ABSTRACT

The important contribution of fertilizers in achieving agricultural productivity to ensure food security is highlighted in this paper. State of the two sub-sectors of the Philippine fertilizer industry, the inorganic fertilizer and bio-fertilizer, was discussed. The inorganic fertilizer industry is private sector-led and operates in a free market while the bio-fertilizer industry is influenced by government programs and initiatives. Landmark policies in the country were enacted that affected the fertilizer industry. These policies included the creation of policy-making bodies or government agencies supporting the operation of the fertilizer industry in the country; policies gearing toward environmental sustainability, hence, supporting the bio-fertilizer sub-industry and policies advocating for quality standards. The Philippines has provided a policy environment that supports the twin goal of improving productivity and protecting the environment from degradation.

Key words: inorganic fertilizers, bio-fertilizers, organic agriculture, fertilizer policies

INTRODUCTION

Prior to 1972, the fertilizer industry in the Philippines was free from control. Fertilizer importation, distribution and marketing were in the hands of the private sector while government restrictions, tariffs and subsidies were lacking. However, with the increasing recognition of fertilizer as one of the important inputs in improving agricultural productivity and ensuring food security for the Filipinos, the country realized the need for policies governing the development of the fertilizer industry.

The growing food production to meet the ever increasing demand for food, especially for grains and cereals, has driven the global growth of the fertilizer industry. World demand for total fertilizer nutrients, nitrogen (N), phosphorus (P) and potassium (K) is estimated to reach an annual growth rate of 1.8% from 2014 to 2018. Moreover, the demand for N, P, K is projected to grow annually by 1.4%, 2.2% and 2.6%, respectively. Forecasts over the next five years also showed increase in global capacity of fertilizer products, intermediaries and raw materials (FAO, 2015).

In the case of the Philippines, its goal of achieving self-sufficiency especially in two of the major staples in the country, rice and corn, was considered one of the major factors driving the policy environment for fertilizers. On average, rice and corn used about 38% and 21% of the total fertilizer supply in the country, respectively (How, 2015). Meanwhile, extent and rate of fertilizer utilization, which were mainly nitrogenous fertilizers, ranged from 93% to 94%. Given this very crucial role of fertilizers, many of the agricultural programs in the country included the provision and usage of fertilizers as one of the major program components.

In 1973, regulation and control of the fertilizer industry was realized in the country through the establishment of a regulatory board, the Fertilizer Industry Authority (FIA). The government completely changed its policy from non-intervention to rigid and all-encompassing control over fertilizer prices, mark up, distribution channels, promotion, importation, exportation, and production (Alcala, 2012). FIA also provides for the outright tax exemption of the importation of all kinds of fertilizers. By 1986, in line with trade liberalization, government's control was relegated and limited to issuance of fertilizer handler licenses, compilation of national statics (statistics?), and monitoring and assurance of good quality fertilizers.

This paper presents the state of the fertilizer industry in the Philippines and its sub-sectors, the inorganic and bio-fertilizers industries. It highlights the significant policies that govern fertilizer production, utilization, and trade as well as their implications in achieving food sufficiency and/or security and environmental sustainability.

PHILIPPINE FERTILIZER INDUSTRY

The fertilizer industry can be subdivided into two sub-industries, inorganic and bio-fertilizers. The inorganic fertilizer industry operates in a free market while the bio-fertilizer industry is generally driven by government policies. A discussion on supply, demand and prices, specifically for inorganic fertilizers, is also presented in this section.

Inorganic sub-industry

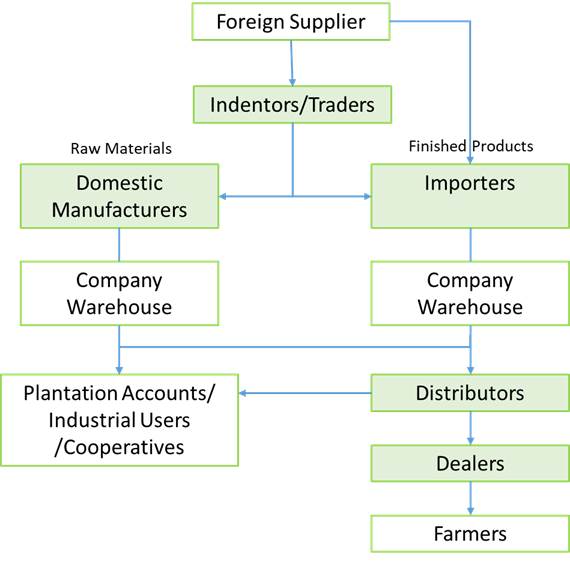

In the Philippines, the marketing, distribution, and prices of inorganic fertilizers are largely dictated by the private sector. Marketing, as shown in Fig. 1 is done in four main levels: (1) indentors/traders; (2) importers/manufacturers; (3) distributors; and (4) dealers (How, 2015). Fertilizers enter the country in the form of raw materials and finished products or the ready to use fertilizers. Both are distributed through the indentors or traders, the finished products though can be directly provided to importers also. End users such as the plantation, industrial users and cooperatives have various sources or suppliers of fertilizer which can be from domestic manufacturers, importers/producers and distributors. On the other hand, fertilizer suppliers of farmers are limited to local dealers or cooperatives. Key players for the domestic production of fertilizers involve five major fertilizer producers manufacturing mainly nitrogen (N) and nitrogen-phosphorus-potassium (NPK) grades, namely: (1) Philphos; (2) AFC Fertilizer & Chemical Inc. (AFC); (3) International Chemical Corp. (INCHEM); (4) Farmix Fertilizer Corp.; and (5) Soiltech Agricultural Products Corp. (Chupungco, 2003 as cited by Aquino et al., 2010).

Fig. 1. Distribution channels of fertilizer in the Philippines

Source: Food and Agriculture Organization, Fertilizer and Pesticide Authority as cited by How, 2015

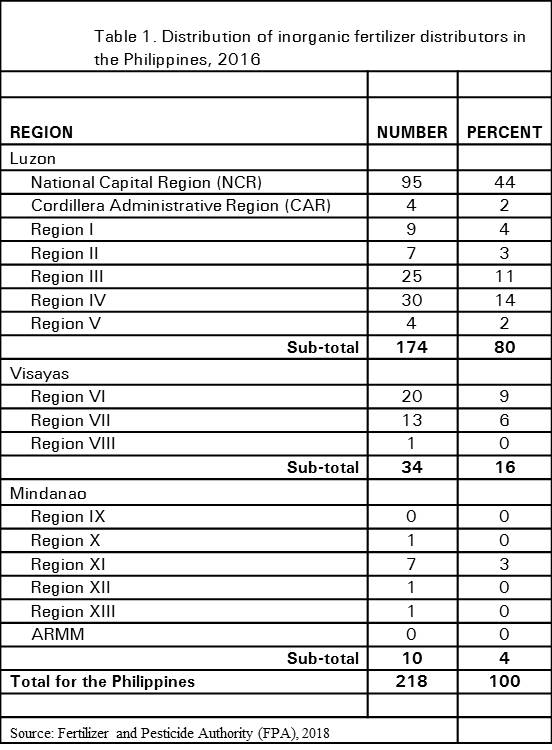

In 2016, there were 218 registered fertilizer distributors in the Philippines (Table 1). Majority (80%) of these distributors were located in Luzon, of which 44% were located in the National Capital Region (NCR). The other distributors were located in the Visayas (16%), while very small number of distributors can be found in Mindanao (5%). On the other hand, the dealers, who are directly connected to the farmers were widely distributed all over the country. There were 4,755 registered fertilizer dealers in the country in 2016, majority (86%) of which were selling both fertilizers and pesticides while 14% were solely dealing fertilizers only (FPA, 2018).

