Source: Bureau of Agricultural Finance, Council of Agriculture

http://www.coa.gov.tw/ws.php?id=2506168&print=Y

INTRODUCTION

Agriculture is the foundation of national development. Capital is one of the key successful factors to secure multiple value in food safety, eco-system and cultural scene for sustainable development. However, because agricultural operation is dependent on the weather, diseases, and market price fluctuations, the instability of farmers’ income due to unpredictable weather, diseases, and price fluctuations often lead to uneasy access to commercial bank loans, or incurring a higher capital cost.

The government offers policy loans for agricultural projects in order to take care of farmers/ fishermen, who are considered minority interest groups in terms of economic conditions. Policy loans reduce economic loadings of interest cost farmers/ fishermen hold. Meanwhile, policy loans can invest in the direction of agricultural policy.

Policy loans are implemented by self-funded sources of Farmers’/ Fishermen’ Associations, but with government funding for the interest spread. In addition, Agriculture Credit Guarantee Fund assists those farmers/ fishermen with low credit ratings to minimize credit risk of Farmers’/ Fishermen’ Associations. Meanwhile, low interest loans benefit more than 190,000 farmers and fishermen to easily access the operation fund with a balance NT$75.5 billion in the year 2016.

MAJOR PROCEDURE OF PROJECT LOAN IN 2016

In order to align with agricultural policy goal and industry development, the agricultural project loans have been adjusted as follows in 2016:

Raising Loan Amount Limit

(1) Counseling Food Operator Project Loans

To assist the upgrade of tea quality, the capital expenditure loans allow up to NT$6 million limit, from the previous limit of NT$3 million, for tea production. In addition, for other capital- and technology- intensive production such as mushroom environment-control greenhouse, the capital expenditure loans allow up to NT$12 million limit, from the previous NT$8 million limit. Extra limit of a specific project is also possible with special approval.

(2) Small Landlord Big Tenant Project Loans

To assist small farmers to expand operation scale, the working capital loans allow up to NT$6 million, from the previous NT$1 million. Loans for organizational big tenants could be even higher, up to NT$15 million limit, from the previous NT$5 million.

(3) Upgrading Livestock & Poultry Operator Project Loans

Because of the recent bird flu problems, the policy intends to push traditional egg farms towards more eco-friendly egg production models. The flexibility of project loans will provide incentives to upgrade facilities by special approval.

(4) Forestation

The demand of capital for forestation is mostly for fertilizing and disease prevention. In addition to current capital investment loans of NT$5 million limit, an extra working capital is included with a NT$1 million limit, with a 5-year repayment term.

Release Loan Qualification and Purpose

(1) Young Farmer Entrepreneur Project Loans

In addition to the existing members of Farmers’/ Fishermen’ Associations, more agricultural policy insurees are included, such as members of agricultural production/ sales classes, winners of agricultural prizes, and internships of farms. Moreover, the young farmer entrepreneur project sponsors innovative marketing of agricultural products, particularly via e-commerce platform, and the limitation of operation scale is also released.

(2) Natural Disaster Recovery & Re-farming by Farmers’ Association & Agribusiness Project Loans

Considering the current situation, the food processing operators are included in the project loans, in addition to the previous conditions. However, food processing operators are specifically for local material processors, and for farmers, farmers’ organizations, or agricultural production/sales classes.

(3) Production Sales & R&D for Farmers’ Association & Agribusiness

Because of the new era of e-commerce business, the project loans encourage the establishment of e-commerce platforms and agricultural sales activities via the platform.

Release Loan Repay Terms and Turnover Cash Payment Methods

(1) Agricultural Machine Project Loans

The previous seven years amortized repayment is extended to 10 years in order to meet the current condition of agricultural machine usages. Meanwhile, for outsourced businesses of farming specific to the loan amount under NT$400,000, the repayment can now be extended to seven years duration instead of the prior four years. Moreover, there is the flexibility for other machine working durations regulated by the central related authorities.

(2) Privileged Loans for Agriculture Science Park Entry Project Loan

The project additionally includes the working capital loan with the revolving credit extension and flexible terms. It intends to assist agribusinesses located in the Agricultural Science Park for flexibility of operations.

