ABSTRACT

This study investigates the evolving landscape and systemic challenges within Thailand's agricultural logistics, with a focus on impediments to efficiency and competitiveness. These include transportation inefficiencies, infrastructure deficits, and fragmented data management across various governmental bodies. The research assesses Thailand's potential to serve as a regional logistics center in ASEAN, aligning with the National Action Plan for Agricultural Logistics Development. The results indicate that despite advancements in infrastructure, significant challenges remain. These encompass elevated logistics expenditures, disjointed data infrastructures, limited logistical expertise among agricultural producers, and external disruptions to agricultural supply networks. Policy recommendations underscore the necessity of infrastructure investments in agriculturally significant regions, the adoption of digital logistics solutions, and the empowerment of farmers through knowledge enhancement. A strategic framework is proposed to synergize national and local strategies with academic research and private-sector involvement, to stimulate innovation, market adaptability, and competitive advantages.

Keywords: Thailand agricultural logistics, infrastructure development, ASEAN regional hub, logistics policy

INTRODUCTION

Thailand's ambition to establish itself as a key ASEAN regional hub is contingent on the advancement and effectiveness of its agricultural logistics system. This requires a comprehensive analysis of the existing infrastructure, operational challenges, and technological integration within the country's agricultural supply chains. As ASEAN continues to pursue regional integration, the need for a resilient logistics sector to support the exchange of goods is becoming increasingly important, with the varying levels of development among Southeast Asian cities presenting both challenges and opportunities (Nguyen, 2020).

To effectively leverage regional integration, Thailand must strategically invest in its logistics infrastructure and cultivate a comprehensive understanding of trade routes and economic development within its agricultural logistics system. Agriculture remains a strategic sector in Thailand’s economy, providing a livelihood for a substantial portion of the population and serving as a major source of export revenue. In 2024, the export value of Thailand’s agricultural and agro-industrial products exceeded US$52 billion, constituting a significant percentage of the country’s total exports (Trade Policy and Strategy Office, 2025).

Thailand's leading agricultural exports demonstrate its rich natural resources and established agro-industrial capabilities. Likewise, processed agricultural products, including canned seafood, pet food, and refined sugar, reinforce the country's standing in global food supply networks.

However, despite robust global demand, the efficiency and resilience of Thailand’s agricultural export logistics system present ongoing challenges. Given that a significant portion of these exports is perishable, a highly coordinated cold chain, advanced warehousing, and effective multimodal transport systems are essential. Nevertheless, the country’s logistics remain heavily dependent on road transport, which accounted for 78.31% of total agricultural freight in 2023, while rail and water transport accounted for only 2.21% and 19.47%, respectively (National Economic and Social Development Council, 2024). This reliance on road transport increases logistics costs, limits scalability, and elevates the risk of delays and spoilage.

The COVID-19 pandemic exposed critical weaknesses within Thailand's cross-border agricultural logistics framework, most notably when rigorous health protocols precipitated delays at border checkpoints. These disruptions disproportionately affected the timely transit of perishable commodities, particularly at the Chinese border under the “Zero-COVID” strategy, resulting in elevated spoilage rates for fruit exports during peak harvesting periods and precipitating considerable financial detriments for both exporters and agricultural producers (Department of International Trade Promotion, 2023).

Furthermore, Thailand’s agricultural logistics infrastructure is characterized by fragmentation and a heterogeneous distribution of refrigerated storage and warehousing capabilities, which exacerbates post-harvest wastage (Office of Agricultural Economics, 2023). The assimilation of advanced information technology, automated systems, and comprehensive traceability mechanisms remains preliminary, especially amongst small and medium-sized enterprises operating within Thailand’s agri-business sector. Consequently, the fortification of logistics capabilities is paramount to sustaining export competitiveness, conforming to stringent international sanitary and phytosanitary regulations, and minimizing post-harvest losses.

Thailand stands to gain from multilateral initiatives like the GMS Cross-Border Transport Facilitation Agreement and ASEAN transport agreements by improving its connectivity, harmonizing transport regulations, and promoting multimodal logistics across borders. Simultaneously, the rapid expansion of Thailand's digital commerce, with e-commerce projections exceeding US$118.56 billion, driven by shifting consumer behaviors and the rise of meta-commerce (Pakawachkrilers, 2022), positions the nation as a prominent player in ASEAN B2C e-commerce. This encourages the adoption of digital channels among businesses, particularly small and medium-sized enterprises, thereby enhancing supply chain efficiency and fostering new economic opportunities for agricultural producers and community enterprises (Ilyas, Hu, & Wiwattanakornwong, 2020; Trade Policy and Strategy Office, 2025).

Ultimately, Thailand’s continued success in agricultural exports depends on its ability to enhance logistics infrastructure, invest in cold chain networks, develop human capital, and leverage regional cooperation to overcome structural inefficiencies. The findings of this study contribute to these national objectives by offering evidence-based insights to inform strategic planning and infrastructure investment, fostering a more competitive, sustainable, and integrated agricultural logistics system.

