ABSTRACT

This paper reviews theories, current conditions, and barriers of liquidization and concentration of farmland in Japan and discusses perspectives on further research. First, to determine the economic conditions required to promote farmland liquidity, this paper formulates the farmland supply-demand behavior of individual farm households. However, various real-world constraints, such as farmland systems, transaction costs, and expectation of land conversion, are not reflected. Secondly, this paper also discusses why and how these constraining factors may inhibit liquidization of farmland. After identifying the reasons that farmland is hardly traded in the market, farmland bank program is quantitatively examined the extent to which plot exchange can consolidate fragmented farmland by simulation. Finally, concluding remark is provided from the viewpoint of an international perspective.

Keywords: land market, farmland consolidation, transaction cost, thin market, plot exchange, market design

INTRODUCTION

A major characteristic of Japanese agricultural landownership is that farmers own small, geographically scattered fields. Owning of scattered fields impedes use of machinery and inhibits efficient production (Kawasaki, 2010; Kawasaki, 2011). To improve productivity and maintain or enhance agricultural production capacity, concentrating farmland ownership in the hands of those who actively farm, as well as consolidating neighboring lots into farmland complexes, are necessary.

Since the establishment of the Agricultural Basic Act in 1961, farmland consolidation has always been a main issue of Japan’s agricultural policy. However, though nearly half a century has passed, no dramatic improvements to the agricultural structure have been observed. Although the World Census of Agriculture and Forestry shows that the average (of all farm households) area of arable land managed by a farm household increased from 0.98 ha in 1960 to 2.30 ha in 2010, the scale of ownership is still very small. Such a phenomenon is commonly observed in Asia (e.g., China, India, Taiwan and Vietnam), where small-scale farming persists. Thus, the struggling experience of Japan provides important lessons for rapidly growing economies―especially in Asia, which faces similar agro-economic land conditions.

This paper reviews theories, current conditions, and barriers of liquidization and concentration of farmland in Japan and discusses perspectives on further research. The rest of this paper is organized as follows. First, to determine the economic conditions required to promote farmland liquidity, Section 2 formulates the farmland supply-demand behavior of individual farm households into simple patterns while focusing on the differences in costs and profitability among farmers as well as the expanding off-farm employment opportunities and rising wages associated therewith as factors that will promote farmland liquidity, and organizes the key issues obtained. In the formulation in Section 2, however, various real-world constraints, such as farmland systems, transaction costs, and expectation of land conversion, are not reflected. So, Section 2 also discusses why and how these constraining factors may inhibit liquidization of farmland. After identifying the reasons that farmland is hardly traded in the market, the section 3 organizes on farmland consolidation policies for young generation in Japan. Considering farmland bank program, the section 4 quantitatively examines the extent to which plot exchange can consolidate fragmented farmland by simulation. The section 5 provides concluding remark from the viewpoint of an international perspective.

How has the Agricultural Economics Seen the Farmland Market?

Perfectly competitive farmland market

The farmland market is a theme that has been studied for a long time, so there is a large accumulation of research results5. Then, what kind of farmer behavior and farmland market are assumed in such agro-economic studies?

The formulation by Deininger and Jin (2005) assumes that farmer .bmp) owns farmland

owns farmland  as the initial endowment, and the labor endowment

as the initial endowment, and the labor endowment  is allocated to farming

is allocated to farming  and off-farm employment

and off-farm employment  . The farmer obtains income from both farming and off-farm employment. The volume of farm production of each farm household is determined by the common production function

. The farmer obtains income from both farming and off-farm employment. The volume of farm production of each farm household is determined by the common production function .bmp) , which satisfies regular characteristics, multiplied by the individual productivity

, which satisfies regular characteristics, multiplied by the individual productivity  . Assuming also the exogenous factors; sales price of farm products, off-farm employment wage, and farm rent per unit area, as

. Assuming also the exogenous factors; sales price of farm products, off-farm employment wage, and farm rent per unit area, as  , respectively, the profit maximization problem of each farm household can be expressed as follows2:

, respectively, the profit maximization problem of each farm household can be expressed as follows2:

Each farmer should decide his optimal farm labor input  and management scale

and management scale  to satisfy the formula (1). The first-order conditions for optimization are expressed as equation (2) and (3):

to satisfy the formula (1). The first-order conditions for optimization are expressed as equation (2) and (3):

The difference between the optimal management scale .bmp) obtained above and the initial endowment

obtained above and the initial endowment  is the amount of farmland demand (supply) of each farmer. By adding up the farmland demand (supply) of individual farmers, total farmland demand (supply) in the relevant farmland market can be obtained. Then

is the amount of farmland demand (supply) of each farmer. By adding up the farmland demand (supply) of individual farmers, total farmland demand (supply) in the relevant farmland market can be obtained. Then  should be set at the level that ensures a balance between the supply and demand.

should be set at the level that ensures a balance between the supply and demand.

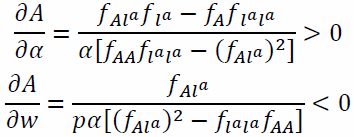

The results of total differentiation of equation (2) and (3) with respect to  and w are as follows:

and w are as follows:

According to .bmp) , when farmers’ productivity rises, their optimal management scale A* expands. In response, they increase borrowing, causing an upward shift of the aggregate demand curve of the market. As a result, r* also rises. Farm households with low productivity then become able to obtain more income from farm rent than from farming, and therefore they lease their farmland to others. This results in an outflow of farmland from farmers with low productivity and concentration into those with high productivity. According to

, when farmers’ productivity rises, their optimal management scale A* expands. In response, they increase borrowing, causing an upward shift of the aggregate demand curve of the market. As a result, r* also rises. Farm households with low productivity then become able to obtain more income from farm rent than from farming, and therefore they lease their farmland to others. This results in an outflow of farmland from farmers with low productivity and concentration into those with high productivity. According to .bmp) , on the other hand, a rise in off-farm wage increases opportunity cost, resulting in a smaller optimal management scale, This means that farmers engage in off-farm employment (as part-time farmers) and lease their farmland to others. Consequently, supply of farmland increases while the equilibrium farm rent declines in the relevant farmland market.

