VIETNAMESE AGRICULTURE UNDER INTEGRATION CONTEXT

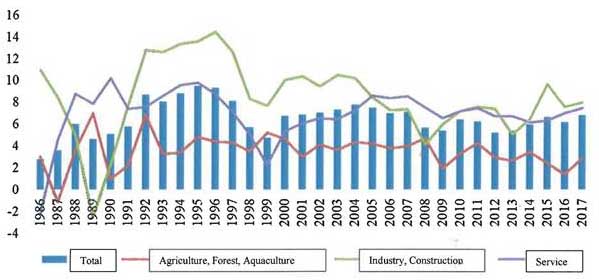

Appropriate and motivational policies have activated potential advantages of Vietnamese agriculture. This significantly contributes to the development of the national economy since Doi Moi, particularly to the agricultural and rural sector. Vietnam’s agricultural growth has been relatively high and stable since Doi Moi (with an average growth rate of approximately 3.3% per annum). This growth not only meets the demand for food supply and raw materials in the domestic industry and service development but also contributes to the export market (about 50% of agricultural-forestry-aquatic products were produced for export in recent 5 years). Agriculture is the only sector that experiences trade surplus, which reached over US$ 8 billion in 2017. With abundant supply and extensive international integration, Vietnam’s agriculture has been closely linked to changes in the world market.

Vietnam’s agriculture has taken part in the process of world globalization and integration with generations of free trade agreements (FTA). These FTAs began with the first generation of FTA that focused on liberalization of goods trading (including tariff reduction, and non-tariff barrier removal), to second generation of FTA with expansion of liberalization scope to several service sectors (deletion of market access conditions in relevant service sectors), and the third generation of FTA which continues to expand the scope to include service and investments. Vietnam has signed 12 FTAs with 56 countries and economies in the world, 10 of which have entered into force, and Vietnam has fully implemented all WTO commitments. Together with conventional FTAs, Vietnam has actively participated in a new generation of FTAs since 2010, namely TPP and EVFTA, with extensive and comprehensive integration. In that global playing field, Vietnam has accepted non-protection commitment, and complied with most of the standards required by member countries and world market. International integration in the future requires Vietnam to accept immediate competition and abide by standards set by countries in terms of economic, social and environmental fields.

Fig. 1. GDP growth by economic sector, 1986-2017

Source: GSO, 2017

Vietnam’s agriculture has taken part in the process of world globalization and integration with generations of free trade agreements (FTA). These FTAs began with the first generation of FTA that focused on liberalization of goods trading (including tariff reduction, and non-tariff barrier removal), to second generation of FTA with expansion of liberalization scope to several service sectors (deletion of market access conditions in relevant service sectors), and the third generation of FTA which continues to expand the scope to include service and investments. Vietnam has signed 12 FTAs with 56 countries and economies in the world, 10 of which have entered into force, and Vietnam has fully implemented all WTO commitments. Together with conventional FTAs, Vietnam has actively participated in a new generation of FTAs since 2010, namely TPP and EVFTA, with extensive and comprehensive integration. In that global playing field, Vietnam has accepted non-protection commitment, and complied with most of the standards required by member countries and world market. International integration in the future requires Vietnam to accept immediate competition and abide by standards set by countries in terms of economic, social and environmental fields.

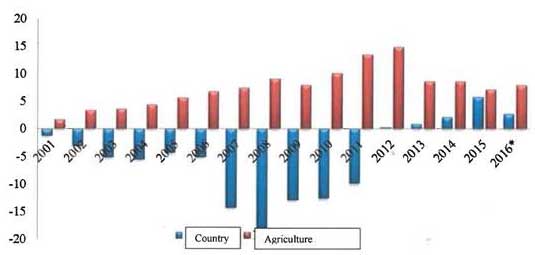

Fig. 2. National Trade Balance and Agricultural Trade Balance

Source: GSO and MARD, 2017

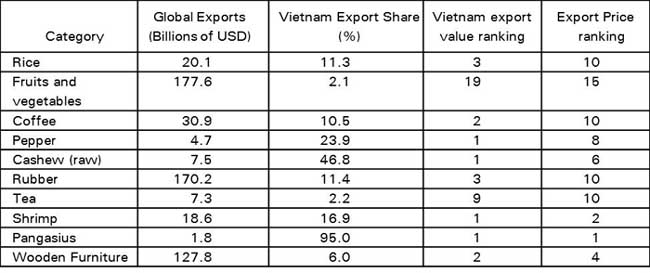

With good supply, Vietnam has gradually asserted itself in the global agricultural – forestry - aquatic products (AFAP) market. Vietnam has also witnessed impressive growth in exports over the past few years through international economic integration, and participation in bilateral and multilateral FTAs. The total value of AFAP exports in 2017 reached US$ 36.4 billion, an increase of 14 times compared with that of 1995 when Vietnam joined in ASEAN, marking an annual growth rate of 12.9%. Several AFAP have high export value in the world, including cashews, peppers, pangasius, coffee, wooden furniture, and rice. However, export prices are relatively low as the majority of exported goods are raw products such as rice, peppers and cashews (Table 1).

Table 1. Position of Vietnamese agricultural exports in the world

Source: ITC-Trademap, GDVC, 2017

The above evidence helps in outlining some general insights on the development trends of global agro-forestry market and the position of Vietnamese agriculture as follows:

- Vietnam’s agriculture possesses strong supply capacity, and has been participating in international integration, and is increasingly dependent on the world market.

- The world has witnessed a strong growing demand for agro-forestry trading along with economic growth and global integration, particularly since the beginning of the 21st century.

- Prices of raw agro-forestry products have closely linked to the changes in oil price as well as other financial investment channels, and the tendency of short-run fluctuation has become increasingly frequent.

- Demand for agro-forestry products has shifted to high nutritional value, processed food, furniture, organic products, functional foods, cosmetics, and environmentally friendly and socially responsible products.

The main trends mentioned above show some suggestions for Vietnam’s agricultural development in the new context:

- Vietnam’s agriculture cannot maintain its advantages by exploited resources and low price. It is necessary to prepare new competitive capacity when joining further into international integration.