ASEAN Context and Thailand’s Strategic Potential

The ASEAN region's significance in global agricultural trade and production is underpinned by its rich endowment of natural resources, amenable climatic conditions, and abundant labor supply, fostering the cultivation of diverse agricultural commodities. Thailand, under its founding membership in ASEAN, holds strategic advantages derived from its geographic location and well-developed multimodal transport infrastructure, enabling seamless connectivity with adjacent nations via terrestrial, fluvial, pipeline, and aerial routes. These synergistic geographical and infrastructural assets position Thailand favorably as a potential nucleus for agricultural logistics within the Southeast Asian region.

The Economic Significance of Agricultural Logistics

Agricultural logistics is a vital mechanism that enhances the competitiveness of agricultural products by managing all stages of the supply chain, including storage, transportation, processing, and distribution to end consumers. An efficient logistics system contributes to reducing production costs, preserving product quality, increasing value, and strengthening market confidence both domestically and internationally. According to the Office of Agricultural Economics (2024), Thailand has a total agricultural area of 23.64 million hectares, which accounts for 46.7% of the country’s total land area. The agricultural sector supports over 30 million people, with approximately 19.72 million engaged in agricultural labor and around 7.9 million farming households. Furthermore, data from the Trade Policy and Strategy Office (2025) indicates that Thailand’s total export value in 2024 reached US$300.53 billion, reflecting a 5.4% increase from the previous year. Exports of agricultural and agro-industrial products represented 17.36% of the total, amounting to US$52.19 billion, which is a 6.0% growth compared to 2023. These numbers highlight the strategic significance of the agricultural sector in Thailand’s economy, especially amid the challenges posed by geopolitical uncertainty, natural disasters, and increasing global competition.

Vision: Thailand as ASEAN’s Agricultural Logistics Hub

The Ministry of Agriculture and Cooperatives of Thailand has established an Action Plan for the Development of Agricultural Logistics Systems (2023–2027), with the strategic vision of positioning Thailand as a central agricultural logistics hub within ASEAN. This initiative is designed to cultivate extensive logistics infrastructure, build the capabilities of agricultural producers and agribusinesses, and promote the integration of advanced technologies and innovations. The primary objectives include decreasing logistics expenses and improving operational effectiveness throughout the agricultural supply chain, from production sites to consumers. Furthermore, the plan underscores the importance of cultivating human capital, reinforcing institutional proficiency in the agricultural domain, and fostering a competitive business environment for agriculture at both regional and global scales.

Objective of the Article

This study provides an in-depth examination of Thailand's agricultural logistics system, highlighting key structural challenges that undermine its efficiency and competitiveness. These challenges encompass transport inefficiencies, inadequacies in specialized infrastructure, and a lack of integrated data systems across relevant institutions. The feasibility of positioning Thailand as a central agricultural logistics hub within ASEAN is assessed, aligning with the national Action Plan for Agricultural Logistics Development (2023–2027), to inform policy development and strategic progress at the national level.

THEORY AND EMPIRICAL PERSPECTIVES

Logistics Cost Structure and Logistics Performance Index in Thailand

Thailand has consistently worked to improve its logistics system's competitiveness at both regional and global levels. The Logistics Performance Index, created by the World Bank, is a crucial macro-level indicator for assessing this advancement. This index includes elements such as infrastructure quality, tracking capabilities, timeliness, and the effectiveness of international shipments. Moreover, the composition of logistics costs as a proportion of GDP offers an empirical overview of the strengths, weaknesses, and patterns in the nation's logistics system.

Thailand’s logistics performance in Table 1 is captured in the LPI Global Rankings, where in 2018, the top five performing countries were Germany, Sweden, Belgium, Austria, and Japan. Thailand scored an average of 3.41, ranking 32nd globally and 2nd within the ASEAN region. The LPI assesses six core dimensions, including customs efficiency, infrastructure quality, international shipment competence, logistics service quality, tracking and tracing capabilities, and timeliness. Among these, Thailand performed strongly in timeliness (3.81) and tracking and tracing (3.47). However, customs procedures and infrastructure received the lowest scores, highlighting persistent vulnerabilities (Department of International Trade Promotion, 2023).

In 2023, Thailand's logistics performance was ranked 34th among 139 countries, with a score of 3.5 out of 5.0, positioning it as the third-best performer in ASEAN, after Singapore and Malaysia. The nation's infrastructure efficiency was ranked 25th worldwide, indicating a moderate level of global competitiveness alongside notable structural constraints, especially in domestic connectivity and rural service delivery. The decline in Thailand’s ranking reflects relative stagnation compared to improvements in other countries, diminishing its competitive advantage in the global logistics sector.

