ABSTRACT

Coffee plantation has contributed to the economic development of Laos over the past three decades. Coffee is one of the most famous agricultural exports of Laos, particularly the product from Bolaven Plateau in the country’s southern part. The widespread of coffee plantation has gradually emerged in the mountainous areas of the north as well. Although there is a high demand of coffee, but Lao coffee production is facing many challenges. In recent years, coffee production in Laos is threatened by cassava plantation intervention, market obstruction, labor insufficiency, and climate change. It is suggested that the government should evaluate its zoning mechanism to strengthen coffee plantation and restrict crop boom that causes vulnerable soil. In addition, raising climate change awareness is essential to help local producers adapt and improve their production. Lao coffee sector development should be paralleled with other potential crops that offer more gains and less negative effect, particularly soil deterioration.

Keywords: coffee, producer, market, crossroad, Laos

INTRODUCTION

Coffee plantation is the prior agricultural production of Lao PDR (hereafter referred to as Laos). Harvested areas have been expanded over the past three decades from 20,000 hectares in 1990 to 88,000 hectares in 2020, which is the fourth crop after rice, cassava, other crop plantation areas (FAO, 2022). More than 80% of coffee plantation is located in the southern part of Laos, particularly the Bolaven Plateau. It is expected to generate more income to local people. Several studies suggest that coffee plantation could offer job opportunities and help farmers to earn more income, particularly farmers who planted organic coffee and could get access to markets (JICA, 2012; Phommavong, Ounmany & Hathalong, 2015; Seneduangdeth et al., 2018; Toro, 2012). However, its contribution in GDP decreased from 0.86% in 2011 to 0.45% and 0.48% in 2020 and 2021, respectively (ASEAN Stats, 2022; World Bank, 2022). A decline in value added to GDP is a result from energy and mining sectors’ contribution, coffee prices’ variation, and foreign exchange’s fluctuation.

Lao coffee sector faces many challenges from both external and internal threats. With respect to external threats, despite the drop of coffee prices and fluctuations of foreign exchange, climate change is playing a crucial role in threatening coffee production. With respect to internal threats, crop boom is threatening coffee plantation due to higher prices. Coffee production also struggles to meet international standard for exports due to a lack of capital, limited credit access, and limited production technique. Despite all these, smallholder farmers have weak bargaining power to negotiate with buyers and prices are suppressed by middlemen and large coffee producers (Enterprise & Development Consultants, 2016; Lao Coffee Association, 2014; Southichack, 2009; Toro, 2012; World Bank & Global Development Solutions, 2005). As a result, coffee farmers probably choose other crops that offer higher income.

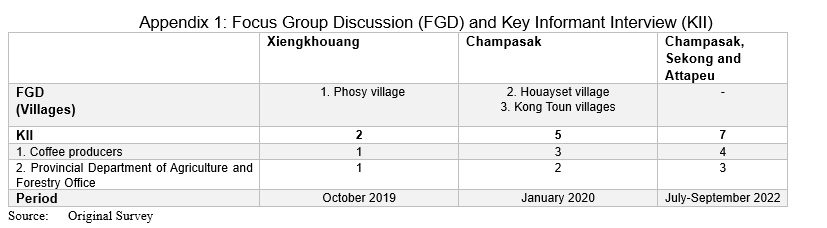

In this respect, this research study aims to investigate the adaptation of farmers in order to mitigate these threats. This paper examines a degree of Lao coffee producers’ adaptation and mitigation by reviewing secondary data on global coffee market, Lao coffee market, and climate change data. In addition, primary data were collected in Khoun district, Xieng Khouang province in October 2019, Paksong district, Champasak province in January 2020, and Champasak, Sekong and Attapeu provinces in July-September 2022 from relevant coffee producers, entrepreneurs, and local authorities to reveal implications for deepening opportunities and challenges in coffee production (Appendix 1).