- It is important to develop agro-forestry processing industry, build a value chain, and adopt appropriate hedging policies to tackle risks and market turbulence.

- Restructuring of products is necessary in order to respond to the world market’s needs of higher nutrition foods (fruits, vegetables, meat, eggs, milk, and seafood), processed foods, furniture, organic products, functional foods and cosmetics.

- Increasingly stringent global market rules in terms of social, economic and environmental aspects that must be complied with.

Development orientation of Vietnam’s agriculture

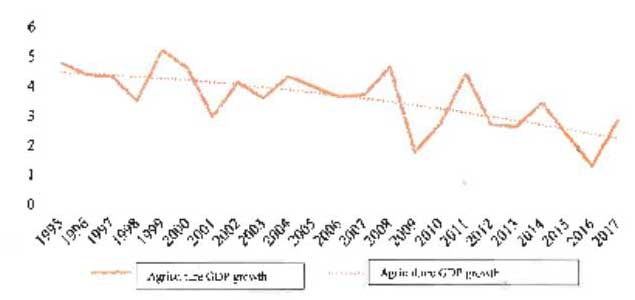

Despite a number of achievements since Doi Moi, Vietnam’s recent agricultural growth rate has slowed down, declining from 4.5% in 1996-2000, to 4.1%, 3.3% and 2.8% in the 2001-2005, 2006-2010, and 2011-2015 periods, respectively. At the same time, resources for agricultural growth tend to reduce, including land fragmentation, increasingly scarce water supply for irrigation particularly during dry season, decrease in domestic investments capital in agriculture, low foreign investments in agriculture compared with that in manufacturing and services, withdrawing of young workforce from agriculture to participate in informal labor market, and low income and high risk. The competitiveness of the agricultural sector appears to decline compared with other regional competitors.

Fig. 3. Decline in agricultural growth 1995-2017

Source: GSO, 2017

Three major challenges to maintaining sustainable growth and competitiveness of Vietnam’s agriculture include (i) small scale production, (ii) unpredictable climate change, and (iii) international integration accompanied by fierce competition. The majority of the total 9.29 million units involved in agricultural, forestry and aquatic production comprises of farmers (accounting for 99.89%), the numbers of enterprises and cooperatives represent insignificant fractions of 0.04% and 0.07% respectively (as of 1st July 2016). Thirty-six percent of farming households possessed less than 0.2 hectare of land. The number of enterprises employing under 10 employees represents almost a half of the total agricultural enterprises. Vietnam is one of the five countries that are most vulnerable to the impacts of climate change and extreme weather. Climate change and the impact of El Niño resulted in the worst salinity intrusion in the Mekong Delta, and recorded drought in South Central and Central Highlands in 2016. Extensive international integration raises competition and pressure on production, resulting in trade disputes despite weak capacity. These factors lead to high cost investment in agriculture while profitability is low and competitiveness is poor, which does not appeal to enterprises.

Agriculture restructuring policy

The Prime Minister promulgated Decision 899/QD-TTg dated 10 June, 2013 approving the restructuring of the agricultural sector projects aiming at enhancing added value and sustainable development, with objectives set out as listed below:

- Maintain growth; improve efficiency and competitiveness through increasing productivity, quality and added value; better meeting domestic consumers’ needs and taste; and promoting export. Achieve the average growth rate of 2.6-3.0% p.a., 3.5-4.0% p.a. for the 2011-2015 and 2016-2020 periods, respectively;

- Improve income and living standards for rural residents, ensure food security (including nutritional safety) both in the short and long term, contributing to poverty reduction. By 2020, rural household income will increase by 2.5 times compared with that of 2008; the number of communes meeting the new rural criteria will be 20% and 50% in 2015 and 2020 respectively.;

- Strengthen natural resource management, reduce greenhouse gas emissions and other negative impacts on the environment, make good use of environmental benefits, improve risk management capacity, proactively prevent natural disasters, increase national forest coverage to 42% by 2020, and contribute to implementing the national green growth strategy.

Three major themes that the project aims to achieve include:

- Develop a market-oriented agricultural production, promoting products with advantages, connecting with industry and agricultural supporting services;

- Reorganize in ways of large-scale production, develop cooperatives, and foster chain linkages. Encourage private investments and improve public investment’s efficiency; and

- Promote the application of science and technology, create new good quality varieties, develop fine and comprehensive processing technology, innovate technology, reduce exploitation of resources, reduce negative impacts on the environment.

Evaluate the implementation of agricultural restructuring

Results of agricultural restructuring for 2013 –2017

Ministry of Agriculture and Rural Development (MARD), under the guidance of the government, has coordinated with other ministries and local governments to execute activities and measures creating positive impacts on production, which contributes to socio-economic development, and income and living conditions’ improvement during the four years of implementing the project “Restructuring agricultural sector project aimed at enhancing added value and sustainable development”.

Agricultural restructuring has made important contribution to the production and business efficiency of the entire sector. The growth target of 2011-2015 was basically achieved, with the average agricultural growth rate of 2.85% p.a. Particularly, during the course of five years between 2013 and 2017, despite encountering a number of difficulties caused by natural disasters and market turbulence, the average growth rate remained at 2.78% p.a. The agricultural GDP of 2017 reached 2.9%, of which agricultural, forestry and fishery products increased by 2.07%, 5.14%, and 5.54% respectively regardless of significant damage caused by typhoons at the end of the year.

Income and living standards of rural residents have also been significantly improved. The average farming household income rose from VND 37.9 million (equivalent 1723 US$) p.a. to VND 105.3 million (equivalent 4786 US$) p.a. between 2008 and 2016, marking an increase of 2.78 times as much as current prices and 1.6 times if taking inflation into account. The National Target Program on Rural Development with activities and measures to restructure agricultural sector has basically achieved all the targets set. By 2017, 2,884 communes (accounting for 32.3% of total communes) achieved 19 criteria (satisfying the target of reaching at least 31% of qualified communes for 2019); and 43 districts were recognized as meeting new rural standard. The proportion of poor households in rural areas is reduced from 17.4% in 2010 to 11.7% in 2016 and the rate of rural residents using hygienic water was approximately 90%.

