2018):

- Mandates the creation of the Coconut Farmers and Industry and Trust Fund (CITF), which shall be for the ultimate benefit of coconut farmers and the coconut industry;

- Grants a reconstituted Philippine Coconut Authority the powers to supervise and manage the money and the new Coconut Farmers and Industry Development Plan;

- Removes the fixed term on the life of the fund, as both the Senate and the House agreed to allow the existence of the bill until the fund runs out;

- Sets aside every year Php 5 billion or US$ 05.75 million for the next 25 years or until the fund runs out as the yearly amount to be drawn from the coco levy fund, which will be spent on the following:

- 30% for shared facilities;

- 15% for scholarship program;

- 15% for empowerment of coconut farmer organization and their cooperatives;

- 30% for farm improvement to encourage self-sufficiency; and

- 10% for health and medical benefits;

- Provides an automatic appropriation of Php10 billion to the annual budget of the PCA from the GAA to augment the coconut farmers and development fund, increase the income, and support PCA’s developmental activities. The amount will be allocated as follows:

- 20% for infrastructure;

- 20% for replanting, planting, and establishment of hybrid coconut nurseries;

- 10% for intercropping;

- 15% for shared facilities;

- 10% for research and development, coconut disease prevention, control, and eradication;

- 5% for fertilization;

- 5% for new products and all derivatives of coconut oil, and marketing

- 10% for credit through Landbank and the Development Bank of the Philippines; and

- 5% for trainings of farmers through TESDA

A twin bill SB No. 1976/HB No. 8552, titled “An Act to Further Strengthen the Philippine Coconut Authority (PCA), Amending Presidential Decree No. 1468, Otherwise known as the ‘Revised Coconut Industry Code’, as Amended, and Appropriating Funds Therefore”, was also crafted in relation to the establishment of the coconut levy trust fund. This aims to ensure the effective utilization of the coconut levy funds, which will be managed by the Philippine Coconut Authority. It has the following key provisions (Committee on Agriculture and Food 2019):

- Expands the membership of the governing board of the PCA from seven (7) to fifteen (15), and provides six (6) seats to coconut farmers sector compromising two (2) representatives each from the island groups of Luzon, Visayas and Mindanao, and one (1) seat for the coconut processing industry sector; and

- Provides that the coconut farmer and the coconut processing industry representatives shall come from their respective organizations;

The bills creating the coconut trust fund, and strengthening the PCA were presented by Congress on January 17 and January 10, respectively, for the President’s approval.

In this regard, PCAARRD has expressed support to both of the bills, highlighting the role and possible contribution of DOST in developing a clear and implementable roadmap for the coconut industry. Specifically, DOST would contribute in identifying and setting directions for R&D initiatives and science-based solutions to address problems in the industry.

Veto of coconut bills

In February 2019, Pres. Duterte vetoed the consolidated bill creating the Coconut Farmers and Industry Trust Fund, as well as the bill strengthening the PCA.

The reconstitution of PCA was vetoed, prior to the creation of the trust fund, by the President for he thinks that the proposed bill allows for corruption of the coco levy fund, and bypass the role of the executive branch. Listed below are the specific reasons, as cited by Ranada (2019) and Elemia (2019):

- “PCA is not required to seek approval from executive branch”. The Palace thinks that the executive branch should also have oversight functions with PCA, instead of Congress alone, to avoid corruption of the coco levy funds. However, the proposed reconstitution of the PCA will, in fact, include executive branch officials in the governing board of PCA - the agriculture secretary as board chairman, finance and budget secretaries are members, and PCA administrator, who is a President’s appointee;

- “PCA authority on sale, dissolution of coco levy assets compromises executive branch actions on coco levy cases”. It was argued that the reconstitution will grant too much power to PCA and may diminish the power of the Department of Justice in terms of dealing with cases regarding the coco levy assets;

- “PCA board composition puts taxpayers’ money in hands of private individuals”. According to the Palace, the bill allows for private individuals to dominate the PCA, and might give them too much influence in the disbursement of public funds; and

- “PCA will end up like ‘corrupt-ridden’ Road Board”. The Palace is afraid that the proposed bill might allow for corruption and misappropriation of funds given that the reconstituted PCA will disburse Php 10 billion or US$ 191.50 million every year in perpetuity, which will only be subjected to review by Congress after 6 years.

With the return of the unsigned bill to Congress, stakeholders were afraid that the President will also veto its twin bill. This is because the reconstituted PCA will be the one in-charge of the coconut levy trust fund, as proposed by the Coconut Farmers and Industry Development Trust Fund Act.