LAOS COFFEE IN INTERNATIONAL CONTEXT

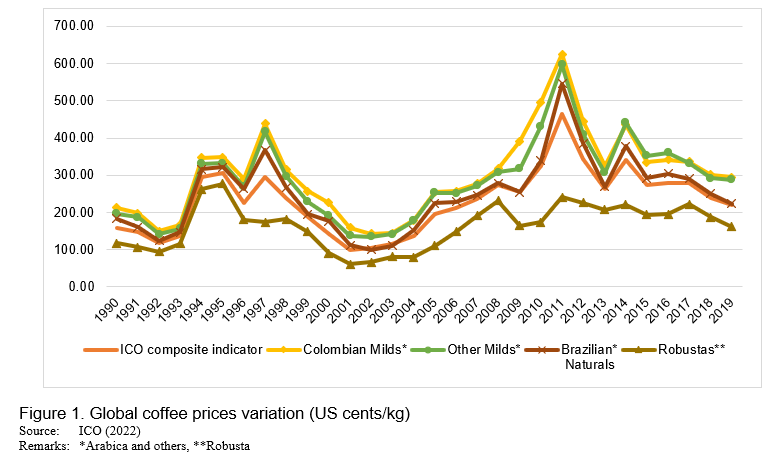

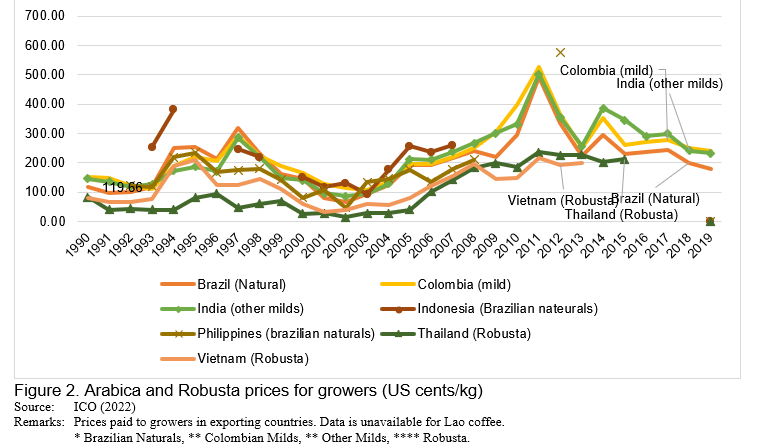

Over the past three decades, Laos’ coffee production increased almost two folds from 6 million tons in crop year 1990/91 to 10 million tons in 2019/20. Whereas, the trend of coffee exports shared a similar pattern, increased from 4 million tons in 1990/91 to 8 million tons in 2019/20 (ICO, 2022). Since 2010, according to the International Coffee Organization (ICO), the top three coffee exporter countries were Brazil, Vietnam, and Colombia, respectively, which accounted for approximately 60% of total exports. On the other hand, the major coffee importer countries were the United States of America, Germany, and Italy, respectively, which accounted for almost 50% of global demands. This implied that there is still a demand for coffee even it faced a small drop during the Global Coffee Crisis in 2000-2004 and the Global Financial Crisis in 2008-2009 (Figures 1 and 2).

In 2021, coffee production areas in Laos covered around 83,320 hectares, which is the fourth crop after rice paddy, maize, and vegetable plantation areas (LSB, 2022).

Previously, 99% of coffee plantation areas varied in the Bolaven Plateau, which is known for its volcanic fields in the southern part of Laos. The most well-known coffee production group in the south is Bolaven Plateau Coffee Producers Cooperative (CPC) that received international assistance from the French investors since its establishment. There are 1,855 farm households as its members from 55 villages in 3 districts of 3 provinces (Champasak, Salavan, and Sekong). Besides this, a new comer Jhai Coffee Farmers Cooperative actively operates its production in Paksong of Champasak province.

