ABSTRACT

Rice is the most important crop in Cambodia. It is the staple food and contributes to around 26% of the GDP, (MAFF 2017). It is estimated that the sector employs around three million people. The cultivated area increased to 3.6 million hectares with an estimated paddy production of 9.9 million tons. The annual paddy production exceeds the domestic consumption by around five million tons and this surplus is exported paddy or milled rice through informal and formal marketing channels. Milled rice exports through formal channels increased from 2010 onwards after the Royal Government of Cambodia issued a policy on the “Promotion of Paddy Production and Rice Exports”. Since 2010 the rice sector and especially the milling sector modernized rapidly and now meets the standards required in the International market. Cambodia’s rice exports increased rapidly in the past seven years and export data from the Secretariat of the One window service for Rice Export formalities (SOW-REF) show that it grew from 105,259 metric tons in 2010 to 635,679 metric tons in 2017. The main share of the exports is aromatic rice (63%) followed by long grain white rice (25%) and parboiled rice (12%). Under the Generalized Scheme of Preferences (GSP) Cambodia enjoys duty free imports into the European Union under the Everything But Arms (EBA) clause for Least Developed Countries. The EU is therefore the largest destination for Cambodian rice followed by China and ASEAN countries. Cambodia developed several aromatic rice varieties such as Phka Rumduol, Phka Romeat and Phka Rumdeng and Cambodian fragrant rice won the title of “World’s Best Rice” for three consecutive years (2012 – 2014). A new challenge for the Cambodian rice sector is the increasing demand for organic and sustainable rice. Although still a niche market, traceability “from farm to fork” will require strictly monitored contract farming which is new to Cambodia. In common with neighboring countries, farmers in Cambodia predominantly use farm saved seed and due to lack of labor have moved from transplanting to hand broadcasting using seeding rates of up to 400 kg/ha. Direct seeding using mechanical seeders has the potential to lower seeding rates to 60 – 100 kg/ha which may give farmers the incentive to use certified seed and thereby increasing the quality of paddy delivered to the mills. Even though Cambodia’s exports have increase significantly over the past years there are several areas where improvement is necessary to compete in the International markets. These areas include reduction of logistical costs through better administration, improved infrastructure, improvement of the supply chain management, promotion of the Angkor Malys certification mark, the adoption of Good Agricultural Practices and the promotion of value added by-products from rice.

Key words: Fragrant rice, Everything But Arms (EBA), traceability, quality of paddy, logistic cost, certification mark, Good Agriculture Practice (GAP)

INTRODUCTION

Rice is the most important crop in Cambodia. It is the staple food and the dominating crop in agriculture which contributes to around 26% of the GDP (MAFF 2017). It is estimated that rice production, processing and market employ around 3 million of the 15 million population. Paddy production occupies around 75% of the cultivated land and rice contributes around 15% of the total agricultural value added (IFC 2015).

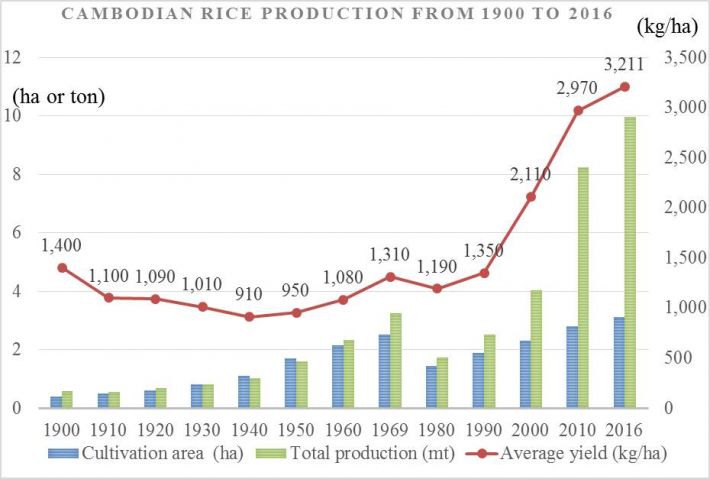

The cultivated area for rice in Cambodia is around 3.052 million hectares in 2016. It comprises of two main seasons-wet season and dry season. Wet season covers around 74% of the total cultivated land and dry season approximately 16% (MAFF 2017). Rice production has increased significantly during the last decade. The production volume has increased more than double from 2000 to 2016. The data shows that the estimated paddy production in 2016 increases to 9.9 million metric tons in 2016 compared to only 4 million metric ton in 2000 (MAFF, 2017). This leaves around 5.1-million-ton surplus of paddy and potential 3.2 million tons of milled rice for export (See Fig. 1).