, on the other hand, a rise in off-farm wage increases opportunity cost, resulting in a smaller optimal management scale, This means that farmers engage in off-farm employment (as part-time farmers) and lease their farmland to others. Consequently, supply of farmland increases while the equilibrium farm rent declines in the relevant farmland market.

Farmland market in the real world

Contrary to expectations of theoretical models, farmland consolidation has shown little progress and most farmers continue inefficient, unprofitable small-scale management. Japanese agricultural economics researchers have presented various key points to explain this reality based on detailed on-site observation, from standpoints far removed from theories. This paper discusses only on the points that are directly relevant to the concept of a farmland market.

Characteristics of farmland as a good

Before entering discussions on specific points, characteristics of farmland as a good that is traded in a market, namely the farmland market, should be clarified, because as stated below, the peculiarities of farmland as a good may inhibit it being efficiently traded in the market.

First, farmland cannot be moved (locational immovability). Second, consolidated farmland lots have higher use efficiency than independent lots of the same area (economy of consolidation). Third, farmland is unique in that only a single form of farmland exists in a certain location. Fourth, since farmland cannot be easily increased (except by reclamation), its supply is inelastic. Fifth, devastated farmland has externalities because such farmland is vulnerable to damage from diseases, insects and animals, which are likely to also harm neighboring farmland. Moreover, since farmland is immovable, presence of a devastated field inhibits other farmers from connecting with such a field. Sixth, in a rural community, farmland not only constitutes an element for production but also serves as a symbolic or political good that determines the social order of each household. In short, farmland is a good that is greatly influenced by the household norms (succession of family name, family business, family industry) or rural community norms (stigma against releasing farmland, feeling of resistance to entry of outsiders).

Gap between the image of a perfectly competitive farmland market and the reality

The theoretical model implicitly contains at least the five hypotheses described below. The gap between theory and reality arises because these hypotheses are not satisfied in reality.

The first hypothesis is that farmers behave based on their interest in profit maximization. While the theoretical model assumes the pursuit of maximization of profits, farmland is actually a good that is greatly influenced by household norms or rural community norms. It not only constitutes a production good but also serve as a consumption good that receives benefits from succession of the household business/industry or farming itself. Thus, farmers do not always behave for the purpose of maximizing their profits.

The second hypothesis is that a farmland market should be competitive. Since farmland is by nature immovable, trading of farmland is geographically constrained. Therefore, the farmland market tends to be thin, inevitably causing an oligopoly on both the lessor and lessee sides. Moreover, under the recent circumstances in which only a few borrowers exist due to farmers’ aging and the inclination to farm part-time, the amount of farm rent cannot be competitively decided, which may lead to an undersupply of farmland.

The third hypothesis is that farm rent is determined at a level that ensures balance between supply and demand. The standard model assumes that farm rent functions to adjust the imbalance between supply and demand in farmland trading. In reality, however, farm rent is decided through negotiation between the lessor and the lessee in view of the standard farm rent (reference farm rent) determined by accumulation of costs (the land residual technique) as the reference point. If the standard farm rent is different from the level of supply-demand balance, there should naturally be an imbalance between supply and demand.

The fourth is that there are no institutional strains surrounding farmland. While the standard model assumes no institutional strains regarding farmland, in reality there are several institutional problems, such as insufficient regulations of farmland conversion, which is associated with expectation of land conversion (Godo, 1998), and problems with the farmland taxation system (inheritance tax moratorium, etc.). These problems help increase reservation demands of lessors, and thus decrease supply of farmland, resulting consequently in a delay in the progress of farmland consolidation.

The fifth hypothesis is that there are no transaction costs. In reality, however, in trading farmland, various costs arise, including the cost of searching for a suitable trading partner or farm plot, the cost of examining the farmland conditions, the cost of negotiating trading conditions, and the time and cost required for institutional procedures (contractual cost).

Besides the above five hypotheses, various policies regarding pricing, income and production adjustment are pointed out to as factors affecting farmers’ behavior and farmland supply/demand, and have inhibited farmland consolidation.

Policies regarding farmland consolidation in Japan[3]

The majority of Japanese farmers are small-scale, land-owning farmers. This structure originated from the agrarian land reform, a policy implemented after World War II to release farmland to cultivators. Before the war in Japan, about a half of all farmland was cultivated by poor, small tenant farmers, and their precarious footing was considered to be the cause of many of the social problems facing farming villages. After the land reform, the ratio of tenanted land held by landowners decreased to 10%. Thus, the agrarian land reform generated so-called “postwar land-owning farmers” who own 1 hectare of farmland each (in all prefectures except Hokkaido), constituting nearly homogenous farming villages to start the postwar farming. To maintain this new farmland ownership structure and secure the rights of cultivators, the Agricultural Land Act was established in 1952 which imposes strict regulations concerning farmland, including restrictions on farmland ownership and control of farm rent. The Agricultural Land Act strictly protects the rights of tenant farmers and restricts landowners from terminating land lease contracts without consent of their tenant farmers. The Act also limits acquisition of farmland to those who actually cultivate the land. Permission by the agricultural committee set for each municipality became necessary for trading of farmland to ensure democratic decision-making.