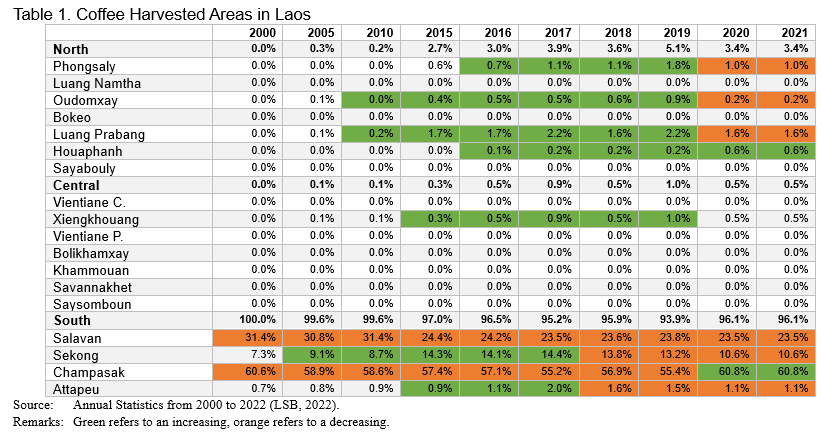

Eighty percent (80%) of coffee plantations in Laos is planted to Arabica coffee, which offers higher prices compared to other variety, Robusta. But Arabica is more sensitive to high temperature and pests, causing higher production costs. In order to solve this problem, growers have tried to plant other coffee varieties. As a result, Catimor variety (a mixture between Arabica and Robusta varieties) was introduced to the Lao coffee farmers since the late 2010s. Now that Laos is experiencing the effects of climate change and farmers are slowly into planting diversification, coffee plantations are expanding to the country’s northern provinces. There are Phongsaly, Oudomxay, Luang Prabang, Houaphanh, and Xiengkhouang, which are increasing more shares in coffee plantation area, as shown in Table 1. A well-known coffee production group in the north is Keoset Community Coffee, which is being operated by a pool of farmers from 5 villages in Khoun district of Xiengkhouang province.

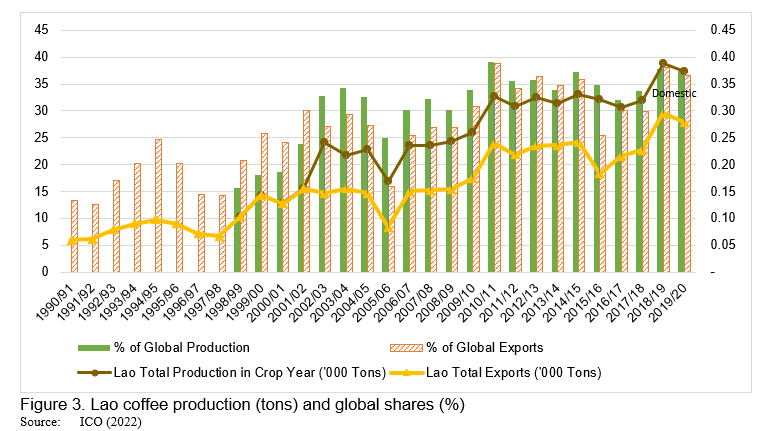

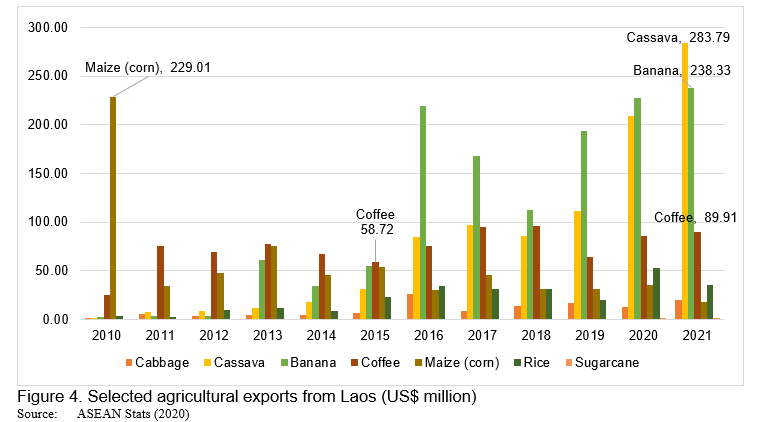

Figure 3 displays the production of Lao coffee in tons and its global shares. In 2021, coffee beans are one of the major agricultural exports of Laos which mostly goes to Vietnam, Thailand, EU-27, Japan, and Cambodia. It accounted for approximately 90% of Lao coffee exports, but the proportion was still low compared with global trade. The remaining coffee export is roasted coffee that is being supplied to the Cambodian, Chinese, and Thai markets (ASEAN Stats, 2022). Although, coffee plantation areas ranked fourth place in agricultural production, there were only 30,000 tons of coffee that have been harvested in 2021 and the production would fall in 2022. This is mainly due to many difficulties, such as the effects of climate change and cassava plantation intervention, as shown in Figure 4.