Supply of inorganic fertilizers

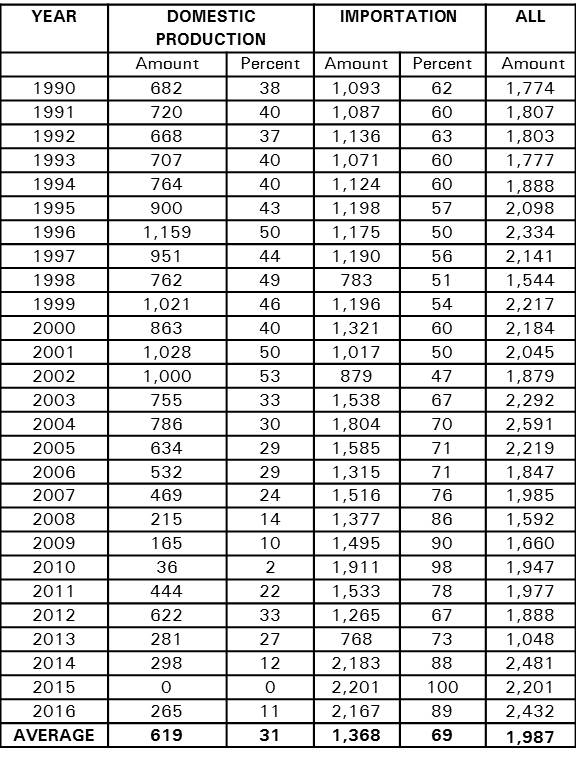

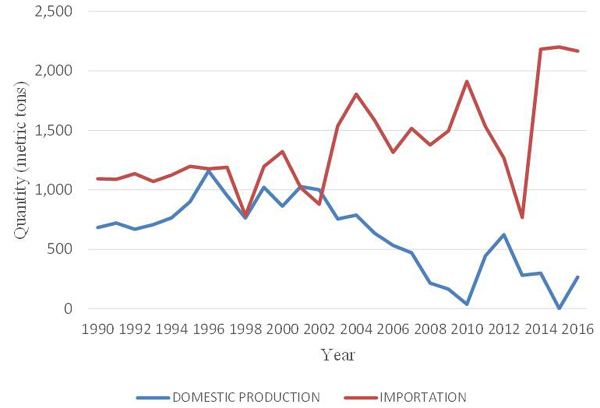

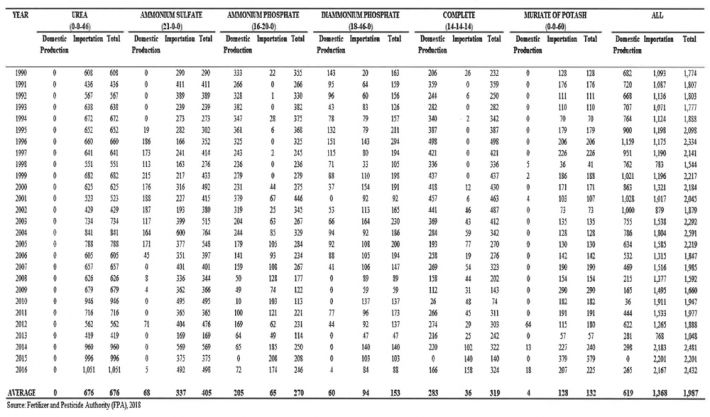

There are six major inorganic fertilizer grades available in the market, namely: Urea (46-0-0); Ammonium Sulfate (21-0-0); Ammonium Phosphate (16-20-0); Diammonium Phosphate (18-46-0); Complete (14-14-14), and Muriate of Potash (0-0-60). Inorganic fertilizers were sourced from importation (69%) and domestic production (31%) (Table 2). In general, total supply increased at annual growth rate of 4.68%. Fluctuations were observed in both domestic supply and imports (Fig. 2). However, domestic supply showed dramatic reduction of 25% annual average from 2002 to 2010. The lowest domestically produced inorganic fertilizers was recorded in 2010 at 36,000 metric tons only and zero production in 2015.

Table 2. Total supply of inorganic fertilizers in the Philippines, in ‘000 metric tons, by source, 1990-2016

Source: Fertilizer and Pesticide Authority (FPA), 2018

Fig. 2. Supply of inorganic fertilizers, by source, 1990-2016

The supply of the six major fertilizers from 1990-2016, as shown in Table 3, indicated nitrogenous fertilizers such as Urea and Ammonium Sulfate as the most supplied fertilizers in the country. Urea ranked first, contributing 34% of the total supply while Ammonium Sulfate ranked second providing 20% of the total supply.

Table 3. Supply of the six major inorganic fertilizers in the Philippines, in ‘000 metric tons, 1990-2016

Source: Fertilizer and Pesticide Authority (FPA), 2018

Complete was the highest domestically produced inorganic fertilizer in the country contributing 44% of the total local supply. Ammonium phosphate ranked second with an average domestic production of 205,000 metric tons while muriate of potash ranked last with only less than 1% contribution to the total domestically produced supply of inorganic fertilizers.

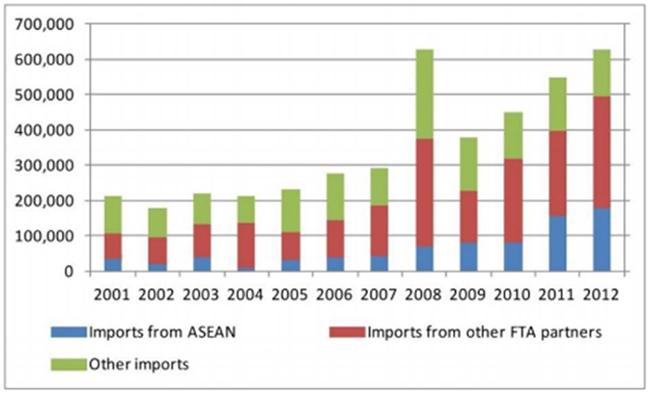

In terms of imports, the highest importation is recorded for urea contributing 49% of the total imported inorganic fertilizers. Moreover, it is the only fertilizer that is not domestically produced and is mainly imported, implying vulnerability of farmers to changes in world prices. Urea is also the primary nitrogenous fertilizer used by farmers. How 2015, also emphasized that importation of fertilizer is generally increasing which peaked in 2008, majority of which were the nitrogenous type. These fertilizers are mainly sourced from ASEAN and other countries where Philippines have trade agreements (Free Trade Agreement (FTA)) (Fig. 3). It should be noted that fertilizer importation was generally liberalized in accordance to trade agreements that promote reduction/elimination of subsidies and products to flow freely. The implementation of the Agriculture and Fisheries Modernization Act (AFMA) provided for imported fertilizers that obtained certification from the Department of Agriculture (DA) be exempted from tariff duties from 2004-2015 (Aquino et al., 2010).