Simplify and Consolidate Loans

(1) Consolidate previous different loans of farmer operation improvement and agricultural production and sales class members into farmer operation and agricultural production and sales loans.

(2) Terminate the loans for financial improvement because the temporary mission has been done.

Loan Interest Rate Cut and Subsidy Base Adjustment

(1) Because of the recent lowering interest rate by Central Bank, the agricultural policy loans cut 0.21% interest rate and 0.28% subsidy rate in total in 2016, which also refers to other policy loans initiated by the other administrative authorities.

(2) In order to direct more businesses investing in agricultural operation, the interest rate of Production Sales & R&D for Farmers’ Association & Agribusiness Project Loans was cut to 1.68% from prior 2%.

Amend Agricultural Energy Saving & Carbon-emission Reduction

(1) Release the loan qualification, purpose, and duration: Due to the agricultural green-energy policy, agribusinesses which establish green-energy facilities will be included as qualified borrowers. Additionally, biogas energy facilities are allowed to pay via loans. In addition to serving practical needs, loan duration is extended to 10 years from the prior seven years. The authority for special approval flexibility for those facilities with over 10-year durable life is also amended.

(2) Cut loan rate: The loan rate is cut to 1.04%~1.68% in order to provide incentives for biogas facilities.

(3) Raise loan limit: The current 50%~70% of facility investment loans is raised to 90% for more flexibility of higher limit agricultural green-energy facilities.

MANAGEMENT ENFORCEMENT

The agricultural project loans are regulated with specific details of qualification and purpose. Farmers and fishermen should prepare the required documentations with operation proposal to apply loans to the responsible institutions for other approval or rejection. COA has been adjusting related policies and rules in order to fit the concurrent agricultural environment and its dramatic change over time. Farmers and fishermen should be secured to legitimate borrowers of project loans. Thus, the following procedures are managed in rigor.

(1) Raise the management/ supervision levels of Farmers’and Fishermen’ Associations: Agricultural project loans are required to be submitted to the association council to get approved in order to prevent flaws.

(2) Strengthen the external audit: The financial related authorities, Financial Examination Bureau, Financial Supervisory Commission , is responsible for ongoing audit of agricultural project loans and view it as top priority, particularly in auditing some specific loan items.

(3) Restrict the fund payment method: The fund payment methods are strictly regulated in order to clearly track the cash flows. It is only allowed to be paid by bank wires, direct transfers, and/ or non-transferrable double-lined cheques

(4) Tighten the admission of borrower qualifications

In addition to the required documents of farmers’ and fishermen’ applications, the admission is tightened according to the operation proposal regarding the purpose of project loans.

(5) Regulate the loan purpose and supervision method

Project loan makers are regulated to clearly check and record the actual fund use and the proposal purpose after six months of funds awarded. In addition, it is regulated that project stakeholders, including the loan project facilitators, cannot be appointed into the check supervision job.

2016 STATUS OF AGRICULTURAL PROJECT LOANS

COA started to promote agricultural project loans since 1973. There are currently 17 categories for agricultural project loans in working capital of farm household and rehabilitation, covering agriculture, forestry, fisheries, and animal husbandry. Agricultural development loans include 16 projects with low interest rate of 1.5% for development purpose, or 1.25% for rehabilitation purpose.

In addition to taking care of farmers and fishermen as well as promoting agricultural policies, COA budgeted NT$27 billion in 2016 for the following project loans listed in Table 1. The outstanding balance of project loans was NT$75.5 billion by the end of 2016 with more than 191,000 beneficial farmers and fishermen.

Agriculture is vulnerable to weather conditions. For example, natural disaster caused by typhoons is quite common in Taiwan. COA budgeted NT$5 billion low-interest loans for agricultural natural disaster low-rate, 1.04%, loan quota. The balance of low-rate loans for rehabilitation was NT$4.6 billion by the end of 2016, with 4,801 farmers and fishermen borrowers. On the one hand, COA promotes agricultural project loans with the amended rules of borrower qualification, purpose, condition, and loan limit. On the other hand, COA makes sure that project loans fit the right needs and assist application processes of farmers and fishermen in aligning the interest of loan making farmers’ and fishermen’ associations. In 2016, the amount of NT$22.5 billion project loans were issued to 40,000 farmers and fishermen operations and businesses.