Fig. 1. Cambodia Rice Production from 1900 to 2016

Source: MAFF 2017

OVERVIEW OF RICE PERFORMANCE IN CAMBODIA

Export market

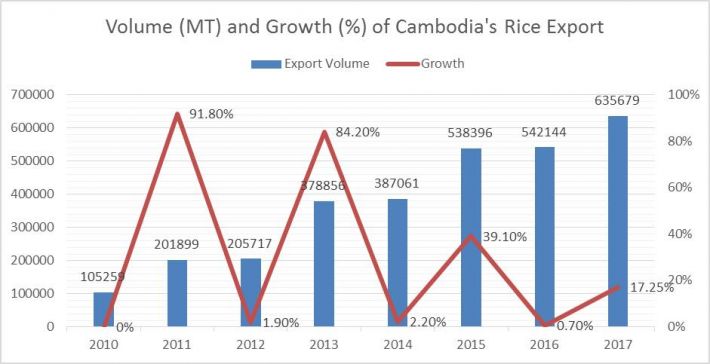

Cambodia’s formal rice export has increased noticeably during the last seven years. In 2010 Cambodia exported only 100,000 metric ton of milled rice, while in 2013 the volume increased to around 378,000 metric tons and transformed itself from a pure paddy trader to a milled rice exporter (Trade map, 2018). Volume of export has reached 542,144 metric tons in 2016 (see Table1 below). Share of Cambodia’s rice export volume in global rice export increased gradually from 0.15% in 2010 to 1.33% in 2016. This market share made Cambodia ranked 12th largest rice export country in 2016 (Trademap 2017).

Cambodian rice sector has gradually transformed the production quality and processing standard, which is accepted by international buyers. The transformation of the rice sector is driven by a number of factors including: 1) a more strategic, coordinated and export focus approach to the industry’s development; 2) Improved and modernized milling capacity; 3) A domestic policy that opens door to access the international market; and 4) Generalized Preferential System (GSP) advantage to export to EU without tariff, (Cambodia CTIS 2014-2018).

Fig. 2. Cambodia Rice Export Volume 2010 to 2017

Market destination

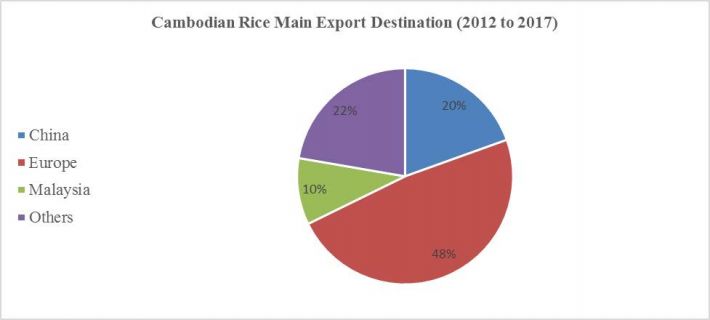

As a least developed country and under the Generalized Preferential System (GSP) Cambodia enjoys duty free imports into the European Union (EU) under the Everything But Arms (EBA). The EU is therefore the largest destination for Cambodian rice market followed by China and ASEAN countries. As shown in the graph below European market shares about 48% of the total export volume from 2012 to 2017. China, the second biggest importer of Cambodia rice, absorbs around 20% of the total export volume during the last six years. Rice export to China increased especially from 2015 when an MOU was signed between the governments of Cambodia and China to allow 100,000 metric tons milled rice quota to latter country per year in 2016, and 200,000 metric tons in 2017. The amount has increased to 300,000 this year, 2018. Malaysia shares 10% and other countries 22%.

Fig. 3. Cambodian rice main export destination 2012 to 2017 (Source: MAFF 2018)

Export value

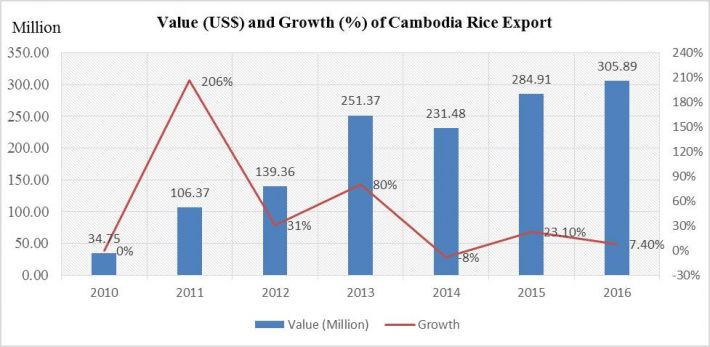

The value of rice export increased significantly between 2010 and 2016. In 2010, Cambodia earned about US$34 million from rice export to the international market. The value had an eightfold increase to US$285 million in 2015 and US$300 million in 2016. Between 2015 and 2016, although volume of rice export only increased 0.7%, the export value grew about 7% (Trademap 2017)

