ABSTRACT

Food industry significantly contributed to industrial GDP of Thailand with a strong backward linkage to the agricultural sector, the foundation of Thai economy. In general, Thai households have spent 33.9% of total expenditures on foods and beverages. Previously, Thai consumers focused on emotional value over than functional value since preferences and tastes became the major factors affecting their decisions to consume food products, rather than cleanliness and nutrition. The Coronavirus pandemic had not only brought a serious effect on the lives and livelihoods of people, but also the food consumption of the Thai people. During the spread of coronavirus pandemic since January 2020, it was found that consumer behaviors were starting to shape the so-called “New Normal” lifestyles. The crisis, however, affected many consumers to change their behaviors and their new experiences as shift to fundamental health and caring economy. It is essential to consider key behaviors going through the prolonged recovery period; health conscious, digitalization, sanitization, balancing of home and duty and personalized food supply that would become the “New Normal” for Thais affecting food consumptions. As Thai consumers put their cautiousness about health and self-immunity, higher digital engagement, online purchasing and hygienic practices, the food industry needs to observe closely in order to be well-prepared of any changes to meet the needs of consumers. This research aims to review the data of the food industry in Thailand, food consumption amid the Coronavirus pandemic, the “New normal” lifestyle of food consumption and key challenges for the food businesses are presented.

Keywords: Coronavirus, Thai food industry, food consumption, new normal, key challenges

INTRODUCTION

Food industry in Thailand

Thailand has long been called “the kitchen of the world” with a significant mark in the global food industry. In 2019, Food industry contributed US$ 29,479 million, approximately 5.5% of Thailand’s GDP and 20.6% of Thai industrial GDP (Food Intelligence Center, 2020). With a strong backward linkage to agricultural sector, the foundation of Thai economy, over 80% of raw material being used in the food industry was locally sourced from the agricultural sector. The total revenue for the Thai food industry was forecasted at US$ 54,420 million in 2020 with an average revenue per capital was US$ 779.66. The market is expected to grow annually by 2.6% (Statista, 2020). The number of food processing manufacturers have registered for 53,642 factories with one million workers who were employed, approximately 19.7% of total industrial sector employment (The Federation of Thai Industries, 2020). Food Intelligence Center (2020) reported that in 2019, the Thai food sector contributed 20.6% to the total industrial GDP while electricity and electronics, automobile, chemical and textile industries were at 13.6%, 11.2%, 9.0% and 4.7%, respectively.

According to Statista (2020), the food market included all kinds of fresh and processed foods. The market was divided into several segments; dairy products and eggs, meat, fish and seafood, vegetables, fruits, bread and cereal products, oils and fats, spreads and sweeteners, sauces and condiments, convenience food, confectionery and snacks, baby and pet foods. Based on the advancement of processing technology, processed foods were categorized into three general categories, which were minimally processed, moderately processed, and highly processed foods (Thailand Board of Investment, 2018). Currently, the food business invested a large amount of resources in research and development in order to boost their productivity and efficiency and innovative creation such as using computerized systems to control the production processes; for example, ready-to-eat meals and conveniently packaged meat and meat products.

Urbanization and hectic lifestyles were the main drivers of consumer purchases of highly processed foods. In addition, the supporting industries including food machinery and equipment, intelligent food packaging and digitalized food services also played significant roles to accelerate the growth rate of the modern food industry. With the growth in smart technologies, entrepreneurs had found several ways to merge technology with food and delivery services. Euromonitor International (2020) reported that there is a market value of key highly processed food segments including ready-to-eat meals (US$ 616 million), functional drinks (US$ 1,802.80 million), healthy foods (US$ 5,980.94 million), supplement and medical foods (US$ 800 million).

Food consumption of households in Thailand

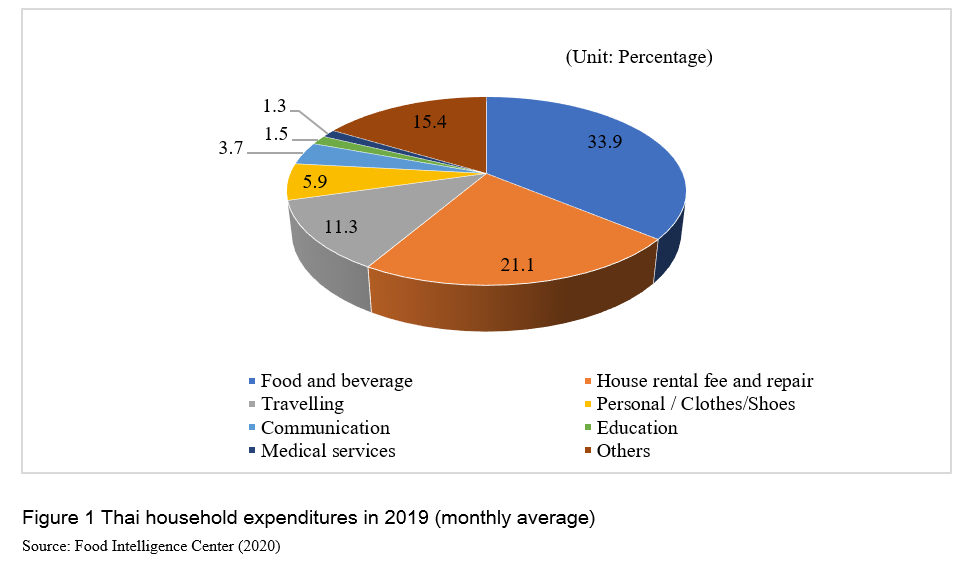

In 2019, Thailand households’ total expenditure amounted to US$ 659.31 per month, while expenditure on foods and beverages accounted the largest amount at US$ 223.52 or 33.9% of total expenses (Food Intelligence Center, 2020) as shown on Figure 1.