After the Agricultural Basic Act was enacted in 1960 for the purpose of improving agricultural productivity and expanding the farming scale to increase income, regulations concerning farmland leasing were gradually eased. More significantly, the Agricultural Land Use Promotion Program was launched in 1975, which covered nearly all (97%) farmland lease transactions. The Agricultural Land Use Promotion Program was developed into the Agricultural Land Use Promotion Act in 1980, which was revised and renamed the Act on Promotion of Improvement of Agricultural Management Foundation in 1993, and has undergone several modifications up to today.

The Act on Promotion of Improvement of Agricultural Management Foundation in 1993 declares as its objective the development of efficient and stable farm management. Specifically, the Act stipulates prioritized support for core farmers such as certified farmers and some specific community farming organizations. Through the Act on Promotion of Improvement of Agricultural Management Foundation, the share of farmland operated by core farmers increased from 20% in 1996 to 42% in 2006; nonetheless, the pace of farmland concentration has been unsatisfactory.

By the way, farms on the 3ha scale would expand to at least 15ha has and costs would be significantly reduced. Figure 1 shows the production costs of rice by farm size. The total production cost for farm operators who cultivate less than a half hectare is more than double of those cultivating more than 15ha. In order to promote farmland consolidation, the Japanese government has initiated new policy such as “Local Plan of Farmers and Farmlands” and the Intermediate and Conservation Organization for Farmlands”. The purpose of these policies is to transfer the rights of farmlands from farmers in the next generation.

.png)

Figure 1. Production costs of rice by farm size in 2012 (Non-Hokkaido)

Source: Rice Production Cost Statistics, Ministry of Agriculture, Forestry and Fisheries

Market design[4] for farmland consolidation

Why can’t farmland complexes be established through plot exchange?

Actually, some political measures[5] have been taken, though they have not caused a major trend of farmland consolidation[6]. There are roughly two structural reasons for this.

The first is that since land cannot be moved, it can be exchanged with a very limited number of exchange partners. Imagine the following situation. A farmer has a farmland complex consisting of several connected plots (main farm) and a distant plot (outlying field). The farmer wishes to exchange plots with another farmer so as to turn the outlying field into a plot next to the main farm. Because the purpose of the exchange is to turn the outlying land into a plot next to the main farm, the exchange can be performed only with farmers who have plots neighboring the main farm. In Figure 2, for example, Farmer 2 intends to exchange his two outlying fields (C2 and F1) for plots next to his main farm at the bottom left, but only Farmer 3 is available for such an exchange.

The second reason is that the “double coincidence of wants” can hardly occur. To reach an agreement on a spontaneous exchange, there must be a situation where you want a plot belonging to another farmer and the other farmer also wants your plot. This situation, where the desires of both sides match, is called a “double coincidence of wants.”[7] It is extremely rare to find such an exchange partner from among the naturally small number of candidates.

Proposing the cycle trading method

Is there any way to enhance the rate of farmland consolidation? The key is to ease the constraint of the double coincidence of wants. In an individual, direct exchange, since farmers exchange plots on a one-to-one basis, the double coincidence of wants needs to be directly satisfied. In the case of Figure 2, for example, Farmer 2 cannot establish the double coincidence of wants with any other farmers and therefore cannot exchange plots.

.png)

Figure 2. Schematic diagram of fragmented farmland

Trading cycle method

Meanwhile, if many farmers join the exchange at the same time and form a “cycle of exchange,” plot exchange will become available even though the double coincidence of wants is not directly satisfied. In the case of Figure 2, Farmer 2 wants Farmer 3’s plot B6, Farmer 3 wants Farmer 4’s plot F7, and Farmer 4 wants Farmer 2’s plot F1. These relationships are described as a cycle of 2→ 3→ 4→ 2. In this cycle, Farmer 2 and Farmer 3 first exchange F1 and B6, and then Farmer 3 and Farmer 4 exchange F1 and F7. In this way, all parties can obtain the plots they want (Figure 3). Generally, exchange is possible if a cycle can be formed by describing each plot owner pointing at the owner of the plot he wants. This is based on the idea used in the algorithm called Top Trading Cycle (TTC) by Shapley and Scarf (1974). An advantage of this method is that it enables exchange with a party with whom the double coincidence of wants does not occur. The key point is that by forming a trading cycle consisting of many farmers and exchanging plots at the same time within the cycle, the participating farmers are guaranteed to obtain the plots connected to their main farm from other farmers. Because of this, farmers can agree on releasing their plots to other farmers with whom the double coincidence of wants does not exist.

.png)

Figure 3. Example of trading cycle method(2→3→4→2)

Simulation of the trading cycle method

Arimoto, Nakajima and Tomita (2014) confirmed the effectiveness of the cycle trading method by conducting a simulation. In the simulation, farmers declare to a mediator such as an agricultural cooperative the outlying fields they wish to exchange with other plots, to combine with their main farm to form a farmland complex, and the mediator redistributes the gathered outlying fields to the new owners. Specifically, it is a repeated sequence of creating a cycle in which each farmer participates with one of the plots they have submitted and redistributing the plots within the cycle[8]. Creating exchange cycles and deciding the redistribution patterns can be performed mechanically if the outlying fields for exchange and the main farms for consolidation are declared in advance. In the simulation, as conducted for the individual, direct method, based on the randomly created 10,000 patterns of farmland layout, 56 patterns of exchange were conducted by varying the farmers’ participation scenario or the algorithm combinations, and their performance was examined.

Performance of the trading cycle method

The results show that similar to the case of individual, direct exchange, performance depends strongly on the rate of participation in the exchange. With participation of 25% of the farmers of the village, the consolidation rate is less than 1%. With the participation of 50%, the consolidation rate rises to between 9 and 11%, depending on the algorithm, which is over double the performance of the individual, direct exchange. With 100% participation, nearly perfect consolidation can be achieved in some algorithms, reaching a consolidation rate between 62 and 97%.