As expected, the coconut trust fund act was vetoed week after rejecting the PCA reconstitution. The Palace cited three main reasons, as stated in their official statement (Malacañang Palace 2019):

- “The establishment of an effectively perpetual trust fund would violate Action 6, Section 29 of the 1987 Constitution”. It was argued that the bill will violate the provision of the 1987 Constitution stating that “[All] money collected on any tax levied for a special purpose shall be treated as a special fund and paid out for such purpose only. If the purpose for which the special fund was created has been fulfilled or abandoned, the balance if any shall be transferred to the general fund of the Government”. Whereas, the proposed bill will not actually create a perpetual trust fund; instead, it will put a 25-year limit or until the funds run out;

- The bill lacks a "limit on a covered land area for the entitlement to the benefits of the Trust Fund”. The Palace believes that not putting a limit might benefit more wealthy coconut farm owners than smallholders, who badly needs assistance. To limit the covered land area, actually, was the initial proposal of coconut farmers prior to crafting the coconut trust fund act. However, the proposed limit was removed in the bicameral; and

- “The broad powers given to the PCA undermine relevant regulations and safeguards that were established precisely to avoid abuses”. Similar to the previous bill, the Palace argues that PCA overseeing the disbursement of funds might end up to corruption. Coconut farmers, indeed, were hesitant to let PCA manage the funds, and proposed to create a separate trust fund committee under the President. However, this was removed again in the crafting of the proposed bill, particularly the Senate version.

KEY STRATEGIC AREAS IN DEVELOPING THE COCONUT INDUSTRY

Huge opportunities, not just for the coconut farmers but also for the coconut industry, were anticipated with the supposed enactment of the coconut trust fund act. In fact, the act has been seen as a “timely and necessary” measure in reviving the coconut industry given that the price of copra is continuously decreasing, and the country is experiencing decline in production. The coconut levy bill could have been the answer to the said problems especially that it will provide funds for developmental programs, improvement of coconut farmer’s income, and improvement of the farms’ productivity, among others.

Given the current state of the industry and the veto of the coconut levy bills, the question now is “how to position the coconut industry” and/or “what could be the entry points for development of the industry”. Another thing to ponder is that, if ever the coconut levy bill will be enacted in the near future, what could be the optimal way to position the industry.

A primary concern is the positioning of the coconut oil industry. Coconut oil is the top export product from coconut, which comprises almost 80% of the total coconut exports and, hence, generates the highest export earnings (PSA 2019). This oil, which is extracted from mature nuts through wet or dry (from dried nuts) process, can be processed into cooking oil, food ingredients, medicines, soaps, and detergents, among others. It is also known to have multiple health benefits (PEF 2016).

At present, the industry is experiencing decline in the supply of coconut oil mainly due to the significant drop in the yield and ‘stagnant to negative’ growth in the coconut production. In contrast, the demand for coconut oil has been growing substantially in the recent years. This can be attributed to consumers opting for healthier options in food and other products (Broaddus 2016).

Accompanying the increase in demand is the tight competition, not just with other coconut-producing and exporting countries, but also with other alternative crops such as corn, and soybean, among others (PEF 2016). In fact, there had been campaigns on the alleged negative impact of too much consumption of coconut oil. This had surely threatened the coconut industry particularly the livelihood of millions of coconut farmers and entrepreneurs. However, the campaign has been debunked by several studies saying that the blame should be put on the soybean oil (Dar 2017).

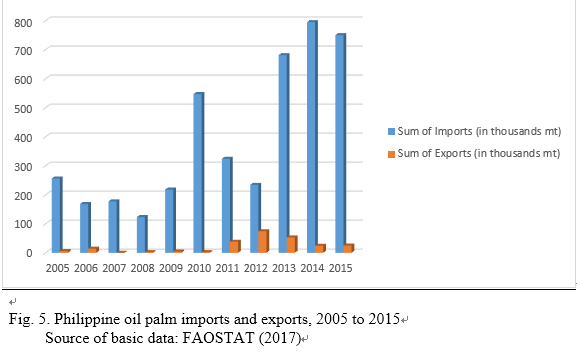

Another issue is the purported competition between coconut and palm oil. The Philippines is known to be a net importer of palm oil with almost 750 thousands mt of imports and 25 thousands mt of exports in 2015 (Fig. 5). Palm oil supplies 80% of the country’s vegetable oil. Currently, there is only 90,000 ha land area allotted for the production of oil palm trees, which only meets 10% of the domestic requirement (Agriculture 2018). This has been the main rationale for eyeing palm oil expansion in the country. However, many believe that this will threaten and might kill the coconut industry. Some even speculate that PCA would use the coco levy fund for the development of the palm oil industry. A research claimed that “oil palm is a big brother” such that it complements the coconut industry. It argued that the expansion of oil palm would aid in controlling coconut insect infestation, particularly by the coconut leaf beetle (CLB), and promote higher yield through adopting oil palm model in the coconut production (Pamplona 2017).

PCAARRD has also expressed support, in 2017, to develop both coconut and oil palm industry especially that the country is blessed with climatic condition highly suitable for both crops. Since coconut is very compatible with the country’s traditional farming system and grows in almost any kind of soil, it can be grown with other crops, particularly oil palm, in an intercrop system. The intercrop/s will provide additional sources of income for the farm households.

The most important advantage of oil palm over coconut is that it produces more oil per hectare (two to five times depending on the productivity of coconut). However, successful production and processing of oil palm is associated with exacting logistical requirements. This means that oil palm should be in plantation type production, where the production sector is highly integrated with processing.