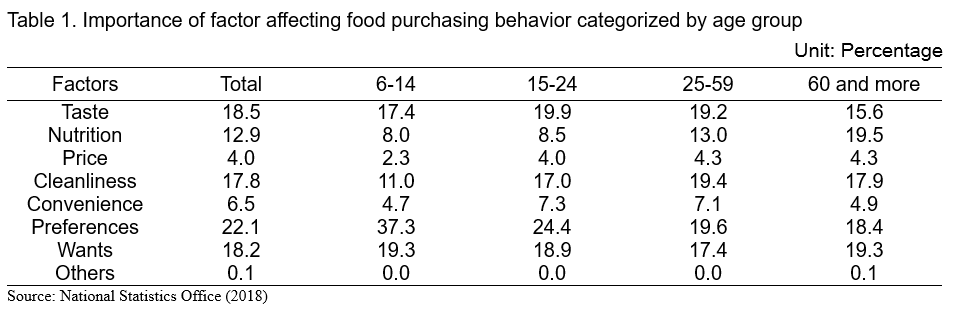

According to the National Statistics Office survey in 2017, with 28,000 Thai households (National Statistics Office, 2018), the most concern for food consumption of Thai population (above 6 years old) were preference (22.1%) followed by taste (18.5%) and want (18.2%), respectively. Considering the concept of value analysis (Smith and Colgate (2007), perceived value can be divided into 4 types: functional, emotional and experiences, symbolic and cost value. Based on the National Statistics Office survey, it can be implied that in general, the Thais gave importance to emotional value over functional value since they consumed foods based on their preferences rather than cleanliness and nutrition of foods (Table 1). Siam Commercial Bank Economic Intelligence Center (2020) reported that Thai people consumed more sweets and salty foods and reduced the frequency of their consumption for fruits and vegetables. There was an increasing number of Consumers who reduced their food consumption in their diets. Furthermore, there was also a marked increase in dietary and food supplements in Thai consumers. The study of food consumption behavior of working age people in Bangkok (2019) indicated that convenience was the most critical factor for food consumption and ready-to-eat meals was the most favorite kind of foods among the working people in Bangkok (Phanwattana, 2019). Both of the studies agreed that emotional and experience value was the critical factor for the Thai people.

FOOD CONSUMPTION AMID COVID-19 PANDEMIC

Since COVID-19 hit Thailand in early 2020, the Thai economy was projected to contract by at least 5% in 2020 due to the weaker global demand, no international tourists arrived and causing a decrease in private consumption which had the retail and recreation sectors getting the most impact (World Bank, 2020). Lockdowns and social distancing measures affected domestic spending especially face-to-face businesses including tourism, travel, recreation, horeca, as well as high-priced items (Siam Commercial Bank Economic Intelligence Center, 2020a). The Thai government had the policy to issue measures to help businesses and the public, with packages amounting to 12.9% of GDP focusing on providing relief to vulnerable households and affected firms. The packages included the relief measures of cash transfers to households and infrastructure projects in the local economy and several instruments (World Bank, 2020).

Siam Commercial Bank Economic Intelligence Center (2020b) reported the COVID-19 impact by industry. Food and beverage industry relatively got less affected from the crisis due to the lockdown and social distance measures than other industries. According to Nielsen Retail Index, FMCG (Fast Moving Consumer Goods) market growth during February-March 2020 significantly increased through all channels from modern to traditional trade. Considering food and beverage products, it was found that shelf-stable and ingredients presented the drastic growth, particularly eggs, edible oil, rice, canned fish, functional drink, instant noodles, sugar, instant coffee and biscuits (The MOMENTUM, 2020). Thai Consumers responded to the lockdown by stocking up their shelves with stable foods while reducing the consumption of luxury foods such as bird’s nest drink, energy drink, candies and snack foods.

Regarding consumption behaviors and lifestyles, Thai consumers have changed their habits during the crisis as seen from the survey of “Suan Dusit Poll” (Chalauysup, 2020). Thais were staying home (89.60%), had more concern for health (85.30%), considered food nutrition when purchasing foods (62.77%) and increased their social network communication (59.16%). Insights of consumer behavior during the COVID-19 pandemic was conducted by Wunderman Thompson and DATTEL (Marketing Oops, 2020) and it was found that food and beverage products were continually purchased with the same quantity or more. Instant noodles were the most increased purchasing product, which rose up to 52%. Convenient stores were considered to be the most preferred channel to purchase and online channel was increasing in transactions among middle income consumers.

The noticeably changing lifestyle and consumption behavior of the Thai people during the COVID-19 pandemic is summarized in Table 2.

Table 2. The changing lifestyle and consumption behavior of Thai people during the COVID-19 pandemic

|

Lifestyle and behavior

|

What/How they consumed

|

Example

|

- Work from home: Consumers connected to the world by internet and do food online shopping. (even senior)

|

- Consumers purchased from new E-marketplaces and social commerce e.g. E-marketplace of universities, school and institution. The case of University marketplace showed that the total sales increased up to 90%. (RYT9, 2020)

- Food delivery service was pervasive.

- E-payment became more popular for cashless society.

|

|

- Consumers were getting used to physical distancing.

- Consumer considered individual food consumption.

|

- Consumers were seeking for fulfillment in their homes e.g. fun and healthy cooking, brewing special coffee or juice or growing backyard with vegetables or flowers.

The report from online platform mentioned that cooking at home was the top 5 activities of Thai consumers during the COVID-19 pandemic (MGR online, 2020

- Consumers preferred to consume fast foods and use online media at home

|

|

- Consumer’s happiness was redefined.

- Consumers bought new luxuries at home e.g. cooking utensils are trendy and healthy.

|

- Consumer’s cooking and using new utensils became a part of maximizing that happiness. As a result, the growth rate of utensils bought increased 63% during COVID-19. (Smart SME Channel, 2020)

|

|

- Consumer’s state of mind focused and family mattered more.

- New activities with families at home e.g. cooking at home that brought family together.

|

- Consumers favored of DIY snack foods or bakeries at home.

- Meal kits were increasing in demand. There was an evidence that many famous restaurants launched the new meal kits during the COVID-19 pandemic (Wongnai, 2020).

|

|

- Consumers raised bar for health and wellness so they prioritized on food safety.

- Consumers focused on higher personal hygiene than ever before.

- Consumers were afraid of transmission of diseases from animals

|

- Consumers provided trust on safety of goods or services. The famous restaurants announced the safety plan to encourage sanitization and safety. (Posttoday, 2020)

- Consumers selected safe foods, safe packaging, safe delivery and traceability.

- Consumers preferred foods with natural ingredients and locally sourced.

- Consumers preferred plant- based protein, immune boosting foods e.g. herbal, functional foods and beverages.

|

|

Source: GroupM Thailand (2020) DATTEL (2020) Author’s analysis

Photo source: Family Bites (2011), Siam PR (2014), Anonymous (2015), RYT9 (2019) Anonymous (2020a), Anonymous (2020b), Central (2020), Destination Riyadh (2015), Entrepreneur Asia Pacific (2020), Johns Hopkins Medicine (2020), Kitchn (2020) and Google site (2020)

“NEW NORMAL” LIFESTYLE OF FOOD CONSUMPTION

The COVID-19 pandemic has shown that Thai consumers’ lifestyle and behavior were remarkable adaptive to this uncertainty. In the short term, consumers initially prepared by purchasing storable food stocks for lockdown, increased online purchase of foods and home deliveries in order to align with social distancing, awareness of the benefits from a healthier diets and lifestyle and etc. In the long run, consumer experiences may have taken on a new dimension from changing their perspective, attitude and lifestyle until getting used to a completely changing environment (Brand Buffet, 2020). Since the COVID-19 pandemic led to consumer adaptation to the “New Normal” lifestyle and behavior, it is expected that the “New Normal” will occur in the post COVID-19 era. It is essential to identify some key “New Normal” lifestyle of Thais food consumption behavior:

- Being health conscious: Consumers give an attention on preventive healthcare. Generation Y people are increasingly focusing on healthcare and expanding across all generations. This may cause from the data reporting that being healthy can protect yourself from viruses (Boonyen, 2020). Group M Thailand (2020) reported that Thais will become more rationale consumers. They will choose to buy more healthy and sanitary products such as fresh produce to cook at home and beverages that can strengthen the immune system. As a result, the demand for functional foods and beverages and herbal supplements for immunity enhancement will continue to rise.

