INTRODUCTION

The main actors in the Vietnamese rice value chain are farmers (paddy growers), traders, processors (drying, milling, polishing), and food trading and export enterprises. Of these, many export enterprises have owned milling and polishing systems to meet the conditions of rice export in accordance with Decree 109/2010/ND-CP. In this case, the export enterprises have also played the role of processors as well as exporters in the value chain.

Vietnam has two main rice production regions such as Red River Delta (RRD) and Mekong River Delta (MRD). Rice production in the RRD mainly serves the domestic market, while rice in the MRD is produced for both domestic as well as export markets. This report analyzes the distribution of economic benefits between actors in both rice export and domestic consumption value chains. Local consumption chains were studied in the RRD, while export chains were studied in the MRD.

Distribution of profits in the domestic rice value chain

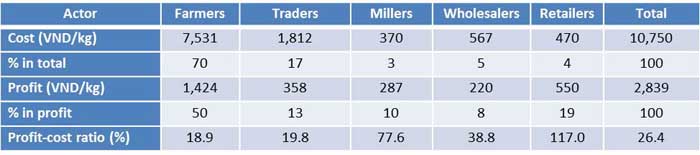

According to Thang et al. (2014), the total cost of the final rice product in 2014 from farm to consumer in the whole value chain was VND10,750/kg (US$0.47/kg) and the total profit was VND2,839/kg (US$0.12/kg). In the total cost of final rice products, farmers contributed the highest rate of 70%. The next was trader with 17%. Wholesalers contributed 5% of total cost and shares of retailers and milling factories were 4% and 3%, respectively. In total of profits in wholevalue chain, farmers captured 50.16% while 19.37% were captured by the retailers. The profit share of traders, milling and exporting companies and wholesalers were 12.61%, 10.11% and 7.75%, respectively. However, the profit-cost ratio (profit/cost) of retailers is highest with 117%, next is milling and export companies with 78%, wholesalers with 39%, traders with 20% and profit ratio of farmers is lowest with only 19%. Thus, in the domestic chain value, despite capturing the highest share in profit of rice products in the whole value chain, if the cost of paddy production paid by farmers is the highest, the profit-cost ratio of farmers is the lowest among actors.

Table 1. Cost and profit per kilogram rice in domestic value chain

Source: Thang T.C et al. (2014)

The absolute profit gained by different stakeholders in the value chain depends on scales of production and trade volume. On average, rice farm size in the Red River Delta is less than 0.5 ha per household. With two seasons per year, according to Thang T.C et al. (2014), after subtracting losses from harvesting, uses for seedlings, home consumption and for animal feed, one farm household sold 3.5 metric tons of paddy and earned net profit of 5 million VND (US$220. Exchange rate of VND on US$ is 22,772 VND on April 19, 2017) per year. Meanwhile, each trader procured and sold 50-100 metric tons of rice per year, then the profit of each trader each year is about 17.9 to 35.8 million VND (US$786 to 1,572) per year. Also with the annual volume of rice trading equivalent to the traders, each wholesale agent gets a profit of about 10 - 20 million VND (US$439 – 878) per year and each retailer will earn about 25 to 50 million VND (US$1,098 to 2,196) per year. The milling and export companies traded average about 300-500 metric tons they earn from 60 to 100 million VND (US$263.5 to 4,391) per year. Thus, after taking into account scale of production and trading, the profit in the rice value chain have been descended from miller to retailer, trader, wholesaler and finally farm household.

Distribution of profits in the value chain of rice export

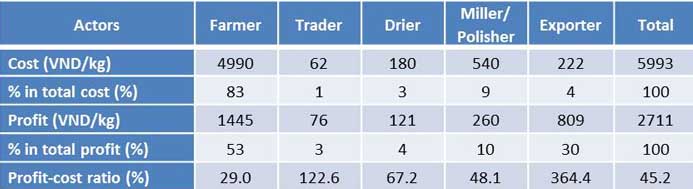

According to Thang T.C. at al. (2014), the total cost of the whole chain of exported rice was 5,993 VND/kg and total profit earned by all actors was 2,711 VND/kg. The cost structure distribution in the whole chain was gradually reduced from farmers (83%), milling and polishing (9%), exporters (4%), dryers (3%), and traders (1%). The structure of profits of the whole chain caputed by different stakeholders decreased gradually from farmers (53%), exporters (30%), millers – polishers (10%), drying agents (4%) and traders (3% ).