Fig. 4. Value and growth of rice export in Cambodia

Types of rice export s

According to Cambodia’s Trade Integration Strategy report, 2014-2018, there are three types of rice exports in Cambodia. First, the informal and unrecorded of paddy flow through land and waterway crossing border to Vietnam and Thailand. Second, the informal and unrecorded milled rice export to Thailand via land border crossing. Finally, it is the formal channel of export through port of Sihanoukville and Phnom Penh.

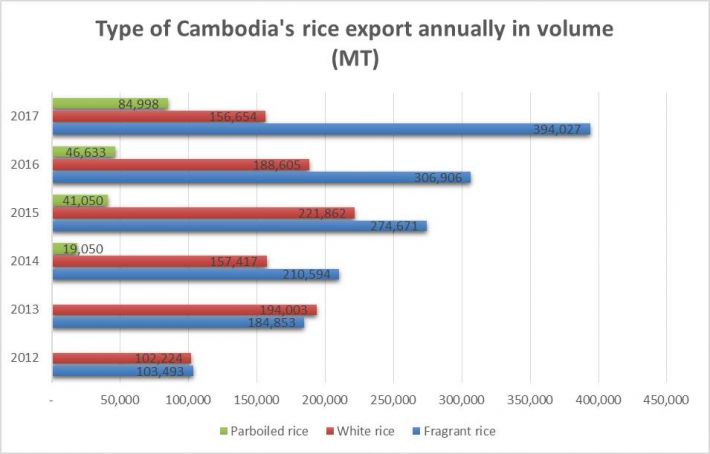

The formal channel mainly exports four types of rice to the international rice market including Premium Jasmine Rice, Aromatic Rice, Long Grain White Rice and Long Grain Parboiled Rice. The first categories include Phka Rumduol, Phka Romeat, Phka Rumdeng and Somaly varieties. Phka Rumduol variety won the world best rice for three consecutively years in 2012, 2013 and 2014. After that Cambodia positions itself as the second rank of the world best rice. The aromatic rice mainly comprises of Sen Kra Ob variety, Sen Pidor and Phka Chansensor varieties. Long grain white rice and long grain par boiled rice are usually processed from white rice variety such as IR 66 and IR 504 04.

Fig. 5. Volume of cambodia rice export variety

Challenges in the Cambodian rice market

There is a change of consumer’s behavior for rice consumption for higher health and safety standard. In China, consumers prefer health and safety food (Lu 2018). Consumers in Europe are also in favor of exotic varieties such as Basmati, Jasmine and organic rice. This demand shows a growth of 6% annually (CBI 2017).

Both buyers and consumers in Europe have a growing concern about sustainability and social affect from their consumption. This pressures rice millers/exports to have a traceability system in place – one that is aligned with the standard requirement. Sustainable Rice Platform (SRP) which is co-convened by IRRI and UNEP in 2011 with involvement of 29 institutions from public and private sector stakeholders, research, financial institutions and NGOs, is now implementing with some exporters in Cambodia in the form of contract farming to supply to few large retailers in Europe such as Mars Food. The Royal Government of Cambodia issued a sub-decree on contract farming in 2011 to facilitate farmers and private companies. However, the farming agreement seems inactive as it is quite new in Cambodia. Until 2014, there are few millers/exporters started to implement their contract farming with agriculture cooperatives (ACs) in Preah Vihear province for organic rice and the implementation of contract farming for SRP has just started in 2017. According the interview with some ACs of organic and SRP of contract farming, all members of the cooperatives have not joined the contract farming with millers/exporters yet because they do not still trust the contract.