- Digitalization: The digital world will not just be a part of life, but there is now such a thing as a digital life. (Brand Buffet, 2020). This behavioral change is partly caused by practicing social distance by staying or working at home. Consumers use mobile phones or online media as a life facilitator for convenient lifestyle ranging from purchasing household products, foods, and other essential appliances. It can be said that there is no barrier between purchasing from the store and online anymore or Online-Merge-Offline (OMO) (Group M Thailand, 2020). After this crisis has ended, it can be predicted that consumers will continue to enjoy purchasing products online and foreseeing the sales of ready-to-eat, fast and convenient foods from E-commerce. This trend has been predicted to continually increase.

- Sanitization: Consumers will continue embracing physical distancing and less of human touch. Personal product for self-sanitation will continue to become a usual behavior, with an extension of consumer expectation for all shops to facilitate cleanliness and hygiene. Consumers also expect stores to place hand sanitizers as well as cleanliness guaranteed packaging. Personal space and touchless self-service will create a new shopping experience. Research from Kantar (Group M Thailand, 2020) showed that 65% of Thais are more concerned about food safety and country of origin. Consumers prefer to select natural ingredients and locally sourced food, safe packaging, safe delivery and food traceability system.

- Balancing of home and duty: After working at home for a certain period of time, consumers or employees begin to better understand the meaning of balancing work and personal life. Consumers consider working from home in order to manage life efficiently which is possible in the future. As this situation has evolved, where and how consumers are eating has changed, with more choices to purchase foods to eat at home and food delivery will become more pervasive (Nielsen, 2020). Urban lifestyle consumers prefer to purchase from E-marketplaces, E-retailers and social commerce beyond the traditional offline stores. Further, Do It Yourself (D.I.Y) snack foods, homemade bakery and meal kits will increase in demand as a result of the physical reconnection of the family, particularly, family with young children.

- Personalized food supply: Consumers pay more attention to personalization in food choices. They will carefully search for details and ingredients when choosing to buy food products, aside from considering price or benefit (IPG Mediabrands, 2020). The demand for food solution or designed food to meet the unique needs of each individual may become more attractive, for examples, vegan foods, plant-based protein, food for diabetes, gluten-free and organic foods. Thus, highly processed foods with biotechnology, supplement and medical foods will be aligned with consumer preferences and become an alternative for consumer wellness.

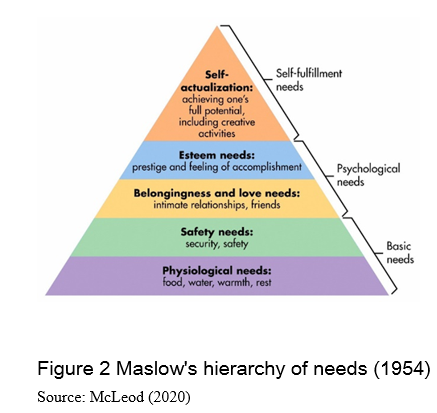

The shift of customer experiences to the “New Normal” lifestyle that resulted from the pandemic crisis may change consumer preferences for food consumption in the future since consumers became aware of their health and wellness. They focused more on sanitization of food consumption. Maslow's hierarchy of needs (Figure 2) is a theory of human motivation which can be used to analyze the need for food consumption of Thai consumers towards the “New Normal” lifestyle.

Considering Maslow’s Hierarchy of Needs (1954), the Thai consumers will return to focus on the basic needs that are Physiological needs. Consumers would prefer to spend on food consumption focusing on value for money over than aesthetic and premium prices. In addition, they will give priority to security and safety needs with the consumption of clean, safe, nutritious foods in order to protect their families and do self-caring activity more than ever. Moreover, consumers focus more on sanitization of food consumption. These behaviors represented the new normal of being health conscious, and sanitated and personalized food supply. For love and belonging needs, consumers are more connected with others through digitalization and purchased foods from E-commerce because of physical distancing. Paranoia in the virus causes consumers to buy food to be consumed at home and purchase food ingredients to cook for themselves. The COVID-19 pandemic becomes a major catalyst, causing consumers to focus their immune systems in order to have preventive actions against the pandemic. As a result, ready-to-cook, ready-to-eat, semi-processed and storable foods with longer shelf life and nutritious and healthy foods begin to have a higher consumption growth rate. Fresh and healthy fruits and vegetables are rising in demand as well. Finally, they will give relatively less importance to esteem and self-actualization needs than ever in the past.

The “New Normal” lifestyle has shown that Thai people are facing an uncertainty from the crisis so they focus on the fundamentals of care and concern (McKinsey and Company, 2020). People need to keep their families safe from the foods they can trust. It can be concluded that food consumption behavior moves toward the selection of cooking ingredients and looking for the menu that provide nutrition and meet sanitary standards. Consumers will choose the food retails and food services which show high standard of hygiene and cleanliness. The use of individual spoons will become a common way of dining habit that all consumers are happy to do. They will be careful when choosing to eat any kinds of meat that they are not familiar with. Local brand foods and beverages would become more in demand as a result of trust and traceable products. Finally, physical distancing causes an increased consumption of online media and significantly accelerated E-commerce of food business.

KEY CHALLENGES FOR FOOD BUSINESS

Since Thailand had confirmed the first Corona virus case on January 13, 2020, by the Ministry of Public Health, the pandemic could take a long time to recover, which will shape consumer behaviors to the “New Normal”. While Thai consumers were anxious of the future, they were preparing and taking precautions to adjust themselves to a new way of living. The food businesses need to be observed more closely in order to be well-prepared for any changes that the future may bring. The impact of COVID-19 pandemic that causes the challenges related to strategic issues for food businesses need to be considered as:

- Key challenges for food manufacturers

The research reveals that Thai consumers’ purchasing decision are staked more on a brand's value proposition, more than just simply price (GroupM Thailand, 2020). Since consumers pay more attention to the quality and safety of the product. Therefore, it is not only a challenge, but also an opportunity for quality competition instead of price. Food manufacturers need to prepare upgrading the supply chain and logistic operations to become proactively aligned with suppliers and prepare for the rebound in consumption. Building online merges with offline (OMO) marketing, digital capabilities and continuously innovate business models need to be focused. Food manufacturers are facing challenges such as 1) require safer and higher standards for production, 2) encourage on local consumers and domestic consumptions, 3) understand consumer lifestyles and behaviors, 4) apply digitalization system and E-commerce, 5) develop technology and cold chain for perishable products and fresh food delivery, 6) develop packaging to increase shelf life, 7) innovate processed foods for healthy and immune boosting system, and 8) create brand trust and traceability system.