Climate change is a real threat in coffee production around the world. According to the NASA and various known research centers, each year global temperature is getting higher, and the arctic glacier continues to melt, which causes the rising of sea level. There have been many extreme disaster events that are affecting livelihoods such as typhoons, hurricanes, earthquakes, heatwaves, landslides, floods, drought, etc. According to the data from the Meteorology and Hydrology Office (Provincial Department of Natural Resource and Environment in Xieng Khouang and Champasak), the temperature has increased and rainfall patterns have changed, all of which directly affected coffee quantity and quality. Coffee plantations are affected by these changes, particularly farmers who depend on natural sources of water.

QUALITATIVE RESULTS

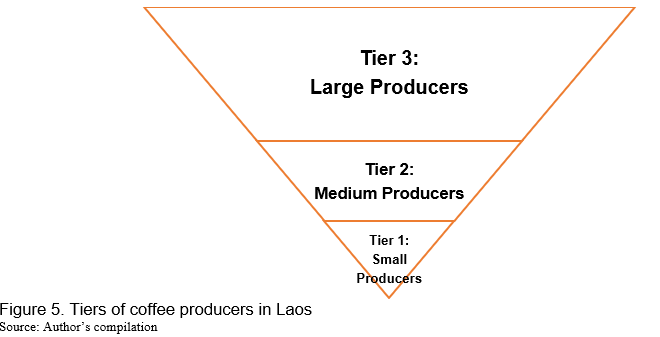

Based on author’s observation and findings from the Focus Group Discussions (FGDs) and the Key Informant Interviews (KIIs) (Appendix 1), Lao coffee producers may be classified into three tiers, namely Tier 1 (smallholder producers), Tier 2 (medium producers), and Tier 3 (large producers), as shown in Figure 5.

- Tier 1 covers smallholder farmers who have small plantation area around 1-2 hectares. Produce from Tier 1 accounts for only 5% of coffee exports. Their production labor consists of family members and temporary workers or seasonal employees. Wages in the north is higher than the south due to mountainous areas and limited workers.

- Tier 2 includes medium coffee producers who have plantation areas not exceeding 100 hectares with proper management. Their produce account for around 15% of coffee exports. Medium producers have higher degree to access to markets locally and internationally compared to smallholder producers, particularly in Vietnam and Thailand. Some of their outputs are also exported to Europe. Tier 2 producers have better management in production, processing, and transporting than Tier 1, but still struggles to upgrade to Tier 3. They tend to supply roasted coffee rather than instant coffee as this type of processing requires intensive capital. In addition, medium producers face a challenge to participate in coffee production group and have access to larger markets due to trade barriers from larger producers in Tier 3.

- Tier 3 are those coffee producers who have great access to finance, and resources, which have the longest history than Tier 1 and Tier 2. Their produce accounts for almost 80% of coffee exports. Large producers have their own trademarks and are well-known in the market locally and internationally. Most of them are founders and co-founders of the Lao Coffee Association, of whom major exporters, and coffee production groups have been operating since 1994, 2002, and 2009, respectively. Moreover, they initiate the Geographical Indications for coffee produce, particularly Lao or Bolaven coffee. It implies that Tier 3 producers have a great influence toward Lao coffee production. Tier 3 is likely to have a form of business operations than Tier 2 and Tier 1. They have greater resilience to global prices’ fluctuation as they receive more opportunities to access credits and production techniques.

Although, there are efforts to improve the quality and quantity of coffee production, they are insufficient to support the coffee sector. Several challenges remain the same for more than a decade. According to FGDs and KIIs, coffee production in Laos is threatened by cash crop intervention, market orientation, labor insufficiency, and climate change.

- First, there is a cassava boom that threatens the coffee plantation areas. Although the price of Robusta has risen from around US$0.27 per kilogram to US$0.99 per kilogram[1], but a demand for cassava rapidly increases, pushing prices even higher. Local farmers abandon coffee plantation to plant cassava that offer more revenues. However, these cash crops have greater vulnerability in terms of soil. In medium- and long-terms, it will affect food security due to soil deterioration.

- Second, small and medium coffee producers claim that it is difficult to access new markets, which are obstructed by large producers. Contrarily, large producers argue that small and medium producers cannot meet international standards when they try to access the global market, particularly the effort to export to Europe.