Table 1. Comparison of country rankings and LPI scores in 2016 and 2018

|

Country

|

2016

|

2018

|

|

LPI score

|

Rank

|

LPI score

|

Rank

|

|

Germany

|

4.23

|

1

|

4.20

|

1

|

|

Sweden

|

4.20

|

3

|

4.05

|

2

|

|

Belgium

|

4.11

|

6

|

4.04

|

3

|

|

Austria

|

4.10

|

7

|

4.03

|

4

|

|

Japan

|

3.97

|

12

|

4.03

|

5

|

|

Thailand

|

3.26

|

45

|

3.41

|

32

|

Source: World Bank (2018)

Logistics expenses are a crucial determinant of total supply chain costs, thereby exerting considerable influence over the competitiveness of both individual enterprises and the broader national economy. As delineated by Ballou (2004), these costs are generally classified into transportation, inventory maintenance, and administrative categories. Each category is instrumental in shaping the operational effectiveness and strategic performance of supply chains.

According to Christopher (2016), strategic reduction of logistics costs can substantially improve an organization's competitive stance, impacting both pricing and the ability to meet consumer needs rapidly. This is especially relevant in the ASEAN Economic Community, where member countries are increasingly competing on cost.

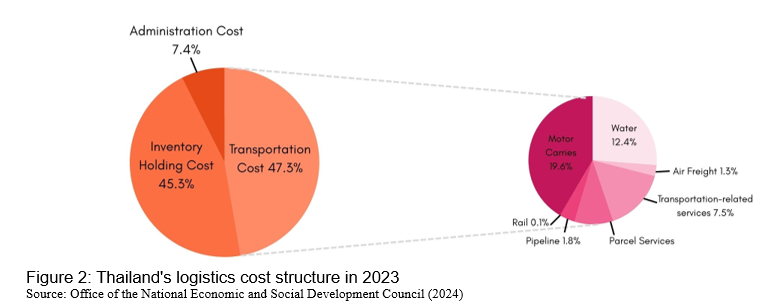

In 2023, the Office of the National Economic and Social Development Council reported that Thailand's total logistics expenditure was approximately US$78.10 billion, representing 14.1% of the nation's GDP (Office of the National Economic and Social Development Council, 2024). Transportation activities constituted the most significant component of this cost, accounting for US$36.92 billion, or 6.7% of GDP. This highlights Thailand’s considerable reliance on road transport and its associated economic implications. Inventory holding costs amounted to US$35.34 billion, equivalent to 6.4% of GDP, indicating potential areas for improvement in warehousing practices, inventory management strategies, and overall supply chain synchronization. Administrative costs, while comparatively lower, still totaled US$5.81 billion, or 1.0% of GDP, encompassing expenses related to logistics planning, coordination efforts, and adherence to regulatory standards. Collectively, these statistics emphasize the imperative for comprehensive enhancements in infrastructure, digitalization initiatives, and logistics policies to foster a cost-efficient and competitive agricultural logistics sector in Figure 2.

Logistics costs in Thailand have shown an upward trend, primarily driven by increased inventory levels due to the slowdown in export activities and rising interest rates, which have significantly impacted financial costs for businesses (Office of Transport and Traffic Policy and Planning, 2023). These developments reflect underlying vulnerabilities in the financial management of supply chain operations, particularly for small and medium-sized enterprises (SMEs) that rely heavily on working capital for inventory financing.

Moreover, the country remains highly dependent on road transport, which accounts for 78.31% of total domestic freight movement. In contrast, rail and water transport remain underutilized, despite their potential for cost-efficiency and sustainability. This over-reliance on road transport underscores the structural imbalance in Thailand’s logistics system and highlights a critical weakness contributing to elevated logistics costs and limited resilience in supply chain networks in Table 2.

To mitigate these challenges, a strategic shift toward multimodal transport infrastructure and investment in alternative freight channels is essential for reducing total logistics costs and enhancing overall national competitiveness.

Table 2: Domestic freight transportation modes structure (Percent of total freight volume)

|

Year

|

Road

|

Water

|

Rail

|

Air

|

|

2022

|

79.48

|

18.55

|

1.96

|

0.01

|

|

2023

|

78.31

|

19.47

|

2.21

|

0.01

|

Source: Office of the National Economic and Social Development Council (2024)

Thailand's agricultural logistics sector is still grappling with considerable infrastructural deficits, most notably in warehousing, cold storage, and pre-cooling technologies. The inadequacy in both the availability and allocation of these critical resources impedes the preservation of agricultural product quality, thereby augmenting the total logistics expenditures (Office of the Permanent Secretary, Ministry of Transport, 2023).

Pre-cooling systems, essential for rapidly decreasing the temperature of newly harvested agricultural products, are critical in maintaining produce quality and prolonging shelf life. Nevertheless, numerous areas, mainly rural and small-scale agricultural regions, lack adequate pre-cooling infrastructure. The Office of the National Economic and Social Development Council (2023) indicates that current logistics infrastructure cannot sustain effective distribution, as cold storage and temperature-controlled warehousing are predominantly located in urban centers or commercial provinces.

