INTRODUCTION

In the Malaysian National Agro-Food Policy (2011-2020) (NAP4), seaweed was identified as one of the high-value commodities under the program of Entry Point Project 3 or EPP 3 (Venturing into Commercial Scale Seaweed Farming in Sabah) which was subjected to the themes of “Capitalizing on Malaysia’s Competitive Advantage”. Sabah is well known as an important site for the commercial production of seaweed in Malaysia. The East Cost Sabah waters have been identified as an Aquaculture Seaweed Industry Zone. To date, through the Ministry of Agriculture and Agro-Based Industry, a strategic approach has been taken to upgrade the small-scale group of seaweed cultivators into clusters through the provision of proper facilities that can create a more conducive and safer working environment (Express, 2014).

Under the current policy, the seaweed industry has been targeted to improve in its productivity through the development of a seaweed industrial zone, which is led by a private company. The private company is responsible for the coordination of quality seeds, cultivation, and the processing of seaweeds into high value products. The potential development to be carried out is in the areas surrounding Semporna, Kudat, and Lahad Datu with a targeted area of 20,500 hectares by 2020. Partnership with government and research institutions has been carried out to develop a Standard Operating Procedure (SOP) for the practice of cultivation and production of seaweeds. The application of mechanization in seaweed production is also used to improve the efficiency of the industry. At present, production has achieved one metric ton per day and is targeted to produce 10 metric tons per day by 2020.

Overview of Malaysian seaweed production

Seaweed is a macro-algae, growing in or near the sea and has been classified into three major groups based on its pigmentation of brown (Phaeophyceae), red (Rhodophycea) or green (Chloropphyceae) (Mohamad, Ahmad, Noh, & Saari, 2013). The supply of seaweed comes either from farmed seaweeds and naturally grown or wild seaweeds. Farmed seaweed has been growing in the last decades and it has contributed to more than 80% of the total seaweed supplies (MTDC, 2000). In the Asian Pacific region, seaweed especially of the green type (Kappaphycus or Eucheuma spp.), is commercially planted and is mostly concentrated in the Sulu sea waters to the borders of the Celebes coastal areas, particularly around Semporna to the island of Zamboanga in the Philippines (Mohamad et al., 2013; Suhaimi, 2011).

In Malaysia, the supply of seaweed comes exclusively from Sabah. It started in 1978 and was concentrated particularly in the areas of Semporna, Tawau, Kunak, and Lahad Datu, and involved an estimated 500 families. In these areas, the people are from the tribes of Bajau and they inhabit the Sulu Sea to cultivate seaweed since time immemorial as a vegetable in their meals (Mohamad et al., 2013).The types of seaweed grown in Sabah are Kappaphycus Cottonii and Kappaphycus Spinosum. Sabah’s seaweed farming project was initially a commercial failure due to lack of local support and farming problems. The production was only evident in 1989 with the initial production capacity of over 10 metric tons. Since then, the industry has experienced an overwhelming growth until now (Sade, Ali, & Mohd. Ariff, 2006)

Total production of Malaysian dried seaweed recorded since 1989 until 2003 showed a gradual increase from 1989 to 2001 and there was a drastic decline in the year 2002. However, the production has steadily increased since 2004 until 2013 (Refer to figure 1). In 2013, seaweed production from Sabah accounted for 28% by volume (33,210 mt) and 3% (RM 198.93 million) by value from the total marine aquaculture production. The seaweed production of Sabah was found to be increased slightly by volume in 2013 to 110.0 metric tons compared to that of the previous year.

Figure 1. Total production of dried seaweed in Malaysia (1989 – 2013)

.jpg)

Source : Sabah Annual Fisheries Statistic (2013)

Export and import of seaweed

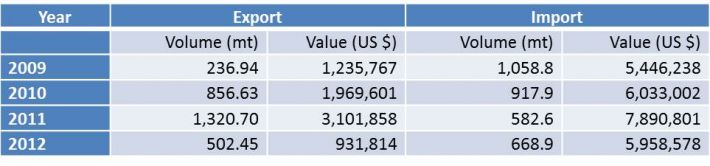

Table 1 shows the trend of Malaysian exports and imports of seaweed starting from 2009 to 2012. The quantity of seaweed exported in the past four years showed a slight fluctuation with the volume increasing from 236.94 metric tons in 2009 to 656.63 metric tons in 2010. There was a further increment to 1,320.70 metric tons in 2011. However, in 2012 it went down to 502.45 metric tons. The fluctuation in the volume exported is accordingly reflected in the amount of value that shows the parallel trend. The value of exported seaweed in the past four years increased steadily from US$ 1.23 million in 2009 to US$ 3.1 million in 2011. Total export in 2012 had declined and it accounted for 1.4% of the total value at USD 0.93 million of global trade of dried seaweed with a total of US$ 64.66 million.