- Third, there is a shortage of labor due to the fact that most of the labor force are being operated on a seasonal employment basis. In other words, workers that be employed in coffee plantation are also working in rice fields of their own or those owned by others. The coffee harvest season starts from October to January for Arabica/Catimor variety and from February for Robusta coffee, which overlap rice harvest season.

- Lastly, climate change is threatening coffee production. The degree of smallholder farmers’ adaptation is low compared with those of medium and large producers, causing lower quality of coffee. Medium and large producers aspire to mitigate this risk by obtaining new technique and plant more Catimor variety.

CONCLUDING REMARKS

Coffee plantation has contributed to economic development of Laos over the past three decades. It offers an opportunity to improve local livelihoods by creating more jobs and income. At the macro level, coffee is one of the most famous agricultural exports of Laos, particularly the produce from Bolaven Plateau, which is located in the southern part of the country. The widespread expansion of coffee plantation has gradually emerged in mountainous areas of the north as well. Currently, Lao coffee production is facing many challenges both from external and internal threats. With respect to external factors, climate change is threatening coffee production. With respect to internal factors, cassava boom intervenes with coffee plantation and causes soil deterioration. It is suggested that the government should determine zoning to strengthen coffee plantation and restrict crop boom that causes vulnerable soil. The government aspires to determine zoning based on geography, areas, and market access potential in order to enhance agricultural production for exports. There are four types of plantation areas, such as rice paddy, biennial plant area, fruit tree plantation area, and pasture. In addition, raising climate change awareness is an essential to help local producers adapt and improve their production. Lao coffee sector development should be paralleled with other potential crops that offer more gains and less effect, particularly soil deterioration.

Despite cassava intervention, market limitation, labor shortage, and climate change, smallholder farmers also have weak bargaining in contract farming enforcement, leading to suppression of prices. Coffee farmer/production group should be improved to support local growers in terms of production techniques, training, credits, and markets. The government should progressively deepen its support and assistance to enhance farmers’ production groups, improve business environment, and facilitate procedures for coffee produce and exports. More importantly, the government should maintain and broaden its coffee market locally and internationally. This should be in parallel with the development of other potential agricultural produce that contribute to improve local livelihoods and economy.

REFERENCES

ASEAN Stats (2022). International Merchandise Trade Statistics (IMTS): ASEAN Stats Data Portal. Retrieved from https://data.aseanstats.org/trade. Accessed 12 October 2022.

Enterprise & Development Consultants. (2016). “Non-Tariff Measures (NTMs) Faced by Exporters of Lao PDR: A Field Survey Report”. Project Report, Vientiane.

FAO. (2022). FAOSTAT. Retrieved from: http://www.fao.org/faostat/en/#data. Accessed on 12 October 2022.

ICO. (2020). Historical Data on the Global Coffee Trade. Retrieved from: http://www.ico.org/new_historical.asp?section=Statistics. Accessed 12 October 2022.

JICA. (2012). “Lao People’s Democratic Republic: Data Collection Survey on Selecting the Processed Food to Be Focused and Promoting Foreign Direct Investment in Food Business in Laos”. Final Report.

Lao Coffee Association. (2014). “2025 Strategy of Lao Coffee Promotion”. Vientiane Capital. [in Lao language].

LSB. (2022). 2021 Annual Statistics. Lao Statistics Bureau, Ministry of Planning and Investment.

Phommavong, S., Ounmany, K., & Hathalong, K. (2015). “Mapping context of land use for a non-traditional agricultural export (NTAE) product: case study of land use for coffee plantation in Pakxong district, Champasak province, Lao PDR”. Conference Paper Np. 75. An International Academic Conference on Land grabbing, conflict and agrarian-environmental transformations: perspectives from East and Southeast Asia. Chiang Mai University. 5-6 June 2015.

Saysana, V. (2011). “Promoting organic and fair trade certification in the Lao PDR coffee sector: Benefits and challenges for farmers and local economies”. Master Dissertation, Faculty of the Graduate College, Oklahoma State University, July 2011.

Seneduangdeth, D., et al. (2018). Labor employment opportunities in coffee production in southern Lao People’s Democratic Republic. Journal of Asian Rural Studies, Vol 2 (1), pp 16-36.