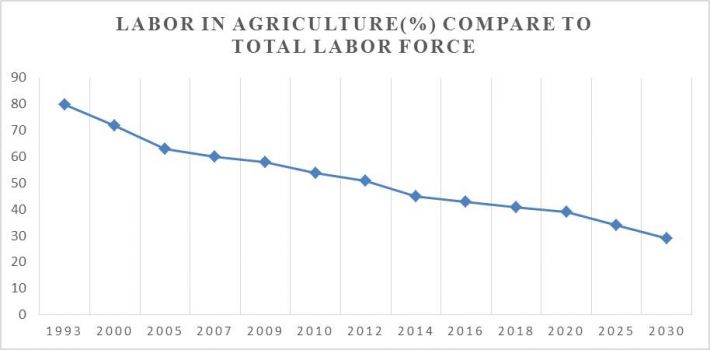

Another challenge is a labor reduction in agriculture sector. Labor in agriculture decreases from 80% in 1993 to 41% in 2018 (MAFF 2017). It is projected that the labor will continue to decrease from year to year and remain only 29% in 2030 (see Fig. 6).

Fig. 6. Labor force in agriculture as compared to overall labor force

Due to labor shortage, farmers in Cambodia change practice from transplanting to broadcasting. As common to other neighboring, farmers use saved seed rather than buying certified seed for paddy production. In addition, Cambodian farmers use a large amount of seeds with an average of 230 kilograms per hectares for dry season variety and 134 kilograms per hectares for wet season variety. Some farmers use up to 400 kilograms of seed per hectare (CAVAC 2016). Using saved seed for many cropping cycles leads to poor quality of paddy and because they apply high seed rate, they have less incentive to buy certified seed for their production. The same study found that certified seed costs US$0.75 per kilogram while farmers’ saved seed just cost them US$0.3 per kilogram. CAVAC has introduced mechanical direct seeders through few companies for dry and wet soil condition. It is shown that the machine can potentially lower seed rate to 60 kilograms per hectare for wet season variety and 100 kilograms per hectare for dry season variety.

Cambodian rice exporters still claim that farmers do not storage the paddy properly after harvesting, which leads to poor quality of paddy for milling (Chan and Kim 2017). Cambodia has higher electricity cost than Vietnam, Thailand and Myanmar. The cost of electricity in Cambodia in 2015 was US$0.177 per kilowatt hour that was higher than Vietnam whose price is only US$0.06, Thailand US$0.046 and Myanmar US$0.054. There was an effort to reduce cost of electricity for rice milling to 0.166 US$ per kilowatt hour but this price remains high for millers. Related by-products of milled rice such as husk and bran are not yet fully utilized or processed yet due to lack of knowledge and technology. Silica that can be produced from rice husk and rice bran oil from rice bran are not seen any production in Cambodia (Profound 2017).

Logistic and milling cost is still a main constraint for exporters in Cambodia. Even though there has been progress in simplifying export procedures and reducing the logistic costs, it is not competitive enough comparing to Cambodia’s competitors (Goletti and Srey 2016). Chan and Kim (2017) showed that Cambodia’s gasoline price is USD0.9 per liter, while Vietnam’s gasoline price is USD0.81 per liter and USD0.51 per liter in Myanmar. Thailand’s gasoline price is 1.04 US$ per liter but most trucks in Thailand are equipped with LPG that costs about half of the gasoline price. Cambodia roads are not easy access everywhere yet. Some areas are not possible for large trucks with 20-metric-ton capacity to access for collecting paddy. Farmers still need to use hand tractors to transport paddy to large trucks. In addition, the Cambodia government has tried an effort to rehabilitate railroad to reduce costs of transportation but it is still not ready and applicable for exporter to use this transportation mode yet.

Myanmar is an emerging competitor for Cambodia rice export to international market as it re-granted again Everything But Arms (EBA) initiative preferential trade regime in 2013 and the trade preferences for Myanmar is applied retroactively as of June 2012. Therefore, Myanmar seems to be a large low-cost rice exporter that competes with Cambodia. Global rice market is unpredictable. In addition, Thailand is seen as a main competitor for fragrant rice and Vietnam for white rice (RGC 2014). As a result, Cambodia’s export is stagnated between 2015 and 2016. Volume of export was 538,396 MT and 542,144 MT respectively, due to those factors including price of Thai rice failed down. In addition, Vietnam is also competitor that can increase its market share in EU because it just obtained quota for Free Trade Agreement for 20,000 MT of milled rice and it is effective in 2018. Lastly, Myanmar and Vietnam have set a policy to produce fragrant rice to meet demand in international market.