Still, there is no need to choose between coconut and oil palm because they can co-exist profitably. As a strategic direction for the country, the continued development of coconut should be pursued while also encouraging the development of oil palm in areas appropriate for the crop. However, instead of coco levy, the government should allocate a separate fund from the annual regular government appropriation for the expansion of the palm oil industry. Still, the coco levy fund must be utilized to conduct R&D, and employ strategies, programs and policies for the benefit of the coconut industry.

On the other hand, while it is no doubt that coconut oil contributes significant amount of foreign earnings, the country must not remain complacent. There are speculations on the deteriorating position of coconut oil in the global vegetable oils market (Javier 2018). Hence, there is a need to keep up, and explore ways to either remain or be more competitive. It is also high time to diversify into new markets and/or other high-value coconut products.

A possible entry point is to boost the domestic demand for coconut oil through the Biofuels Act. The country could take advantage of the Biofuels Act, which proposes to increase the coconut biodiesel blend in automotive diesel from the current 2% to 5%, if this will be enacted soon. Aside from promoting cleaner fuel and emission, the increase in the coconut content of diesel would create new demand for the coconut oil; hence, could provide additional revenue for the coconut farmers. However, the Biofuels Act is still subject to review, and yet to be passed as a law (Simeon 2018).

Other than oil, the coconut industry remains to offer lot of opportunities that could be entry points for its development. The industry may focus its investments in producing and/or developing other coconut products such as coconut water, coconut sugar, virgin coconut oil, coconut flour, and coco coir. Indeed, coconut water, which is rich in minerals such as potassium, calcium, and magnesium, is gaining popularity as a drink in tropical countries. Coconut sugar and coconut flour are also widely used as healthier alternatives (Orbis 2018, Javier 2018, PEF 2016). Diversifying into this kind of products will generate more employment among small and medium enterprises, and will promote inclusive growth in the coconut industry (Javier 2018).

CONCLUSION

The coconut industry is an important pillar of Philippine agriculture. Its development would mean significant welfare improvement on the lives of millions of Filipino people. Many efforts have been exerted to finally claim back, for the benefits of the coconut farmers and their families, the billion worth coco levy funds. In positioning, and striving to reach the full potential of the coconut industry, the country should be persistent in pushing for the disbursement of the coco levy. The release of this funds, however, should be accompanied by a clear and implementable roadmap for the sector as well as transparent policies. While waiting for this mechanism to materialize, other issues in the industry should not be set aside and should be acted upon to achieve inclusive development.

REFERENCES

Agriculture (2018). “The facts: Addressing the campaign to stop the planting of oil palm trees in the Philippines.” Retrived from: https://www.pressreader.com/philippines/agriculture-9ggr/20180101/282467119278597.

Ani, PA. and A. Aquino (2016). “The Long Climb towards Achieving the Promises of the Tree of Life: A review of the Philippine Coconut Levy Fund Policies.” FFTC Agricultural Policy Articles 2016-01-28. Retrieved from: http://ap.fftc.agnet.org/ap_db.php?id=577&print=1.

Aquino, A.P. 1993. The Effects of Tax Policy on the Level and Distribution of Benefits from Technological Change in the Philippine Coconut Industry. Master Thesis on Agricultural Economics, University of the Philippines Los Baños.

Broaddus, H. (2016). “Supply and Demand in the Coconut Oil Market (Market Update). CentraFoods.” Retrieved from: http://www.centrafoods.com/blog/supply-and-demand-in-the-coconut-oil-market-market-update.

Elemia, C (2019). “'Na-Duterte kami:' Why farmers feel betrayed by coco levy vetoes.” Rappler. Retrieved from: https://www.rappler.com/newsbreak/in-depth/223809-farmers-reaction-coco-levy-vetoes.

Committee on Agriculture and Food (2019). House Bill 5745 Fact Sheet.

Dar, W. (2017). “State of the PH coconut industry and what must be done.” The Manila Times. Retrieved from: https://www.manilatimes.net/state-ph-coconut-industry-must-done/346624/.

House of Representative (2018). “House ratifies coco levy twin bills.” Retrieved from: http://www.congress.gov.ph/press/details.php?pressid=11090.

Javier, E. (2018). “The Philippine coconut industry in the long term.” Manila Bulletin Business. Retrieved from: https://business.mb.com.ph/2018/08/25/the-philippine-coconut-industry-in-the-long-term-2/.

Lapina, G. and E.G. Andal (2017). ASEAN Economic Community: Opportunities and Challengers for the Crops Sector.

Malacañang Palace (2019). Official statement re. veto of Senate Bill No. 1233/ House Bill No. 5745.

Myles, G. D. (2009), “Economic Growth and the Role of Taxation-Theory”, OECD Economics Department Working Papers, No. 713, OECD Publishing. http://dx.doi.org/10.1787/222800633678

Orbis (2018). Global Coconut Water Market and Coconut Oil Market 2018 By Demand, Consumption, Production, Top Regions, Key Manufacturers, Growth & Forecast Till 2023. Retrieved from: https://www.reuters.com/brandfeatures/venture-capital/article?id=38929.