Southichack, M. (2009). “The Lao Coffee Economy: A New Growth Path on the Horizon?”. Vientiane.

Toro, M. (2012). “Coffee Markets, Smallholder Credit, and Landscape Changes in the Bolaven Plateau Region, Laos”. Master Thesis, University of Miami, May 2012.

World Bank. (2022). GDP (current US$) – Lao PDR. Retrieved from: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=LA. Accessed 12 October 2022.

World Bank, & Global Development Solutions, LLC. (2005). “Integrated Value Chain Analysis of Selected Strategic Sectors in Lao People’s Democratic Republic”. Report.

[1] US$1 is equivalent to 11,159 kip, as Bank of Lao PDR’s average reference rate in January 2022.

Is Lao Coffee Sector at Its Crossroad? An Analysis of Coffee Market and Coffee Producers

ABSTRACT

Coffee plantation has contributed to the economic development of Laos over the past three decades. Coffee is one of the most famous agricultural exports of Laos, particularly the product from Bolaven Plateau in the country’s southern part. The widespread of coffee plantation has gradually emerged in the mountainous areas of the north as well. Although there is a high demand of coffee, but Lao coffee production is facing many challenges. In recent years, coffee production in Laos is threatened by cassava plantation intervention, market obstruction, labor insufficiency, and climate change. It is suggested that the government should evaluate its zoning mechanism to strengthen coffee plantation and restrict crop boom that causes vulnerable soil. In addition, raising climate change awareness is essential to help local producers adapt and improve their production. Lao coffee sector development should be paralleled with other potential crops that offer more gains and less negative effect, particularly soil deterioration.

Keywords: coffee, producer, market, crossroad, Laos

INTRODUCTION

Coffee plantation is the prior agricultural production of Lao PDR (hereafter referred to as Laos). Harvested areas have been expanded over the past three decades from 20,000 hectares in 1990 to 88,000 hectares in 2020, which is the fourth crop after rice, cassava, other crop plantation areas (FAO, 2022). More than 80% of coffee plantation is located in the southern part of Laos, particularly the Bolaven Plateau. It is expected to generate more income to local people. Several studies suggest that coffee plantation could offer job opportunities and help farmers to earn more income, particularly farmers who planted organic coffee and could get access to markets (JICA, 2012; Phommavong, Ounmany & Hathalong, 2015; Seneduangdeth et al., 2018; Toro, 2012). However, its contribution in GDP decreased from 0.86% in 2011 to 0.45% and 0.48% in 2020 and 2021, respectively (ASEAN Stats, 2022; World Bank, 2022). A decline in value added to GDP is a result from energy and mining sectors’ contribution, coffee prices’ variation, and foreign exchange’s fluctuation.

Lao coffee sector faces many challenges from both external and internal threats. With respect to external threats, despite the drop of coffee prices and fluctuations of foreign exchange, climate change is playing a crucial role in threatening coffee production. With respect to internal threats, crop boom is threatening coffee plantation due to higher prices. Coffee production also struggles to meet international standard for exports due to a lack of capital, limited credit access, and limited production technique. Despite all these, smallholder farmers have weak bargaining power to negotiate with buyers and prices are suppressed by middlemen and large coffee producers (Enterprise & Development Consultants, 2016; Lao Coffee Association, 2014; Southichack, 2009; Toro, 2012; World Bank & Global Development Solutions, 2005). As a result, coffee farmers probably choose other crops that offer higher income.

In this respect, this research study aims to investigate the adaptation of farmers in order to mitigate these threats. This paper examines a degree of Lao coffee producers’ adaptation and mitigation by reviewing secondary data on global coffee market, Lao coffee market, and climate change data. In addition, primary data were collected in Khoun district, Xieng Khouang province in October 2019, Paksong district, Champasak province in January 2020, and Champasak, Sekong and Attapeu provinces in July-September 2022 from relevant coffee producers, entrepreneurs, and local authorities to reveal implications for deepening opportunities and challenges in coffee production (Appendix 1).