The uneven distribution of resources in Thailand's logistics infrastructure results in significant inventory holding and transportation costs. Thailand's inventory holding costs in 2023 reached US$35.34 billion, accounting for 6.4% of the GDP, a 7.4% increase from the previous year (Office of the National Economic and Social Development Council, 2023). This trend reflects upstream logistics system inefficiencies and highlights structural bottlenecks.

Ballou (2004) and Christopher (2016) highlight the critical role of efficient warehousing and cold chain systems in ensuring the global competitiveness of agricultural supply chains. Inadequate infrastructure can lead to product degradation, reduced export values, and increased spoilage risks, thereby impeding Thailand's agricultural trade potential.

Furthermore, the volume of road freight in Thailand experienced a decline from 460.3 million tons in 2022 to 428.4 million tons in 2023, reflecting a slowdown in both domestic economic activity and export demand. These trends underscore the imperative for strategic investments in agricultural logistics infrastructure, particularly given the sector's susceptibility to external financial shocks.

In terms of policy, forecasts suggest a reduction in the logistics costs-to-GDP ratio to 13.4–13.8% in 2024 (Office of Agricultural Economics, 2024), driven by economic recovery, growth in domestic consumption, and the optimization of infrastructure investments. Despite the continued presence of high costs, governmental efforts are aimed at promoting multimodal transport development, particularly shifting freight from road to rail.

Additionally, there are ongoing initiatives to establish interoperable data standards across logistics systems, which will provide a basis for Thailand’s transition to smart logistics. Nevertheless, in comparison to regional competitors, Thailand's logistics system remains limited. Ongoing challenges such as protracted infrastructure development, fluctuating logistics costs, and external factors like global oil prices, economic uncertainties, and pandemic-related disruptions continue to hinder the sector’s efficiency and long-term competitiveness.

Conceptual Underpinnings of Agricultural Logistics in Thailand

Agricultural logistics is integral to the management of the agricultural supply chain, involving the strategic planning, execution, and oversight of the movement of raw materials, products, and associated data to ensure efficient, transparent, and traceable storage, transportation, and delivery of agricultural goods to end consumers. The fundamental goal of agricultural logistics is to minimize costs, reduce post-harvest losses, maintain product quality, and ensure timely delivery, which is particularly critical for perishable goods (Johnson et al., 2015).

Agricultural logistics is an integral component of farming, encompassing activities such as seed procurement, cultivation, crop management, harvesting, and delivery to collection points, processing facilities, or cooperative organizations. Each stage incurs explicit and implicit logistical expenses. Effective agricultural logistics systems rely on robust infrastructure, advanced technology, and sound management practices to ensure seamless operations from production to market. Thailand's strategic location in Southeast Asia, with its shared borders and extensive coastlines, positions it as a key transit point for agricultural goods within ASEAN and beyond (Sundram, 2023).

Therefore, agricultural logistics is a pivotal factor in bolstering the competitive edge of both farmers and agribusinesses. This holds particularly true in modern agricultural markets, where efficiency, accuracy, and transparency are paramount for ensuring the seamless transit of products from production sites to consumers. Effective management of logistics activities exerts a direct influence on the competitiveness of agricultural products within both domestic and regional markets, where logistics costs, including transportation, warehousing, and administrative expenses, serve as key indicators of overall logistics performance.

According to the Thai Ministry of Agriculture and Cooperatives, logistics costs constitute a substantial proportion of agricultural product sales. Specifically, pineapple logistics costs average 10.41% of total sales, oil palm 8.89%, white rice 8.59%, and jasmine rice 6.90%. These percentages surpass international benchmarks, where developed nations typically aim for levels below 5% of GDP (World Bank, 2023). These elevated costs are indicative of inefficiencies, including superfluous transportation steps, unproductive labor practices, and a deficiency in technological support.

Table 3: Transport cost by product and mode (USD per ton-kilometer)

|

Product

|

Road (USD)

|

Rail (USD)

|

Water (USD)

|

|

Rice

|

0.05

|

0.03

|

0.02

|

|

Cassava

|

0.05

|

0.03

|

0.02

|

|

Sugar

|

0.05

|

0.03

|

0.02

|

|

Rubber

|

0.05

|

0.02

|

0.01

|

|

Soybean Oil

|

0.08

|

-

|

-

|

|

Fuel Oil

|

0.07

|

0.03

|

0.02

|

|

Plastic Pellets

|

0.07

|

-

|

-

|

|

Hot Rolled Steel

|

0.04

|

-

|

0.02

|

|

Construction Steel

|

0.05

|

-

|

0.02

|

|

Cement

|

0.04

|

0.03

|

0.02

|

|

Drinking Water

|

0.06

|

-

|

0.02

|

|

Consumer Goods

|

0.05

|

-

|

-

|

|

Average

|

0.05

|

0.03

|

0.02

|

Remark: According to World Bank/IMF data, the average exchange rate in 2008 was 1 USD = 33.36 THB (World Bank, 2009)

Source: Office of Transport and Traffic Policy and Planning (2009)

Beyond transportation, logistics costs for agricultural products in Thailand also extend to storage and sales-related activities. The Office of Transport and Traffic Policy and Planning (2009) emphasized that while road transport represents the highest direct cost, the overall burden on farmers and producers also arises from limited post-harvest storage capacity and reliance on intermediaries in marketing channels. These weaknesses increase spoilage, reduce efficiency, and add to final consumer prices. Thus, logistics costs are not confined to transport alone but are distributed across three interrelated sectors such as post-production storage, transportation, and sales indicating that comprehensive strategies are required to improve efficiency throughout the agricultural supply chain in Table 3.