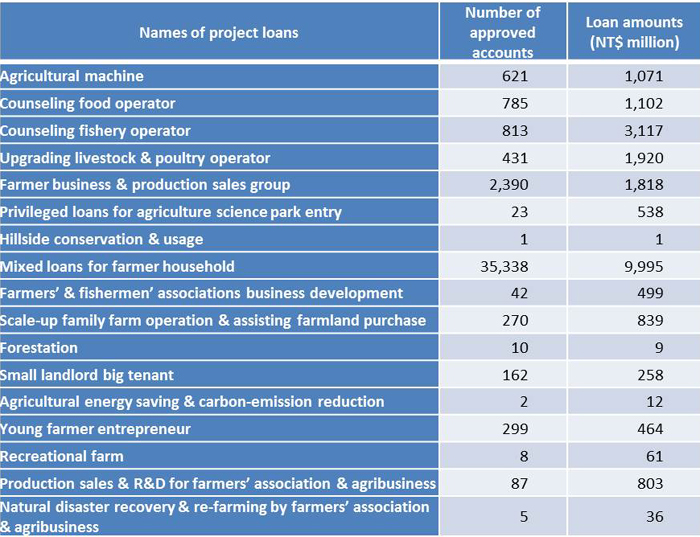

Table 1. 2016 List of Agricultural Project Loans

The most loans have been issued as Mixed Loans for Farmer Household projects, for multi-different purposes. The maximum loans per account is NT$300,000, while these kinds of small loans are mostly used for farm household lives and education. Because inspection of these kinds of small loans is waived, yet the subsidy of interest is still valid, associations would particularly promote such loans to affiliated farmers and fishermen.

As the second major loans, Counseling Fishery Operator projects are issued for marine fisheries (fishing and breeding), land breeding fisheries, recreational fisheries (fishery development as foundations), facilities construction and repair, fishing vessel acquisition and repair, fishing materials, processing facilities and hygiene improvement, and working capital for fishing operations. Because many cases involve large investments in fishing vessels, which are not typically preferred by commercial banks, the feasible way to access funds is to take the policy-oriented project loans.

In recent years, the transformation of new agriculture value-added chain is pushed by the transitional government policy. The production-oriented model is gradually moved to more value-added in processing and distribution activities in the chain. The candidate qualification for loans also extends to agribusinesses in addition to farmers and fishermen in the past.

The Act of “Issuing Agricultural Policy Loans” was amended by including agribusinesses and recreational farms as qualified borrowers, and in particular, also releasing the qualifications and purpose for young farmers. For example, to encourage young farmers, the Young Farmer Entrepreneur project takes care of young people with educational backgrounds in agriculture whose ages are between 18 and 45. The loans aim to motivate young people to commit themselves to farming businesses, with over 80 hours of agricultural training within five years or with practical agricultural jobs. More than loans, COA also selects young farmers from the project to provide further capital/ expenditure assistance in agricultural production and distribution, such as farming material supplies, facilities, greenhouse construction, processing and distribution activities. The limit of this project can normally be up to NT$5 million loan limit with 1.5% interest rate terms. For special project cases counseled by COA, the limit can be raised as high as NT$10 million with zero-interest for rental and 1% interest rate for others, if meeting the scale requirement.

COA started the project loans of Production Sales & R&D for Farmers’ Association & Agribusiness in Oct. 24, 2014.This project extended to agribusinesses with prior limitations to farmers and fishermen. This project helps to support agricultural industry upgrade towards new type of agri-value chain.

Distribution/ sales management and R&D innovations are two kinds for project loans for agribusinesses to develop business operations in farming, forestry, fishery, and husbandry, for various value-added activities in R&D, manufacturing, sales, and/or exporting. The limit can be as high as NT$50 million with a permit of working capital NT$10 million from it. Working capital is allowed as long as three years for farmers, Farmers’ Associations, agricultural production and sales classes. These new agricultural project loans all provide policy implications for upgrading agricultural competitiveness, which are expected to have some effective outcomes years after its promotional efforts.