LAOS COFFEE IN INTERNATIONAL CONTEXT

Over the past three decades, Laos’ coffee production increased almost two folds from 6 million tons in crop year 1990/91 to 10 million tons in 2019/20. Whereas, the trend of coffee exports shared a similar pattern, increased from 4 million tons in 1990/91 to 8 million tons in 2019/20 (ICO, 2022). Since 2010, according to the International Coffee Organization (ICO), the top three coffee exporter countries were Brazil, Vietnam, and Colombia, respectively, which accounted for approximately 60% of total exports. On the other hand, the major coffee importer countries were the United States of America, Germany, and Italy, respectively, which accounted for almost 50% of global demands. This implied that there is still a demand for coffee even it faced a small drop during the Global Coffee Crisis in 2000-2004 and the Global Financial Crisis in 2008-2009 (Figures 1 and 2).

In 2021, coffee production areas in Laos covered around 83,320 hectares, which is the fourth crop after rice paddy, maize, and vegetable plantation areas (LSB, 2022).

Previously, 99% of coffee plantation areas varied in the Bolaven Plateau, which is known for its volcanic fields in the southern part of Laos. The most well-known coffee production group in the south is Bolaven Plateau Coffee Producers Cooperative (CPC) that received international assistance from the French investors since its establishment. There are 1,855 farm households as its members from 55 villages in 3 districts of 3 provinces (Champasak, Salavan, and Sekong). Besides this, a new comer Jhai Coffee Farmers Cooperative actively operates its production in Paksong of Champasak province.

Eighty percent (80%) of coffee plantations in Laos is planted to Arabica coffee, which offers higher prices compared to other variety, Robusta. But Arabica is more sensitive to high temperature and pests, causing higher production costs. In order to solve this problem, growers have tried to plant other coffee varieties. As a result, Catimor variety (a mixture between Arabica and Robusta varieties) was introduced to the Lao coffee farmers since the late 2010s. Now that Laos is experiencing the effects of climate change and farmers are slowly into planting diversification, coffee plantations are expanding to the country’s northern provinces. There are Phongsaly, Oudomxay, Luang Prabang, Houaphanh, and Xiengkhouang, which are increasing more shares in coffee plantation area, as shown in Table 1. A well-known coffee production group in the north is Keoset Community Coffee, which is being operated by a pool of farmers from 5 villages in Khoun district of Xiengkhouang province.

Figure 3 displays the production of Lao coffee in tons and its global shares. In 2021, coffee beans are one of the major agricultural exports of Laos which mostly goes to Vietnam, Thailand, EU-27, Japan, and Cambodia. It accounted for approximately 90% of Lao coffee exports, but the proportion was still low compared with global trade. The remaining coffee export is roasted coffee that is being supplied to the Cambodian, Chinese, and Thai markets (ASEAN Stats, 2022). Although, coffee plantation areas ranked fourth place in agricultural production, there were only 30,000 tons of coffee that have been harvested in 2021 and the production would fall in 2022. This is mainly due to many difficulties, such as the effects of climate change and cassava plantation intervention, as shown in Figure 4.

Climate change is a real threat in coffee production around the world. According to the NASA and various known research centers, each year global temperature is getting higher, and the arctic glacier continues to melt, which causes the rising of sea level. There have been many extreme disaster events that are affecting livelihoods such as typhoons, hurricanes, earthquakes, heatwaves, landslides, floods, drought, etc. According to the data from the Meteorology and Hydrology Office (Provincial Department of Natural Resource and Environment in Xieng Khouang and Champasak), the temperature has increased and rainfall patterns have changed, all of which directly affected coffee quantity and quality. Coffee plantations are affected by these changes, particularly farmers who depend on natural sources of water.

QUALITATIVE RESULTS

Based on author’s observation and findings from the Focus Group Discussions (FGDs) and the Key Informant Interviews (KIIs) (Appendix 1), Lao coffee producers may be classified into three tiers, namely Tier 1 (smallholder producers), Tier 2 (medium producers), and Tier 3 (large producers), as shown in Figure 5.

Although, there are efforts to improve the quality and quantity of coffee production, they are insufficient to support the coffee sector. Several challenges remain the same for more than a decade. According to FGDs and KIIs, coffee production in Laos is threatened by cash crop intervention, market orientation, labor insufficiency, and climate change.