CONCLUSION

Cambodia can stay its optimal success in the market if there has been an effort from Cambodian Rice Federation (CRF), government and developing agencies to develop a certification mark “Malys Angkor”. It is the first certification mark developed in Cambodia and launched in January 2018. CRF who owns the mark will need to work more to strengthen traceability and transparency in order to promote this mark for national and international market. It is recommended that high quality of Cambodian fragrant rice should be sold on the basis of brand and value, rather than on a price basis in the market (IFC 2015).

Besides SRP, Good Agricultural Practice (GAP) is generally recognised as a series of measures to increase food safety for domestic and foreign consumers. It is a kind of sustainable system of agriculture that provide health and safety to farmers and other operators along the supply chain. EUREPGAP became Global GAP in 2007, initiated by retailer association in Europe to address the concerns of consumers regarding safety, environmental impact and health, safety and welfare of workers and animals. Thailand already developed national standard, ThaiGAP, in 2008. Vietnam also has VietGAP. However, Cambodia does not start any initiative yet for Rice GAP. Since consumers’ behavior change over health and safety is growing in foreign countries it might also affect local consumers. Cambodia government should also take measure to protect its population to live healthier and in better environment. Therefore, adoption of GAP in the country should be undertaken soon.

REFERENCES

CAVAC, 2016. Farmers' Behavior on Using Rice Seed in Cambodia. Phnom Penh: Cambodian Agriculture Value Chain Program (CAVAC).

CBI, 2017. Exporting specialty rice varieties to Europe. Center for Import Promotion from Least Developed Countries.

Goletti, F and C. Srey, 2016. Draft Report of Review of the Rice Policy. Phnom Penh: Supreme National Economic Council (SNEC).

IFC, 2015. Cambodia Rice Export Potential and Strategies. Phnom Penh: International Finance Corporation.

Lu, Y. ,2018. China’s Agricultural Supply Side Strutural Reform and Opportunity for Cambodian Green Rice. Power Point Presentation. China: COFCO Group.

MAFF, 2017. Cambodian Agriculture Master Plan 2017 - 2030. Phnom Penh: Ministry of Agriculture Forestry and Fisheries.

Profound, 2017. European for value added rice products. Center for Export Promotion from Least Developed Countries.

RGC, 2010. Policy Paper on Promotiong of Paddy Production and Milled Rice Export. Royal Government of Cambodia

RGC, 2014. Cambodia's Diagnostic Trade Integration Strategy and Trade SWAp Roadmap 2014-2018. Phnom Penh: Royal Government of Cambodia. Royal Government of Cambodia

Chan, S. and M. Kim, 2017. Understanding Stagnation of Cambodia's Rice Export. Phnom Penh.

SOWS-REF, 2017. Secretariat of One-Window Service for Rice Export Formality.

Trademap, 2017. www.trademap.org. Retrieved from www.trademap.org

|

(Submitted as a paper for the International Seminar on “Promoting Rice Farmers’ Market through value-adding Activities”, June 6-7, 2018, Kasetsart University, Thailand)

|

Overview of the Cambodian Rice Market_ Challenges and the way forward

ABSTRACT

Rice is the most important crop in Cambodia. It is the staple food and contributes to around 26% of the GDP, (MAFF 2017). It is estimated that the sector employs around three million people. The cultivated area increased to 3.6 million hectares with an estimated paddy production of 9.9 million tons. The annual paddy production exceeds the domestic consumption by around five million tons and this surplus is exported paddy or milled rice through informal and formal marketing channels. Milled rice exports through formal channels increased from 2010 onwards after the Royal Government of Cambodia issued a policy on the “Promotion of Paddy Production and Rice Exports”. Since 2010 the rice sector and especially the milling sector modernized rapidly and now meets the standards required in the International market. Cambodia’s rice exports increased rapidly in the past seven years and export data from the Secretariat of the One window service for Rice Export formalities (SOW-REF) show that it grew from 105,259 metric tons in 2010 to 635,679 metric tons in 2017. The main share of the exports is aromatic rice (63%) followed by long grain white rice (25%) and parboiled rice (12%). Under the Generalized Scheme of Preferences (GSP) Cambodia enjoys duty free imports into the European Union under the Everything But Arms (EBA) clause for Least Developed Countries. The EU is therefore the largest destination for Cambodian rice followed by China and ASEAN countries. Cambodia developed several aromatic rice varieties such as Phka Rumduol, Phka Romeat and Phka Rumdeng and Cambodian fragrant rice won the title of “World’s Best Rice” for three consecutive years (2012 – 2014). A new challenge for the Cambodian rice sector is the increasing demand for organic and sustainable rice. Although still a niche market, traceability “from farm to fork” will require strictly monitored contract farming which is new to Cambodia. In common with neighboring countries, farmers in Cambodia predominantly use farm saved seed and due to lack of labor have moved from transplanting to hand broadcasting using seeding rates of up to 400 kg/ha. Direct seeding using mechanical seeders has the potential to lower seeding rates to 60 – 100 kg/ha which may give farmers the incentive to use certified seed and thereby increasing the quality of paddy delivered to the mills. Even though Cambodia’s exports have increase significantly over the past years there are several areas where improvement is necessary to compete in the International markets. These areas include reduction of logistical costs through better administration, improved infrastructure, improvement of the supply chain management, promotion of the Angkor Malys certification mark, the adoption of Good Agricultural Practices and the promotion of value added by-products from rice.