CONCLUSION

Financial loan is a key to agricultural development. COA continues to promote project loans in alignment with policy and industry development trajectory. To make sure effective project loans fully support agricultural development policy, quite a few of management procedures are detected and amended with rigor inspection regulation in order to secure the loan purposes and prevent flaws. COA will expect to continue meeting future demand of policy in supporting sustainable agricultural development as well as good farmers’ living by utilizing agricultural project loans in coordination with agricultural financial institutions such as Agricultural Bank of Taiwan and the Agricultural Credit Guarantee Fund.

|

Date submitted: April 27, 2017

Reviewed, edited and uploaded: June 9, 2016

|

Taiwan's Performance of Agricultural Policy Loans in 2016

Source: Bureau of Agricultural Finance, Council of Agriculture

http://www.coa.gov.tw/ws.php?id=2506168&print=Y

INTRODUCTION

Agriculture is the foundation of national development. Capital is one of the key successful factors to secure multiple value in food safety, eco-system and cultural scene for sustainable development. However, because agricultural operation is dependent on the weather, diseases, and market price fluctuations, the instability of farmers’ income due to unpredictable weather, diseases, and price fluctuations often lead to uneasy access to commercial bank loans, or incurring a higher capital cost.

The government offers policy loans for agricultural projects in order to take care of farmers/ fishermen, who are considered minority interest groups in terms of economic conditions. Policy loans reduce economic loadings of interest cost farmers/ fishermen hold. Meanwhile, policy loans can invest in the direction of agricultural policy.

Policy loans are implemented by self-funded sources of Farmers’/ Fishermen’ Associations, but with government funding for the interest spread. In addition, Agriculture Credit Guarantee Fund assists those farmers/ fishermen with low credit ratings to minimize credit risk of Farmers’/ Fishermen’ Associations. Meanwhile, low interest loans benefit more than 190,000 farmers and fishermen to easily access the operation fund with a balance NT$75.5 billion in the year 2016.

MAJOR PROCEDURE OF PROJECT LOAN IN 2016

In order to align with agricultural policy goal and industry development, the agricultural project loans have been adjusted as follows in 2016:

Raising Loan Amount Limit

(1) Counseling Food Operator Project Loans

To assist the upgrade of tea quality, the capital expenditure loans allow up to NT$6 million limit, from the previous limit of NT$3 million, for tea production. In addition, for other capital- and technology- intensive production such as mushroom environment-control greenhouse, the capital expenditure loans allow up to NT$12 million limit, from the previous NT$8 million limit. Extra limit of a specific project is also possible with special approval.

(2) Small Landlord Big Tenant Project Loans

To assist small farmers to expand operation scale, the working capital loans allow up to NT$6 million, from the previous NT$1 million. Loans for organizational big tenants could be even higher, up to NT$15 million limit, from the previous NT$5 million.

(3) Upgrading Livestock & Poultry Operator Project Loans

Because of the recent bird flu problems, the policy intends to push traditional egg farms towards more eco-friendly egg production models. The flexibility of project loans will provide incentives to upgrade facilities by special approval.

(4) Forestation

The demand of capital for forestation is mostly for fertilizing and disease prevention. In addition to current capital investment loans of NT$5 million limit, an extra working capital is included with a NT$1 million limit, with a 5-year repayment term.

Release Loan Qualification and Purpose

(1) Young Farmer Entrepreneur Project Loans

In addition to the existing members of Farmers’/ Fishermen’ Associations, more agricultural policy insurees are included, such as members of agricultural production/ sales classes, winners of agricultural prizes, and internships of farms. Moreover, the young farmer entrepreneur project sponsors innovative marketing of agricultural products, particularly via e-commerce platform, and the limitation of operation scale is also released.

(2) Natural Disaster Recovery & Re-farming by Farmers’ Association & Agribusiness Project Loans

Considering the current situation, the food processing operators are included in the project loans, in addition to the previous conditions. However, food processing operators are specifically for local material processors, and for farmers, farmers’ organizations, or agricultural production/sales classes.

(3) Production Sales & R&D for Farmers’ Association & Agribusiness

Because of the new era of e-commerce business, the project loans encourage the establishment of e-commerce platforms and agricultural sales activities via the platform.