Fig. 3. Distribution of imported inorganic fertilizers, by source, 2012-2014

Source: How, 2015

Disposition of inorganic fertilizers

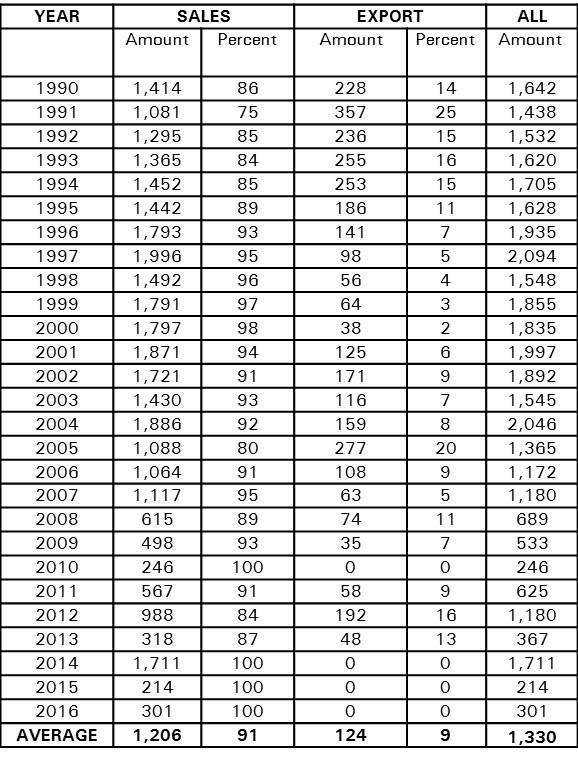

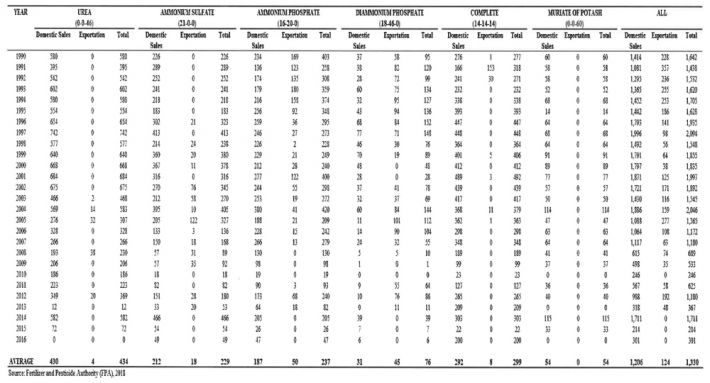

In terms of fertilizer disposition from 1990-2016, the Philippines recorded an average total local sales of 1,206,000 metric tons (91%) while exports comprised 124,000 metric tons (9%) (Table 4). Highest domestic sales were recorded in 1997 at 1,996,000 metric tons while minimal exports were observed with highest amount recorded in 1991 at only 357,000 metric tons. In 2014-2016, the country has no exportation of the six major fertilizers.

Table 4. Disposition of inorganic fertilizers in the Philippines, in ‘000 metric tons, 1990-2016

Source: Fertilizer and Pesticide Authority (FPA), 2018

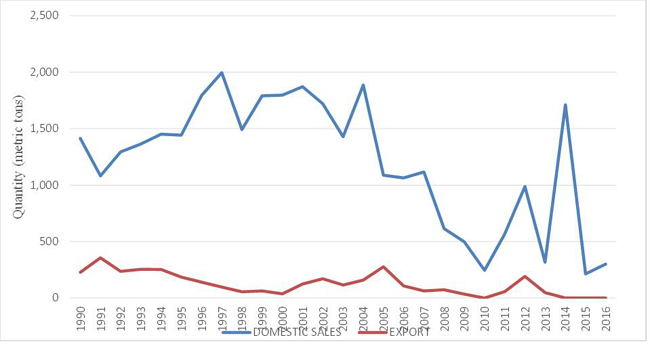

Similar to supply, both local sales and exportation experienced fluctuations (Fig. 4). Dramatic reduction in sales, 16% annual average, was also observed for the period 2002-2010. Peaks of domestic sale were observed in 1996, 2012 and 2014 while deepest fall was recorded in 2015 with only 214,000 metric tons locally used fertilizers.

Fig. 4. Disposition of inorganic fertilizers in the Philippines, 1990-2016

Among the six major fertilizers, as shown in Table 5, the highest amount used locally is Urea at 432,000 metric tons (32%). Complete fertilizer ranked second with an average local sales of 292,000 metric tons (16%) while Ammonium Sulfate closely followed contributing 14% of the total local sales or 212,000 metric tons, on average. Considering the limited supply, muriate of potash expectedly ranked last among the fertilizers locally used with only 54,000 metric tons (4%).

Table 5. Disposition of the six major inorganic fertilizers in the Philippines, in ‘000 metric ton, 1990-2016.

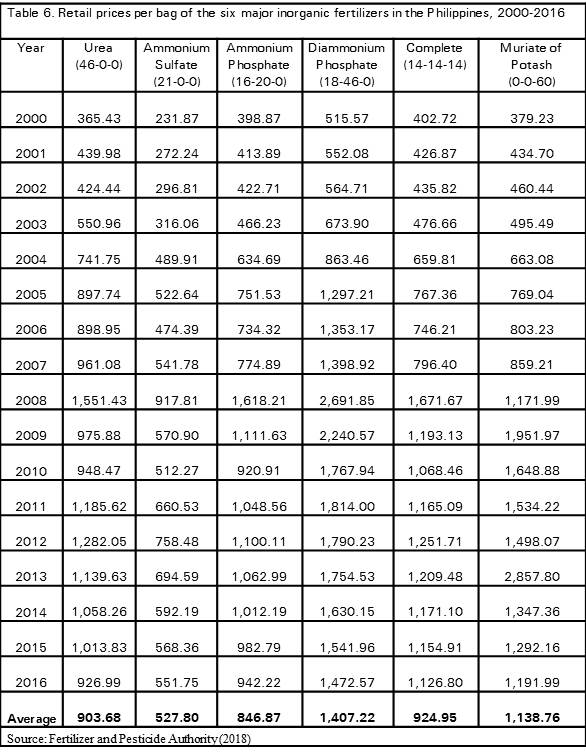

Price

Retail prices of the six major fertilizer grades generally increased (Table 6). Significant surge in fertilizer prices was observed in 2008, almost all fertilizers doubled their prices. It should be noted that oil prices also spike during this period. After 2008 price hike, prices of fertilizers generally decreased except for Muriate of Potash which reached its highest price at P2,858/bag in 2013. Trade liberalization, which allowed for free movement and decrease in tariffs of products, could have contributed to the decrease in prices of fertilizers.

Bio-fertilizer sub-industry

Bio-fertilizers is gaining recognition in the Philippine market. With the environmental threat caused by the extensive and inappropriate use of inorganic fertilizer which resulted to land degradation and significant loss of soil fertility (Tirado and Bedoya, 2008) policy makers have been pushing for balanced fertilization[1] and adoption of organic farming. The use of bio-fertilizers was among the key component of organic agriculture and was promoted through various government policies and programs. Incidentally, these initiatives were supported by the private sector which started with the organic movement by some non-government organizations (NGOs) in the 1980s. This was followed by the movement for sustainable development and supported through the Organic Producers and Trade Association (OPTA) formed in 1995. OPTA became the frontrunner in advocating for organic agriculture including the use of bio-fertilizers.

As of 2006, there were 59 FPA-registered organic fertilizers and 18-registered plant growth regulator brands available in the market. Domestically, 76% of the organic fertilizers and 50% of the plant growth regulator brands were produced. Organic fertilizers comprised 86% of the bio-fertilizer industry which were composed of 54 manufacturers, 13 importers, 67 distributors and 2 exporters (Aquino et al., 2010).

Relative to inorganic fertilizer sub-industry, bio-fertilizer sub-industry is not well developed. This can be closely associated with the still formative stage of organic farming in the Philippines. It should be noted that the production of organic products is still marginal. They are planted in less than one percent of the total agricultural land in the country (NOAP 2012-2016). Also, marketing and distribution of bio-fertilizers is simple. The manufacturers or producers, in most cases, are also the traders who distribute organic fertilizers directly to customers such as other traders/distributors and farmers. To increase sales, other incentives given to users include trainings, seminars, discounts and free or no cost delivery of organic fertilizers.

Government programs serve as key driver to move the initiatives for the use of bio-fertilizers. As indicated in the recommendations of Aquino et al. (2010), for the bio-fertilizer industry to remain competitive, the government could focus on these initiatives: (1) market development to address issues on seasonality of demand; (2) establishment of royalty policy to support researchers and investors; (3) support for R&D investment; and (4) other necessary support services.