The amount of imported dried seaweed showed a decreasing trend of 37% from 1,058.8 metric tons in 2009 to 668.9 metric tons in 2012. However, the declining trend was not reflected much in the value of imports where it fluctuated with a comparable average of 25%, from US$ 5.4 million in 2009 increasing to US$ 6.0 million in 2010 and US$ 7.9 million in 2011. A decline to US$ 5.9 million was observed in 2012. This fluctuation had given rise to the market volatility.

Table 1 : Exports and imports of dried seaweed (2009 – 2012)

Source : COMTRADE (2015)

Applications of seaweed

Seaweed is used in various fields of application such as in food, pharmaceutical, nutraceuticals, cosmesueticals, medical or other industries. It contains an array of bioactive compounds in the form of agar, alginate or carragenan powder. It is also commercially important as a stabilizer, thickener, gelling and emulsifier. It may be found in ice-cream and other milk products, jellies, gel-type air fresheners, sausages, toothpastes, and “power shakes” (INFOFISH, 1996). Its carragenan extract has a variety of applications ranging from food to non-food products either used as a ready-made blend or as a tailored formulation. Nevertheless, these differences are merely a reflection of the source of the raw materials and their processing procedures. There are three (3) types of carragenan extraction: (1) Highly Refined Carragenan, (2) Refined Carragenan (RC), and (3) Semi-Refined Carragenan (SRC). The existence of over 200 blends of these extractions in the market is predominantly due to variations in their combination and concentration, and on the many different functions performed based on the properties desired (Whistler and BeMiller, 1993).

Prospect industry

The world demand for seaweed, especially in carragenan, grew tremendously at a faster rate during the past decade. This was mostly due to the increasing applications of carragenan in various products. In 2006, the market for carragenan was estimated at 40 ,000 metric tons and it is projected to increase at a rate of 10–15% per annum with an estimated value of US$3.3 billion. The Ministry of Agriculture and Agro-Based Industry projected that wet seaweed production is expected to expand by 19.7%, from 365,000 metric tons in 2015, tripling to about 900,000 metric tons in 2020. Moreover, the Malaysian export value of dry seaweed and carragenan is also expected to increase in parallel with its production. It also assumed the export value to triple by 2020, from RM 376 million in 2015 to RM 1.4 billion (2020). Generally, the cycle and the overall dynamics of the carragenan industry are dependent on the economy, particularly with the food industry. The growth in the food industry or any related industries will signify the potential growth in the carragenan market (MTDC, 2002). Hence, with an estimated world population of 8 billion in 2030 , the overall food consumption is certainly going to increase, while the demand for carragenan is also expected to increase.

CONCLUSION

Seaweed has become an important industry to be strengthened and has been highlighted as one of the high-value commodities under the Malaysian National Agro Policy for the year 2011-2020 Malaysia has the potential to be a major seaweed player in the region, provided the country has fully developed and utilized the existing strengths. These include the availability of infrastructure, manpower, product quality, transfer of technology, industrial support, and marketing. The production volume and value would increase if more efforts, inclusive of research activities and prevalent technology are put into boosting the industry. Malaysia will strive to ensure that this industry will have a competitive advantage as stipulated in the policy. The high demand of carragenan applications in non-food and food industries will augur well in the future.

REFERENCES

Express, D. (2014). Govt supports UMS’ research development of seaweed _ Daily Express Newspaper Online, Sabah, Malaysia. Sabah Publishing Sdn Bhd. Retrieved March 24, 2015, from http://www.dailyexpress.com.my/news.cfm?NewsID=92960

Mohamad, R., Ahmad, M., Noh, N., & Saari, N. (2013). Daya maju dan daya saing industri rumpai laut Malaysia. Retrieved from http://etmr.mardi.gov.my/Content/ETMR Vol.8 (2013)/1. Rashilah.pdf

Sade, A., Ali, I., & Mohd. Ariff, M. R. (2006). the Seaweed Industry in Sabah, East Malaysia. Jati, 11(December 2006), 97–107.