In the period 2013-2017, although weather conditions were subject to abnormal changes, forecast and prevention of natural disasters were improved to reduce people and material loss. The forest coverage rate reached 40.84% and 41.45% in 2015 and 2017 respectively, with the growth rate for 2013-2017 of 0.28%.

Achievements and limitations of restructuring agricultural sector

Achievements

The production structure was adjusted to promote the advantages of each locality and the entire country, coupling with market demand. A number of major items have confirmed their position and competitiveness in the world market, ensuring a firm stand on international integration. The structure of commodity and export products has shown relatively obvious results, namely, increasing the proportion of products with advantages such as aquatic products, vegetables, flowers, tropical fruits, valuable industrial trees (including coffee, cashews, rubber, peppers), furniture; and reducing products which tend to see an increase in supply such as rice and pork, or discouraging the development of products (like cassava). As a result, the total agricultural exports increased sharply, reaching US$ 157.2 billion in the 2013-2017 period, with an average rise of US$ 1.7 billion p.a; in 2017 alone, it was estimated to reach US$ 36.4 billion.

Production organizations were also renewed more appropriately and effectively to include more enterprises and cooperatives, reducing the number of households in agro-forestry. There have been 19 agricultural cooperative unions, 11,688 efficiently running cooperatives; of which cthe number of cooperatives has significantly increased, gradually adapting to the market mechanism, and effectively supporting household economically by 2017. Farming also rose sharply. There have been 33,500 farms nationwide, up by 61.7% compared with the figure for 2012. The number of agricultural enterprises also grew from 3,517 in 2012 to 4,500 in 2016 and 5,400 in 2017. Large scale production with value chain linking farmers and other farming organizations including cooperative unions, cooperatives and enterprises has been formed in almost all production arenas and expanded to an increasing number of localities. This fact affirms the efficiency and stability of agricultural production of goods and international competition. The size of land lot for agricultural production also increased from 1,619.7 m2 in 2011 to 1,843.1 m2 in 2016.

Research, transfer and application of science and technology are promoted. MARD has adjusted the structure of scientific and agricultural extension tasks to prioritize research, transfer and application of high-tech and clean agricultural production; focusing on urgent production problems such as high quality variety production, pest and disease resistance, adaptation to climate change, advanced production process, standard development, etc. A number of new varieties, new technology, and advanced production processes have been put into practice to improve productivity of fruits, livestock and aquaculture. Some major companies invested in new varieties for superior productivity. In 2017, science and technology contributed 45% of added value to agriculture, with over 80% of cultivated areas of rice, maize, sugarcane and cotton being used for new varieties; 45% of cows, 65% of pigs used hybrid breeds; nearly 200 technical processes have been recognized and applied in production.

Limitations

- The restructuring process is slow while a number of localities have no clear plan to identify the appropriate structure and advantages; production is beyond plan and in movement. Agricultural growth is not stable, and it is difficult to reach the target set for the period 2016-2020 of 3.5% and 4.0%.

- Income and living conditions of people, especially in remote and mountainous areas encounter great difficulties with slow improvement; the rate of poor households remains relatively large.

- New rural development is uneven with large gaps amongst localities and regions. Regarding implementation, the majority of localities have focused on improving infrastructure facility whereas the development of production, cultural lifestyle, and environmental protection have not been paid proper attention to.

- Waste water and waste gas pollution in industrial parks and craft villages are directly deteriorating the environment, endangering the sustainable livelihood of the people, and depleting natural resources.

- Labor productivity as well as the productivity, quality and competitiveness of many agricultural products remain relatively low, particularly under the context of further international integration; meanwhile, the damage caused by natural disasters is severe and complex.

- The market is unpredictable while statistics and forecast work is still weak, and prices usually fluctuate. Agricultural products for export are primarily raw, and the quality is often hard to categorize. 80% of agricultural products have not built any brand, logo or label.

- Innovation and development of production forms happen slowly. Small-scale household accounts for a high share with 99.98% of farming households, 0.04% of enterprises, and 0.07% of cooperatives; 36% of farming households owns less than 0.2 ha of cultivation area; 50% of enterprises has less than 10 employees. Weaknesses hindering the modernization and industrialization of agriculture have gradually been exposed. Large scale production in value chain associating raw materials with preservation, processing and consuming has not become the mainstream. There have been too few complete value chains, which still lack the linkage between large enterprises and local small and medium enterprises, and farmers ‘organization. Total social investment is about US$ 3 billion, 50% of which comes from state budget, only 16.7% is from enterprises.

- Science and technology have not fully promoted its role. The application of advanced science and technology in production, processing and preservation is still limited, which has not created any breakthrough.

ORIENTATIONS AND SOLUTIONS FOR AGRICULTURAL POLICIES IN THE NEXT PERIOD

In the next period, agriculture and rural development needs to drastically implement restructuring in association with developing new rural areas to create breakthrough in sustainable agriculture and rural development, improving added value, efficiency and competitiveness. This will quickly improve the lives of farmers, contributing to poverty reduction, environmental protection, and ensuring national security.

In order to achieve the above objectives, agriculture and rural development must execute the three groups of solutions, including (i) reformat product structure and large balances; (ii) reorganize production into three pivots i.e. national, provincial and regional/ provincial specialty; and (iii) institutional and policy reform measures.

Orientation of agriculture product structure and utilization of production resources

Balance of agricultural land

Based on comparative advantages, market needs and adaptation to climate changes, land balance shall shift from rice land to other annual crops such as legumes or maize, fruit trees and aquaculture; reducing the area of perennial trees, and increasing forestry areas specified as follows:

- Reducing paddy land from 4.0 million hectares in 2017 to 3.1 million hectares in 2025 (Table 2).

- Increasing grass land and annual crop land from 140,000 hectares to 354,000 hectares for the former, and from 2.7 million hectares to 3.2 million hectares for the latter between 2017 and 2025.

- Reducing land for coffee, rubber and pepper from 664,000; 971,000; and 152,000 hectares in 2017 to 634,000; 947,000, and 105,000 hectares in 2025 respectively.

- Increasing land for cashew from 297,000 hectares in 2017 to 418,000 hectares in 2025.