PHILIPPINE FERTILIZER POLICIES AND PROGRAMS

Initially, fertilizer industry in the Philippines was marked by a laissez faire policy. By 1973, fertilizer has been recognized as one of the major components in improving farm productivity. This has led to the promulgation of agriculture and fertilizer laws which in the end have been translated into various government programs and projects.

Landmark legislations affecting the fertilizer industry were enacted which include the Creation of the Fertilizer and Pesticide Authority (Presidential Decree (PD) 1144), Agriculture and Fisheries Modernization Act (Republic Act (RA) 8435), Organic Agriculture Act of 2010 (RA 10068), and Ecological Solid Waste Management Act (RA 9003). The Bureau of Agriculture and Fisheries Standards (BAFS) also developed the national standard for organic fertilizers.

Creation of the regulatory board

Through the promulgation of PD 135, the Fertilizer Industry Authority (FIA) was created on February 22, 1973. FIA was mandated to control and regulate the prices, mark-ups, distribution channels, promotion, storage, production, import and export of fertilizer. It also had the power to negotiate and enter into contract for all imports and experts of fertilizer and fertilizer inputs. In addition, importation of all kinds of fertilizers made by FIA was exempted from custom duties, compensating and sales taxes and all other taxes.

By 1977, PD 1144 merged the fertilizer and pesticide industries and placed them under the jurisdiction of a single government agency, the Fertilizer and Pesticide Authority (FPA). PD 1144 abolished FIA but adopted and retained the board power provided under PD 135 on fertilizer regulation and control.

In line with the liberalization policy of the government, the Philippine fertilizer industry has been deregulated since 1986. The government’s role is now confined to issuance of fertilizer handler licenses, compilation of national statistics, and monitoring and assurance of good quality fertilizers (Alcala, 2012).

Fertilizer as a strategic component in modernizing agriculture

On July 28, 1997, RA 8435 also known as the Agriculture and Fisheries Modernization Act (AFMA) of 1997 was promulgated. The law aims to modernize the agriculture and fisheries sectors by transforming these sectors from a resource-based to a technology-based industry. This is with the end in view of attaining food security, poverty alleviation, social equity, global competitiveness and environmental sustainability.

The law specifically cites provisions that support the optimal use of farm inputs like fertilizers. These could be seen in the credit and financing support, infrastructure support service and trade and fiscal incentives. The Agro-Industry Modernization Credit and Financing Program under the AFMA provide support to the acquisition of fertilizer and other farm inputs like seeds, poultry, livestock, feeds and other similar items as well as agriculture and fisheries production inputs including processing of fisheries and agri-based products and farm inputs.

Infrastructure support to ensure that agriculture and fisheries production inputs (including fertilizers) as well as information and technology were readily available to farmers, fisherfolks, cooperatives and entrepreneurs. This is part of the special concerns in formulating the Agriculture and Fisheries Modernization Plan.

Promotion and commercialization of organic fertilizer

The approval of the RA 10068, An Act Providing for the Development and Promotion of Organic Agriculture in the Philippines and for Other Purposes also known as the Organic Agriculture Act of 2010 has profound implication on the development of the bio-fertilizer sub-industry. The law promotes, propagate, develop further and implement the practice of organic agriculture in the Philippines that will cumulatively condition and enrich the fertility of the soil, increase farm productivity, reduce pollution and destruction of the environment, prevent the depletion of natural resources, further protect the health of farmers, consumers, and the general public, and save on imported farm inputs. Towards this end, a comprehensive program was developed for the promotion of community-based organic agriculture systems.

Recognition of the use of bio-fertilizers has been accorded both by the private and public sectors. Private initiatives started with the organic movement by some NGOs in the 1980s, followed by sustainable development initiatives of many farmer organizations and other NGOs in the 1990s. The Organic Producers and Trade Association (OPTA) became one of the frontrunners in advocating for organic agriculture which include the use of bio-fertilizers (Aquino, et al., 2010).

An attached office to the Department of Agriculture, the National Organic Agricultural Board was created under RA 10068. Mandated by law, NOAB serves as the policy-making body that provides direction and general guidelines for the implementation of the National Organic Agricultural Program (NOAP). The NOAP developed for 2012-2016 is a collaborative initiative among various stakeholders of the organic industry, the national government agencies/offices, NGOs, civil society and people’s organizations. NOAP serves as guide in the implementation of the organic agriculture as stipulated under the provisions of RA 10068. NOAP 2012-2016 envisions to contribute to the overall welfare and development of the Philippines wherein 5% of the total farm areas adopts and practices organic agriculture. NOAP’s objective of enhancing soil fertility and farm biodiversity may have great impacts on demand and utilization of bio-fertilizers. Further, advancement in the bio-fertilizer industry is foreseen with the implementation of RA 9003 or the Ecological Solid Waste Management Act of 2000 and RA 10068 as well as the establishment of Philippine National Standard for Organic Soil Amendments.

Major issues on organic fertilizer production include irregular production due to non-continuous demand from end users. There is also non-uniformity of product pricing both at the manufacturers’ and traders’ levels. Hence, there is a need for strong promotion and encouragement of the establishment of facilities, equipment and processing plants that would accelerate the production and commercialization of organic fertilizers, pesticides, herbicides and other farm inputs. A facilitative delivery and extension system can also provide an enabling environment for the promotion of the use of organic fertilizers (Aquino et al., 2010).

Composting as a solid waste management approach

The beneficial effects of compost application to the soil and plant productivity cannot be understated. It improves the soil’s physical, chemical and biochemical properties resulting to enhanced nutrient utilization by plants and minimized nutrient leaching (Tejada, et. al., 2006 as cited by Abrigo, 2008). Furthermore, it helps mitigate environmental imbalances brought by the increasing carbon dioxide concentration in the atmospheres.

The Ecological Solid Waste Management Act of 2000 (RA 9003) laid the framework for biodegradable waste to be used for organic fertilizer production. RA 9003 provides for the establishment of materials recovery facility (MRF) for composting activities which is particularly important to meet the provisions of Section 7 of the implementing rules and regulations of RA 9003 which states that at least 25% of all solid waste from waste disposal facilities should be diverted through composting.

Establishment of the Philippine National Standards for Soil Amendments

Originally developed as the Philippine National Standards (PNS) for organic fertilizers (PNS/BAFS 40:2013), the BAFS revised the said PNS to include the results of recent scientific and technological studies both local and international on the specifications of organic fertilizers, compost, soil conditioner, microbial inoculants and organic plant supplements. The PNS was then revised and changed from PNS for Organic Fertilizer to PNS for Organic Soil Amendments. The PNS indicates the specifications of theses soil amendments including the laboratory tests for finished products, labeling of these products (e.g. on bottles or cartons) and the permitted/allowed raw materials in the production of the soil amendments.

CONCLUSION

The fertilizer industry has a very important role in the development of agricultural productivity. It has a great deal of responsibility in meeting the world's increasing demand for food through improvement in food crop productivity. To produce the greatest possible output in ensuring food security, the Philippine government promulgated landmark legislations that created the Fertilizer and Pesticide Authority and incentives that would encourage fertilizer traders to increase their imports and made it easier for domestic manufacturers to import raw materials for locally produced fertilizer as stipulated in the AFMA.