Logistics performance is evaluated using perception and satisfaction indices, such as the Industrial Logistics Performance Index, which the Logistics Bureau developed under the Department of Primary Industries and Mines, Ministry of Industry. The Ministry of Agriculture and Cooperatives has recently conducted studies to assess agricultural logistics costs for rice, oil palm, and pineapple across 13 provinces. These studies employed surveys and data management systems to analyze logistics performance across three dimensions.

- Cost Dimension: Logistics costs, measured as a percentage of sales, encompass transport, warehousing, and management expenses. Pineapple exhibited the highest average logistics cost at 10.41%, followed by oil palm at 8.89%, white rice at 8.59%, and jasmine rice at 6.90%.

- Time Dimension: Transport and storage duration. Jasmine rice had an average delivery time of 1.2 days, white rice and oil palm 1 day, and pineapple the shortest at 0.7 days.

- Reliability Dimension: Product damage and return rates. Oil palm had a 100.00% delivery success rate with only 0.95% damage and 1.66% return rate. Jasmine rice had a 99.63% success rate, 5.00% damage, and 0.35% return. White rice had 98.28% delivery success, 3.19% damage, and 1.57% return. Pineapple had 98.26% delivery success, 2.52% damage, and 1.50% return.

Nonetheless, persistent challenges impede progress, notably farmers' restricted understanding of logistics, the geographical scattering of production, and insufficient infrastructure to achieve sustained cost efficiencies. Strategic investment in technology, product aggregation mechanisms, and collaborative networks is therefore essential to the advancement of agricultural logistics, facilitating Thailand's aspirations to establish itself as a prominent logistics hub within ASEAN.

IMPLEMENTATION

Alignment with National Strategic Plans

The development of Thailand’s agricultural logistics system is guided by the 20-Year National Strategy (2018–2037), which prioritizes enhancing national competitiveness through reduced logistics costs and improved transport efficiency in the agricultural sector. This overarching strategy has been operationalized through specific frameworks, such as the National Logistics Development Plan and the Agricultural Logistics Action Plan (2023–2027). These plans provide clearly defined strategic objectives and measurable indicators designed to drive long-term improvements in Thailand’s agricultural economy.

Development Planning for the 2023–2027 Agricultural Logistics Initiative

The 2023–2027 Agricultural Logistics Plan resulted from a collaborative effort involving the Office of Agricultural Economics, the Ministry of Agriculture and Cooperatives, representatives from both public and private sectors, and academic institutions. The planning methodology encompassed an analysis of actual logistical scenarios within the agricultural domain, the compilation of expert perspectives, an evaluation of sectoral requirements, and the formulation of a practically oriented action plan. The plan is dedicated to improving logistical efficacy and cost reduction, thereby facilitating access for farmers and entrepreneurs to superior logistics services, alongside the localized execution of the plan. This integrated strategy ensures alignment with national development goals and cultivates resilience within the agricultural sector.

Stakeholders and Participation Mechanism

A comprehensive stakeholder engagement strategy is integral to the plan, including farmers, community enterprises, cooperatives, logistics service providers, academics, and government agencies. It promotes public discussions, brainstorming forums, public hearings, and survey data collection, which inform the formulation of actionable strategies. It also fosters inter-agency collaboration to achieve sustainable logistics development.

Objectives, Indicators, and Key Activities

The Agricultural Logistics Plan for 2023–2027 is designed to achieve multiple objectives, including the reduction of logistics costs for agricultural products, enhancement of infrastructure efficiency, promotion of technological integration in logistics processes, and development of comprehensive warehouse and distribution networks. Key performance indicators encompass the ratio of logistics costs to agricultural GDP, average product delivery times, user satisfaction metrics, and the utilization rates of multimodal transport. Primary activities include the expansion of rail and water transport networks, enhancement of agricultural warehousing systems, promotion of smart agricultural practices, and integration of logistics data systems.

CURRENT PROGRESS OF AGRICULTURAL LOGISTICS

National and Regional Flagship Projects

The Thai government has undertaken several key national initiatives to improve agricultural logistics, including developing transportation corridors between the northern and central regions and establishing regional distribution centers. Strategically positioned agricultural warehouses in provinces such as Chiang Rai, Khon Kaen, and Songkhla, linked to rail and port networks, are intended to lower transportation costs. At the regional level, the ASEAN Smart Logistics Network aims to integrate agricultural logistics across CLMV countries by promoting collaborative infrastructure development, data exchange, and the expansion of agricultural exports among ASEAN member states.