- Increasing land for fruit trees from 923,000 hectares in 2017 to 1.1 million hectares in 2025.

- Increasing aquaculture areas from 749,000 hectares in 2017 to 790,000 hectares in 2025.

- Increasing forest areas from 15.7 million hectares in 2017 to 16.9 million hectares in 205, marking an increase in the forest coverage rate from 41.45% to 44.53%.

Table 2. Balance of agro-foresty land (thousands of hectares)

|

Years

|

2017

|

2020

|

2025

|

|

Rice

|

4,030

|

3,760

|

3,129

|

|

Grassland

|

140

|

240

|

354

|

|

Other annual crops

|

2,730

|

2,780

|

3,160

|

|

Tea

|

129

|

134

|

140

|

|

Coffee

|

664

|

650

|

634

|

|

Rubber

|

971

|

960

|

947

|

|

Cashew

|

297

|

400

|

418

|

|

Pepper

|

152

|

130

|

105

|

|

Fruit trees

|

923

|

970

|

1.124

|

|

Aquaculture

|

749

|

768

|

790

|

|

Forest

|

15,700

|

16,245

|

16,868

|

|

Forest coverage rate (%)

|

41.45

|

42.89

|

44.53

|

Source: Calculation from statistics of MARD, 2017

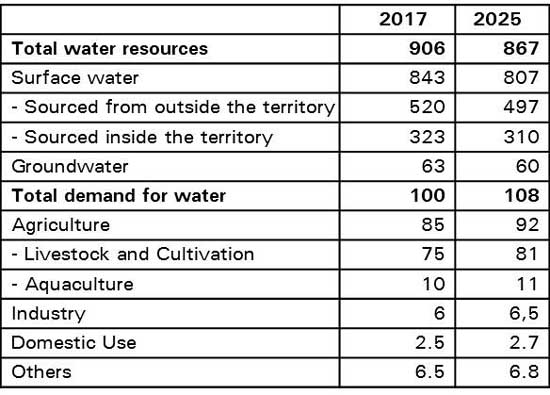

Balance of water resources

In the context of declining water resources, water resource balancing is developed based on the goal of saving and developing multifunctional irrigation. The total current water resource constitutes about 906 billion m3, but this figure will drop to 867 billion m3 by 2025. Meanwhile, water demand for agricultural production is estimated to rise from 85 billion m3 in 2017 to 92 billion m3 in 2025 (Table 3).

Table 3. Balance of water resources (unit: billion m3)

Source: Calculation from statistics of Department for Irrigation (MARD) and Department for Water Resources Management (MONRE), 2017

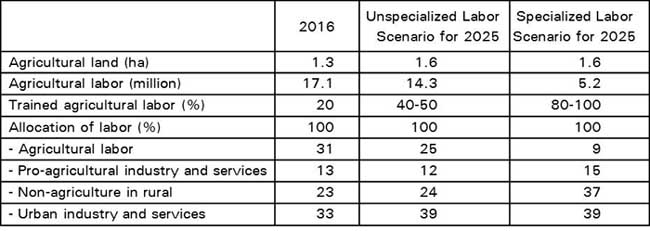

Balance of Agricultural Labor

Labor balances are based on the specialization of agricultural labor, increasing the production scale, and developing pro-agricultural services. Two labor balance scenarios are projected as follows:

- Scenario 1: Unspecialized agricultural labor (yet increasing the average production are from 1.3 to 1.6 hectares). With an average land for each household of 1.6 ha/ households, the total agricultural labor will decline to 14.3 million, marking a drop to 25% labor working in agricultural sector. Those who move out of agriculture to non-agriculture and to industry and urban services will rise from 23% to 24% for the former, and from 33% to 39% for the latter. The proportion of labor in pro-agricultural services will remain at 12%. About 40-50% of agricultural labor is trained.

- Scenario 2: Specialized agricultural labor (full-time labor as industrial labor, coupling with the rising average production area from 1.3 to 1.6 hectares). With an average land for each household of 1.6 ha/ households, agricultural labor is predicted to drop to 5.2 million in 2025, of which agricultural labor sharply drops from 31% to 9%, rising pro-agricultural service labor from 12% to 15%, and other non-agriculture industry from 23% to 37%. Approximately from 80 to 100% rural labor is trained (Table 4).

Table 4. Balance of Agricultural Labor

Source: Estimates based on Census on Agriculture, Forestry and Aquaculture, and IO Balance Sheet, GSO 2016.

Reorganize production of key product groups in value chain

The selection of value chain development for key product groups is based on the following principles:

- Based on the value of the sector

- Enterprise will play as the core element affiliating with other economic entities in the production area that have appropriate production scale

- Developing comprehensive value chain from input to production, processing and consumption

- Applying high-tech to ensure competitiveness in accordance with requirements by markets at all stages

Develop national key products (products with export values of US$ 1 billion or more, together with pork and poultry)

It is necessary to ensure that the areas have a high level of natural adaptability, high socio-economic conditions, production conditions, environment protection, proper landscape and natural resource provision. Large scale production areas should be built with consideration to nationwide production scale to maintain price favorable production level. It is advisable to collaborate with major corporate organizations that are able to lead the value chain of key products, to review the entire planning strategy and planned areas, develop and propose investments in comprehensive value chain in form of clusters. Major corporate organizations are encouraged to affiliate with local SMEs, local authorities, and farmer organizations to implement investments in value chains in the form of Public-Private partnership.

Develop provincial key products

Provinces, based on their advantages and market needs, need to select key products for planning specialized cultivation areas where favorable natural and socio-economic conditions, technical infrastructure and supporting services, as well as convenient traffic routes exist to facilitate the connection to main markets. Main markets for key agricultural products must be identified with priority put on local enterprises as leaders specializing in each product line. It is necessary to connect with processing enterprises, large scale distributors and target markets. The government must act as the bridge between local enterprises, farmer organizations and markets or large processing and trading enterprises by providing market information, market brokerage, and investment brokerage. The government should collaborate with large enterprises, research institutes or associations to carry out modern technology transfer that is suitable for local SMEs and farmers; or develop innovative agricultural incubators for local enterprises and farmers. Agricultural extension work should be renovated with greater participation as technology transfer agent.