However, excess fertilizer uses and poor application methods can cause harmful effects to soil fertility and to the environment in general. The need for a responsible and sustainable manner in the use of fertilizer prompted the Philippine government in a decisive shift towards mainstreaming policies that promotes sustainable and environmentally sound options to improve quality of soil and fertility. The country has promulgated policies that encouraged the adoption of organic agriculture (RA 10068) and support it through sustainable solid waste management (RA 9003) and development of standards (PNS/BAFS 40:2013). These policies in turn supported the production and adoption of the use of soil amendments which include organic fertilizers. Clearly, the Philippine policies on fertilizers are promulgated with the ultimate goal of striking balance between increasing productivity and preventing degradation of the environment.

REFERENCES

Alcala, P. J. 2012. Fertilizer Market in the Philippines: Evolution, Challenges and Outlook. Keynote Message presented by Dr, Norlito R. Gicana, Executive Director of the Fertilizer and Pesticide Authority in behalf of Secretary Proceso J. Alcala of the Philippines Department of Agriculture during the International Fertilizer Association Crossroads Asia-Pacific Conference, Manila, Philippines 29-31 October 2012.

Aquino, A.P., Deriquito, J.A.P. and Tidon, A.G. 2010. Fertilizer Policy for Ensuring Sustainable Food Production in the Philippines. International Seminar on Fertilizer Policy for Ensuring Sustainable Food Production in the Asia- Pacific Region, International Technology Cooperation Center (ITCC), Rural Development Administration, Suwon, South Korea, 21-26 June 2010.

Briones, R. M. 2014. The Role of Mineral Fertilizers in Transforming Philippine Agriculture. Discussion Paper Series No. 2014-14. Philippine Institute for Development Studies. February 2014. (https://dirp4.pids.gov.ph/webportal/CDN/PUBLICATIONS/pidsdps1414.pdf; Accessed 15 April 2018).

Bureau of Agriculture and Fisheries Standards. Philippine National Standard for Organic Soil Amendments. (http://organic.da.gov.ph/images/downloadables/PNS/PNS-Organic-Soil-Amendments-PNS-BAFS-40-2016.pdf; Accessed 15 April 2018).

Chupungco, A. R. 2003. Impact of trade policies on prices of fertilizer: Working Paper No. 03-07. Institute of Strategic Planning and Policy Studies, College of Public Affairs, University of the Philippines Los Banos, Laguna.

Fertilizer and Pesticide Authority. 2010. Fertilizer supply and demand, by major grade, 1980-2008. (http://fpa.da.gov.ph/1970-2008fertSDandaveprices.pdf; Accessed 15 January 2018).

Fertilizer and Pesticide Authority. 2016 List of License Fertilizer Distributor. (http://www.fpa.da.gov.ph/images/FPAfiles/DATA/Regulation/Fertilizer/Files-2017/Fertilizer-Distributor.pdf; Accessed 15 April 2018)

Fertilizer and Pesticide Authority. 2016 List of License Fertilizer and Pesticide Dealers. (http://www.fpa.da.gov.ph/images/FPAfiles/DATA/Regulation/Fertilizer/Files-2017/License-F-P-FP-Delears-July2017.pdf; Accessed 15 April 2018)

Food and Agriculture Organization. 2015. World Fertilizer Trends and Outlook to 2018. (http://www.fao.org/3/a-i4324e.pdf; Accessed 15 April 2018).

How, M.O. 2015. The agriculture sector and the fertilizer industry in the Philippines: Updates, Trends and Outlook. Paper presented during the 2015 International Fertilizer Industry Association at Kuala Lumpur City Centre, Kuala Lumpur, 20-22 October, 2015. (https://www.fertilizer.org//images/Library_Downloads/2015_Crossroads_KL_How.pdf; Accessed 15 January 2018).

Presidential Decree (PD) 135. Creating the Fertilizer Industry Authority. (https://www.lawphil.net/statutes/presdecs/pd1973/pd_135_1973.html; Accessed February 11, 2018).

PD 1144. Creating the Fertilizer and Pesticide Authority and Abolishing the Fertilizer Industry Authority. (http://fpa.da.gov.ph/index.php/policies-laws-and-regulations/presidential-decree-no-1144; Accessed Feb 11, 2018).

Republic Act (RA) 8435. An Act Prescribing Urgent Related Measures to Modernize the Agriculture and Fisheries Sectors of the Country in Order to Enhance their Profitability, and Prepare Said Sectors for the Challenges of the Globalization through an Adequate, Focused and Rational Delivery of Necessary Support Services, Appropriating Funds Therefor and for Other Purposes. (https://www.lawphil.net/statutes/repacts/ra1997/ra_8435_1997.html; Accessed February 11, 2018)

RA 10068. An Act providing for the Development and Promotion of Organic Agriculture in the Philippines and for Other Purposes. (https://www.lawphil.net/statutes/repacts/ra2010/ra_10068_2010.html; Accessed February 11, 2017)

RA 9003. An Act Providing for an Ecological Solid Waste Management Program, Creating the Necessary Institutional Mechanisms and Incentives, Declaring Certain Acts Prohibited and Providing Penalties, Appropriating Funds Therefor, and for Other Purposes. (https://www.lawphil.net/statutes/repacts/ra2001/ra_9003_2001.html; Accessed February 11, 2018)

Tirado, R. and Bedoya, D. 2008. Agrochemical use in the Philippines and its consequences to the environment. Greenpeace Southeast Asia 24 KJ Street, East Kamias Quezon City, Philippines. (http://www.greenpeace.to/publications/gpsea_agrochemical-use-in-the-philip.pdf; Accessed 15 January 2018)

|

Date submitted: July 24, 2018

Reviewed, edited and uploaded: August 1, 2018

|

[1] Balanced fertilization is a location specific application of organic and inorganic fertilizers to reduce the effect of wide variation in soil and climatic condition (Department of Agriculture, n.d.)

Towards a More Productive Agriculture: A Review of the Policies Affecting the Philippine Fertilizer Industry

ABSTRACT

The important contribution of fertilizers in achieving agricultural productivity to ensure food security is highlighted in this paper. State of the two sub-sectors of the Philippine fertilizer industry, the inorganic fertilizer and bio-fertilizer, was discussed. The inorganic fertilizer industry is private sector-led and operates in a free market while the bio-fertilizer industry is influenced by government programs and initiatives. Landmark policies in the country were enacted that affected the fertilizer industry. These policies included the creation of policy-making bodies or government agencies supporting the operation of the fertilizer industry in the country; policies gearing toward environmental sustainability, hence, supporting the bio-fertilizer sub-industry and policies advocating for quality standards. The Philippines has provided a policy environment that supports the twin goal of improving productivity and protecting the environment from degradation.

Key words: inorganic fertilizers, bio-fertilizers, organic agriculture, fertilizer policies

INTRODUCTION

Prior to 1972, the fertilizer industry in the Philippines was free from control. Fertilizer importation, distribution and marketing were in the hands of the private sector while government restrictions, tariffs and subsidies were lacking. However, with the increasing recognition of fertilizer as one of the important inputs in improving agricultural productivity and ensuring food security for the Filipinos, the country realized the need for policies governing the development of the fertilizer industry.

The growing food production to meet the ever increasing demand for food, especially for grains and cereals, has driven the global growth of the fertilizer industry. World demand for total fertilizer nutrients, nitrogen (N), phosphorus (P) and potassium (K) is estimated to reach an annual growth rate of 1.8% from 2014 to 2018. Moreover, the demand for N, P, K is projected to grow annually by 1.4%, 2.2% and 2.6%, respectively. Forecasts over the next five years also showed increase in global capacity of fertilizer products, intermediaries and raw materials (FAO, 2015).

In the case of the Philippines, its goal of achieving self-sufficiency especially in two of the major staples in the country, rice and corn, was considered one of the major factors driving the policy environment for fertilizers. On average, rice and corn used about 38% and 21% of the total fertilizer supply in the country, respectively (How, 2015). Meanwhile, extent and rate of fertilizer utilization, which were mainly nitrogenous fertilizers, ranged from 93% to 94%. Given this very crucial role of fertilizers, many of the agricultural programs in the country included the provision and usage of fertilizers as one of the major program components.