Key words: Fragrant rice, Everything But Arms (EBA), traceability, quality of paddy, logistic cost, certification mark, Good Agriculture Practice (GAP)

INTRODUCTION

Rice is the most important crop in Cambodia. It is the staple food and the dominating crop in agriculture which contributes to around 26% of the GDP (MAFF 2017). It is estimated that rice production, processing and market employ around 3 million of the 15 million population. Paddy production occupies around 75% of the cultivated land and rice contributes around 15% of the total agricultural value added (IFC 2015).

The cultivated area for rice in Cambodia is around 3.052 million hectares in 2016. It comprises of two main seasons-wet season and dry season. Wet season covers around 74% of the total cultivated land and dry season approximately 16% (MAFF 2017). Rice production has increased significantly during the last decade. The production volume has increased more than double from 2000 to 2016. The data shows that the estimated paddy production in 2016 increases to 9.9 million metric tons in 2016 compared to only 4 million metric ton in 2000 (MAFF, 2017). This leaves around 5.1-million-ton surplus of paddy and potential 3.2 million tons of milled rice for export (See Fig. 1).

Fig. 1. Cambodia Rice Production from 1900 to 2016

Source: MAFF 2017

OVERVIEW OF RICE PERFORMANCE IN CAMBODIA

Export market

Cambodia’s formal rice export has increased noticeably during the last seven years. In 2010 Cambodia exported only 100,000 metric ton of milled rice, while in 2013 the volume increased to around 378,000 metric tons and transformed itself from a pure paddy trader to a milled rice exporter (Trade map, 2018). Volume of export has reached 542,144 metric tons in 2016 (see Table1 below). Share of Cambodia’s rice export volume in global rice export increased gradually from 0.15% in 2010 to 1.33% in 2016. This market share made Cambodia ranked 12th largest rice export country in 2016 (Trademap 2017).

Cambodian rice sector has gradually transformed the production quality and processing standard, which is accepted by international buyers. The transformation of the rice sector is driven by a number of factors including: 1) a more strategic, coordinated and export focus approach to the industry’s development; 2) Improved and modernized milling capacity; 3) A domestic policy that opens door to access the international market; and 4) Generalized Preferential System (GSP) advantage to export to EU without tariff, (Cambodia CTIS 2014-2018).

Fig. 2. Cambodia Rice Export Volume 2010 to 2017

Market destination

As a least developed country and under the Generalized Preferential System (GSP) Cambodia enjoys duty free imports into the European Union (EU) under the Everything But Arms (EBA). The EU is therefore the largest destination for Cambodian rice market followed by China and ASEAN countries. As shown in the graph below European market shares about 48% of the total export volume from 2012 to 2017. China, the second biggest importer of Cambodia rice, absorbs around 20% of the total export volume during the last six years. Rice export to China increased especially from 2015 when an MOU was signed between the governments of Cambodia and China to allow 100,000 metric tons milled rice quota to latter country per year in 2016, and 200,000 metric tons in 2017. The amount has increased to 300,000 this year, 2018. Malaysia shares 10% and other countries 22%.

Fig. 3. Cambodian rice main export destination 2012 to 2017 (Source: MAFF 2018)

Export value

The value of rice export increased significantly between 2010 and 2016. In 2010, Cambodia earned about US$34 million from rice export to the international market. The value had an eightfold increase to US$285 million in 2015 and US$300 million in 2016. Between 2015 and 2016, although volume of rice export only increased 0.7%, the export value grew about 7% (Trademap 2017)

Fig. 4. Value and growth of rice export in Cambodia

Types of rice export s

According to Cambodia’s Trade Integration Strategy report, 2014-2018, there are three types of rice exports in Cambodia. First, the informal and unrecorded of paddy flow through land and waterway crossing border to Vietnam and Thailand. Second, the informal and unrecorded milled rice export to Thailand via land border crossing. Finally, it is the formal channel of export through port of Sihanoukville and Phnom Penh.