Ramos, Charmaine G. 2013. The Power and the Peril: Producers Associations Seeking Rents in the Philippines and Colombia in the Twentieth Century. A Dissertation submitted to the Department of International Development of the London School of Economics, London, United Kingdom.

Pamplona, P (2017). “Oil Palm: Coconut’s “Big Brother”.” Agriculture Monthly. Retrieved from: https://agriculture.com.ph/2018/01/23/oil-palm-coconuts-big-brother/.

Peace and Equity Foundation (PEF) (2016). A Primer on PEF’s Priority Commodities: Industry Study on Coconut.

Philippine Coconut Authority (PCA). Coconut Statistics. Retrieved from: http://www.pca.da.gov.ph/index.php/2015-10-26-03-15-57/2015-10-26-03-22-41.

Philippine News Agency (PNA) (2018). “‘Historic' coco levy fund measure to benefit farmers: Nograles.” Retrieved from: http://www.pna.gov.ph/articles/1054883.

Philippine Statistics Authority (PSA) (2019). Data on Coconut Production, Yield, and Area Planted. Retrieved from http://countrystat.psa.gov.ph.

Ranada, P. (2019). “Duterte vetoes bill reconstituting Philippine Coconut Authority.” Rappler. Retrieved from: https://www.rappler.com/nation/223056-duterte-vetoes-bill-reconstituting-philippine-coconut-authority.

Taylor, Madeline. 2012. Is it a levy, or is it a tax, or both? Revenue Law Journal, 22 (1). Retrieved January 31, 2015, from http://epublications.bond.edu.au/rlj/vol22/iss1/7

Trademap (2019). List of importing markets for coconut exported by Philippines. Retrieved from: https://www.trademap.org/Country_SelProductCountry_TS_Graph.aspx? nvpm=1%7c608%7c%7c%7c%7c1513%7c%7c%7c4%7c1%7c1%7c2%7c2%7c1%7c2%7c1%7c1

|

Date submitted: Apr. 24, 2019

Reviewed, edited and uploaded: June. 13, 2019

|

The Philippine Coconut Industry: Status, Policies and Strategic Directions for Development

ABSTRACT

Coconut remains to be one of the most important crops and a major export of the Philippines. However, despite the continued boom of coconut exports, there has been no significant improvement in the coconut industry for the past years. A factor that has considerably affected the industry is the controversies surrounding the coconut levy fund. In February 2019, Pres. Rodrigo Duterte vetoed the consolidated bill creating the Coconut Farmers and Industry Trust Fund and the bill strengthening the Philippine Coconut Authority (PCA). These bills are deemed to address the stagnant growth of the coconut industry especially that these will provide funds for developmental programs, improvement of coconut farmer’s income, and improvement of the farms’ productivity, among others. However, given the current state of the industry and the veto of the coconut levy bills, other issues should be acted upon in relation to positioning of the coconut industry. A strategic direction could be the continued development of coconut while also encouraging the development of oil palm. Another is to focus investments in producing and/or developing other coconut products such as coconut water, coconut sugar, virgin coconut oil, coconut flour, and coco coir, among others."

INTRODUCTION

Current status of the coconut industry

Coconut, also known as the “tree of life”, is one of the most important crops in the Philippines. It is considered a major export, contributing 3.6% of the country’s gross value-added (GVA) in agriculture, next to banana, corn and rice. Indeed, the country remains to be a top producer and exporter of coconut worldwide (PSA 2019, Lapina and Andal 2017).

Generally, the coconut production had been stagnant from 2000 to 2017 (Fig. 1). There had been no significant increase in the production’s growth rate. The production has started to slow down in 2010 and 2013 mainly due to the infestation of the coconut scale insects and the occurrence of major typhoons, which destroyed huge number of coconut trees. Evidently, the yield has declined significantly since 2010. On the other hand, the area planted had generally increased from 2000 to 2017, which also caused the production growth in the recent years. The area planted accounted for almost 26% of the total agricultural land in 2015 that covers 68 provinces in the Philippines (Fig. 2) (PSA 2019, PCA 2019, Lapina and Andal 2017).

In terms of trade, the country continues to export huge amount of coconut products, about 70% of the country’s total coconut production. Among the coconut products exported include coconut oil (CNO), desiccated coconut (DCN), copra meal, and oleo chemicals (Ani and Aquino 2016). In 2017, the total export amounted to US $ 1, 519,639 (in thousands) with Netherlands and US as the top importing countries (Fig. 3) (Trademap 2019).

Despite the continued boom of exports, there has been no significant improvement in the coconut industry. In fact, the industry is still considered an “orphan” in the country’s agriculture due to poor investments. Also, high poverty incidence still prevails among millions of Filipino coconut farmers (Ani and Aquino 2016).

Among the identified problems in the industry are the unorganized supply chain, vulnerability of coconut to world price fluctuations, low farm productivity, which roots from infestations of cocolisap, the aging of current crop of coconut trees and poor nutrition, inadequate infrastructure support and poor farm to market roads, low allocation on research and development (R&D), and presence of corruption and bureaucracy. Another is the controversies surrounding the coconut levy fund (Ani and Aquino 2016, Lapina and Andal 2017).