- Key challenges for food retails

Food retail values in the Asian market has increased up to 20-25% per week since January 2020 (Food Intelligence Unit, 2020). However, Thai consumers have shown an increase in online spending across a variety of goods and services, with 41% of consumers who reported using a food delivery service during the crisis (GroupM Thailand, 2020). Similarly, home delivery has gone from a convenience to a necessity since consumers reduced a number of shops visiting trips. Rapid development of digital functionalities is a key to ensuring continuity of food retails after the crisis. Food retails are facing the following challenges: 1) seek for safer and higher standards of product and stores; 2) offer health and wellness values; 3) build a strong foundation for E-commerce to meet the customer demand; 4) use data analytics with customers big data for identifying personalized solutions; 5) find partnerships in logistics service providers 6) strengthen online merges with offline channel (OMO); and 7) design for innovation such as virtual store and lifestyle mall.

- Key challenges for food services (Restaurant)

The food service sector is highly affected by the lockdown and emergency decrees announcement during the crisis. Nielsen (2020) found a high demand for more takeaway and home deliveries of foods in Thailand. Many consumers used to eat out at the restaurant, but home cooking has become a new habit that the Thai people will need to adjust. Hence, on-the-go lifestyles and value the convenience of on-the-go food offerings will be highly demanded, especially by urban consumers. The restaurants and other out-of-home businesses need to consider adjusting their stores to meet the new demand. Food services are facing challenges such as 1) going online and service delivery with digital platform, 2) being used to restaurant signature dishes appearing on shelves, 3) seeking for safer and higher standards for products and services, 4) adapting to hygienic and social distancing measures, and 5) having food deliveries with microwaveable packaging, hygienic packaging or sealed personalized packaging.

CONCLUSION

In Thailand, the food industry has a strong backward linkage to agricultural sector with 80% of locally sourced raw materials. The Thai food market is expected to grow annually by 2.6% and Thai households paid 33.9% of total expenditure on foods and beverages. In 2018, National Statistics Office (NSO) reported that Thai consumers gave importance on emotional value over than functional value since they consumed foods based on preferences and tastes rather than cleanliness and nutrition. During the spread of coronavirus pandemic in Thailand, it was found that consumer behaviors were starting to shape to the “New Normal” lifestyles. After the coronavirus situation has evolved, food consumption behavior has been changed for both pattern and diet choices upon their lifestyles. Consumers raised their concerns on health and wellness so they prioritized on food safety and personal hygiene than ever before. Five types of behavior can be foreseen going through the prolonged recovery period: health consciousness, digitalization, sanitization, balancing of home and duty and personalized food supply that would become the “New Normal” for Thais regarding food consumption. Even people return to their daily routines, but there will be focus on cautiousness about health and self-immunity, higher digital engagement, online purchasing and hygienic practices. Dealing with the COVID-19 crisis and its aftermath could be the biggest challenging tasks for the food industry. All food businesses including food manufacturers, food retailers and food services are confronting this “New Normal” changing consumer behavior. In general, the Thai food industry must aim to have higher food safety or create food safety culture, increase in brand trust on food quality, and promote hygiene and safety. The drive towards digital transformation of food business sector needs to be considered to achieve the business development in the “New Normal Era”.

REFERENCES

Anonymous. 2015. Healthy Foods. Available from http://healthfoodbymin.blogspot.com/. [Accessed 13 September 2020].

Anonymous. 2020a. KU Market Place. Available from www.facebook.com/groups/210008013625799/about/. [Accessed 13 September 2020].

Anonymous. 2020b. Chula Market Place. Available from www.facebook.com/groups/1162370287441092/. [Accessed 13 September 2020].

Boonyen, K. 2020. Never the same again 8 Consumer Behavior Changes to New Normal. Available from http://www.bizpromptinfo.com/-พฤติกรรมผู้บริโภค-new-normal/. [Accessed 21 July 2020].

Brand Buffet. 2020. 4D+1H Consumer Behavior, New Normal, Post Covid-19 Era. Available from https://www.brandbuffet.in.th/2020/04/new-normal-in-post-covid19-era-by-.... [Accessed 21 July 2020].

Central. 2020. Product selling. Available from www.central.co.th/th/tefal-ey201866-1200-cds21925979. [Accessed 13 September 2020].

Chalauysup, S. 2020. Behaviors of Thais during Crisis Covid-19. Siamrath. 9 April 2020.

DATTEL. 2020. COVID-19 Insights Circle (CIC) Reimagines Consumers in ASEAN. Available from https://www.dattel.asia/covid-19-insights-circle-cic-reimagines-consumer.... [Accessed 21 July 2020].

Destination Riyadh. 2015. 30 Nights of Ramadan Fun for The Whole Family. Available from destinationksa.com/30-nights-of-ramadan-fun-for-the-whole-family/. [Accessed 13 September 2020].

Entrepreneur Asia Pacific. 2020. How to support your team while WFH. Available from www.entrepreneur.com/article/348270. [Accessed 13 September 2020].

Family Bites. 2011. DIY: Ice Cream Sundae Kit. Available from www.familybites.ca/2011/06/diy-ice-cream-sundae-kit.html?pintix=1. [Accessed 13 September 2020].

Food Intelligence Center. 2020. Thailand Food Industry Profile 2019. National Food Institute, Thailand. Available from http://fic.nfi.or.th/info_graphic_detail.php?id=28 . [Accessed 20 July 2020].

Google site. 2020. Type of social media. Available from sites.google.com/site/tanyapornparakornwatthana/laksna-khxng-social-media. [Accessed 13 September 2020].

GroupM Thailand. 2020. Social Distancing and the Impact on Thai Consumer Behaviors. Available from http://www.groupmthailand.com/insightm/home/view/176. [Accessed 21 July 2020].

IPG Mediabrands. 2020. Envisioning Post COVID-19 Pandemic in Thailand The Era of Distance: Consumers with Emerging Behaviors Creating the “New Normal” to Last in Thai Society. Available from ipg-connect.com/covid-19-กับยุคของ-d●i●s●t●a●n●c●e-consumers-8-พฤ/. [Accessed 21 July 2020].

Johns Hopkins Medicine. 2020. Patient Safety and Quality. Available from www.hopkinsmedicine.org/patient_safety/infection_prevention/hand_hygiene... [Accessed 13 September 2020].

Kitchn. 2020. How to Make the Easiest Pancakes Ever. Available from www.thekitchn.com/pancakes-recipe-263226. [Accessed 13 September 2020].