The simulation results above demonstrate that the trading cycle method can achieve a significantly higher consolidation rate than individual, direct exchange. It is common for both methods, however, that the final performance depends strongly on the number of farm households that participate in the exchange and therefore the key is to invite as many participants as possible to the exchange.

Proposing the cycle trading method

Now, how should exchange based on the trading cycle method be carried out? Since the key to successful cycle trading is to have as many farmers as possible exchange their plots at one time, it is necessary to set up an opportunity for such simultaneous exchange. A possible method is that a mediator such as an agricultural committee or agricultural cooperative calls for participation in a simultaneous exchange and redistributes the submitted outlying fields to the participants.

To implement the cycle trading-based exchange, the challenges below need to be overcome.

-

To facilitate smooth plot exchange, properties of each plot, including area, soil type, shape, and adjacent roads, must be accurately measured to ensure monetary equivalence of the subject plots. For this, introduction of an objective and transparent system for land valuation and settlement money calculation becomes necessary.

-

If plot exchange is conducted periodically, the period during which a farmer cultivates the same plot becomes shorter, which may undermine the incentive for investment in farmland (problem with beneficial expenses). It is therefore necessary to establish clear rules regarding the range and calculation method of beneficial expenses, which will facilitate reimbursement of beneficial expenses.

-

Organizational resources allocation associated with group decision-making, like the cycle trading-based exchange, is more likely to generate conflicts between farmers than market resource allocation, which is based on individual, decentralized decision-making. This makes consensus-building rather difficult. In the past, each village’s innate adjustment function has worked effectively in consensus-building. As we cannot expect such a function to work in the future, it is necessary to rely on an external facilitator. Future discussions will therefore focus on who will serve as the facilitator or how such a facilitator will be developed.

CONCLUSION

Agro-economic studies concerning farmland consolidation in Japan have developed discussions on a perfectly competitive farmland market while presenting various findings based on a more realistic view of farmland market according to in-depth reality analysis. To bridge these two approaches, analysis of Japanese farmland market should pay attention to the following: (1) Since profit maximization is not always the behavioral principle of farmers, analysis should be conducted in a framework taking into consideration rural community norms, etc. (2) The peculiarities of farmland as a good may cause localization of market where oligopoly is likely to occur. (3) In reality, trading of farmland involves costs for searching and negotiation. Concerning the trading costs of (3), both theoretical and empirical studies have been accumulated, while future development is expected for (1) and (2).

From view point of international perspective, as to the studies concerning farmland market, the approach to identify and theorize a more realistic image of a farmland market will continue to be necessary. At the same time, it is also important to build consensus on the degree of generality or impact of the findings that have been presented. To this end, it is crucial to share and theorize the findings obtained in case studies and conduct quantitative analysis using highly representative micro-data with a large sample size, so as to raise the evidence level. Econometric techniques, such as regression analysis, are effective in describing or presenting the reality.

REFERENCES

Arimoto, Y. and Nakajima, S. 2013. Farmland Concentration, Consolidation and the Land Market, Journal of Rural Economics, 85(2): 70-79. (in Japanese).

Arimoto, Y., Nakajima, S. and Tomita, K. 2014. Farmland Consolidation by Plot Exchange: A Simulation-based Approach, Journal of Rural Economics, 86(3): 193-206. (in Japanese).

Deininger, K. 1995. Collective Agricultural Production: A Solution for Transition Economics. World Development, Vol. 23 (8): 1317-1334.

Godo, Y. 1998. A Statistical Description of the Concentration and Conversion of Farmland, Japanese Journal of Farm Management, 34(1): 62-71. (in Japanese).

Kawasaki, K. 2010. The Costs and Benefits of Land Fragmentation of Rice Farms in Japan, Australian Journal of Agricultural and Resource Economics, 54(4): 509-526.

Kawasaki, K. 2011. The Impact of Land Fragmentation on Rice Production Cost and Input Use, The Japanese Journal of Rural Economics, 13: 1-14.

Martini, R. and Kimura, S. 2009. Evaluation of Agricultural Policy Reforms in Japan, Paris: OECD.

Otsuka, K. 2007. Efficiency and Equity Effects of Land Markets, in R. E. Evenson and P. Pingali, eds. Handbook of Agricultural Economics, Vol.3: 2671-2703.

Shapley, L. and Scarf, H. 1974. On Cores and Indivisibility, Journal of Mathematical Economics, 1(1): 23-37.

Tanaka, T. 2007. Resource Allocation with Spatial Externalities: Experiments on Land Consolidation, The B.E. Journal of Economic Analysis & Policy, 7(1): Article 7.

Teruoka, S. 2008. Agriculture in the Modernization of Japan (1850-2000). Manohar, New Delhi.

Vulkan, N., Roth, A. E. and Neeman, Z. 2013. The Handbook of Market Design, Oxford University Press.

[1] The literature of the farmland market, see Arimoto and Nakajima (2013) and Otsuka (2007).

[2] Since this formulation includes off-farm income in the second term, there is no problem with considering it as the income maximization problem for part-time farmers.

[3] Summaries of agriculture in Japan, see Martini and Kimura (2009) and Teruoka (2008).

[4] For an explanation of the Top Trading Cycle (TTC), refer to Vulkan, Roth and Neeman (2013). The literature applying market design to farmland consolidation, see Tanaka (2008).

[5] According to Kawasaki (2010), several land consolidation measures have been implemented in Japan. One is called kanchi and is linked to the land improvement schemes of plot reshaping, plot size expansion, drainage and irrigation development, and road building. On the other hand, there is a measure which is not linked to land improvement. Under this program, called kokan bungo, farmers exchange plots without changing the plot size or shape.