Table 2. Costs and profit (per kilogram) of long-grain white rice in export value chain

Source: Thang T.C et al. (2014)

Though farmers take the largest percentage of profit per kilogram of rice product in the value chain, due to their small size (approximately one hectare per household), the income of paddy growers is much lower than other stakeholders. On average, profit from paddy production is about 12 million VND (US$527) per hectare per season. Meanwhile, a trader with total trade volume of 40 M/T per season can earn 25- 30 million VND (US$1,098 – US$1,317) per season, about 60-75 million VND per year.

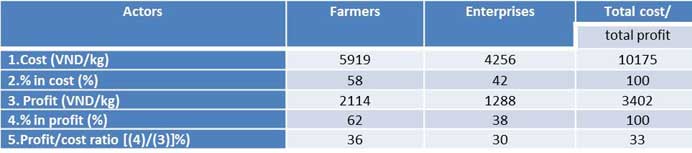

In recent years, linkage between farmers and enterprises value chain has been improved even though it is slow. According to Thang T.C et al. (2014), approximately 4% of the total rice product at the Mekong River Delta was sold directly to export enterprises. The model of the direct link between farmers and enterprises included two main types: (i) complete value chain where enterprise provides input to paddy growers and procure paddy; (ii) contract farming where enterprise signed contract with farmers to buy paddy. It is noteworthy that farmers who engage in direct linkage with enterprises have a higher profit-cost ratio (36%) than farmers who do not. Simultaneously, the distribution of costs and benefits in the direct linkage was also relatively fairer, in which, paddy growers contribute 58% of total cost of final rice product and they received 62% of total profit. Apart from better income for rice farmers, the value chain of direct linkage between farmers and companies value chain can give a favorable condition for doing traceability of the rice, controlling the pesticide residue and homogeneous level of rice and registering the brand for rice products.

Table 3. Cost - profit distribution of Jasmine rice (5% milled) in the direct linkage between farmers and companies

Source: Thang T.C et al. (2014)

CONCLUSION

The rice value chain in Vietnam is characterized by many middlemen. Profit share per one kilogram of rice received by rice growers among stakeholders in value chain is not small but profit-cost ratio of the growers is much smaller than other actors. In addition, due to small farm sizes, the income earned by farmers are much smaller than other stakeholders in the value chain. The farmers in the complete value chain where they sell directly their paddy to companies get better income. This explains why the development of the complete value chain is strongly demanded in Vietnam as a strategy for assuring income for farmers.

REFERENCES

Thang T.C. et al. (2014), Policies and measures for improve the efficiency of value chain: the cases of rice and pork in Vietnam, Hanoi, Vietnam.

|

Date submitted: March 30, 2017

Reviewed, edited and uploaded: April 19, 2017

|

Income Distribution in Vietnam’s Rice Value Chain

INTRODUCTION

The main actors in the Vietnamese rice value chain are farmers (paddy growers), traders, processors (drying, milling, polishing), and food trading and export enterprises. Of these, many export enterprises have owned milling and polishing systems to meet the conditions of rice export in accordance with Decree 109/2010/ND-CP. In this case, the export enterprises have also played the role of processors as well as exporters in the value chain.

Vietnam has two main rice production regions such as Red River Delta (RRD) and Mekong River Delta (MRD). Rice production in the RRD mainly serves the domestic market, while rice in the MRD is produced for both domestic as well as export markets. This report analyzes the distribution of economic benefits between actors in both rice export and domestic consumption value chains. Local consumption chains were studied in the RRD, while export chains were studied in the MRD.

Distribution of profits in the domestic rice value chain

According to Thang et al. (2014), the total cost of the final rice product in 2014 from farm to consumer in the whole value chain was VND10,750/kg (US$0.47/kg) and the total profit was VND2,839/kg (US$0.12/kg). In the total cost of final rice products, farmers contributed the highest rate of 70%. The next was trader with 17%. Wholesalers contributed 5% of total cost and shares of retailers and milling factories were 4% and 3%, respectively. In total of profits in wholevalue chain, farmers captured 50.16% while 19.37% were captured by the retailers. The profit share of traders, milling and exporting companies and wholesalers were 12.61%, 10.11% and 7.75%, respectively. However, the profit-cost ratio (profit/cost) of retailers is highest with 117%, next is milling and export companies with 78%, wholesalers with 39%, traders with 20% and profit ratio of farmers is lowest with only 19%. Thus, in the domestic chain value, despite capturing the highest share in profit of rice products in the whole value chain, if the cost of paddy production paid by farmers is the highest, the profit-cost ratio of farmers is the lowest among actors.