Progress in Agricultural Logistics Infrastructure

From 2023 to 2027, considerable capital has been allocated to bolster infrastructure, specifically through enhancements to dual-track rail lines like the Chira-Khon Kaen and Khon Kaen-Nong Khai routes, with the intention of augmenting rail freight capacity. Additional improvements encompass upgrades to provincial road networks, expansion of Laem Chabang Port, enhancements to southern coastal ports, and streamlining of national warehousing infrastructure. Moreover, new agricultural logistics centers have been established in Phitsanulok and Khon Kaen to centralize agricultural commodities and facilitate their transit via rail and maritime channels, thereby fortifying both internal and external logistics capabilities.

Agri-Logistics Technology

Thailand's agricultural logistics sector is undergoing a digital transformation. Despite disparities in infrastructure and cost barriers, the increased adoption of digital technologies such as Internet of Things (IoT), AI, drones, and e-commerce platforms has the potential to enhance value-added efficiency significantly. The COVID-19 pandemic accelerated this shift as consumer preferences moved toward online channels, driving the growth of last-mile and door-to-door delivery services. Digital platforms like Freshket exemplify the potential for end-to-end integration across production, processing, and market access.

Regional Cooperation

Regional collaborative frameworks, including the Greater Mekong Subregion (GMS), CLMV, and ACMECS play a pivotal role in strengthening Thailand's logistics connectivity. These collaborations support the development of cross-border logistics hubs, the harmonization of agricultural standards, the implementation of electronic documentation, and the integration of data systems. Together, these initiatives help reduce customs processing times and lower overall logistics costs. These are operationalized through key agreements such as the GMS Cross-Border Transport Facilitation Agreement (GMS CBTA), which mandates expedited border procedures for perishable goods to minimize spoilage and economic loss. Furthermore, ASEAN-level instruments such as the ASEAN Framework Agreement on the Facilitation of Goods in Transit (AFAFGIT), the ASEAN Framework Agreement on the Facilitation of Inter-State Transport (AFAFIST), and the ASEAN Framework Agreement on Multimodal Transport (AFAMT) serve to harmonize regulatory procedures, promote multimodal transport interoperability, and reduce non-tariff barriers across member states. These protocols are supported by the ASEAN Transport Strategic Plan 2016 to 2025, aligning regional infrastructure development with sustainable economic objectives. Despite these advancements, continued harmonization, rigorous enforcement, and enhanced capacity building among member states are crucial for realizing a resilient and integrated ASEAN logistics ecosystem.

PROBLEMS AND CONCERNS

Thailand's journey towards becoming an ASEAN agricultural logistics hub faces persistent obstacles across five major dimensions.

Infrastructure and Cost Constraints

Despite ongoing infrastructure investments, rural transport remains underdeveloped. In 2023, 78.31% of agricultural freight was transported by road, which is more expensive than rail or water transport. Controlled-temperature logistics such as cold chains are costly and remain underdeveloped. Warehousing, cold-storage, and pre-cooling facilities are limited and unevenly distributed across the country. These constraints contribute to persistently high logistics costs, with inventory holding and transportation accounting for approximately 6.4% and 6.7% of GDP, respectively. Such inefficiencies continue to undermine the competitiveness of Thailand’s agricultural exports.

Digital Systems and Data Integration Limitations

Thailand faces challenges due to the lack of a comprehensive logistics information system that effectively connects diverse stakeholders, including smallholder farmers and exporters. The incompleteness of existing traceability systems elevates food safety risks and curtails opportunities for value addition. Furthermore, the restricted adoption of technologies such as the Internet of Things and Enterprise Resource Planning systems for optimizing order and supply chain management impedes the seamless integration and overall effectiveness of logistics operations at the farm level.

Workforce and Institutional Capacity Gaps

A significant portion of Thailand's agricultural workforce, comprising over 30 million individuals (representing approximately 46.4% of the population as of 2022), experiences skills deficits in logistics technologies and lacks a contemporary agribusiness orientation. Fragmentation among smallholder farmers and cooperatives exacerbates cost inefficiencies and compromises quality control. Moreover, institutional limitations in strategic capabilities, data accessibility, and effective governance impede sector advancement.

A significant portion of Thailand’s agricultural workforce, comprising more than 30 million individuals (46.4% of the population as of 2022), continues to face systemic challenges in logistics, technology, and organizational capacity. Fragmentation among smallholder farmers and cooperatives results in inefficiencies and compromises quality control, while limited access to finance and weak institutional support further constrain competitiveness. These gaps not only elevate logistics costs but also reduce the sector’s ability to respond to regional and global market demands.

A critical root cause of fragmentation is Thailand’s inheritance system, which requires farmland to be equally divided among heirs. This practice leads to progressively smaller farm sizes across generations, undermining economies of scale and creating structural inefficiencies in production and logistics (Benoit & Partners, 2025). In parallel, longstanding insecurity of land tenure and the inability to consolidate holdings hinder farmers’ access to credit, investment, and modern storage infrastructure (World Bank, 1985). The combined effect of fragmented landholdings and weak institutional mechanisms limits farmers’ bargaining power, reinforces dependence on intermediaries, and restricts opportunities to achieve consistent product quality.