[6] According to Martini and Kimura (2009), ‘a survey of 202 core farmers outside Hokkaido in 2007 found that core farmers cultivate on average 28.5 plots with average plot size of 0.52ha. The share of large plots of more than 2ha was 26.7%.’

[7] It is similarly true for goods other than farmland that the double coincidence of wants makes trading difficult. Generally, this friction is eliminated by money mediating transactions.

[8] To maximize the farmland consolidation rate of a village, distributing all the submitted exchangeable plots at one time is more desirable than following this sequential algorithm. Because it was difficult to find an algorithm that enables optimal distribution, this sequential algorithm was adopted as the second-best approach to conduct the simulation.

|

Submitted as a resource paper for the FFTC-MARDI International Seminar on Cultivating the Young Generation of Farmers with Farmland Policy Implications, May 25-29, MARDI, Serdang, Selangor, Malaysia |

Land Concentration and Land Market in Japan: An International Perspective

ABSTRACT

This paper reviews theories, current conditions, and barriers of liquidization and concentration of farmland in Japan and discusses perspectives on further research. First, to determine the economic conditions required to promote farmland liquidity, this paper formulates the farmland supply-demand behavior of individual farm households. However, various real-world constraints, such as farmland systems, transaction costs, and expectation of land conversion, are not reflected. Secondly, this paper also discusses why and how these constraining factors may inhibit liquidization of farmland. After identifying the reasons that farmland is hardly traded in the market, farmland bank program is quantitatively examined the extent to which plot exchange can consolidate fragmented farmland by simulation. Finally, concluding remark is provided from the viewpoint of an international perspective.

Keywords: land market, farmland consolidation, transaction cost, thin market, plot exchange, market design

INTRODUCTION

A major characteristic of Japanese agricultural landownership is that farmers own small, geographically scattered fields. Owning of scattered fields impedes use of machinery and inhibits efficient production (Kawasaki, 2010; Kawasaki, 2011). To improve productivity and maintain or enhance agricultural production capacity, concentrating farmland ownership in the hands of those who actively farm, as well as consolidating neighboring lots into farmland complexes, are necessary.

Since the establishment of the Agricultural Basic Act in 1961, farmland consolidation has always been a main issue of Japan’s agricultural policy. However, though nearly half a century has passed, no dramatic improvements to the agricultural structure have been observed. Although the World Census of Agriculture and Forestry shows that the average (of all farm households) area of arable land managed by a farm household increased from 0.98 ha in 1960 to 2.30 ha in 2010, the scale of ownership is still very small. Such a phenomenon is commonly observed in Asia (e.g., China, India, Taiwan and Vietnam), where small-scale farming persists. Thus, the struggling experience of Japan provides important lessons for rapidly growing economies―especially in Asia, which faces similar agro-economic land conditions.

This paper reviews theories, current conditions, and barriers of liquidization and concentration of farmland in Japan and discusses perspectives on further research. The rest of this paper is organized as follows. First, to determine the economic conditions required to promote farmland liquidity, Section 2 formulates the farmland supply-demand behavior of individual farm households into simple patterns while focusing on the differences in costs and profitability among farmers as well as the expanding off-farm employment opportunities and rising wages associated therewith as factors that will promote farmland liquidity, and organizes the key issues obtained. In the formulation in Section 2, however, various real-world constraints, such as farmland systems, transaction costs, and expectation of land conversion, are not reflected. So, Section 2 also discusses why and how these constraining factors may inhibit liquidization of farmland. After identifying the reasons that farmland is hardly traded in the market, the section 3 organizes on farmland consolidation policies for young generation in Japan. Considering farmland bank program, the section 4 quantitatively examines the extent to which plot exchange can consolidate fragmented farmland by simulation. The section 5 provides concluding remark from the viewpoint of an international perspective.

How has the Agricultural Economics Seen the Farmland Market?

Perfectly competitive farmland market

The farmland market is a theme that has been studied for a long time, so there is a large accumulation of research results5. Then, what kind of farmer behavior and farmland market are assumed in such agro-economic studies?

The formulation by Deininger and Jin (2005) assumes that farmer.bmp) owns farmland

owns farmland  as the initial endowment, and the labor endowment

as the initial endowment, and the labor endowment  is allocated to farming

is allocated to farming  and off-farm employment

and off-farm employment  . The farmer obtains income from both farming and off-farm employment. The volume of farm production of each farm household is determined by the common production function

. The farmer obtains income from both farming and off-farm employment. The volume of farm production of each farm household is determined by the common production function .bmp) , which satisfies regular characteristics, multiplied by the individual productivity

, which satisfies regular characteristics, multiplied by the individual productivity  . Assuming also the exogenous factors; sales price of farm products, off-farm employment wage, and farm rent per unit area, as

. Assuming also the exogenous factors; sales price of farm products, off-farm employment wage, and farm rent per unit area, as  , respectively, the profit maximization problem of each farm household can be expressed as follows2:

, respectively, the profit maximization problem of each farm household can be expressed as follows2:

Each farmer should decide his optimal farm labor input and management scale

and management scale  to satisfy the formula (1). The first-order conditions for optimization are expressed as equation (2) and (3):

to satisfy the formula (1). The first-order conditions for optimization are expressed as equation (2) and (3):

The difference between the optimal management scale.bmp) obtained above and the initial endowment

obtained above and the initial endowment  is the amount of farmland demand (supply) of each farmer. By adding up the farmland demand (supply) of individual farmers, total farmland demand (supply) in the relevant farmland market can be obtained. Then

is the amount of farmland demand (supply) of each farmer. By adding up the farmland demand (supply) of individual farmers, total farmland demand (supply) in the relevant farmland market can be obtained. Then  should be set at the level that ensures a balance between the supply and demand.

should be set at the level that ensures a balance between the supply and demand.