Develop local specialty

Local specialty usually has small scale production which are closely linked with specific geographical locations. The development of these products needs to be closely connected to the development of new rural development at commune and district level in accordance with the model of “Each commune has one specialty.” The most suitable location and production unit must be defined; technical processes and criteria must be developed; production plans must be systemized. Developing management capacity for farmers and craft villages of available specialty should be focused on. Intermediate financial brokers and commercial brokers should be attracted to commercialize the specialty in local and international markets.

Policy and institutions measures

- Review planning and production structure in line with the advantages, markets and adaptation to climate change.

- Reform and improve policies, including (i) improving business environment, (ii) reducing tax on agricultural and rural investment, (iii) developing agricultural insurance market, (iv) introducing preferential access to land, enhancing land aggravation and accumulation for farming purposes, and (v) providing support for credit access of all economic sectors investing in agriculture and rural areas.

- Reform and develop cooperatives and farms; develop various forms of value chains, attract private investment, promote PPP, reform state enterprises, and restructure industrial associations.

- Promote and improve vocational training for farmers, shift agricultural labor force to service, industry and rural trades.

- Strengthen research, application and transfer science and technology to agriculture, focusing on variety, production, processing and managing value chain. Adopt preferential policies for development of high-tech, green, clean and organic agriculture.

- Develop, improve and apply standard and norm system as well as technical process.

- Enhance international integration and market development: strengthen the capacity of information, forecast, warning, negotiation, dispute settlement, brand development, origin traceability, and trade promotion for domestic and foreign markets.

- Renovate state manage: consolidate vertical management system; decentralization, increasing local autonomy; socialization of public services and public service delivery bodies.

- Mobilize social resources, focusing on modern infrastructure, strengthening the capacity to prevent and mitigate natural disasters, adapting to climate change and developing new rural areas.

REFERENCES

IPSARD, 2017. Reposistionning Vietnam agriculture. Internal working paper in Vietnamese only.

GSO, 2017. Statistical year book.

GSO. 2016. Census on Agriculture, Forestry and Aquaculture, and IO Balance Sheet

MARD, 2017. Database on Agriculture and Irrigation

MONRE, 2017. Database on landuse and water resources.

ITC-Trademap, 2017.

|

Date submitted: July 24, 2018

Reviewed, edited and uploaded: Oct. 18, 2018

|

A Review of Vietnam’s Recent Agricultural Policies

VIETNAMESE AGRICULTURE UNDER INTEGRATION CONTEXT

Appropriate and motivational policies have activated potential advantages of Vietnamese agriculture. This significantly contributes to the development of the national economy since Doi Moi, particularly to the agricultural and rural sector. Vietnam’s agricultural growth has been relatively high and stable since Doi Moi (with an average growth rate of approximately 3.3% per annum). This growth not only meets the demand for food supply and raw materials in the domestic industry and service development but also contributes to the export market (about 50% of agricultural-forestry-aquatic products were produced for export in recent 5 years). Agriculture is the only sector that experiences trade surplus, which reached over US$ 8 billion in 2017. With abundant supply and extensive international integration, Vietnam’s agriculture has been closely linked to changes in the world market.

Vietnam’s agriculture has taken part in the process of world globalization and integration with generations of free trade agreements (FTA). These FTAs began with the first generation of FTA that focused on liberalization of goods trading (including tariff reduction, and non-tariff barrier removal), to second generation of FTA with expansion of liberalization scope to several service sectors (deletion of market access conditions in relevant service sectors), and the third generation of FTA which continues to expand the scope to include service and investments. Vietnam has signed 12 FTAs with 56 countries and economies in the world, 10 of which have entered into force, and Vietnam has fully implemented all WTO commitments. Together with conventional FTAs, Vietnam has actively participated in a new generation of FTAs since 2010, namely TPP and EVFTA, with extensive and comprehensive integration. In that global playing field, Vietnam has accepted non-protection commitment, and complied with most of the standards required by member countries and world market. International integration in the future requires Vietnam to accept immediate competition and abide by standards set by countries in terms of economic, social and environmental fields.

Fig. 1. GDP growth by economic sector, 1986-2017

Source: GSO, 2017

Vietnam’s agriculture has taken part in the process of world globalization and integration with generations of free trade agreements (FTA). These FTAs began with the first generation of FTA that focused on liberalization of goods trading (including tariff reduction, and non-tariff barrier removal), to second generation of FTA with expansion of liberalization scope to several service sectors (deletion of market access conditions in relevant service sectors), and the third generation of FTA which continues to expand the scope to include service and investments. Vietnam has signed 12 FTAs with 56 countries and economies in the world, 10 of which have entered into force, and Vietnam has fully implemented all WTO commitments. Together with conventional FTAs, Vietnam has actively participated in a new generation of FTAs since 2010, namely TPP and EVFTA, with extensive and comprehensive integration. In that global playing field, Vietnam has accepted non-protection commitment, and complied with most of the standards required by member countries and world market. International integration in the future requires Vietnam to accept immediate competition and abide by standards set by countries in terms of economic, social and environmental fields.

Fig. 2. National Trade Balance and Agricultural Trade Balance

Source: GSO and MARD, 2017

With good supply, Vietnam has gradually asserted itself in the global agricultural – forestry - aquatic products (AFAP) market. Vietnam has also witnessed impressive growth in exports over the past few years through international economic integration, and participation in bilateral and multilateral FTAs. The total value of AFAP exports in 2017 reached US$ 36.4 billion, an increase of 14 times compared with that of 1995 when Vietnam joined in ASEAN, marking an annual growth rate of 12.9%. Several AFAP have high export value in the world, including cashews, peppers, pangasius, coffee, wooden furniture, and rice. However, export prices are relatively low as the majority of exported goods are raw products such as rice, peppers and cashews (Table 1).

Table 1. Position of Vietnamese agricultural exports in the world

Source: ITC-Trademap, GDVC, 2017

The above evidence helps in outlining some general insights on the development trends of global agro-forestry market and the position of Vietnamese agriculture as follows:

- Vietnam’s agriculture possesses strong supply capacity, and has been participating in international integration, and is increasingly dependent on the world market.