Maslow, A. H. 1954. Motivation and personality. New York: Harper & Row.

Marketing Oops. 2020. Insights of Thai Purchasing Behavior on FMCG-High Involvement-Retail Before-During-After Covid-19. Available from https://www.marketingoops.com/reports/consumer-insights-and-purchase-beh... [Accessed 21 July 2020].

Mckinsey and Company. 2020. Adapting customer experience in the time of coronavirus. Available from https://www.mckinsey.com/business-functions/marketing-and-sales/our-insi... [Accessed 21 July 2020].

McLeod, S. 2020. Maslow’s Hierarchy of Needs. Available from www.simplypsychology.org/maslow.html. [Accessed 10 Sep 2020].

MGR online. 2020. Twitter: 5 popular trends during Covid 19. Available from https://mgronline.com/cyberbiz/detail/9630000060823. [Accessed 10 Sep 2020].

National Statistics Office. 2018. Survey on food consumption of Thai population in 2017. Executive Summary, 1-3.

Nielsen. 2020. Asian Consumers are Rethinking how they eat Post Covid-19. Available from https://www.nielsen.com/eu/en/insights/article/2020/asian-consumers-are-rethinking-how-they-eat-post-covid-19/. [Accessed 18 July 2020].

Phanwattana, P.. 2019. Food consumption behavior of working age people in Bangkok. Journal of the Office of DPC 7 Khon Khann 26:2, 93-103.

Posttoday. 2020. Announcement of New Normal for Thai restaurant (S&P). Available from www.posttoday.com/life/travel/624106. [Accessed 10 Sep 2020].

RYT9. 2019. McDelivery Surprise. Available from www.ryt9.com/s/prg/3037301. [Accessed 13 September 2020].

RYT9. 2020. 3 Famous Online Market place “TU CU and KU”. Available from www.ryt9.com/s/prg/3132830. [Accessed 10 Sep 2020].

Siam Commercial Bank Economic Intelligence Center. 2020a. Thailand After Covid-19 Part 1: The Impact of the Economy and Thai Labor Market. Available from https://www.scb.co.th/en/personal-banking/stories/business-maker/thailand-after-covid-ep1.html. [Accessed 10 September 2020].

Siam Commercial Bank Economic Intelligence Center. 2020b. Thailand After Covid-19 Part 2: Business Opportunities and Survival. Available from https://www.scb.co.th/en/personal-banking/stories/business-maker/thailan... [Accessed 18 July 2020].

Siam PR. 2014. Online Shopping. Available from http://siampr.net/229/online-shopping. [Accessed 13 September 2020].

Smart SME Chanel. 2020. Why sale growth of utensils and gadget is increase during Covid 19? Available from https://www.smartsme.co.th/content/237232. [Accessed 20 May 2020].

Smith J. B. and M. Colgate (2007) Customer Value Creation: A Practical Framework. Journal of Marketing Theory and Practice. 15:1, 7-23.

Statista. 2020. Consumer Market Outlook of Food in 2020: Thailand. Available from https://www.statista.com/outlook/40000000/126/food/thailand. [Accessed 20 July 2020].

The Federation of Thai Industries. 2020. Thai Food Industry Amid Covvid-19...Rise or Fall? Food Focus Virtual Connect. 21 April 2020.

Thailand Board of Investment. 2018. Thailand Food Industry. Available from https://www.boi.go.th/upload/content/Food%20industry_5aa7b40bd758b.pdf. [Accessed 18 July 2020].

The MOMENTUM. 2020. Looking at the minds of consumers through product purchased during Covid-19: Will the world never be the same? April 7, 2020. Available from https://themomentum.co/covid-19-change-consumer-behavior/. [Accessed 21 July 2020].

Wongnai. 2020. 4 Product idea launched during Covid 19. Available from www.wongnai.com/business-owners/new-products-during-covid19. [Accessed 10 Sep 2020].

World Bank. 2020. Thailand Economic Monitor June 2020: Thailand in the Time of Covid-19. Available from https://www.worldbank.org/en/country/thailand/publication/thailand-economic-monitor-june-2020-thailand-in-the-time-of-covid-19. [Accessed 10 September 2020]

Towards the New Normal Lifestyle of Food Consumption in Thailand

ABSTRACT

Food industry significantly contributed to industrial GDP of Thailand with a strong backward linkage to the agricultural sector, the foundation of Thai economy. In general, Thai households have spent 33.9% of total expenditures on foods and beverages. Previously, Thai consumers focused on emotional value over than functional value since preferences and tastes became the major factors affecting their decisions to consume food products, rather than cleanliness and nutrition. The Coronavirus pandemic had not only brought a serious effect on the lives and livelihoods of people, but also the food consumption of the Thai people. During the spread of coronavirus pandemic since January 2020, it was found that consumer behaviors were starting to shape the so-called “New Normal” lifestyles. The crisis, however, affected many consumers to change their behaviors and their new experiences as shift to fundamental health and caring economy. It is essential to consider key behaviors going through the prolonged recovery period; health conscious, digitalization, sanitization, balancing of home and duty and personalized food supply that would become the “New Normal” for Thais affecting food consumptions. As Thai consumers put their cautiousness about health and self-immunity, higher digital engagement, online purchasing and hygienic practices, the food industry needs to observe closely in order to be well-prepared of any changes to meet the needs of consumers. This research aims to review the data of the food industry in Thailand, food consumption amid the Coronavirus pandemic, the “New normal” lifestyle of food consumption and key challenges for the food businesses are presented.

Keywords: Coronavirus, Thai food industry, food consumption, new normal, key challenges

INTRODUCTION

Food industry in Thailand

Thailand has long been called “the kitchen of the world” with a significant mark in the global food industry. In 2019, Food industry contributed US$ 29,479 million, approximately 5.5% of Thailand’s GDP and 20.6% of Thai industrial GDP (Food Intelligence Center, 2020). With a strong backward linkage to agricultural sector, the foundation of Thai economy, over 80% of raw material being used in the food industry was locally sourced from the agricultural sector. The total revenue for the Thai food industry was forecasted at US$ 54,420 million in 2020 with an average revenue per capital was US$ 779.66. The market is expected to grow annually by 2.6% (Statista, 2020). The number of food processing manufacturers have registered for 53,642 factories with one million workers who were employed, approximately 19.7% of total industrial sector employment (The Federation of Thai Industries, 2020). Food Intelligence Center (2020) reported that in 2019, the Thai food sector contributed 20.6% to the total industrial GDP while electricity and electronics, automobile, chemical and textile industries were at 13.6%, 11.2%, 9.0% and 4.7%, respectively.