In 1973, regulation and control of the fertilizer industry was realized in the country through the establishment of a regulatory board, the Fertilizer Industry Authority (FIA). The government completely changed its policy from non-intervention to rigid and all-encompassing control over fertilizer prices, mark up, distribution channels, promotion, importation, exportation, and production (Alcala, 2012). FIA also provides for the outright tax exemption of the importation of all kinds of fertilizers. By 1986, in line with trade liberalization, government's control was relegated and limited to issuance of fertilizer handler licenses, compilation of national statics (statistics?), and monitoring and assurance of good quality fertilizers.

This paper presents the state of the fertilizer industry in the Philippines and its sub-sectors, the inorganic and bio-fertilizers industries. It highlights the significant policies that govern fertilizer production, utilization, and trade as well as their implications in achieving food sufficiency and/or security and environmental sustainability.

PHILIPPINE FERTILIZER INDUSTRY

The fertilizer industry can be subdivided into two sub-industries, inorganic and bio-fertilizers. The inorganic fertilizer industry operates in a free market while the bio-fertilizer industry is generally driven by government policies. A discussion on supply, demand and prices, specifically for inorganic fertilizers, is also presented in this section.

Inorganic sub-industry

In the Philippines, the marketing, distribution, and prices of inorganic fertilizers are largely dictated by the private sector. Marketing, as shown in Fig. 1 is done in four main levels: (1) indentors/traders; (2) importers/manufacturers; (3) distributors; and (4) dealers (How, 2015). Fertilizers enter the country in the form of raw materials and finished products or the ready to use fertilizers. Both are distributed through the indentors or traders, the finished products though can be directly provided to importers also. End users such as the plantation, industrial users and cooperatives have various sources or suppliers of fertilizer which can be from domestic manufacturers, importers/producers and distributors. On the other hand, fertilizer suppliers of farmers are limited to local dealers or cooperatives. Key players for the domestic production of fertilizers involve five major fertilizer producers manufacturing mainly nitrogen (N) and nitrogen-phosphorus-potassium (NPK) grades, namely: (1) Philphos; (2) AFC Fertilizer & Chemical Inc. (AFC); (3) International Chemical Corp. (INCHEM); (4) Farmix Fertilizer Corp.; and (5) Soiltech Agricultural Products Corp. (Chupungco, 2003 as cited by Aquino et al., 2010).

Fig. 1. Distribution channels of fertilizer in the Philippines

Source: Food and Agriculture Organization, Fertilizer and Pesticide Authority as cited by How, 2015

In 2016, there were 218 registered fertilizer distributors in the Philippines (Table 1). Majority (80%) of these distributors were located in Luzon, of which 44% were located in the National Capital Region (NCR). The other distributors were located in the Visayas (16%), while very small number of distributors can be found in Mindanao (5%). On the other hand, the dealers, who are directly connected to the farmers were widely distributed all over the country. There were 4,755 registered fertilizer dealers in the country in 2016, majority (86%) of which were selling both fertilizers and pesticides while 14% were solely dealing fertilizers only (FPA, 2018).

Supply of inorganic fertilizers

There are six major inorganic fertilizer grades available in the market, namely: Urea (46-0-0); Ammonium Sulfate (21-0-0); Ammonium Phosphate (16-20-0); Diammonium Phosphate (18-46-0); Complete (14-14-14), and Muriate of Potash (0-0-60). Inorganic fertilizers were sourced from importation (69%) and domestic production (31%) (Table 2). In general, total supply increased at annual growth rate of 4.68%. Fluctuations were observed in both domestic supply and imports (Fig. 2). However, domestic supply showed dramatic reduction of 25% annual average from 2002 to 2010. The lowest domestically produced inorganic fertilizers was recorded in 2010 at 36,000 metric tons only and zero production in 2015.

Table 2. Total supply of inorganic fertilizers in the Philippines, in ‘000 metric tons, by source, 1990-2016

Source: Fertilizer and Pesticide Authority (FPA), 2018

Fig. 2. Supply of inorganic fertilizers, by source, 1990-2016

The supply of the six major fertilizers from 1990-2016, as shown in Table 3, indicated nitrogenous fertilizers such as Urea and Ammonium Sulfate as the most supplied fertilizers in the country. Urea ranked first, contributing 34% of the total supply while Ammonium Sulfate ranked second providing 20% of the total supply.

Table 3. Supply of the six major inorganic fertilizers in the Philippines, in ‘000 metric tons, 1990-2016

Source: Fertilizer and Pesticide Authority (FPA), 2018

Complete was the highest domestically produced inorganic fertilizer in the country contributing 44% of the total local supply. Ammonium phosphate ranked second with an average domestic production of 205,000 metric tons while muriate of potash ranked last with only less than 1% contribution to the total domestically produced supply of inorganic fertilizers.

In terms of imports, the highest importation is recorded for urea contributing 49% of the total imported inorganic fertilizers. Moreover, it is the only fertilizer that is not domestically produced and is mainly imported, implying vulnerability of farmers to changes in world prices. Urea is also the primary nitrogenous fertilizer used by farmers. How 2015, also emphasized that importation of fertilizer is generally increasing which peaked in 2008, majority of which were the nitrogenous type. These fertilizers are mainly sourced from ASEAN and other countries where Philippines have trade agreements (Free Trade Agreement (FTA)) (Fig. 3). It should be noted that fertilizer importation was generally liberalized in accordance to trade agreements that promote reduction/elimination of subsidies and products to flow freely. The implementation of the Agriculture and Fisheries Modernization Act (AFMA) provided for imported fertilizers that obtained certification from the Department of Agriculture (DA) be exempted from tariff duties from 2004-2015 (Aquino et al., 2010).

Fig. 3. Distribution of imported inorganic fertilizers, by source, 2012-2014

Source: How, 2015

Disposition of inorganic fertilizers

In terms of fertilizer disposition from 1990-2016, the Philippines recorded an average total local sales of 1,206,000 metric tons (91%) while exports comprised 124,000 metric tons (9%) (Table 4). Highest domestic sales were recorded in 1997 at 1,996,000 metric tons while minimal exports were observed with highest amount recorded in 1991 at only 357,000 metric tons. In 2014-2016, the country has no exportation of the six major fertilizers.

Table 4. Disposition of inorganic fertilizers in the Philippines, in ‘000 metric tons, 1990-2016

Source: Fertilizer and Pesticide Authority (FPA), 2018

Similar to supply, both local sales and exportation experienced fluctuations (Fig. 4). Dramatic reduction in sales, 16% annual average, was also observed for the period 2002-2010. Peaks of domestic sale were observed in 1996, 2012 and 2014 while deepest fall was recorded in 2015 with only 214,000 metric tons locally used fertilizers.

Fig. 4. Disposition of inorganic fertilizers in the Philippines, 1990-2016

Among the six major fertilizers, as shown in Table 5, the highest amount used locally is Urea at 432,000 metric tons (32%). Complete fertilizer ranked second with an average local sales of 292,000 metric tons (16%) while Ammonium Sulfate closely followed contributing 14% of the total local sales or 212,000 metric tons, on average. Considering the limited supply, muriate of potash expectedly ranked last among the fertilizers locally used with only 54,000 metric tons (4%).

Table 5. Disposition of the six major inorganic fertilizers in the Philippines, in ‘000 metric ton, 1990-2016.