Suhaimi, Y. (2011). NKEA – Agriculture EPP 3 – Seaweed mini estate (Community based – Commercial approach). Paper presented in National Key Economic Area (NKEA) Workshop by Department of Fisheries Malaysia, 25 – 27 Januari 2011, Melaka

Whistler, R.L., and BeMiller, J.N., (1993). Industrial Gums : Polysaccharides and Their Derivatives3rd edition, California : Acedemic Press.

|

Date submitted: May 12, 2015

Reviewed, edited and uploaded: May 13, 2015

|

Prospects and Policy Review of seaweed as a High-Value Commodity in Malaysia

INTRODUCTION

In the Malaysian National Agro-Food Policy (2011-2020) (NAP4), seaweed was identified as one of the high-value commodities under the program of Entry Point Project 3 or EPP 3 (Venturing into Commercial Scale Seaweed Farming in Sabah) which was subjected to the themes of “Capitalizing on Malaysia’s Competitive Advantage”. Sabah is well known as an important site for the commercial production of seaweed in Malaysia. The East Cost Sabah waters have been identified as an Aquaculture Seaweed Industry Zone. To date, through the Ministry of Agriculture and Agro-Based Industry, a strategic approach has been taken to upgrade the small-scale group of seaweed cultivators into clusters through the provision of proper facilities that can create a more conducive and safer working environment (Express, 2014).

Under the current policy, the seaweed industry has been targeted to improve in its productivity through the development of a seaweed industrial zone, which is led by a private company. The private company is responsible for the coordination of quality seeds, cultivation, and the processing of seaweeds into high value products. The potential development to be carried out is in the areas surrounding Semporna, Kudat, and Lahad Datu with a targeted area of 20,500 hectares by 2020. Partnership with government and research institutions has been carried out to develop a Standard Operating Procedure (SOP) for the practice of cultivation and production of seaweeds. The application of mechanization in seaweed production is also used to improve the efficiency of the industry. At present, production has achieved one metric ton per day and is targeted to produce 10 metric tons per day by 2020.

Overview of Malaysian seaweed production

Seaweed is a macro-algae, growing in or near the sea and has been classified into three major groups based on its pigmentation of brown (Phaeophyceae), red (Rhodophycea) or green (Chloropphyceae) (Mohamad, Ahmad, Noh, & Saari, 2013). The supply of seaweed comes either from farmed seaweeds and naturally grown or wild seaweeds. Farmed seaweed has been growing in the last decades and it has contributed to more than 80% of the total seaweed supplies (MTDC, 2000). In the Asian Pacific region, seaweed especially of the green type (Kappaphycus or Eucheuma spp.), is commercially planted and is mostly concentrated in the Sulu sea waters to the borders of the Celebes coastal areas, particularly around Semporna to the island of Zamboanga in the Philippines (Mohamad et al., 2013; Suhaimi, 2011).

In Malaysia, the supply of seaweed comes exclusively from Sabah. It started in 1978 and was concentrated particularly in the areas of Semporna, Tawau, Kunak, and Lahad Datu, and involved an estimated 500 families. In these areas, the people are from the tribes of Bajau and they inhabit the Sulu Sea to cultivate seaweed since time immemorial as a vegetable in their meals (Mohamad et al., 2013).The types of seaweed grown in Sabah are Kappaphycus Cottonii and Kappaphycus Spinosum. Sabah’s seaweed farming project was initially a commercial failure due to lack of local support and farming problems. The production was only evident in 1989 with the initial production capacity of over 10 metric tons. Since then, the industry has experienced an overwhelming growth until now (Sade, Ali, & Mohd. Ariff, 2006)

Total production of Malaysian dried seaweed recorded since 1989 until 2003 showed a gradual increase from 1989 to 2001 and there was a drastic decline in the year 2002. However, the production has steadily increased since 2004 until 2013 (Refer to figure 1). In 2013, seaweed production from Sabah accounted for 28% by volume (33,210 mt) and 3% (RM 198.93 million) by value from the total marine aquaculture production. The seaweed production of Sabah was found to be increased slightly by volume in 2013 to 110.0 metric tons compared to that of the previous year.

Figure 1. Total production of dried seaweed in Malaysia (1989 – 2013)

Source : Sabah Annual Fisheries Statistic (2013)

Export and import of seaweed

Table 1 shows the trend of Malaysian exports and imports of seaweed starting from 2009 to 2012. The quantity of seaweed exported in the past four years showed a slight fluctuation with the volume increasing from 236.94 metric tons in 2009 to 656.63 metric tons in 2010. There was a further increment to 1,320.70 metric tons in 2011. However, in 2012 it went down to 502.45 metric tons. The fluctuation in the volume exported is accordingly reflected in the amount of value that shows the parallel trend. The value of exported seaweed in the past four years increased steadily from US$ 1.23 million in 2009 to US$ 3.1 million in 2011. Total export in 2012 had declined and it accounted for 1.4% of the total value at USD 0.93 million of global trade of dried seaweed with a total of US$ 64.66 million.