According to Statista (2020), the food market included all kinds of fresh and processed foods. The market was divided into several segments; dairy products and eggs, meat, fish and seafood, vegetables, fruits, bread and cereal products, oils and fats, spreads and sweeteners, sauces and condiments, convenience food, confectionery and snacks, baby and pet foods. Based on the advancement of processing technology, processed foods were categorized into three general categories, which were minimally processed, moderately processed, and highly processed foods (Thailand Board of Investment, 2018). Currently, the food business invested a large amount of resources in research and development in order to boost their productivity and efficiency and innovative creation such as using computerized systems to control the production processes; for example, ready-to-eat meals and conveniently packaged meat and meat products.

Urbanization and hectic lifestyles were the main drivers of consumer purchases of highly processed foods. In addition, the supporting industries including food machinery and equipment, intelligent food packaging and digitalized food services also played significant roles to accelerate the growth rate of the modern food industry. With the growth in smart technologies, entrepreneurs had found several ways to merge technology with food and delivery services. Euromonitor International (2020) reported that there is a market value of key highly processed food segments including ready-to-eat meals (US$ 616 million), functional drinks (US$ 1,802.80 million), healthy foods (US$ 5,980.94 million), supplement and medical foods (US$ 800 million).

Food consumption of households in Thailand

In 2019, Thailand households’ total expenditure amounted to US$ 659.31 per month, while expenditure on foods and beverages accounted the largest amount at US$ 223.52 or 33.9% of total expenses (Food Intelligence Center, 2020) as shown on Figure 1.

According to the National Statistics Office survey in 2017, with 28,000 Thai households (National Statistics Office, 2018), the most concern for food consumption of Thai population (above 6 years old) were preference (22.1%) followed by taste (18.5%) and want (18.2%), respectively. Considering the concept of value analysis (Smith and Colgate (2007), perceived value can be divided into 4 types: functional, emotional and experiences, symbolic and cost value. Based on the National Statistics Office survey, it can be implied that in general, the Thais gave importance to emotional value over functional value since they consumed foods based on their preferences rather than cleanliness and nutrition of foods (Table 1). Siam Commercial Bank Economic Intelligence Center (2020) reported that Thai people consumed more sweets and salty foods and reduced the frequency of their consumption for fruits and vegetables. There was an increasing number of Consumers who reduced their food consumption in their diets. Furthermore, there was also a marked increase in dietary and food supplements in Thai consumers. The study of food consumption behavior of working age people in Bangkok (2019) indicated that convenience was the most critical factor for food consumption and ready-to-eat meals was the most favorite kind of foods among the working people in Bangkok (Phanwattana, 2019). Both of the studies agreed that emotional and experience value was the critical factor for the Thai people.

FOOD CONSUMPTION AMID COVID-19 PANDEMIC

Since COVID-19 hit Thailand in early 2020, the Thai economy was projected to contract by at least 5% in 2020 due to the weaker global demand, no international tourists arrived and causing a decrease in private consumption which had the retail and recreation sectors getting the most impact (World Bank, 2020). Lockdowns and social distancing measures affected domestic spending especially face-to-face businesses including tourism, travel, recreation, horeca, as well as high-priced items (Siam Commercial Bank Economic Intelligence Center, 2020a). The Thai government had the policy to issue measures to help businesses and the public, with packages amounting to 12.9% of GDP focusing on providing relief to vulnerable households and affected firms. The packages included the relief measures of cash transfers to households and infrastructure projects in the local economy and several instruments (World Bank, 2020).

Siam Commercial Bank Economic Intelligence Center (2020b) reported the COVID-19 impact by industry. Food and beverage industry relatively got less affected from the crisis due to the lockdown and social distance measures than other industries. According to Nielsen Retail Index, FMCG (Fast Moving Consumer Goods) market growth during February-March 2020 significantly increased through all channels from modern to traditional trade. Considering food and beverage products, it was found that shelf-stable and ingredients presented the drastic growth, particularly eggs, edible oil, rice, canned fish, functional drink, instant noodles, sugar, instant coffee and biscuits (The MOMENTUM, 2020). Thai Consumers responded to the lockdown by stocking up their shelves with stable foods while reducing the consumption of luxury foods such as bird’s nest drink, energy drink, candies and snack foods.

Regarding consumption behaviors and lifestyles, Thai consumers have changed their habits during the crisis as seen from the survey of “Suan Dusit Poll” (Chalauysup, 2020). Thais were staying home (89.60%), had more concern for health (85.30%), considered food nutrition when purchasing foods (62.77%) and increased their social network communication (59.16%). Insights of consumer behavior during the COVID-19 pandemic was conducted by Wunderman Thompson and DATTEL (Marketing Oops, 2020) and it was found that food and beverage products were continually purchased with the same quantity or more. Instant noodles were the most increased purchasing product, which rose up to 52%. Convenient stores were considered to be the most preferred channel to purchase and online channel was increasing in transactions among middle income consumers.

The noticeably changing lifestyle and consumption behavior of the Thai people during the COVID-19 pandemic is summarized in Table 2.

Table 2. The changing lifestyle and consumption behavior of Thai people during the COVID-19 pandemic

Lifestyle and behavior

What/How they consumed

Example

The report from online platform mentioned that cooking at home was the top 5 activities of Thai consumers during the COVID-19 pandemic (MGR online, 2020

Source: GroupM Thailand (2020) DATTEL (2020) Author’s analysis

Photo source: Family Bites (2011), Siam PR (2014), Anonymous (2015), RYT9 (2019) Anonymous (2020a), Anonymous (2020b), Central (2020), Destination Riyadh (2015), Entrepreneur Asia Pacific (2020), Johns Hopkins Medicine (2020), Kitchn (2020) and Google site (2020)

“NEW NORMAL” LIFESTYLE OF FOOD CONSUMPTION

The COVID-19 pandemic has shown that Thai consumers’ lifestyle and behavior were remarkable adaptive to this uncertainty. In the short term, consumers initially prepared by purchasing storable food stocks for lockdown, increased online purchase of foods and home deliveries in order to align with social distancing, awareness of the benefits from a healthier diets and lifestyle and etc. In the long run, consumer experiences may have taken on a new dimension from changing their perspective, attitude and lifestyle until getting used to a completely changing environment (Brand Buffet, 2020). Since the COVID-19 pandemic led to consumer adaptation to the “New Normal” lifestyle and behavior, it is expected that the “New Normal” will occur in the post COVID-19 era. It is essential to identify some key “New Normal” lifestyle of Thais food consumption behavior:

The shift of customer experiences to the “New Normal” lifestyle that resulted from the pandemic crisis may change consumer preferences for food consumption in the future since consumers became aware of their health and wellness. They focused more on sanitization of food consumption. Maslow's hierarchy of needs (Figure 2) is a theory of human motivation which can be used to analyze the need for food consumption of Thai consumers towards the “New Normal” lifestyle.