Price

Retail prices of the six major fertilizer grades generally increased (Table 6). Significant surge in fertilizer prices was observed in 2008, almost all fertilizers doubled their prices. It should be noted that oil prices also spike during this period. After 2008 price hike, prices of fertilizers generally decreased except for Muriate of Potash which reached its highest price at P2,858/bag in 2013. Trade liberalization, which allowed for free movement and decrease in tariffs of products, could have contributed to the decrease in prices of fertilizers.

Bio-fertilizer sub-industry

Bio-fertilizers is gaining recognition in the Philippine market. With the environmental threat caused by the extensive and inappropriate use of inorganic fertilizer which resulted to land degradation and significant loss of soil fertility (Tirado and Bedoya, 2008) policy makers have been pushing for balanced fertilization[1] and adoption of organic farming. The use of bio-fertilizers was among the key component of organic agriculture and was promoted through various government policies and programs. Incidentally, these initiatives were supported by the private sector which started with the organic movement by some non-government organizations (NGOs) in the 1980s. This was followed by the movement for sustainable development and supported through the Organic Producers and Trade Association (OPTA) formed in 1995. OPTA became the frontrunner in advocating for organic agriculture including the use of bio-fertilizers.

As of 2006, there were 59 FPA-registered organic fertilizers and 18-registered plant growth regulator brands available in the market. Domestically, 76% of the organic fertilizers and 50% of the plant growth regulator brands were produced. Organic fertilizers comprised 86% of the bio-fertilizer industry which were composed of 54 manufacturers, 13 importers, 67 distributors and 2 exporters (Aquino et al., 2010).

Relative to inorganic fertilizer sub-industry, bio-fertilizer sub-industry is not well developed. This can be closely associated with the still formative stage of organic farming in the Philippines. It should be noted that the production of organic products is still marginal. They are planted in less than one percent of the total agricultural land in the country (NOAP 2012-2016). Also, marketing and distribution of bio-fertilizers is simple. The manufacturers or producers, in most cases, are also the traders who distribute organic fertilizers directly to customers such as other traders/distributors and farmers. To increase sales, other incentives given to users include trainings, seminars, discounts and free or no cost delivery of organic fertilizers.

Government programs serve as key driver to move the initiatives for the use of bio-fertilizers. As indicated in the recommendations of Aquino et al. (2010), for the bio-fertilizer industry to remain competitive, the government could focus on these initiatives: (1) market development to address issues on seasonality of demand; (2) establishment of royalty policy to support researchers and investors; (3) support for R&D investment; and (4) other necessary support services.

PHILIPPINE FERTILIZER POLICIES AND PROGRAMS

Initially, fertilizer industry in the Philippines was marked by a laissez faire policy. By 1973, fertilizer has been recognized as one of the major components in improving farm productivity. This has led to the promulgation of agriculture and fertilizer laws which in the end have been translated into various government programs and projects.

Landmark legislations affecting the fertilizer industry were enacted which include the Creation of the Fertilizer and Pesticide Authority (Presidential Decree (PD) 1144), Agriculture and Fisheries Modernization Act (Republic Act (RA) 8435), Organic Agriculture Act of 2010 (RA 10068), and Ecological Solid Waste Management Act (RA 9003). The Bureau of Agriculture and Fisheries Standards (BAFS) also developed the national standard for organic fertilizers.

Creation of the regulatory board

Through the promulgation of PD 135, the Fertilizer Industry Authority (FIA) was created on February 22, 1973. FIA was mandated to control and regulate the prices, mark-ups, distribution channels, promotion, storage, production, import and export of fertilizer. It also had the power to negotiate and enter into contract for all imports and experts of fertilizer and fertilizer inputs. In addition, importation of all kinds of fertilizers made by FIA was exempted from custom duties, compensating and sales taxes and all other taxes.

By 1977, PD 1144 merged the fertilizer and pesticide industries and placed them under the jurisdiction of a single government agency, the Fertilizer and Pesticide Authority (FPA). PD 1144 abolished FIA but adopted and retained the board power provided under PD 135 on fertilizer regulation and control.

In line with the liberalization policy of the government, the Philippine fertilizer industry has been deregulated since 1986. The government’s role is now confined to issuance of fertilizer handler licenses, compilation of national statistics, and monitoring and assurance of good quality fertilizers (Alcala, 2012).

Fertilizer as a strategic component in modernizing agriculture

On July 28, 1997, RA 8435 also known as the Agriculture and Fisheries Modernization Act (AFMA) of 1997 was promulgated. The law aims to modernize the agriculture and fisheries sectors by transforming these sectors from a resource-based to a technology-based industry. This is with the end in view of attaining food security, poverty alleviation, social equity, global competitiveness and environmental sustainability.

The law specifically cites provisions that support the optimal use of farm inputs like fertilizers. These could be seen in the credit and financing support, infrastructure support service and trade and fiscal incentives. The Agro-Industry Modernization Credit and Financing Program under the AFMA provide support to the acquisition of fertilizer and other farm inputs like seeds, poultry, livestock, feeds and other similar items as well as agriculture and fisheries production inputs including processing of fisheries and agri-based products and farm inputs.

Infrastructure support to ensure that agriculture and fisheries production inputs (including fertilizers) as well as information and technology were readily available to farmers, fisherfolks, cooperatives and entrepreneurs. This is part of the special concerns in formulating the Agriculture and Fisheries Modernization Plan.

Promotion and commercialization of organic fertilizer

The approval of the RA 10068, An Act Providing for the Development and Promotion of Organic Agriculture in the Philippines and for Other Purposes also known as the Organic Agriculture Act of 2010 has profound implication on the development of the bio-fertilizer sub-industry. The law promotes, propagate, develop further and implement the practice of organic agriculture in the Philippines that will cumulatively condition and enrich the fertility of the soil, increase farm productivity, reduce pollution and destruction of the environment, prevent the depletion of natural resources, further protect the health of farmers, consumers, and the general public, and save on imported farm inputs. Towards this end, a comprehensive program was developed for the promotion of community-based organic agriculture systems.

Recognition of the use of bio-fertilizers has been accorded both by the private and public sectors. Private initiatives started with the organic movement by some NGOs in the 1980s, followed by sustainable development initiatives of many farmer organizations and other NGOs in the 1990s. The Organic Producers and Trade Association (OPTA) became one of the frontrunners in advocating for organic agriculture which include the use of bio-fertilizers (Aquino, et al., 2010).

An attached office to the Department of Agriculture, the National Organic Agricultural Board was created under RA 10068. Mandated by law, NOAB serves as the policy-making body that provides direction and general guidelines for the implementation of the National Organic Agricultural Program (NOAP). The NOAP developed for 2012-2016 is a collaborative initiative among various stakeholders of the organic industry, the national government agencies/offices, NGOs, civil society and people’s organizations. NOAP serves as guide in the implementation of the organic agriculture as stipulated under the provisions of RA 10068. NOAP 2012-2016 envisions to contribute to the overall welfare and development of the Philippines wherein 5% of the total farm areas adopts and practices organic agriculture. NOAP’s objective of enhancing soil fertility and farm biodiversity may have great impacts on demand and utilization of bio-fertilizers. Further, advancement in the bio-fertilizer industry is foreseen with the implementation of RA 9003 or the Ecological Solid Waste Management Act of 2000 and RA 10068 as well as the establishment of Philippine National Standard for Organic Soil Amendments.

Major issues on organic fertilizer production include irregular production due to non-continuous demand from end users. There is also non-uniformity of product pricing both at the manufacturers’ and traders’ levels. Hence, there is a need for strong promotion and encouragement of the establishment of facilities, equipment and processing plants that would accelerate the production and commercialization of organic fertilizers, pesticides, herbicides and other farm inputs. A facilitative delivery and extension system can also provide an enabling environment for the promotion of the use of organic fertilizers (Aquino et al., 2010).