Moreover, policy frameworks such as the Contract Farming Act have struggled to adequately protect smallholders, leaving them vulnerable to price volatility and unfavorable contractual arrangements. This weakens incentives for innovation and cooperation, exacerbating disparities between large agribusinesses and small-scale producers (Hall & Rambo, 2024). Addressing these institutional and workforce capacity gaps is essential for reducing overall logistics inefficiencies and for building the foundation of a more competitive agricultural sector.

Economic, Climate, and Trade Volatility

The agricultural sector in Thailand is becoming increasingly susceptible to rising average temperatures, erratic seasonal patterns, and more frequent natural disasters. These climatic shifts have a direct impact on food security and diminish the competitiveness of agricultural exports. Even slight temperature increases in tropical zones can substantially decrease crop yields. Moreover, the risks to food delivery and safety are exacerbated by droughts, pest infestations, and the proliferation of plant pathogens. Agriculture is both affected by and contributes to climate change, accounting for about 17% to 20% of Thailand's total greenhouse gas emissions, second only to the energy sector. Additionally, the country faces the challenges of increased competition from nations with lower production costs, stringent non-tariff trade barriers, and evolving phytosanitary standards in export markets (Sutthachaidee et al., 2020).

Policy, Standards, and Regulatory Gaps

The enforcement of sanitary and phytosanitary standards, along with logistics regulations, continues to be inconsistently applied. This results in duplicated expenses and challenges for farmers and exporters because of the varying application of these standards. Deficient institutional policy coordination hinders comprehensive oversight concerning warehousing standards and export logistics prerequisites. The prevailing laws and regulations related to cross-border trade, along with international transportation rules, are perceived as non-competitive, necessitating substantial reforms to promote greater competitiveness (Suvittawat, 2014).

CONCLUSION AND POLICY IMPLICATION

An Overview of the Current Challenges

Thailand has demonstrated notable advancements in the development of its agricultural logistics sector through investments in transportation infrastructure, warehouse systems, cold storage facilities, and cold chain technologies. These initiatives have collectively contributed to the reduction of post-harvest losses and the enhancement of overall supply chain efficiency. Nevertheless, several critical challenges persist, including elevated logistics costs, the absence of integrated data systems, deficits in logistics knowledge and skills among farmers, and external disruptions that adversely affect transportation networks and agricultural markets.

Thailand's advancement in agricultural logistics is reflected in its strategic planning, infrastructure investments, and the integration of digital technologies into transportation and warehousing systems. However, critical obstacles persist, including disproportionately high logistics expenses, uneven infrastructure distribution, a deficiency of integrated data systems, and a scarcity of proficient labor within the agricultural sector.

Policy Direction: Infrastructure, Technology, and Farmers’ Engagement

Policy initiatives should prioritize the enhancement of infrastructure to establish robust connections between agricultural production zones and market outlets. Furthermore, it is crucial to encourage the adoption of advanced logistics technologies, including IoT, Big Data, Blockchain, and ERP systems, to foster enhanced transparency, traceability, and cost-effectiveness throughout the agricultural supply chain. Concurrently, investing in human capital development is of paramount importance through the implementation of training programs designed to augment farmers' expertise in agricultural logistics and supply chain management. Additional emphasis should be placed on expanding climate-controlled warehousing capabilities, refining traceability systems from the point of origin to the final destination, and empowering smallholder farmers to engage in contemporary and efficient supply chain frameworks actively.

To elevate Thailand’s agricultural logistics system to the level of a regional hub, it is essential to move beyond incremental improvements and address the structural barriers that continue to constrain efficiency. A central challenge lies in land fragmentation, which limits economies of scale and weakens long-term investment incentives. A first priority should be the acceleration of a systematic land titling program to ensure that farmers hold secure and transferable rights. Strengthened land ownership will provide the legal certainty required to unlock access to formal credit, reduce reliance on informal lending, and encourage sustainable investments in land improvement and technology adoption.

At the same time, the development of a dynamic and secure land rental market is necessary to decouple farm operation from ownership. By modernizing tenancy regulations and creating a transparent land-matching platform, entrepreneurial farmers could consolidate operational control over larger, more viable plots without requiring full ownership. Such a system would lower transaction barriers, enhance mobility of agricultural resources, and enable the scale of operations needed for competitive production.

A complementary step is the reform of inheritance practices that perpetuate land subdivision. Instead of physical division of farmland, policy should promote co-ownership structures such as family corporations or partnerships that allow heirs to retain joint stakes while preserving the integrity of agricultural units. Financial incentives, including reduced inheritance taxes and low-interest credit facilities would further encourage heirs to maintain land as productive assets rather than fragmenting it into uneconomical parcels.