Release Loan Repay Terms and Turnover Cash Payment Methods

(1) Agricultural Machine Project Loans

The previous seven years amortized repayment is extended to 10 years in order to meet the current condition of agricultural machine usages. Meanwhile, for outsourced businesses of farming specific to the loan amount under NT$400,000, the repayment can now be extended to seven years duration instead of the prior four years. Moreover, there is the flexibility for other machine working durations regulated by the central related authorities.

(2) Privileged Loans for Agriculture Science Park Entry Project Loan

The project additionally includes the working capital loan with the revolving credit extension and flexible terms. It intends to assist agribusinesses located in the Agricultural Science Park for flexibility of operations.

Simplify and Consolidate Loans

(1) Consolidate previous different loans of farmer operation improvement and agricultural production and sales class members into farmer operation and agricultural production and sales loans.

(2) Terminate the loans for financial improvement because the temporary mission has been done.

Loan Interest Rate Cut and Subsidy Base Adjustment

(1) Because of the recent lowering interest rate by Central Bank, the agricultural policy loans cut 0.21% interest rate and 0.28% subsidy rate in total in 2016, which also refers to other policy loans initiated by the other administrative authorities.

(2) In order to direct more businesses investing in agricultural operation, the interest rate of Production Sales & R&D for Farmers’ Association & Agribusiness Project Loans was cut to 1.68% from prior 2%.

Amend Agricultural Energy Saving & Carbon-emission Reduction

(1) Release the loan qualification, purpose, and duration: Due to the agricultural green-energy policy, agribusinesses which establish green-energy facilities will be included as qualified borrowers. Additionally, biogas energy facilities are allowed to pay via loans. In addition to serving practical needs, loan duration is extended to 10 years from the prior seven years. The authority for special approval flexibility for those facilities with over 10-year durable life is also amended.

(2) Cut loan rate: The loan rate is cut to 1.04%~1.68% in order to provide incentives for biogas facilities.

(3) Raise loan limit: The current 50%~70% of facility investment loans is raised to 90% for more flexibility of higher limit agricultural green-energy facilities.

MANAGEMENT ENFORCEMENT

The agricultural project loans are regulated with specific details of qualification and purpose. Farmers and fishermen should prepare the required documentations with operation proposal to apply loans to the responsible institutions for other approval or rejection. COA has been adjusting related policies and rules in order to fit the concurrent agricultural environment and its dramatic change over time. Farmers and fishermen should be secured to legitimate borrowers of project loans. Thus, the following procedures are managed in rigor.

(1) Raise the management/ supervision levels of Farmers’and Fishermen’ Associations: Agricultural project loans are required to be submitted to the association council to get approved in order to prevent flaws.

(2) Strengthen the external audit: The financial related authorities, Financial Examination Bureau, Financial Supervisory Commission , is responsible for ongoing audit of agricultural project loans and view it as top priority, particularly in auditing some specific loan items.

(3) Restrict the fund payment method: The fund payment methods are strictly regulated in order to clearly track the cash flows. It is only allowed to be paid by bank wires, direct transfers, and/ or non-transferrable double-lined cheques

(4) Tighten the admission of borrower qualifications

In addition to the required documents of farmers’ and fishermen’ applications, the admission is tightened according to the operation proposal regarding the purpose of project loans.

(5) Regulate the loan purpose and supervision method

Project loan makers are regulated to clearly check and record the actual fund use and the proposal purpose after six months of funds awarded. In addition, it is regulated that project stakeholders, including the loan project facilitators, cannot be appointed into the check supervision job.

2016 STATUS OF AGRICULTURAL PROJECT LOANS

COA started to promote agricultural project loans since 1973. There are currently 17 categories for agricultural project loans in working capital of farm household and rehabilitation, covering agriculture, forestry, fisheries, and animal husbandry. Agricultural development loans include 16 projects with low interest rate of 1.5% for development purpose, or 1.25% for rehabilitation purpose.

In addition to taking care of farmers and fishermen as well as promoting agricultural policies, COA budgeted NT$27 billion in 2016 for the following project loans listed in Table 1. The outstanding balance of project loans was NT$75.5 billion by the end of 2016 with more than 191,000 beneficial farmers and fishermen.