This paper provides an overview of the status of the Philippine coconut industry, the policies that governed the coco levy fund and some strategic directions for its development. The first section provides the current situation of the coconut productivity. The second section provides a theoretical construct on the economic implications of levies and taxes while the third section discusses the coco levy policies and the current status of the coco levy proposed utilization policies. The last section presents some key strategic areas for the development of the coconut industry.

THE INEFFICIENCY OF TAXATION: A THEORETICAL CONSTRUCT

The economics of taxation

This section provides a theoretical construct on the implication of tax or levy policies on economic welfare. The important role of the government in providing foundation for the environment where tax or levy policies operate is also highlighted. It serves as basis in the analysis of how the coconut levy in the Philippines was established and how governance and administration directed the fate of this landmark tax or levy policy in the country.

Tax or levy system is primarily established to provide revenue for the government to finance essential expenditures on goods and services (Myles, 2009). For developing countries like the Philippines, tax provides the means to boost public expenditures on productivity-enhancing services such as infrastructure, research and development, public education and health care. However, while taxation and the related policies on it are viewed important in developing an economy, a central concern on public finance is the inefficiency due to distortions created by taxation or levies imposed.

The effects of taxation in an economy can be viewed through its impacts on economic welfare. Economic theory posits that economic welfare is the total benefit available to society provided by various economic transaction and situation (Economic Online, 2014). Economic welfare can be evaluated through consumer surplus and producer surplus. Consumer surplus is defined as the difference between the amount that the consumers are willing and able to pay for a good or service (as indicated by the demand curve) and the total amount they actually pay (as indicated by the market price). Producer surplus, on the other hand, captures the difference between the amount that the producer is willing to supply for a good or service (as indicated by the supply curve) and the actual amount received when he makes trade (as indicated by the market price).

Figure 4 shows the effect of taxation on economic welfare. Graphically, prior to the imposition of tax or any levy on a commodity or good, economic welfare is represented by area ABCDEF. This also denotes the total amount of the consumer surplus (Area ABC) and producer surplus (Area DEF). At this point, the level of economic welfare is determined by market forces. The quantity demanded and produced as well as the price paid and received are at equilibrium level of Q* and P*, respectively.

On the other hand, given the imposition of tax or levy, government policy intervention is injected in the scenario. Tax or levy imposed a two-pronged effect on prices of the commodity. Tax increases the price of commodity or good paid by the consumers (Pc) while it reduces the amount received by the producers (Ps). At the same time because of tax, quantity produced and demanded is reduced from Q* to QT. With the new level of prices and quantity of goods due to the additional cost from tax or levy, the consumer surplus and producer surplus are reduced to areas A and F, respectively. Portion of the reduction in the consumer and producer surpluses is transformed into tax revenues remitted to the government (Area BD). Tax revenues, represented by area BD, is considered part of the total economic welfare since the government use them to fund national programs and projects. However, the reduction in consumer and producer surpluses due to the imposition of taxes or levies is not entirely transmitted to the government in the form of tax or levy revenues. The total economic welfare is reduced by area CE which represents the deadweight loss or excess burden attributable to the inefficiency accompanying market distortions of taxation.

Levies, rents and corruption

Levies, enacted through policies and regulations, are temporary taxes collected and state-enforced non-voluntary contributions which are purposively allocated to a sector. Unlike income taxes, levies are not reverted to the government to form part of the national funds for redistribution to the entire economy (Taylor, 2012 and Ramos, 2013). In this sense, levies are considered funds that is sectoral in nature. Hence, in the case of coconut levies, property rights over the use of funds belong to the coconut industry.

In most cases and as practice in other countries, the utilization and management of levy funds are usually lodged to associations of the concerned sector. This institutional framework in managing levies, as claimed by Khan (2000), provides private agents access to income streams which they would have not had without the policy interventions. In this context, Khan defined levies as state-mediated rents that resulted from a politically organized transfers which converted public property into private ones. As such, state policies and regulations on levies give opportunities for possible rent-seeking which refers to all activities that seek to create, maintain and change rights and institutions to which rents are based. This effectively assigns the rights to the economic rent to a privileged portion of society. At worst, the privileged few given access to the funds through political assignments had little or nothing to do with the concerned sector, hence, property rights are attenuated. In the Philippines, Ramos (2013) pointed out that the coconut levy administered during the Marcos regime is considered a rent-allocation under a monopolistic corruption structure.

As cited in Ani and Aquino (2016), innate inefficiencies of coco levy imposition caused welfare loss. It has become disincentive to farmers since it adversely affected farm profitability (Aquino, 1993). Majority of the taxes on coconut products collected at any point along the marketing chain were borne by the farmers (Habito and Inatal, 1988). The farmers’ loss in income because of the coconut levy imposition was further aggravated by poor governance and administration of the levy returns.