- The world has witnessed a strong growing demand for agro-forestry trading along with economic growth and global integration, particularly since the beginning of the 21st century.

- Prices of raw agro-forestry products have closely linked to the changes in oil price as well as other financial investment channels, and the tendency of short-run fluctuation has become increasingly frequent.

- Demand for agro-forestry products has shifted to high nutritional value, processed food, furniture, organic products, functional foods, cosmetics, and environmentally friendly and socially responsible products.

The main trends mentioned above show some suggestions for Vietnam’s agricultural development in the new context:

- Vietnam’s agriculture cannot maintain its advantages by exploited resources and low price. It is necessary to prepare new competitive capacity when joining further into international integration.

- It is important to develop agro-forestry processing industry, build a value chain, and adopt appropriate hedging policies to tackle risks and market turbulence.

- Restructuring of products is necessary in order to respond to the world market’s needs of higher nutrition foods (fruits, vegetables, meat, eggs, milk, and seafood), processed foods, furniture, organic products, functional foods and cosmetics.

- Increasingly stringent global market rules in terms of social, economic and environmental aspects that must be complied with.

Development orientation of Vietnam’s agriculture

Despite a number of achievements since Doi Moi, Vietnam’s recent agricultural growth rate has slowed down, declining from 4.5% in 1996-2000, to 4.1%, 3.3% and 2.8% in the 2001-2005, 2006-2010, and 2011-2015 periods, respectively. At the same time, resources for agricultural growth tend to reduce, including land fragmentation, increasingly scarce water supply for irrigation particularly during dry season, decrease in domestic investments capital in agriculture, low foreign investments in agriculture compared with that in manufacturing and services, withdrawing of young workforce from agriculture to participate in informal labor market, and low income and high risk. The competitiveness of the agricultural sector appears to decline compared with other regional competitors.

Fig. 3. Decline in agricultural growth 1995-2017

Source: GSO, 2017

Three major challenges to maintaining sustainable growth and competitiveness of Vietnam’s agriculture include (i) small scale production, (ii) unpredictable climate change, and (iii) international integration accompanied by fierce competition. The majority of the total 9.29 million units involved in agricultural, forestry and aquatic production comprises of farmers (accounting for 99.89%), the numbers of enterprises and cooperatives represent insignificant fractions of 0.04% and 0.07% respectively (as of 1st July 2016). Thirty-six percent of farming households possessed less than 0.2 hectare of land. The number of enterprises employing under 10 employees represents almost a half of the total agricultural enterprises. Vietnam is one of the five countries that are most vulnerable to the impacts of climate change and extreme weather. Climate change and the impact of El Niño resulted in the worst salinity intrusion in the Mekong Delta, and recorded drought in South Central and Central Highlands in 2016. Extensive international integration raises competition and pressure on production, resulting in trade disputes despite weak capacity. These factors lead to high cost investment in agriculture while profitability is low and competitiveness is poor, which does not appeal to enterprises.

Agriculture restructuring policy

The Prime Minister promulgated Decision 899/QD-TTg dated 10 June, 2013 approving the restructuring of the agricultural sector projects aiming at enhancing added value and sustainable development, with objectives set out as listed below:

- Maintain growth; improve efficiency and competitiveness through increasing productivity, quality and added value; better meeting domestic consumers’ needs and taste; and promoting export. Achieve the average growth rate of 2.6-3.0% p.a., 3.5-4.0% p.a. for the 2011-2015 and 2016-2020 periods, respectively;

- Improve income and living standards for rural residents, ensure food security (including nutritional safety) both in the short and long term, contributing to poverty reduction. By 2020, rural household income will increase by 2.5 times compared with that of 2008; the number of communes meeting the new rural criteria will be 20% and 50% in 2015 and 2020 respectively.;

- Strengthen natural resource management, reduce greenhouse gas emissions and other negative impacts on the environment, make good use of environmental benefits, improve risk management capacity, proactively prevent natural disasters, increase national forest coverage to 42% by 2020, and contribute to implementing the national green growth strategy.

Three major themes that the project aims to achieve include:

- Develop a market-oriented agricultural production, promoting products with advantages, connecting with industry and agricultural supporting services;

- Reorganize in ways of large-scale production, develop cooperatives, and foster chain linkages. Encourage private investments and improve public investment’s efficiency; and

- Promote the application of science and technology, create new good quality varieties, develop fine and comprehensive processing technology, innovate technology, reduce exploitation of resources, reduce negative impacts on the environment.

Evaluate the implementation of agricultural restructuring

Results of agricultural restructuring for 2013 –2017

Ministry of Agriculture and Rural Development (MARD), under the guidance of the government, has coordinated with other ministries and local governments to execute activities and measures creating positive impacts on production, which contributes to socio-economic development, and income and living conditions’ improvement during the four years of implementing the project “Restructuring agricultural sector project aimed at enhancing added value and sustainable development”.

Agricultural restructuring has made important contribution to the production and business efficiency of the entire sector. The growth target of 2011-2015 was basically achieved, with the average agricultural growth rate of 2.85% p.a. Particularly, during the course of five years between 2013 and 2017, despite encountering a number of difficulties caused by natural disasters and market turbulence, the average growth rate remained at 2.78% p.a. The agricultural GDP of 2017 reached 2.9%, of which agricultural, forestry and fishery products increased by 2.07%, 5.14%, and 5.54% respectively regardless of significant damage caused by typhoons at the end of the year.

Income and living standards of rural residents have also been significantly improved. The average farming household income rose from VND 37.9 million (equivalent 1723 US$) p.a. to VND 105.3 million (equivalent 4786 US$) p.a. between 2008 and 2016, marking an increase of 2.78 times as much as current prices and 1.6 times if taking inflation into account. The National Target Program on Rural Development with activities and measures to restructure agricultural sector has basically achieved all the targets set. By 2017, 2,884 communes (accounting for 32.3% of total communes) achieved 19 criteria (satisfying the target of reaching at least 31% of qualified communes for 2019); and 43 districts were recognized as meeting new rural standard. The proportion of poor households in rural areas is reduced from 17.4% in 2010 to 11.7% in 2016 and the rate of rural residents using hygienic water was approximately 90%.