Agriculture is vulnerable to weather conditions. For example, natural disaster caused by typhoons is quite common in Taiwan. COA budgeted NT$5 billion low-interest loans for agricultural natural disaster low-rate, 1.04%, loan quota. The balance of low-rate loans for rehabilitation was NT$4.6 billion by the end of 2016, with 4,801 farmers and fishermen borrowers. On the one hand, COA promotes agricultural project loans with the amended rules of borrower qualification, purpose, condition, and loan limit. On the other hand, COA makes sure that project loans fit the right needs and assist application processes of farmers and fishermen in aligning the interest of loan making farmers’ and fishermen’ associations. In 2016, the amount of NT$22.5 billion project loans were issued to 40,000 farmers and fishermen operations and businesses.

Table 1. 2016 List of Agricultural Project Loans

The most loans have been issued as Mixed Loans for Farmer Household projects, for multi-different purposes. The maximum loans per account is NT$300,000, while these kinds of small loans are mostly used for farm household lives and education. Because inspection of these kinds of small loans is waived, yet the subsidy of interest is still valid, associations would particularly promote such loans to affiliated farmers and fishermen.

As the second major loans, Counseling Fishery Operator projects are issued for marine fisheries (fishing and breeding), land breeding fisheries, recreational fisheries (fishery development as foundations), facilities construction and repair, fishing vessel acquisition and repair, fishing materials, processing facilities and hygiene improvement, and working capital for fishing operations. Because many cases involve large investments in fishing vessels, which are not typically preferred by commercial banks, the feasible way to access funds is to take the policy-oriented project loans.

In recent years, the transformation of new agriculture value-added chain is pushed by the transitional government policy. The production-oriented model is gradually moved to more value-added in processing and distribution activities in the chain. The candidate qualification for loans also extends to agribusinesses in addition to farmers and fishermen in the past.

The Act of “Issuing Agricultural Policy Loans” was amended by including agribusinesses and recreational farms as qualified borrowers, and in particular, also releasing the qualifications and purpose for young farmers. For example, to encourage young farmers, the Young Farmer Entrepreneur project takes care of young people with educational backgrounds in agriculture whose ages are between 18 and 45. The loans aim to motivate young people to commit themselves to farming businesses, with over 80 hours of agricultural training within five years or with practical agricultural jobs. More than loans, COA also selects young farmers from the project to provide further capital/ expenditure assistance in agricultural production and distribution, such as farming material supplies, facilities, greenhouse construction, processing and distribution activities. The limit of this project can normally be up to NT$5 million loan limit with 1.5% interest rate terms. For special project cases counseled by COA, the limit can be raised as high as NT$10 million with zero-interest for rental and 1% interest rate for others, if meeting the scale requirement.

COA started the project loans of Production Sales & R&D for Farmers’ Association & Agribusiness in Oct. 24, 2014.This project extended to agribusinesses with prior limitations to farmers and fishermen. This project helps to support agricultural industry upgrade towards new type of agri-value chain.

Distribution/ sales management and R&D innovations are two kinds for project loans for agribusinesses to develop business operations in farming, forestry, fishery, and husbandry, for various value-added activities in R&D, manufacturing, sales, and/or exporting. The limit can be as high as NT$50 million with a permit of working capital NT$10 million from it. Working capital is allowed as long as three years for farmers, Farmers’ Associations, agricultural production and sales classes. These new agricultural project loans all provide policy implications for upgrading agricultural competitiveness, which are expected to have some effective outcomes years after its promotional efforts.

CONCLUSION

Financial loan is a key to agricultural development. COA continues to promote project loans in alignment with policy and industry development trajectory. To make sure effective project loans fully support agricultural development policy, quite a few of management procedures are detected and amended with rigor inspection regulation in order to secure the loan purposes and prevent flaws. COA will expect to continue meeting future demand of policy in supporting sustainable agricultural development as well as good farmers’ living by utilizing agricultural project loans in coordination with agricultural financial institutions such as Agricultural Bank of Taiwan and the Agricultural Credit Guarantee Fund.

Date submitted: April 27, 2017

Reviewed, edited and uploaded: June 9, 2016