Considering Maslow’s Hierarchy of Needs (1954), the Thai consumers will return to focus on the basic needs that are Physiological needs. Consumers would prefer to spend on food consumption focusing on value for money over than aesthetic and premium prices. In addition, they will give priority to security and safety needs with the consumption of clean, safe, nutritious foods in order to protect their families and do self-caring activity more than ever. Moreover, consumers focus more on sanitization of food consumption. These behaviors represented the new normal of being health conscious, and sanitated and personalized food supply. For love and belonging needs, consumers are more connected with others through digitalization and purchased foods from E-commerce because of physical distancing. Paranoia in the virus causes consumers to buy food to be consumed at home and purchase food ingredients to cook for themselves. The COVID-19 pandemic becomes a major catalyst, causing consumers to focus their immune systems in order to have preventive actions against the pandemic. As a result, ready-to-cook, ready-to-eat, semi-processed and storable foods with longer shelf life and nutritious and healthy foods begin to have a higher consumption growth rate. Fresh and healthy fruits and vegetables are rising in demand as well. Finally, they will give relatively less importance to esteem and self-actualization needs than ever in the past.

The “New Normal” lifestyle has shown that Thai people are facing an uncertainty from the crisis so they focus on the fundamentals of care and concern (McKinsey and Company, 2020). People need to keep their families safe from the foods they can trust. It can be concluded that food consumption behavior moves toward the selection of cooking ingredients and looking for the menu that provide nutrition and meet sanitary standards. Consumers will choose the food retails and food services which show high standard of hygiene and cleanliness. The use of individual spoons will become a common way of dining habit that all consumers are happy to do. They will be careful when choosing to eat any kinds of meat that they are not familiar with. Local brand foods and beverages would become more in demand as a result of trust and traceable products. Finally, physical distancing causes an increased consumption of online media and significantly accelerated E-commerce of food business.

KEY CHALLENGES FOR FOOD BUSINESS

Since Thailand had confirmed the first Corona virus case on January 13, 2020, by the Ministry of Public Health, the pandemic could take a long time to recover, which will shape consumer behaviors to the “New Normal”. While Thai consumers were anxious of the future, they were preparing and taking precautions to adjust themselves to a new way of living. The food businesses need to be observed more closely in order to be well-prepared for any changes that the future may bring. The impact of COVID-19 pandemic that causes the challenges related to strategic issues for food businesses need to be considered as:

The research reveals that Thai consumers’ purchasing decision are staked more on a brand's value proposition, more than just simply price (GroupM Thailand, 2020). Since consumers pay more attention to the quality and safety of the product. Therefore, it is not only a challenge, but also an opportunity for quality competition instead of price. Food manufacturers need to prepare upgrading the supply chain and logistic operations to become proactively aligned with suppliers and prepare for the rebound in consumption. Building online merges with offline (OMO) marketing, digital capabilities and continuously innovate business models need to be focused. Food manufacturers are facing challenges such as 1) require safer and higher standards for production, 2) encourage on local consumers and domestic consumptions, 3) understand consumer lifestyles and behaviors, 4) apply digitalization system and E-commerce, 5) develop technology and cold chain for perishable products and fresh food delivery, 6) develop packaging to increase shelf life, 7) innovate processed foods for healthy and immune boosting system, and 8) create brand trust and traceability system.

Food retail values in the Asian market has increased up to 20-25% per week since January 2020 (Food Intelligence Unit, 2020). However, Thai consumers have shown an increase in online spending across a variety of goods and services, with 41% of consumers who reported using a food delivery service during the crisis (GroupM Thailand, 2020). Similarly, home delivery has gone from a convenience to a necessity since consumers reduced a number of shops visiting trips. Rapid development of digital functionalities is a key to ensuring continuity of food retails after the crisis. Food retails are facing the following challenges: 1) seek for safer and higher standards of product and stores; 2) offer health and wellness values; 3) build a strong foundation for E-commerce to meet the customer demand; 4) use data analytics with customers big data for identifying personalized solutions; 5) find partnerships in logistics service providers 6) strengthen online merges with offline channel (OMO); and 7) design for innovation such as virtual store and lifestyle mall.

The food service sector is highly affected by the lockdown and emergency decrees announcement during the crisis. Nielsen (2020) found a high demand for more takeaway and home deliveries of foods in Thailand. Many consumers used to eat out at the restaurant, but home cooking has become a new habit that the Thai people will need to adjust. Hence, on-the-go lifestyles and value the convenience of on-the-go food offerings will be highly demanded, especially by urban consumers. The restaurants and other out-of-home businesses need to consider adjusting their stores to meet the new demand. Food services are facing challenges such as 1) going online and service delivery with digital platform, 2) being used to restaurant signature dishes appearing on shelves, 3) seeking for safer and higher standards for products and services, 4) adapting to hygienic and social distancing measures, and 5) having food deliveries with microwaveable packaging, hygienic packaging or sealed personalized packaging.

CONCLUSION

In Thailand, the food industry has a strong backward linkage to agricultural sector with 80% of locally sourced raw materials. The Thai food market is expected to grow annually by 2.6% and Thai households paid 33.9% of total expenditure on foods and beverages. In 2018, National Statistics Office (NSO) reported that Thai consumers gave importance on emotional value over than functional value since they consumed foods based on preferences and tastes rather than cleanliness and nutrition. During the spread of coronavirus pandemic in Thailand, it was found that consumer behaviors were starting to shape to the “New Normal” lifestyles. After the coronavirus situation has evolved, food consumption behavior has been changed for both pattern and diet choices upon their lifestyles. Consumers raised their concerns on health and wellness so they prioritized on food safety and personal hygiene than ever before. Five types of behavior can be foreseen going through the prolonged recovery period: health consciousness, digitalization, sanitization, balancing of home and duty and personalized food supply that would become the “New Normal” for Thais regarding food consumption. Even people return to their daily routines, but there will be focus on cautiousness about health and self-immunity, higher digital engagement, online purchasing and hygienic practices. Dealing with the COVID-19 crisis and its aftermath could be the biggest challenging tasks for the food industry. All food businesses including food manufacturers, food retailers and food services are confronting this “New Normal” changing consumer behavior. In general, the Thai food industry must aim to have higher food safety or create food safety culture, increase in brand trust on food quality, and promote hygiene and safety. The drive towards digital transformation of food business sector needs to be considered to achieve the business development in the “New Normal Era”.

REFERENCES

Anonymous. 2015. Healthy Foods. Available from http://healthfoodbymin.blogspot.com/. [Accessed 13 September 2020].

Anonymous. 2020a. KU Market Place. Available from www.facebook.com/groups/210008013625799/about/. [Accessed 13 September 2020].

Anonymous. 2020b. Chula Market Place. Available from www.facebook.com/groups/1162370287441092/. [Accessed 13 September 2020].

Boonyen, K. 2020. Never the same again 8 Consumer Behavior Changes to New Normal. Available from http://www.bizpromptinfo.com/-พฤติกรรมผู้บริโภค-new-normal/. [Accessed 21 July 2020].