In the period 2013-2017, although weather conditions were subject to abnormal changes, forecast and prevention of natural disasters were improved to reduce people and material loss. The forest coverage rate reached 40.84% and 41.45% in 2015 and 2017 respectively, with the growth rate for 2013-2017 of 0.28%.

Achievements and limitations of restructuring agricultural sector

Achievements

The production structure was adjusted to promote the advantages of each locality and the entire country, coupling with market demand. A number of major items have confirmed their position and competitiveness in the world market, ensuring a firm stand on international integration. The structure of commodity and export products has shown relatively obvious results, namely, increasing the proportion of products with advantages such as aquatic products, vegetables, flowers, tropical fruits, valuable industrial trees (including coffee, cashews, rubber, peppers), furniture; and reducing products which tend to see an increase in supply such as rice and pork, or discouraging the development of products (like cassava). As a result, the total agricultural exports increased sharply, reaching US$ 157.2 billion in the 2013-2017 period, with an average rise of US$ 1.7 billion p.a; in 2017 alone, it was estimated to reach US$ 36.4 billion.

Production organizations were also renewed more appropriately and effectively to include more enterprises and cooperatives, reducing the number of households in agro-forestry. There have been 19 agricultural cooperative unions, 11,688 efficiently running cooperatives; of which cthe number of cooperatives has significantly increased, gradually adapting to the market mechanism, and effectively supporting household economically by 2017. Farming also rose sharply. There have been 33,500 farms nationwide, up by 61.7% compared with the figure for 2012. The number of agricultural enterprises also grew from 3,517 in 2012 to 4,500 in 2016 and 5,400 in 2017. Large scale production with value chain linking farmers and other farming organizations including cooperative unions, cooperatives and enterprises has been formed in almost all production arenas and expanded to an increasing number of localities. This fact affirms the efficiency and stability of agricultural production of goods and international competition. The size of land lot for agricultural production also increased from 1,619.7 m2 in 2011 to 1,843.1 m2 in 2016.

Research, transfer and application of science and technology are promoted. MARD has adjusted the structure of scientific and agricultural extension tasks to prioritize research, transfer and application of high-tech and clean agricultural production; focusing on urgent production problems such as high quality variety production, pest and disease resistance, adaptation to climate change, advanced production process, standard development, etc. A number of new varieties, new technology, and advanced production processes have been put into practice to improve productivity of fruits, livestock and aquaculture. Some major companies invested in new varieties for superior productivity. In 2017, science and technology contributed 45% of added value to agriculture, with over 80% of cultivated areas of rice, maize, sugarcane and cotton being used for new varieties; 45% of cows, 65% of pigs used hybrid breeds; nearly 200 technical processes have been recognized and applied in production.

Limitations

- The restructuring process is slow while a number of localities have no clear plan to identify the appropriate structure and advantages; production is beyond plan and in movement. Agricultural growth is not stable, and it is difficult to reach the target set for the period 2016-2020 of 3.5% and 4.0%.

- Income and living conditions of people, especially in remote and mountainous areas encounter great difficulties with slow improvement; the rate of poor households remains relatively large.

- New rural development is uneven with large gaps amongst localities and regions. Regarding implementation, the majority of localities have focused on improving infrastructure facility whereas the development of production, cultural lifestyle, and environmental protection have not been paid proper attention to.

- Waste water and waste gas pollution in industrial parks and craft villages are directly deteriorating the environment, endangering the sustainable livelihood of the people, and depleting natural resources.

- Labor productivity as well as the productivity, quality and competitiveness of many agricultural products remain relatively low, particularly under the context of further international integration; meanwhile, the damage caused by natural disasters is severe and complex.

- The market is unpredictable while statistics and forecast work is still weak, and prices usually fluctuate. Agricultural products for export are primarily raw, and the quality is often hard to categorize. 80% of agricultural products have not built any brand, logo or label.

- Innovation and development of production forms happen slowly. Small-scale household accounts for a high share with 99.98% of farming households, 0.04% of enterprises, and 0.07% of cooperatives; 36% of farming households owns less than 0.2 ha of cultivation area; 50% of enterprises has less than 10 employees. Weaknesses hindering the modernization and industrialization of agriculture have gradually been exposed. Large scale production in value chain associating raw materials with preservation, processing and consuming has not become the mainstream. There have been too few complete value chains, which still lack the linkage between large enterprises and local small and medium enterprises, and farmers ‘organization. Total social investment is about US$ 3 billion, 50% of which comes from state budget, only 16.7% is from enterprises.

- Science and technology have not fully promoted its role. The application of advanced science and technology in production, processing and preservation is still limited, which has not created any breakthrough.

ORIENTATIONS AND SOLUTIONS FOR AGRICULTURAL POLICIES IN THE NEXT PERIOD

In the next period, agriculture and rural development needs to drastically implement restructuring in association with developing new rural areas to create breakthrough in sustainable agriculture and rural development, improving added value, efficiency and competitiveness. This will quickly improve the lives of farmers, contributing to poverty reduction, environmental protection, and ensuring national security.

In order to achieve the above objectives, agriculture and rural development must execute the three groups of solutions, including (i) reformat product structure and large balances; (ii) reorganize production into three pivots i.e. national, provincial and regional/ provincial specialty; and (iii) institutional and policy reform measures.

Orientation of agriculture product structure and utilization of production resources

Balance of agricultural land

Based on comparative advantages, market needs and adaptation to climate changes, land balance shall shift from rice land to other annual crops such as legumes or maize, fruit trees and aquaculture; reducing the area of perennial trees, and increasing forestry areas specified as follows:

- Reducing paddy land from 4.0 million hectares in 2017 to 3.1 million hectares in 2025 (Table 2).

- Increasing grass land and annual crop land from 140,000 hectares to 354,000 hectares for the former, and from 2.7 million hectares to 3.2 million hectares for the latter between 2017 and 2025.