The levy funds have become a tool for corruption. Corrupt practices in managing and implementing the coco levy returns allowed for welfare losses. As Taylor (2012) emphasized in his report, tax or levy can be an abused or abusive means resulting to ignoble ends. It has always been associated with extortion and misuse. The situation is a classic “double whammy” case where farmers were grabbed with benefits from the inefficiencies caused by levies or taxation policies and from the corruption that stolen the welfare due to the programs and projects created under the coconut levy funds.

COCONUT LEVY FUND

One of the most controversial issues, which has considerably affected the coconut industry, is the enactment of the coconut levy fund under the administration of former president Ferdinand Marcos in 1971. Coconut levy is the state-enforced tax imposed on coconut products and collected from the coconut farmers to be used supposedly for the development of the coconut industry and improvement of the lives of coconut farmers. However, until now, coconut farmers have not yet fully realized the benefits from this fund, and there were no evidences that the funds were actually utilized for the sector. In fact, only about 33% of the Php 9.68 billion or US$185.37 million (exchange rate at Php 52.22 per US$ 1.00), estimated total amount of levy in 1997, was used to support programs directly benefitting farmers (Ani and Aquino 2016).

The coconut levy fund was imposed through series of major funds, which were enacted between the 1970s and early 1980s, namely Coconut Investment Fund (CIF) levy, Coconut Consumer Stabilization Fund (CCSF), Coconut Industry Development Fund (CIDF), and Coconut Industry Stabilization Fund (CISF). CIF, established in 1971 through Republic Act 6260, was created supposedly to provide medium- and long-term financing for capital investments. CCSF, on the other hand, was used to provide subsidy for coconut-based products, fund investments in processing plants, R&D, and extension services. CIDF was created to establish, operate and manage the hybrid coconut seed farm for the national replanting program, while CISF was designed to support socio-economic and development programs (Ani and Aquino 2016).

After the Marcos regime, recovering the assets and properties, acquired through the coconut levy fund, has been a priority agenda of the next administrations. Through the Presidential Commission on Good Governance, significant amount of assets was recovered, currently amounting to around Php 100 billion or US$ 1.91 billion (PNA 2018). But, still, this recovered fund remains to be unutilized.

Both Senate and House have crafted several bills with regard to developing mechanisms on how to utilize and allocate the said fund. Yet, after almost four decades, there had been no actual law enacted to distribute and return this fund to coconut farmers.

Meanwhile, coconut farmers had high hopes that with the current administration under Pres. Rodrigo Duterte in which he signed a manifesto and committed to return the coco levy fund to farmers (Elemia 2019), things would be better. However, just recently, the President had vetoed the bill creating the coco levy trust fund.

Coconut levy twin bill

The consolidated bill Senate Bill No. 1233/ House Bill No. 5745, titled “An Act Creating the Coconut Farmers and Industry Trust Fund, Providing for its Management and Utilization, and for Other Purposes” and also known as the “Coconut Farmers and Industry Development Trust Fund Act”, aims to consolidate all assets and benefits emanating from the coconut levy, and create a Trust Fund for the benefit of coconut farmers and farm workers. It has the following key provisions (House of Representatives 2018):

A twin bill SB No. 1976/HB No. 8552, titled “An Act to Further Strengthen the Philippine Coconut Authority (PCA), Amending Presidential Decree No. 1468, Otherwise known as the ‘Revised Coconut Industry Code’, as Amended, and Appropriating Funds Therefore”, was also crafted in relation to the establishment of the coconut levy trust fund. This aims to ensure the effective utilization of the coconut levy funds, which will be managed by the Philippine Coconut Authority. It has the following key provisions (Committee on Agriculture and Food 2019):

The bills creating the coconut trust fund, and strengthening the PCA were presented by Congress on January 17 and January 10, respectively, for the President’s approval.

In this regard, PCAARRD has expressed support to both of the bills, highlighting the role and possible contribution of DOST in developing a clear and implementable roadmap for the coconut industry. Specifically, DOST would contribute in identifying and setting directions for R&D initiatives and science-based solutions to address problems in the industry.

Veto of coconut bills

In February 2019, Pres. Duterte vetoed the consolidated bill creating the Coconut Farmers and Industry Trust Fund, as well as the bill strengthening the PCA.

The reconstitution of PCA was vetoed, prior to the creation of the trust fund, by the President for he thinks that the proposed bill allows for corruption of the coco levy fund, and bypass the role of the executive branch. Listed below are the specific reasons, as cited by Ranada (2019) and Elemia (2019):

With the return of the unsigned bill to Congress, stakeholders were afraid that the President will also veto its twin bill. This is because the reconstituted PCA will be the one in-charge of the coconut levy trust fund, as proposed by the Coconut Farmers and Industry Development Trust Fund Act.

As expected, the coconut trust fund act was vetoed week after rejecting the PCA reconstitution. The Palace cited three main reasons, as stated in their official statement (Malacañang Palace 2019):

KEY STRATEGIC AREAS IN DEVELOPING THE COCONUT INDUSTRY

Huge opportunities, not just for the coconut farmers but also for the coconut industry, were anticipated with the supposed enactment of the coconut trust fund act. In fact, the act has been seen as a “timely and necessary” measure in reviving the coconut industry given that the price of copra is continuously decreasing, and the country is experiencing decline in production. The coconut levy bill could have been the answer to the said problems especially that it will provide funds for developmental programs, improvement of coconut farmer’s income, and improvement of the farms’ productivity, among others.