Table 1. Cost and profit per kilogram rice in domestic value chain

Source: Thang T.C et al. (2014)

The absolute profit gained by different stakeholders in the value chain depends on scales of production and trade volume. On average, rice farm size in the Red River Delta is less than 0.5 ha per household. With two seasons per year, according to Thang T.C et al. (2014), after subtracting losses from harvesting, uses for seedlings, home consumption and for animal feed, one farm household sold 3.5 metric tons of paddy and earned net profit of 5 million VND (US$220. Exchange rate of VND on US$ is 22,772 VND on April 19, 2017) per year. Meanwhile, each trader procured and sold 50-100 metric tons of rice per year, then the profit of each trader each year is about 17.9 to 35.8 million VND (US$786 to 1,572) per year. Also with the annual volume of rice trading equivalent to the traders, each wholesale agent gets a profit of about 10 - 20 million VND (US$439 – 878) per year and each retailer will earn about 25 to 50 million VND (US$1,098 to 2,196) per year. The milling and export companies traded average about 300-500 metric tons they earn from 60 to 100 million VND (US$263.5 to 4,391) per year. Thus, after taking into account scale of production and trading, the profit in the rice value chain have been descended from miller to retailer, trader, wholesaler and finally farm household.

Distribution of profits in the value chain of rice export

According to Thang T.C. at al. (2014), the total cost of the whole chain of exported rice was 5,993 VND/kg and total profit earned by all actors was 2,711 VND/kg. The cost structure distribution in the whole chain was gradually reduced from farmers (83%), milling and polishing (9%), exporters (4%), dryers (3%), and traders (1%). The structure of profits of the whole chain caputed by different stakeholders decreased gradually from farmers (53%), exporters (30%), millers – polishers (10%), drying agents (4%) and traders (3% ).

Table 2. Costs and profit (per kilogram) of long-grain white rice in export value chain

Source: Thang T.C et al. (2014)

Though farmers take the largest percentage of profit per kilogram of rice product in the value chain, due to their small size (approximately one hectare per household), the income of paddy growers is much lower than other stakeholders. On average, profit from paddy production is about 12 million VND (US$527) per hectare per season. Meanwhile, a trader with total trade volume of 40 M/T per season can earn 25- 30 million VND (US$1,098 – US$1,317) per season, about 60-75 million VND per year.

In recent years, linkage between farmers and enterprises value chain has been improved even though it is slow. According to Thang T.C et al. (2014), approximately 4% of the total rice product at the Mekong River Delta was sold directly to export enterprises. The model of the direct link between farmers and enterprises included two main types: (i) complete value chain where enterprise provides input to paddy growers and procure paddy; (ii) contract farming where enterprise signed contract with farmers to buy paddy. It is noteworthy that farmers who engage in direct linkage with enterprises have a higher profit-cost ratio (36%) than farmers who do not. Simultaneously, the distribution of costs and benefits in the direct linkage was also relatively fairer, in which, paddy growers contribute 58% of total cost of final rice product and they received 62% of total profit. Apart from better income for rice farmers, the value chain of direct linkage between farmers and companies value chain can give a favorable condition for doing traceability of the rice, controlling the pesticide residue and homogeneous level of rice and registering the brand for rice products.

Table 3. Cost - profit distribution of Jasmine rice (5% milled) in the direct linkage between farmers and companies

Source: Thang T.C et al. (2014)

CONCLUSION

The rice value chain in Vietnam is characterized by many middlemen. Profit share per one kilogram of rice received by rice growers among stakeholders in value chain is not small but profit-cost ratio of the growers is much smaller than other actors. In addition, due to small farm sizes, the income earned by farmers are much smaller than other stakeholders in the value chain. The farmers in the complete value chain where they sell directly their paddy to companies get better income. This explains why the development of the complete value chain is strongly demanded in Vietnam as a strategy for assuring income for farmers.

REFERENCES

Thang T.C. et al. (2014), Policies and measures for improve the efficiency of value chain: the cases of rice and pork in Vietnam, Hanoi, Vietnam.

Date submitted: March 30, 2017

Reviewed, edited and uploaded: April 19, 2017