CONCLUDING REMARKS

Coffee plantation has contributed to economic development of Laos over the past three decades. It offers an opportunity to improve local livelihoods by creating more jobs and income. At the macro level, coffee is one of the most famous agricultural exports of Laos, particularly the produce from Bolaven Plateau, which is located in the southern part of the country. The widespread expansion of coffee plantation has gradually emerged in mountainous areas of the north as well. Currently, Lao coffee production is facing many challenges both from external and internal threats. With respect to external factors, climate change is threatening coffee production. With respect to internal factors, cassava boom intervenes with coffee plantation and causes soil deterioration. It is suggested that the government should determine zoning to strengthen coffee plantation and restrict crop boom that causes vulnerable soil. The government aspires to determine zoning based on geography, areas, and market access potential in order to enhance agricultural production for exports. There are four types of plantation areas, such as rice paddy, biennial plant area, fruit tree plantation area, and pasture. In addition, raising climate change awareness is an essential to help local producers adapt and improve their production. Lao coffee sector development should be paralleled with other potential crops that offer more gains and less effect, particularly soil deterioration.

Despite cassava intervention, market limitation, labor shortage, and climate change, smallholder farmers also have weak bargaining in contract farming enforcement, leading to suppression of prices. Coffee farmer/production group should be improved to support local growers in terms of production techniques, training, credits, and markets. The government should progressively deepen its support and assistance to enhance farmers’ production groups, improve business environment, and facilitate procedures for coffee produce and exports. More importantly, the government should maintain and broaden its coffee market locally and internationally. This should be in parallel with the development of other potential agricultural produce that contribute to improve local livelihoods and economy.

REFERENCES

ASEAN Stats (2022). International Merchandise Trade Statistics (IMTS): ASEAN Stats Data Portal. Retrieved from https://data.aseanstats.org/trade. Accessed 12 October 2022.

Enterprise & Development Consultants. (2016). “Non-Tariff Measures (NTMs) Faced by Exporters of Lao PDR: A Field Survey Report”. Project Report, Vientiane.

FAO. (2022). FAOSTAT. Retrieved from: http://www.fao.org/faostat/en/#data. Accessed on 12 October 2022.

ICO. (2020). Historical Data on the Global Coffee Trade. Retrieved from: http://www.ico.org/new_historical.asp?section=Statistics. Accessed 12 October 2022.

JICA. (2012). “Lao People’s Democratic Republic: Data Collection Survey on Selecting the Processed Food to Be Focused and Promoting Foreign Direct Investment in Food Business in Laos”. Final Report.

Lao Coffee Association. (2014). “2025 Strategy of Lao Coffee Promotion”. Vientiane Capital. [in Lao language].

LSB. (2022). 2021 Annual Statistics. Lao Statistics Bureau, Ministry of Planning and Investment.

Phommavong, S., Ounmany, K., & Hathalong, K. (2015). “Mapping context of land use for a non-traditional agricultural export (NTAE) product: case study of land use for coffee plantation in Pakxong district, Champasak province, Lao PDR”. Conference Paper Np. 75. An International Academic Conference on Land grabbing, conflict and agrarian-environmental transformations: perspectives from East and Southeast Asia. Chiang Mai University. 5-6 June 2015.

Saysana, V. (2011). “Promoting organic and fair trade certification in the Lao PDR coffee sector: Benefits and challenges for farmers and local economies”. Master Dissertation, Faculty of the Graduate College, Oklahoma State University, July 2011.

Seneduangdeth, D., et al. (2018). Labor employment opportunities in coffee production in southern Lao People’s Democratic Republic. Journal of Asian Rural Studies, Vol 2 (1), pp 16-36.

Southichack, M. (2009). “The Lao Coffee Economy: A New Growth Path on the Horizon?”. Vientiane.

Toro, M. (2012). “Coffee Markets, Smallholder Credit, and Landscape Changes in the Bolaven Plateau Region, Laos”. Master Thesis, University of Miami, May 2012.

World Bank. (2022). GDP (current US$) – Lao PDR. Retrieved from: https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=LA. Accessed 12 October 2022.

World Bank, & Global Development Solutions, LLC. (2005). “Integrated Value Chain Analysis of Selected Strategic Sectors in Lao People’s Democratic Republic”. Report.

[1] US$1 is equivalent to 11,159 kip, as Bank of Lao PDR’s average reference rate in January 2022.