The amount of imported dried seaweed showed a decreasing trend of 37% from 1,058.8 metric tons in 2009 to 668.9 metric tons in 2012. However, the declining trend was not reflected much in the value of imports where it fluctuated with a comparable average of 25%, from US$ 5.4 million in 2009 increasing to US$ 6.0 million in 2010 and US$ 7.9 million in 2011. A decline to US$ 5.9 million was observed in 2012. This fluctuation had given rise to the market volatility.

Table 1 : Exports and imports of dried seaweed (2009 – 2012)

Source : COMTRADE (2015)

Applications of seaweed

Seaweed is used in various fields of application such as in food, pharmaceutical, nutraceuticals, cosmesueticals, medical or other industries. It contains an array of bioactive compounds in the form of agar, alginate or carragenan powder. It is also commercially important as a stabilizer, thickener, gelling and emulsifier. It may be found in ice-cream and other milk products, jellies, gel-type air fresheners, sausages, toothpastes, and “power shakes” (INFOFISH, 1996). Its carragenan extract has a variety of applications ranging from food to non-food products either used as a ready-made blend or as a tailored formulation. Nevertheless, these differences are merely a reflection of the source of the raw materials and their processing procedures. There are three (3) types of carragenan extraction: (1) Highly Refined Carragenan, (2) Refined Carragenan (RC), and (3) Semi-Refined Carragenan (SRC). The existence of over 200 blends of these extractions in the market is predominantly due to variations in their combination and concentration, and on the many different functions performed based on the properties desired (Whistler and BeMiller, 1993).

Prospect industry

The world demand for seaweed, especially in carragenan, grew tremendously at a faster rate during the past decade. This was mostly due to the increasing applications of carragenan in various products. In 2006, the market for carragenan was estimated at 40 ,000 metric tons and it is projected to increase at a rate of 10–15% per annum with an estimated value of US$3.3 billion. The Ministry of Agriculture and Agro-Based Industry projected that wet seaweed production is expected to expand by 19.7%, from 365,000 metric tons in 2015, tripling to about 900,000 metric tons in 2020. Moreover, the Malaysian export value of dry seaweed and carragenan is also expected to increase in parallel with its production. It also assumed the export value to triple by 2020, from RM 376 million in 2015 to RM 1.4 billion (2020). Generally, the cycle and the overall dynamics of the carragenan industry are dependent on the economy, particularly with the food industry. The growth in the food industry or any related industries will signify the potential growth in the carragenan market (MTDC, 2002). Hence, with an estimated world population of 8 billion in 2030 , the overall food consumption is certainly going to increase, while the demand for carragenan is also expected to increase.

CONCLUSION

Seaweed has become an important industry to be strengthened and has been highlighted as one of the high-value commodities under the Malaysian National Agro Policy for the year 2011-2020 Malaysia has the potential to be a major seaweed player in the region, provided the country has fully developed and utilized the existing strengths. These include the availability of infrastructure, manpower, product quality, transfer of technology, industrial support, and marketing. The production volume and value would increase if more efforts, inclusive of research activities and prevalent technology are put into boosting the industry. Malaysia will strive to ensure that this industry will have a competitive advantage as stipulated in the policy. The high demand of carragenan applications in non-food and food industries will augur well in the future.

REFERENCES

Express, D. (2014). Govt supports UMS’ research development of seaweed _ Daily Express Newspaper Online, Sabah, Malaysia. Sabah Publishing Sdn Bhd. Retrieved March 24, 2015, from http://www.dailyexpress.com.my/news.cfm?NewsID=92960

Mohamad, R., Ahmad, M., Noh, N., & Saari, N. (2013). Daya maju dan daya saing industri rumpai laut Malaysia. Retrieved from http://etmr.mardi.gov.my/Content/ETMR Vol.8 (2013)/1. Rashilah.pdf

Sade, A., Ali, I., & Mohd. Ariff, M. R. (2006). the Seaweed Industry in Sabah, East Malaysia. Jati, 11(December 2006), 97–107.

Suhaimi, Y. (2011). NKEA – Agriculture EPP 3 – Seaweed mini estate (Community based – Commercial approach). Paper presented in National Key Economic Area (NKEA) Workshop by Department of Fisheries Malaysia, 25 – 27 Januari 2011, Melaka

Whistler, R.L., and BeMiller, J.N., (1993). Industrial Gums : Polysaccharides and Their Derivatives3rd edition, California : Acedemic Press.

Date submitted: May 12, 2015

Reviewed, edited and uploaded: May 13, 2015