Composting as a solid waste management approach

The beneficial effects of compost application to the soil and plant productivity cannot be understated. It improves the soil’s physical, chemical and biochemical properties resulting to enhanced nutrient utilization by plants and minimized nutrient leaching (Tejada, et. al., 2006 as cited by Abrigo, 2008). Furthermore, it helps mitigate environmental imbalances brought by the increasing carbon dioxide concentration in the atmospheres.

The Ecological Solid Waste Management Act of 2000 (RA 9003) laid the framework for biodegradable waste to be used for organic fertilizer production. RA 9003 provides for the establishment of materials recovery facility (MRF) for composting activities which is particularly important to meet the provisions of Section 7 of the implementing rules and regulations of RA 9003 which states that at least 25% of all solid waste from waste disposal facilities should be diverted through composting.

Establishment of the Philippine National Standards for Soil Amendments

Originally developed as the Philippine National Standards (PNS) for organic fertilizers (PNS/BAFS 40:2013), the BAFS revised the said PNS to include the results of recent scientific and technological studies both local and international on the specifications of organic fertilizers, compost, soil conditioner, microbial inoculants and organic plant supplements. The PNS was then revised and changed from PNS for Organic Fertilizer to PNS for Organic Soil Amendments. The PNS indicates the specifications of theses soil amendments including the laboratory tests for finished products, labeling of these products (e.g. on bottles or cartons) and the permitted/allowed raw materials in the production of the soil amendments.

CONCLUSION

The fertilizer industry has a very important role in the development of agricultural productivity. It has a great deal of responsibility in meeting the world's increasing demand for food through improvement in food crop productivity. To produce the greatest possible output in ensuring food security, the Philippine government promulgated landmark legislations that created the Fertilizer and Pesticide Authority and incentives that would encourage fertilizer traders to increase their imports and made it easier for domestic manufacturers to import raw materials for locally produced fertilizer as stipulated in the AFMA.

However, excess fertilizer uses and poor application methods can cause harmful effects to soil fertility and to the environment in general. The need for a responsible and sustainable manner in the use of fertilizer prompted the Philippine government in a decisive shift towards mainstreaming policies that promotes sustainable and environmentally sound options to improve quality of soil and fertility. The country has promulgated policies that encouraged the adoption of organic agriculture (RA 10068) and support it through sustainable solid waste management (RA 9003) and development of standards (PNS/BAFS 40:2013). These policies in turn supported the production and adoption of the use of soil amendments which include organic fertilizers. Clearly, the Philippine policies on fertilizers are promulgated with the ultimate goal of striking balance between increasing productivity and preventing degradation of the environment.

REFERENCES

Alcala, P. J. 2012. Fertilizer Market in the Philippines: Evolution, Challenges and Outlook. Keynote Message presented by Dr, Norlito R. Gicana, Executive Director of the Fertilizer and Pesticide Authority in behalf of Secretary Proceso J. Alcala of the Philippines Department of Agriculture during the International Fertilizer Association Crossroads Asia-Pacific Conference, Manila, Philippines 29-31 October 2012.

Aquino, A.P., Deriquito, J.A.P. and Tidon, A.G. 2010. Fertilizer Policy for Ensuring Sustainable Food Production in the Philippines. International Seminar on Fertilizer Policy for Ensuring Sustainable Food Production in the Asia- Pacific Region, International Technology Cooperation Center (ITCC), Rural Development Administration, Suwon, South Korea, 21-26 June 2010.

Briones, R. M. 2014. The Role of Mineral Fertilizers in Transforming Philippine Agriculture. Discussion Paper Series No. 2014-14. Philippine Institute for Development Studies. February 2014. (https://dirp4.pids.gov.ph/webportal/CDN/PUBLICATIONS/pidsdps1414.pdf; Accessed 15 April 2018).

Bureau of Agriculture and Fisheries Standards. Philippine National Standard for Organic Soil Amendments. (http://organic.da.gov.ph/images/downloadables/PNS/PNS-Organic-Soil-Amendments-PNS-BAFS-40-2016.pdf; Accessed 15 April 2018).

Chupungco, A. R. 2003. Impact of trade policies on prices of fertilizer: Working Paper No. 03-07. Institute of Strategic Planning and Policy Studies, College of Public Affairs, University of the Philippines Los Banos, Laguna.

Fertilizer and Pesticide Authority. 2010. Fertilizer supply and demand, by major grade, 1980-2008. (http://fpa.da.gov.ph/1970-2008fertSDandaveprices.pdf; Accessed 15 January 2018).

Fertilizer and Pesticide Authority. 2016 List of License Fertilizer Distributor. (http://www.fpa.da.gov.ph/images/FPAfiles/DATA/Regulation/Fertilizer/Files-2017/Fertilizer-Distributor.pdf; Accessed 15 April 2018)

Fertilizer and Pesticide Authority. 2016 List of License Fertilizer and Pesticide Dealers. (http://www.fpa.da.gov.ph/images/FPAfiles/DATA/Regulation/Fertilizer/Files-2017/License-F-P-FP-Delears-July2017.pdf; Accessed 15 April 2018)

Food and Agriculture Organization. 2015. World Fertilizer Trends and Outlook to 2018. (http://www.fao.org/3/a-i4324e.pdf; Accessed 15 April 2018).

How, M.O. 2015. The agriculture sector and the fertilizer industry in the Philippines: Updates, Trends and Outlook. Paper presented during the 2015 International Fertilizer Industry Association at Kuala Lumpur City Centre, Kuala Lumpur, 20-22 October, 2015. (https://www.fertilizer.org//images/Library_Downloads/2015_Crossroads_KL_How.pdf; Accessed 15 January 2018).

Presidential Decree (PD) 135. Creating the Fertilizer Industry Authority. (https://www.lawphil.net/statutes/presdecs/pd1973/pd_135_1973.html; Accessed February 11, 2018).

PD 1144. Creating the Fertilizer and Pesticide Authority and Abolishing the Fertilizer Industry Authority. (http://fpa.da.gov.ph/index.php/policies-laws-and-regulations/presidential-decree-no-1144; Accessed Feb 11, 2018).

Republic Act (RA) 8435. An Act Prescribing Urgent Related Measures to Modernize the Agriculture and Fisheries Sectors of the Country in Order to Enhance their Profitability, and Prepare Said Sectors for the Challenges of the Globalization through an Adequate, Focused and Rational Delivery of Necessary Support Services, Appropriating Funds Therefor and for Other Purposes. (https://www.lawphil.net/statutes/repacts/ra1997/ra_8435_1997.html; Accessed February 11, 2018)

RA 10068. An Act providing for the Development and Promotion of Organic Agriculture in the Philippines and for Other Purposes. (https://www.lawphil.net/statutes/repacts/ra2010/ra_10068_2010.html; Accessed February 11, 2017)

RA 9003. An Act Providing for an Ecological Solid Waste Management Program, Creating the Necessary Institutional Mechanisms and Incentives, Declaring Certain Acts Prohibited and Providing Penalties, Appropriating Funds Therefor, and for Other Purposes. (https://www.lawphil.net/statutes/repacts/ra2001/ra_9003_2001.html; Accessed February 11, 2018)

Tirado, R. and Bedoya, D. 2008. Agrochemical use in the Philippines and its consequences to the environment. Greenpeace Southeast Asia 24 KJ Street, East Kamias Quezon City, Philippines. (http://www.greenpeace.to/publications/gpsea_agrochemical-use-in-the-philip.pdf; Accessed 15 January 2018)

Date submitted: July 24, 2018

Reviewed, edited and uploaded: August 1, 2018

[1] Balanced fertilization is a location specific application of organic and inorganic fertilizers to reduce the effect of wide variation in soil and climatic condition (Department of Agriculture, n.d.)