The formal channel mainly exports four types of rice to the international rice market including Premium Jasmine Rice, Aromatic Rice, Long Grain White Rice and Long Grain Parboiled Rice. The first categories include Phka Rumduol, Phka Romeat, Phka Rumdeng and Somaly varieties. Phka Rumduol variety won the world best rice for three consecutively years in 2012, 2013 and 2014. After that Cambodia positions itself as the second rank of the world best rice. The aromatic rice mainly comprises of Sen Kra Ob variety, Sen Pidor and Phka Chansensor varieties. Long grain white rice and long grain par boiled rice are usually processed from white rice variety such as IR 66 and IR 504 04.

Fig. 5. Volume of cambodia rice export variety

Challenges in the Cambodian rice market

There is a change of consumer’s behavior for rice consumption for higher health and safety standard. In China, consumers prefer health and safety food (Lu 2018). Consumers in Europe are also in favor of exotic varieties such as Basmati, Jasmine and organic rice. This demand shows a growth of 6% annually (CBI 2017).

Both buyers and consumers in Europe have a growing concern about sustainability and social affect from their consumption. This pressures rice millers/exports to have a traceability system in place – one that is aligned with the standard requirement. Sustainable Rice Platform (SRP) which is co-convened by IRRI and UNEP in 2011 with involvement of 29 institutions from public and private sector stakeholders, research, financial institutions and NGOs, is now implementing with some exporters in Cambodia in the form of contract farming to supply to few large retailers in Europe such as Mars Food. The Royal Government of Cambodia issued a sub-decree on contract farming in 2011 to facilitate farmers and private companies. However, the farming agreement seems inactive as it is quite new in Cambodia. Until 2014, there are few millers/exporters started to implement their contract farming with agriculture cooperatives (ACs) in Preah Vihear province for organic rice and the implementation of contract farming for SRP has just started in 2017. According the interview with some ACs of organic and SRP of contract farming, all members of the cooperatives have not joined the contract farming with millers/exporters yet because they do not still trust the contract.

Another challenge is a labor reduction in agriculture sector. Labor in agriculture decreases from 80% in 1993 to 41% in 2018 (MAFF 2017). It is projected that the labor will continue to decrease from year to year and remain only 29% in 2030 (see Fig. 6).

Fig. 6. Labor force in agriculture as compared to overall labor force

Due to labor shortage, farmers in Cambodia change practice from transplanting to broadcasting. As common to other neighboring, farmers use saved seed rather than buying certified seed for paddy production. In addition, Cambodian farmers use a large amount of seeds with an average of 230 kilograms per hectares for dry season variety and 134 kilograms per hectares for wet season variety. Some farmers use up to 400 kilograms of seed per hectare (CAVAC 2016). Using saved seed for many cropping cycles leads to poor quality of paddy and because they apply high seed rate, they have less incentive to buy certified seed for their production. The same study found that certified seed costs US$0.75 per kilogram while farmers’ saved seed just cost them US$0.3 per kilogram. CAVAC has introduced mechanical direct seeders through few companies for dry and wet soil condition. It is shown that the machine can potentially lower seed rate to 60 kilograms per hectare for wet season variety and 100 kilograms per hectare for dry season variety.

Cambodian rice exporters still claim that farmers do not storage the paddy properly after harvesting, which leads to poor quality of paddy for milling (Chan and Kim 2017). Cambodia has higher electricity cost than Vietnam, Thailand and Myanmar. The cost of electricity in Cambodia in 2015 was US$0.177 per kilowatt hour that was higher than Vietnam whose price is only US$0.06, Thailand US$0.046 and Myanmar US$0.054. There was an effort to reduce cost of electricity for rice milling to 0.166 US$ per kilowatt hour but this price remains high for millers. Related by-products of milled rice such as husk and bran are not yet fully utilized or processed yet due to lack of knowledge and technology. Silica that can be produced from rice husk and rice bran oil from rice bran are not seen any production in Cambodia (Profound 2017).