Given the current state of the industry and the veto of the coconut levy bills, the question now is “how to position the coconut industry” and/or “what could be the entry points for development of the industry”. Another thing to ponder is that, if ever the coconut levy bill will be enacted in the near future, what could be the optimal way to position the industry.

A primary concern is the positioning of the coconut oil industry. Coconut oil is the top export product from coconut, which comprises almost 80% of the total coconut exports and, hence, generates the highest export earnings (PSA 2019). This oil, which is extracted from mature nuts through wet or dry (from dried nuts) process, can be processed into cooking oil, food ingredients, medicines, soaps, and detergents, among others. It is also known to have multiple health benefits (PEF 2016).

At present, the industry is experiencing decline in the supply of coconut oil mainly due to the significant drop in the yield and ‘stagnant to negative’ growth in the coconut production. In contrast, the demand for coconut oil has been growing substantially in the recent years. This can be attributed to consumers opting for healthier options in food and other products (Broaddus 2016).

Accompanying the increase in demand is the tight competition, not just with other coconut-producing and exporting countries, but also with other alternative crops such as corn, and soybean, among others (PEF 2016). In fact, there had been campaigns on the alleged negative impact of too much consumption of coconut oil. This had surely threatened the coconut industry particularly the livelihood of millions of coconut farmers and entrepreneurs. However, the campaign has been debunked by several studies saying that the blame should be put on the soybean oil (Dar 2017).

Another issue is the purported competition between coconut and palm oil. The Philippines is known to be a net importer of palm oil with almost 750 thousands mt of imports and 25 thousands mt of exports in 2015 (Fig. 5). Palm oil supplies 80% of the country’s vegetable oil. Currently, there is only 90,000 ha land area allotted for the production of oil palm trees, which only meets 10% of the domestic requirement (Agriculture 2018). This has been the main rationale for eyeing palm oil expansion in the country. However, many believe that this will threaten and might kill the coconut industry. Some even speculate that PCA would use the coco levy fund for the development of the palm oil industry. A research claimed that “oil palm is a big brother” such that it complements the coconut industry. It argued that the expansion of oil palm would aid in controlling coconut insect infestation, particularly by the coconut leaf beetle (CLB), and promote higher yield through adopting oil palm model in the coconut production (Pamplona 2017).

PCAARRD has also expressed support, in 2017, to develop both coconut and oil palm industry especially that the country is blessed with climatic condition highly suitable for both crops. Since coconut is very compatible with the country’s traditional farming system and grows in almost any kind of soil, it can be grown with other crops, particularly oil palm, in an intercrop system. The intercrop/s will provide additional sources of income for the farm households.

The most important advantage of oil palm over coconut is that it produces more oil per hectare (two to five times depending on the productivity of coconut). However, successful production and processing of oil palm is associated with exacting logistical requirements. This means that oil palm should be in plantation type production, where the production sector is highly integrated with processing.

Still, there is no need to choose between coconut and oil palm because they can co-exist profitably. As a strategic direction for the country, the continued development of coconut should be pursued while also encouraging the development of oil palm in areas appropriate for the crop. However, instead of coco levy, the government should allocate a separate fund from the annual regular government appropriation for the expansion of the palm oil industry. Still, the coco levy fund must be utilized to conduct R&D, and employ strategies, programs and policies for the benefit of the coconut industry.

On the other hand, while it is no doubt that coconut oil contributes significant amount of foreign earnings, the country must not remain complacent. There are speculations on the deteriorating position of coconut oil in the global vegetable oils market (Javier 2018). Hence, there is a need to keep up, and explore ways to either remain or be more competitive. It is also high time to diversify into new markets and/or other high-value coconut products.

A possible entry point is to boost the domestic demand for coconut oil through the Biofuels Act. The country could take advantage of the Biofuels Act, which proposes to increase the coconut biodiesel blend in automotive diesel from the current 2% to 5%, if this will be enacted soon. Aside from promoting cleaner fuel and emission, the increase in the coconut content of diesel would create new demand for the coconut oil; hence, could provide additional revenue for the coconut farmers. However, the Biofuels Act is still subject to review, and yet to be passed as a law (Simeon 2018).

Other than oil, the coconut industry remains to offer lot of opportunities that could be entry points for its development. The industry may focus its investments in producing and/or developing other coconut products such as coconut water, coconut sugar, virgin coconut oil, coconut flour, and coco coir. Indeed, coconut water, which is rich in minerals such as potassium, calcium, and magnesium, is gaining popularity as a drink in tropical countries. Coconut sugar and coconut flour are also widely used as healthier alternatives (Orbis 2018, Javier 2018, PEF 2016). Diversifying into this kind of products will generate more employment among small and medium enterprises, and will promote inclusive growth in the coconut industry (Javier 2018).