- Reducing land for coffee, rubber and pepper from 664,000; 971,000; and 152,000 hectares in 2017 to 634,000; 947,000, and 105,000 hectares in 2025 respectively.

- Increasing land for cashew from 297,000 hectares in 2017 to 418,000 hectares in 2025.

- Increasing land for fruit trees from 923,000 hectares in 2017 to 1.1 million hectares in 2025.

- Increasing aquaculture areas from 749,000 hectares in 2017 to 790,000 hectares in 2025.

- Increasing forest areas from 15.7 million hectares in 2017 to 16.9 million hectares in 205, marking an increase in the forest coverage rate from 41.45% to 44.53%.

Table 2. Balance of agro-foresty land (thousands of hectares)

Years

2017

2020

2025

Rice

4,030

3,760

3,129

Grassland

140

240

354

Other annual crops

2,730

2,780

3,160

Tea

129

134

140

Coffee

664

650

634

Rubber

971

960

947

Cashew

297

400

418

Pepper

152

130

105

Fruit trees

923

970

1.124

Aquaculture

749

768

790

Forest

15,700

16,245

16,868

Forest coverage rate (%)

41.45

42.89

44.53

Source: Calculation from statistics of MARD, 2017

Balance of water resources

In the context of declining water resources, water resource balancing is developed based on the goal of saving and developing multifunctional irrigation. The total current water resource constitutes about 906 billion m3, but this figure will drop to 867 billion m3 by 2025. Meanwhile, water demand for agricultural production is estimated to rise from 85 billion m3 in 2017 to 92 billion m3 in 2025 (Table 3).

Table 3. Balance of water resources (unit: billion m3)

Source: Calculation from statistics of Department for Irrigation (MARD) and Department for Water Resources Management (MONRE), 2017

Balance of Agricultural Labor

Labor balances are based on the specialization of agricultural labor, increasing the production scale, and developing pro-agricultural services. Two labor balance scenarios are projected as follows:

Table 4. Balance of Agricultural Labor

Source: Estimates based on Census on Agriculture, Forestry and Aquaculture, and IO Balance Sheet, GSO 2016.

Reorganize production of key product groups in value chain

The selection of value chain development for key product groups is based on the following principles:

- Based on the value of the sector

- Enterprise will play as the core element affiliating with other economic entities in the production area that have appropriate production scale

- Developing comprehensive value chain from input to production, processing and consumption

- Applying high-tech to ensure competitiveness in accordance with requirements by markets at all stages

Develop national key products (products with export values of US$ 1 billion or more, together with pork and poultry)

It is necessary to ensure that the areas have a high level of natural adaptability, high socio-economic conditions, production conditions, environment protection, proper landscape and natural resource provision. Large scale production areas should be built with consideration to nationwide production scale to maintain price favorable production level. It is advisable to collaborate with major corporate organizations that are able to lead the value chain of key products, to review the entire planning strategy and planned areas, develop and propose investments in comprehensive value chain in form of clusters. Major corporate organizations are encouraged to affiliate with local SMEs, local authorities, and farmer organizations to implement investments in value chains in the form of Public-Private partnership.

Develop provincial key products

Provinces, based on their advantages and market needs, need to select key products for planning specialized cultivation areas where favorable natural and socio-economic conditions, technical infrastructure and supporting services, as well as convenient traffic routes exist to facilitate the connection to main markets. Main markets for key agricultural products must be identified with priority put on local enterprises as leaders specializing in each product line. It is necessary to connect with processing enterprises, large scale distributors and target markets. The government must act as the bridge between local enterprises, farmer organizations and markets or large processing and trading enterprises by providing market information, market brokerage, and investment brokerage. The government should collaborate with large enterprises, research institutes or associations to carry out modern technology transfer that is suitable for local SMEs and farmers; or develop innovative agricultural incubators for local enterprises and farmers. Agricultural extension work should be renovated with greater participation as technology transfer agent.

Develop local specialty

Local specialty usually has small scale production which are closely linked with specific geographical locations. The development of these products needs to be closely connected to the development of new rural development at commune and district level in accordance with the model of “Each commune has one specialty.” The most suitable location and production unit must be defined; technical processes and criteria must be developed; production plans must be systemized. Developing management capacity for farmers and craft villages of available specialty should be focused on. Intermediate financial brokers and commercial brokers should be attracted to commercialize the specialty in local and international markets.

Policy and institutions measures

- Review planning and production structure in line with the advantages, markets and adaptation to climate change.

- Reform and improve policies, including (i) improving business environment, (ii) reducing tax on agricultural and rural investment, (iii) developing agricultural insurance market, (iv) introducing preferential access to land, enhancing land aggravation and accumulation for farming purposes, and (v) providing support for credit access of all economic sectors investing in agriculture and rural areas.

- Reform and develop cooperatives and farms; develop various forms of value chains, attract private investment, promote PPP, reform state enterprises, and restructure industrial associations.

- Promote and improve vocational training for farmers, shift agricultural labor force to service, industry and rural trades.

- Strengthen research, application and transfer science and technology to agriculture, focusing on variety, production, processing and managing value chain. Adopt preferential policies for development of high-tech, green, clean and organic agriculture.

- Develop, improve and apply standard and norm system as well as technical process.

- Enhance international integration and market development: strengthen the capacity of information, forecast, warning, negotiation, dispute settlement, brand development, origin traceability, and trade promotion for domestic and foreign markets.

- Renovate state manage: consolidate vertical management system; decentralization, increasing local autonomy; socialization of public services and public service delivery bodies.

- Mobilize social resources, focusing on modern infrastructure, strengthening the capacity to prevent and mitigate natural disasters, adapting to climate change and developing new rural areas.

REFERENCES

IPSARD, 2017. Reposistionning Vietnam agriculture. Internal working paper in Vietnamese only.

GSO, 2017. Statistical year book.

GSO. 2016. Census on Agriculture, Forestry and Aquaculture, and IO Balance Sheet

MARD, 2017. Database on Agriculture and Irrigation

MONRE, 2017. Database on landuse and water resources.

ITC-Trademap, 2017.

Date submitted: July 24, 2018

Reviewed, edited and uploaded: Oct. 18, 2018