Logistic and milling cost is still a main constraint for exporters in Cambodia. Even though there has been progress in simplifying export procedures and reducing the logistic costs, it is not competitive enough comparing to Cambodia’s competitors (Goletti and Srey 2016). Chan and Kim (2017) showed that Cambodia’s gasoline price is USD0.9 per liter, while Vietnam’s gasoline price is USD0.81 per liter and USD0.51 per liter in Myanmar. Thailand’s gasoline price is 1.04 US$ per liter but most trucks in Thailand are equipped with LPG that costs about half of the gasoline price. Cambodia roads are not easy access everywhere yet. Some areas are not possible for large trucks with 20-metric-ton capacity to access for collecting paddy. Farmers still need to use hand tractors to transport paddy to large trucks. In addition, the Cambodia government has tried an effort to rehabilitate railroad to reduce costs of transportation but it is still not ready and applicable for exporter to use this transportation mode yet.

Myanmar is an emerging competitor for Cambodia rice export to international market as it re-granted again Everything But Arms (EBA) initiative preferential trade regime in 2013 and the trade preferences for Myanmar is applied retroactively as of June 2012. Therefore, Myanmar seems to be a large low-cost rice exporter that competes with Cambodia. Global rice market is unpredictable. In addition, Thailand is seen as a main competitor for fragrant rice and Vietnam for white rice (RGC 2014). As a result, Cambodia’s export is stagnated between 2015 and 2016. Volume of export was 538,396 MT and 542,144 MT respectively, due to those factors including price of Thai rice failed down. In addition, Vietnam is also competitor that can increase its market share in EU because it just obtained quota for Free Trade Agreement for 20,000 MT of milled rice and it is effective in 2018. Lastly, Myanmar and Vietnam have set a policy to produce fragrant rice to meet demand in international market.

CONCLUSION

Cambodia can stay its optimal success in the market if there has been an effort from Cambodian Rice Federation (CRF), government and developing agencies to develop a certification mark “Malys Angkor”. It is the first certification mark developed in Cambodia and launched in January 2018. CRF who owns the mark will need to work more to strengthen traceability and transparency in order to promote this mark for national and international market. It is recommended that high quality of Cambodian fragrant rice should be sold on the basis of brand and value, rather than on a price basis in the market (IFC 2015).

Besides SRP, Good Agricultural Practice (GAP) is generally recognised as a series of measures to increase food safety for domestic and foreign consumers. It is a kind of sustainable system of agriculture that provide health and safety to farmers and other operators along the supply chain. EUREPGAP became Global GAP in 2007, initiated by retailer association in Europe to address the concerns of consumers regarding safety, environmental impact and health, safety and welfare of workers and animals. Thailand already developed national standard, ThaiGAP, in 2008. Vietnam also has VietGAP. However, Cambodia does not start any initiative yet for Rice GAP. Since consumers’ behavior change over health and safety is growing in foreign countries it might also affect local consumers. Cambodia government should also take measure to protect its population to live healthier and in better environment. Therefore, adoption of GAP in the country should be undertaken soon.

REFERENCES

CAVAC, 2016. Farmers' Behavior on Using Rice Seed in Cambodia. Phnom Penh: Cambodian Agriculture Value Chain Program (CAVAC).

CBI, 2017. Exporting specialty rice varieties to Europe. Center for Import Promotion from Least Developed Countries.

Goletti, F and C. Srey, 2016. Draft Report of Review of the Rice Policy. Phnom Penh: Supreme National Economic Council (SNEC).

IFC, 2015. Cambodia Rice Export Potential and Strategies. Phnom Penh: International Finance Corporation.

Lu, Y. ,2018. China’s Agricultural Supply Side Strutural Reform and Opportunity for Cambodian Green Rice. Power Point Presentation. China: COFCO Group.

MAFF, 2017. Cambodian Agriculture Master Plan 2017 - 2030. Phnom Penh: Ministry of Agriculture Forestry and Fisheries.

Profound, 2017. European for value added rice products. Center for Export Promotion from Least Developed Countries.

RGC, 2010. Policy Paper on Promotiong of Paddy Production and Milled Rice Export. Royal Government of Cambodia

RGC, 2014. Cambodia's Diagnostic Trade Integration Strategy and Trade SWAp Roadmap 2014-2018. Phnom Penh: Royal Government of Cambodia. Royal Government of Cambodia

Chan, S. and M. Kim, 2017. Understanding Stagnation of Cambodia's Rice Export. Phnom Penh.

SOWS-REF, 2017. Secretariat of One-Window Service for Rice Export Formality.

Trademap, 2017. www.trademap.org. Retrieved from www.trademap.org

(Submitted as a paper for the International Seminar on “Promoting Rice Farmers’ Market through value-adding Activities”, June 6-7, 2018, Kasetsart University, Thailand)