Brand Buffet. 2020. 4D+1H Consumer Behavior, New Normal, Post Covid-19 Era. Available from https://www.brandbuffet.in.th/2020/04/new-normal-in-post-covid19-era-by-.... [Accessed 21 July 2020].

Central. 2020. Product selling. Available from www.central.co.th/th/tefal-ey201866-1200-cds21925979. [Accessed 13 September 2020].

Chalauysup, S. 2020. Behaviors of Thais during Crisis Covid-19. Siamrath. 9 April 2020.

DATTEL. 2020. COVID-19 Insights Circle (CIC) Reimagines Consumers in ASEAN. Available from https://www.dattel.asia/covid-19-insights-circle-cic-reimagines-consumer.... [Accessed 21 July 2020].

Destination Riyadh. 2015. 30 Nights of Ramadan Fun for The Whole Family. Available from destinationksa.com/30-nights-of-ramadan-fun-for-the-whole-family/. [Accessed 13 September 2020].

Entrepreneur Asia Pacific. 2020. How to support your team while WFH. Available from www.entrepreneur.com/article/348270. [Accessed 13 September 2020].

Family Bites. 2011. DIY: Ice Cream Sundae Kit. Available from www.familybites.ca/2011/06/diy-ice-cream-sundae-kit.html?pintix=1. [Accessed 13 September 2020].

Food Intelligence Center. 2020. Thailand Food Industry Profile 2019. National Food Institute, Thailand. Available from http://fic.nfi.or.th/info_graphic_detail.php?id=28 . [Accessed 20 July 2020].

Google site. 2020. Type of social media. Available from sites.google.com/site/tanyapornparakornwatthana/laksna-khxng-social-media. [Accessed 13 September 2020].

GroupM Thailand. 2020. Social Distancing and the Impact on Thai Consumer Behaviors. Available from http://www.groupmthailand.com/insightm/home/view/176. [Accessed 21 July 2020].

IPG Mediabrands. 2020. Envisioning Post COVID-19 Pandemic in Thailand The Era of Distance: Consumers with Emerging Behaviors Creating the “New Normal” to Last in Thai Society. Available from ipg-connect.com/covid-19-กับยุคของ-d●i●s●t●a●n●c●e-consumers-8-พฤ/. [Accessed 21 July 2020].

Johns Hopkins Medicine. 2020. Patient Safety and Quality. Available from www.hopkinsmedicine.org/patient_safety/infection_prevention/hand_hygiene... [Accessed 13 September 2020].

Kitchn. 2020. How to Make the Easiest Pancakes Ever. Available from www.thekitchn.com/pancakes-recipe-263226. [Accessed 13 September 2020].

Maslow, A. H. 1954. Motivation and personality. New York: Harper & Row.

Marketing Oops. 2020. Insights of Thai Purchasing Behavior on FMCG-High Involvement-Retail Before-During-After Covid-19. Available from https://www.marketingoops.com/reports/consumer-insights-and-purchase-beh... [Accessed 21 July 2020].

Mckinsey and Company. 2020. Adapting customer experience in the time of coronavirus. Available from https://www.mckinsey.com/business-functions/marketing-and-sales/our-insi... [Accessed 21 July 2020].

McLeod, S. 2020. Maslow’s Hierarchy of Needs. Available from www.simplypsychology.org/maslow.html. [Accessed 10 Sep 2020].

MGR online. 2020. Twitter: 5 popular trends during Covid 19. Available from https://mgronline.com/cyberbiz/detail/9630000060823. [Accessed 10 Sep 2020].

National Statistics Office. 2018. Survey on food consumption of Thai population in 2017. Executive Summary, 1-3.

Nielsen. 2020. Asian Consumers are Rethinking how they eat Post Covid-19. Available from https://www.nielsen.com/eu/en/insights/article/2020/asian-consumers-are-rethinking-how-they-eat-post-covid-19/. [Accessed 18 July 2020].

Phanwattana, P.. 2019. Food consumption behavior of working age people in Bangkok. Journal of the Office of DPC 7 Khon Khann 26:2, 93-103.

Posttoday. 2020. Announcement of New Normal for Thai restaurant (S&P). Available from www.posttoday.com/life/travel/624106. [Accessed 10 Sep 2020].

RYT9. 2019. McDelivery Surprise. Available from www.ryt9.com/s/prg/3037301. [Accessed 13 September 2020].

RYT9. 2020. 3 Famous Online Market place “TU CU and KU”. Available from www.ryt9.com/s/prg/3132830. [Accessed 10 Sep 2020].

Siam Commercial Bank Economic Intelligence Center. 2020a. Thailand After Covid-19 Part 1: The Impact of the Economy and Thai Labor Market. Available from https://www.scb.co.th/en/personal-banking/stories/business-maker/thailand-after-covid-ep1.html. [Accessed 10 September 2020].

Siam Commercial Bank Economic Intelligence Center. 2020b. Thailand After Covid-19 Part 2: Business Opportunities and Survival. Available from https://www.scb.co.th/en/personal-banking/stories/business-maker/thailan... [Accessed 18 July 2020].

Siam PR. 2014. Online Shopping. Available from http://siampr.net/229/online-shopping. [Accessed 13 September 2020].

Smart SME Chanel. 2020. Why sale growth of utensils and gadget is increase during Covid 19? Available from https://www.smartsme.co.th/content/237232. [Accessed 20 May 2020].

Smith J. B. and M. Colgate (2007) Customer Value Creation: A Practical Framework. Journal of Marketing Theory and Practice. 15:1, 7-23.

Statista. 2020. Consumer Market Outlook of Food in 2020: Thailand. Available from https://www.statista.com/outlook/40000000/126/food/thailand. [Accessed 20 July 2020].

The Federation of Thai Industries. 2020. Thai Food Industry Amid Covvid-19...Rise or Fall? Food Focus Virtual Connect. 21 April 2020.

Thailand Board of Investment. 2018. Thailand Food Industry. Available from https://www.boi.go.th/upload/content/Food%20industry_5aa7b40bd758b.pdf. [Accessed 18 July 2020].

The MOMENTUM. 2020. Looking at the minds of consumers through product purchased during Covid-19: Will the world never be the same? April 7, 2020. Available from https://themomentum.co/covid-19-change-consumer-behavior/. [Accessed 21 July 2020].

Wongnai. 2020. 4 Product idea launched during Covid 19. Available from www.wongnai.com/business-owners/new-products-during-covid19. [Accessed 10 Sep 2020].

World Bank. 2020. Thailand Economic Monitor June 2020: Thailand in the Time of Covid-19. Available from https://www.worldbank.org/en/country/thailand/publication/thailand-economic-monitor-june-2020-thailand-in-the-time-of-covid-19. [Accessed 10 September 2020]