The results of total differentiation of equation (2) and (3) with respect to and w are as follows:

and w are as follows:

According to.bmp) , when farmers’ productivity rises, their optimal management scale A* expands. In response, they increase borrowing, causing an upward shift of the aggregate demand curve of the market. As a result, r* also rises. Farm households with low productivity then become able to obtain more income from farm rent than from farming, and therefore they lease their farmland to others. This results in an outflow of farmland from farmers with low productivity and concentration into those with high productivity. According to

, when farmers’ productivity rises, their optimal management scale A* expands. In response, they increase borrowing, causing an upward shift of the aggregate demand curve of the market. As a result, r* also rises. Farm households with low productivity then become able to obtain more income from farm rent than from farming, and therefore they lease their farmland to others. This results in an outflow of farmland from farmers with low productivity and concentration into those with high productivity. According to .bmp) , on the other hand, a rise in off-farm wage increases opportunity cost, resulting in a smaller optimal management scale, This means that farmers engage in off-farm employment (as part-time farmers) and lease their farmland to others. Consequently, supply of farmland increases while the equilibrium farm rent declines in the relevant farmland market.

, on the other hand, a rise in off-farm wage increases opportunity cost, resulting in a smaller optimal management scale, This means that farmers engage in off-farm employment (as part-time farmers) and lease their farmland to others. Consequently, supply of farmland increases while the equilibrium farm rent declines in the relevant farmland market.

Farmland market in the real world

Contrary to expectations of theoretical models, farmland consolidation has shown little progress and most farmers continue inefficient, unprofitable small-scale management. Japanese agricultural economics researchers have presented various key points to explain this reality based on detailed on-site observation, from standpoints far removed from theories. This paper discusses only on the points that are directly relevant to the concept of a farmland market.

Characteristics of farmland as a good

Before entering discussions on specific points, characteristics of farmland as a good that is traded in a market, namely the farmland market, should be clarified, because as stated below, the peculiarities of farmland as a good may inhibit it being efficiently traded in the market.

First, farmland cannot be moved (locational immovability). Second, consolidated farmland lots have higher use efficiency than independent lots of the same area (economy of consolidation). Third, farmland is unique in that only a single form of farmland exists in a certain location. Fourth, since farmland cannot be easily increased (except by reclamation), its supply is inelastic. Fifth, devastated farmland has externalities because such farmland is vulnerable to damage from diseases, insects and animals, which are likely to also harm neighboring farmland. Moreover, since farmland is immovable, presence of a devastated field inhibits other farmers from connecting with such a field. Sixth, in a rural community, farmland not only constitutes an element for production but also serves as a symbolic or political good that determines the social order of each household. In short, farmland is a good that is greatly influenced by the household norms (succession of family name, family business, family industry) or rural community norms (stigma against releasing farmland, feeling of resistance to entry of outsiders).

Gap between the image of a perfectly competitive farmland market and the reality

The theoretical model implicitly contains at least the five hypotheses described below. The gap between theory and reality arises because these hypotheses are not satisfied in reality.

The first hypothesis is that farmers behave based on their interest in profit maximization. While the theoretical model assumes the pursuit of maximization of profits, farmland is actually a good that is greatly influenced by household norms or rural community norms. It not only constitutes a production good but also serve as a consumption good that receives benefits from succession of the household business/industry or farming itself. Thus, farmers do not always behave for the purpose of maximizing their profits.

The second hypothesis is that a farmland market should be competitive. Since farmland is by nature immovable, trading of farmland is geographically constrained. Therefore, the farmland market tends to be thin, inevitably causing an oligopoly on both the lessor and lessee sides. Moreover, under the recent circumstances in which only a few borrowers exist due to farmers’ aging and the inclination to farm part-time, the amount of farm rent cannot be competitively decided, which may lead to an undersupply of farmland.

The third hypothesis is that farm rent is determined at a level that ensures balance between supply and demand. The standard model assumes that farm rent functions to adjust the imbalance between supply and demand in farmland trading. In reality, however, farm rent is decided through negotiation between the lessor and the lessee in view of the standard farm rent (reference farm rent) determined by accumulation of costs (the land residual technique) as the reference point. If the standard farm rent is different from the level of supply-demand balance, there should naturally be an imbalance between supply and demand.

The fourth is that there are no institutional strains surrounding farmland. While the standard model assumes no institutional strains regarding farmland, in reality there are several institutional problems, such as insufficient regulations of farmland conversion, which is associated with expectation of land conversion (Godo, 1998), and problems with the farmland taxation system (inheritance tax moratorium, etc.). These problems help increase reservation demands of lessors, and thus decrease supply of farmland, resulting consequently in a delay in the progress of farmland consolidation.

The fifth hypothesis is that there are no transaction costs. In reality, however, in trading farmland, various costs arise, including the cost of searching for a suitable trading partner or farm plot, the cost of examining the farmland conditions, the cost of negotiating trading conditions, and the time and cost required for institutional procedures (contractual cost).

Besides the above five hypotheses, various policies regarding pricing, income and production adjustment are pointed out to as factors affecting farmers’ behavior and farmland supply/demand, and have inhibited farmland consolidation.

Policies regarding farmland consolidation in Japan[3]

The majority of Japanese farmers are small-scale, land-owning farmers. This structure originated from the agrarian land reform, a policy implemented after World War II to release farmland to cultivators. Before the war in Japan, about a half of all farmland was cultivated by poor, small tenant farmers, and their precarious footing was considered to be the cause of many of the social problems facing farming villages. After the land reform, the ratio of tenanted land held by landowners decreased to 10%. Thus, the agrarian land reform generated so-called “postwar land-owning farmers” who own 1 hectare of farmland each (in all prefectures except Hokkaido), constituting nearly homogenous farming villages to start the postwar farming. To maintain this new farmland ownership structure and secure the rights of cultivators, the Agricultural Land Act was established in 1952 which imposes strict regulations concerning farmland, including restrictions on farmland ownership and control of farm rent. The Agricultural Land Act strictly protects the rights of tenant farmers and restricts landowners from terminating land lease contracts without consent of their tenant farmers. The Act also limits acquisition of farmland to those who actually cultivate the land. Permission by the agricultural committee set for each municipality became necessary for trading of farmland to ensure democratic decision-making.