CONCLUSION

The coconut industry is an important pillar of Philippine agriculture. Its development would mean significant welfare improvement on the lives of millions of Filipino people. Many efforts have been exerted to finally claim back, for the benefits of the coconut farmers and their families, the billion worth coco levy funds. In positioning, and striving to reach the full potential of the coconut industry, the country should be persistent in pushing for the disbursement of the coco levy. The release of this funds, however, should be accompanied by a clear and implementable roadmap for the sector as well as transparent policies. While waiting for this mechanism to materialize, other issues in the industry should not be set aside and should be acted upon to achieve inclusive development.

REFERENCES

Agriculture (2018). “The facts: Addressing the campaign to stop the planting of oil palm trees in the Philippines.” Retrived from: https://www.pressreader.com/philippines/agriculture-9ggr/20180101/282467119278597.

Ani, PA. and A. Aquino (2016). “The Long Climb towards Achieving the Promises of the Tree of Life: A review of the Philippine Coconut Levy Fund Policies.” FFTC Agricultural Policy Articles 2016-01-28. Retrieved from: http://ap.fftc.agnet.org/ap_db.php?id=577&print=1.

Aquino, A.P. 1993. The Effects of Tax Policy on the Level and Distribution of Benefits from Technological Change in the Philippine Coconut Industry. Master Thesis on Agricultural Economics, University of the Philippines Los Baños.

Broaddus, H. (2016). “Supply and Demand in the Coconut Oil Market (Market Update). CentraFoods.” Retrieved from: http://www.centrafoods.com/blog/supply-and-demand-in-the-coconut-oil-market-market-update.

Elemia, C (2019). “'Na-Duterte kami:' Why farmers feel betrayed by coco levy vetoes.” Rappler. Retrieved from: https://www.rappler.com/newsbreak/in-depth/223809-farmers-reaction-coco-levy-vetoes.

Committee on Agriculture and Food (2019). House Bill 5745 Fact Sheet.

Dar, W. (2017). “State of the PH coconut industry and what must be done.” The Manila Times. Retrieved from: https://www.manilatimes.net/state-ph-coconut-industry-must-done/346624/.

House of Representative (2018). “House ratifies coco levy twin bills.” Retrieved from: http://www.congress.gov.ph/press/details.php?pressid=11090.

Javier, E. (2018). “The Philippine coconut industry in the long term.” Manila Bulletin Business. Retrieved from: https://business.mb.com.ph/2018/08/25/the-philippine-coconut-industry-in-the-long-term-2/.

Lapina, G. and E.G. Andal (2017). ASEAN Economic Community: Opportunities and Challengers for the Crops Sector.

Malacañang Palace (2019). Official statement re. veto of Senate Bill No. 1233/ House Bill No. 5745.

Myles, G. D. (2009), “Economic Growth and the Role of Taxation-Theory”, OECD Economics Department Working Papers, No. 713, OECD Publishing. http://dx.doi.org/10.1787/222800633678

Orbis (2018). Global Coconut Water Market and Coconut Oil Market 2018 By Demand, Consumption, Production, Top Regions, Key Manufacturers, Growth & Forecast Till 2023. Retrieved from: https://www.reuters.com/brandfeatures/venture-capital/article?id=38929.

Ramos, Charmaine G. 2013. The Power and the Peril: Producers Associations Seeking Rents in the Philippines and Colombia in the Twentieth Century. A Dissertation submitted to the Department of International Development of the London School of Economics, London, United Kingdom.

Pamplona, P (2017). “Oil Palm: Coconut’s “Big Brother”.” Agriculture Monthly. Retrieved from: https://agriculture.com.ph/2018/01/23/oil-palm-coconuts-big-brother/.

Peace and Equity Foundation (PEF) (2016). A Primer on PEF’s Priority Commodities: Industry Study on Coconut.

Philippine Coconut Authority (PCA). Coconut Statistics. Retrieved from: http://www.pca.da.gov.ph/index.php/2015-10-26-03-15-57/2015-10-26-03-22-41.

Philippine News Agency (PNA) (2018). “‘Historic' coco levy fund measure to benefit farmers: Nograles.” Retrieved from: http://www.pna.gov.ph/articles/1054883.

Philippine Statistics Authority (PSA) (2019). Data on Coconut Production, Yield, and Area Planted. Retrieved from http://countrystat.psa.gov.ph.

Ranada, P. (2019). “Duterte vetoes bill reconstituting Philippine Coconut Authority.” Rappler. Retrieved from: https://www.rappler.com/nation/223056-duterte-vetoes-bill-reconstituting-philippine-coconut-authority.

Taylor, Madeline. 2012. Is it a levy, or is it a tax, or both? Revenue Law Journal, 22 (1). Retrieved January 31, 2015, from http://epublications.bond.edu.au/rlj/vol22/iss1/7

Trademap (2019). List of importing markets for coconut exported by Philippines. Retrieved from: https://www.trademap.org/Country_SelProductCountry_TS_Graph.aspx? nvpm=1%7c608%7c%7c%7c%7c1513%7c%7c%7c4%7c1%7c1%7c2%7c2%7c1%7c2%7c1%7c1

Date submitted: Apr. 24, 2019

Reviewed, edited and uploaded: June. 13, 2019