After the Agricultural Basic Act was enacted in 1960 for the purpose of improving agricultural productivity and expanding the farming scale to increase income, regulations concerning farmland leasing were gradually eased. More significantly, the Agricultural Land Use Promotion Program was launched in 1975, which covered nearly all (97%) farmland lease transactions. The Agricultural Land Use Promotion Program was developed into the Agricultural Land Use Promotion Act in 1980, which was revised and renamed the Act on Promotion of Improvement of Agricultural Management Foundation in 1993, and has undergone several modifications up to today.

The Act on Promotion of Improvement of Agricultural Management Foundation in 1993 declares as its objective the development of efficient and stable farm management. Specifically, the Act stipulates prioritized support for core farmers such as certified farmers and some specific community farming organizations. Through the Act on Promotion of Improvement of Agricultural Management Foundation, the share of farmland operated by core farmers increased from 20% in 1996 to 42% in 2006; nonetheless, the pace of farmland concentration has been unsatisfactory.

By the way, farms on the 3ha scale would expand to at least 15ha has and costs would be significantly reduced. Figure 1 shows the production costs of rice by farm size. The total production cost for farm operators who cultivate less than a half hectare is more than double of those cultivating more than 15ha. In order to promote farmland consolidation, the Japanese government has initiated new policy such as “Local Plan of Farmers and Farmlands” and the Intermediate and Conservation Organization for Farmlands”. The purpose of these policies is to transfer the rights of farmlands from farmers in the next generation.

Market design[4] for farmland consolidation

Why can’t farmland complexes be established through plot exchange?

Actually, some political measures[5] have been taken, though they have not caused a major trend of farmland consolidation[6]. There are roughly two structural reasons for this.

The first is that since land cannot be moved, it can be exchanged with a very limited number of exchange partners. Imagine the following situation. A farmer has a farmland complex consisting of several connected plots (main farm) and a distant plot (outlying field). The farmer wishes to exchange plots with another farmer so as to turn the outlying field into a plot next to the main farm. Because the purpose of the exchange is to turn the outlying land into a plot next to the main farm, the exchange can be performed only with farmers who have plots neighboring the main farm. In Figure 2, for example, Farmer 2 intends to exchange his two outlying fields (C2 and F1) for plots next to his main farm at the bottom left, but only Farmer 3 is available for such an exchange.

The second reason is that the “double coincidence of wants” can hardly occur. To reach an agreement on a spontaneous exchange, there must be a situation where you want a plot belonging to another farmer and the other farmer also wants your plot. This situation, where the desires of both sides match, is called a “double coincidence of wants.”[7] It is extremely rare to find such an exchange partner from among the naturally small number of candidates.

Proposing the cycle trading method

Is there any way to enhance the rate of farmland consolidation? The key is to ease the constraint of the double coincidence of wants. In an individual, direct exchange, since farmers exchange plots on a one-to-one basis, the double coincidence of wants needs to be directly satisfied. In the case of Figure 2, for example, Farmer 2 cannot establish the double coincidence of wants with any other farmers and therefore cannot exchange plots.

Figure 2. Schematic diagram of fragmented farmland

Trading cycle method

Meanwhile, if many farmers join the exchange at the same time and form a “cycle of exchange,” plot exchange will become available even though the double coincidence of wants is not directly satisfied. In the case of Figure 2, Farmer 2 wants Farmer 3’s plot B6, Farmer 3 wants Farmer 4’s plot F7, and Farmer 4 wants Farmer 2’s plot F1. These relationships are described as a cycle of 2→ 3→ 4→ 2. In this cycle, Farmer 2 and Farmer 3 first exchange F1 and B6, and then Farmer 3 and Farmer 4 exchange F1 and F7. In this way, all parties can obtain the plots they want (Figure 3). Generally, exchange is possible if a cycle can be formed by describing each plot owner pointing at the owner of the plot he wants. This is based on the idea used in the algorithm called Top Trading Cycle (TTC) by Shapley and Scarf (1974). An advantage of this method is that it enables exchange with a party with whom the double coincidence of wants does not occur. The key point is that by forming a trading cycle consisting of many farmers and exchanging plots at the same time within the cycle, the participating farmers are guaranteed to obtain the plots connected to their main farm from other farmers. Because of this, farmers can agree on releasing their plots to other farmers with whom the double coincidence of wants does not exist.

Figure 3. Example of trading cycle method(2→3→4→2)

Simulation of the trading cycle method

Arimoto, Nakajima and Tomita (2014) confirmed the effectiveness of the cycle trading method by conducting a simulation. In the simulation, farmers declare to a mediator such as an agricultural cooperative the outlying fields they wish to exchange with other plots, to combine with their main farm to form a farmland complex, and the mediator redistributes the gathered outlying fields to the new owners. Specifically, it is a repeated sequence of creating a cycle in which each farmer participates with one of the plots they have submitted and redistributing the plots within the cycle[8]. Creating exchange cycles and deciding the redistribution patterns can be performed mechanically if the outlying fields for exchange and the main farms for consolidation are declared in advance. In the simulation, as conducted for the individual, direct method, based on the randomly created 10,000 patterns of farmland layout, 56 patterns of exchange were conducted by varying the farmers’ participation scenario or the algorithm combinations, and their performance was examined.

Performance of the trading cycle method

The results show that similar to the case of individual, direct exchange, performance depends strongly on the rate of participation in the exchange. With participation of 25% of the farmers of the village, the consolidation rate is less than 1%. With the participation of 50%, the consolidation rate rises to between 9 and 11%, depending on the algorithm, which is over double the performance of the individual, direct exchange. With 100% participation, nearly perfect consolidation can be achieved in some algorithms, reaching a consolidation rate between 62 and 97%.

The simulation results above demonstrate that the trading cycle method can achieve a significantly higher consolidation rate than individual, direct exchange. It is common for both methods, however, that the final performance depends strongly on the number of farm households that participate in the exchange and therefore the key is to invite as many participants as possible to the exchange.

Proposing the cycle trading method

Now, how should exchange based on the trading cycle method be carried out? Since the key to successful cycle trading is to have as many farmers as possible exchange their plots at one time, it is necessary to set up an opportunity for such simultaneous exchange. A possible method is that a mediator such as an agricultural committee or agricultural cooperative calls for participation in a simultaneous exchange and redistributes the submitted outlying fields to the participants.

To implement the cycle trading-based exchange, the challenges below need to be overcome.

CONCLUSION

Agro-economic studies concerning farmland consolidation in Japan have developed discussions on a perfectly competitive farmland market while presenting various findings based on a more realistic view of farmland market according to in-depth reality analysis. To bridge these two approaches, analysis of Japanese farmland market should pay attention to the following: (1) Since profit maximization is not always the behavioral principle of farmers, analysis should be conducted in a framework taking into consideration rural community norms, etc. (2) The peculiarities of farmland as a good may cause localization of market where oligopoly is likely to occur. (3) In reality, trading of farmland involves costs for searching and negotiation. Concerning the trading costs of (3), both theoretical and empirical studies have been accumulated, while future development is expected for (1) and (2).

From view point of international perspective, as to the studies concerning farmland market, the approach to identify and theorize a more realistic image of a farmland market will continue to be necessary. At the same time, it is also important to build consensus on the degree of generality or impact of the findings that have been presented. To this end, it is crucial to share and theorize the findings obtained in case studies and conduct quantitative analysis using highly representative micro-data with a large sample size, so as to raise the evidence level. Econometric techniques, such as regression analysis, are effective in describing or presenting the reality.

REFERENCES

Arimoto, Y. and Nakajima, S. 2013. Farmland Concentration, Consolidation and the Land Market, Journal of Rural Economics, 85(2): 70-79. (in Japanese).

Arimoto, Y., Nakajima, S. and Tomita, K. 2014. Farmland Consolidation by Plot Exchange: A Simulation-based Approach, Journal of Rural Economics, 86(3): 193-206. (in Japanese).

Deininger, K. 1995. Collective Agricultural Production: A Solution for Transition Economics. World Development, Vol. 23 (8): 1317-1334.

Godo, Y. 1998. A Statistical Description of the Concentration and Conversion of Farmland, Japanese Journal of Farm Management, 34(1): 62-71. (in Japanese).

Kawasaki, K. 2010. The Costs and Benefits of Land Fragmentation of Rice Farms in Japan, Australian Journal of Agricultural and Resource Economics, 54(4): 509-526.

Kawasaki, K. 2011. The Impact of Land Fragmentation on Rice Production Cost and Input Use, The Japanese Journal of Rural Economics, 13: 1-14.

Martini, R. and Kimura, S. 2009. Evaluation of Agricultural Policy Reforms in Japan, Paris: OECD.

Otsuka, K. 2007. Efficiency and Equity Effects of Land Markets, in R. E. Evenson and P. Pingali, eds. Handbook of Agricultural Economics, Vol.3: 2671-2703.

Shapley, L. and Scarf, H. 1974. On Cores and Indivisibility, Journal of Mathematical Economics, 1(1): 23-37.

Tanaka, T. 2007. Resource Allocation with Spatial Externalities: Experiments on Land Consolidation, The B.E. Journal of Economic Analysis & Policy, 7(1): Article 7.

Teruoka, S. 2008. Agriculture in the Modernization of Japan (1850-2000). Manohar, New Delhi.

Vulkan, N., Roth, A. E. and Neeman, Z. 2013. The Handbook of Market Design, Oxford University Press.

[1] The literature of the farmland market, see Arimoto and Nakajima (2013) and Otsuka (2007).

[2] Since this formulation includes off-farm income in the second term, there is no problem with considering it as the income maximization problem for part-time farmers.

[3] Summaries of agriculture in Japan, see Martini and Kimura (2009) and Teruoka (2008).

[4] For an explanation of the Top Trading Cycle (TTC), refer to Vulkan, Roth and Neeman (2013). The literature applying market design to farmland consolidation, see Tanaka (2008).

[5] According to Kawasaki (2010), several land consolidation measures have been implemented in Japan. One is called kanchi and is linked to the land improvement schemes of plot reshaping, plot size expansion, drainage and irrigation development, and road building. On the other hand, there is a measure which is not linked to land improvement. Under this program, called kokan bungo, farmers exchange plots without changing the plot size or shape.

[6] According to Martini and Kimura (2009), ‘a survey of 202 core farmers outside Hokkaido in 2007 found that core farmers cultivate on average 28.5 plots with average plot size of 0.52ha. The share of large plots of more than 2ha was 26.7%.’

[7] It is similarly true for goods other than farmland that the double coincidence of wants makes trading difficult. Generally, this friction is eliminated by money mediating transactions.

[8] To maximize the farmland consolidation rate of a village, distributing all the submitted exchangeable plots at one time is more desirable than following this sequential algorithm. Because it was difficult to find an algorithm that enables optimal distribution, this sequential algorithm was adopted as the second-best approach to conduct the simulation.