In conclusion, these reforms would create an enabling environment for larger, more efficient production units to emerge, supported by stronger investment incentives and modern logistics infrastructure. By tackling the underlying structural causes of inefficiency, Thailand can build an agricultural logistics system that is not only regionally competitive but also resilient, inclusive, and capable of supporting long-term national development goals.

Strategic Proposals: Integrations of Policy, Research, and Private Sector

To effectively integrate logistics, agricultural, and trade policies, governmental intervention is crucial across various ministries. This necessitates collaboration with academic research centers, such as the Office of Agricultural Economics and the Thailand Development Research Institute, to ensure evidence-based decision-making that is in accordance with international trends. Aligning national and local strategies with research findings is essential to addressing tangible production challenges. Furthermore, cooperation between private logistics providers and agricultural logistics researchers will stimulate innovation and market-responsive services. Strategic policy implementation should focus on establishing a centralized logistics data hub, defining national logistics standards, and developing integrated systems to enhance the global competitiveness of Thai agricultural products. A key component of Thailand 4.0 involves applying scientific knowledge, technology, and innovation to improve the value chain (Kaewyongphang, 2021). The adoption and acceptance of technology by Thai farmers also provide opportunities to incorporate technology in their farming and agricultural processes to produce better crops and high-quality food (Chaveesuk et al., 2020; Kaewyongphang, 2021).

Future Research Directions

Future research endeavors should prioritize cost-benefit analyses of logistics technologies like cold chain and pre-cooling systems, especially for high-value or perishable agricultural commodities. Developing economic logistics models tailored to specific agricultural product clusters, alongside implementing demand-supply matching systems, is crucial for optimizing supply chain performance. Further research areas encompass spatial efficiency assessments of logistics infrastructure, economic evaluations of technology adoption in logistics, and exploring market mechanisms for niche agricultural products reliant on advanced logistics systems. Moreover, cross-border collaboration frameworks, such as GMS, CLMV, and ACMECS, warrant study to establish resilient and integrated regional logistics networks. In essence, these research areas will serve to inform policies, advance logistics practices, and solidify Thailand's position as a prominent player in the ASEAN regional agricultural hub, promoting the long-term viability of its agricultural sector.

REFERENCES

Ballou, R. H. (2004). Business logistics/supply chain management (5th ed.). Pearson Education.

Benoit & Partners. (2025, September 11). Understanding inheritance rules in Thailand: A complete guide. Retrieved September 11, 2025, from https://benoit-partners.com/inheritance-rules-thailand/

Chaveesuk, S., Chaiyasoonthorn, W., & Khalid, B. (2020). Understanding the Model of User Adoption and Acceptance of Technology by Thai Farmers. https://doi.org/10.1145/3396743.3396781

Christopher, M. (2016). Logistics & supply chain management (5th ed.). Pearson UK.

Department of International Trade Promotion. (2023). Logistics industry in Thailand. Ministry of Commerce. Retrieved from https://www.ditp.go.th/wp-content/uploads/2023/11/12_Logistics-Industry-in-Thailand.pdf

Hall, D., & Rambo, A. T. (2024). Thailand's Contract Farming Act at a crossroads: Impacts, shortfalls, and the need to better protect smallholders. Journal of Contemporary Asia, 54(4), 623–641. https://doi.org/10.1080/14672715.2024.2365872

Ilyas, S., Hu, Z., & Wiwattanakornwong, K. (2020). Unleashing the role of top management and government support in green supply chain management and sustainable development goals. Environmental Science and Pollution Research, 27(8), 8210–8223. https://doi.org/10.1007/s11356-019-07268-3

Johnson, P. N., Nketia, S., & Quaye, W. (2015). Appraisal of Logistics Management Issues in the Agro-Food Industry Sector in Ghana. Journal of Agricultural Science, 7(3). https://doi.org/10.5539/jas.v7n3p164

Kaewyongphang, M. M. P. (2021). The Environment and Guidelines of Administration to Develop Innovators Among Secondary Science Teachers at Saint Gabriel’s Foundation, Thailand. Psychology and Education Journal, 58(1), 1738. https://doi.org/10.17762/pae.v58i1.976

Mahidol University, & Department of Land Transport. (2022). GMS cross-border transport facilitation analysis. Department of Land Transport.

Mungwatana, A., & Team. (2022). Enhancing multimodal transport efficiency in Thailand to support ASEAN Economic Community integration. National Science and Technology Development Agency (NSTDA).

Namboonruang, W., Amdee, N., Suphadon, N., & Krisonsri, B. (2018). Economic-engineering design for logistics infrastructure routing. MATEC Web of Conferences, 207, 1003. https://doi.org/10.1051/matecconf/201820701003

National Economic and Social Development Council. (2024). Thailand’s logistics cost structure report 2023. NESDC.

Nguyen, L. T. (2020). ASEAN logistics integration: Challenges and opportunities. ASEAN Studies Center.

Office of Agricultural Economics. (2023). Agricultural logistics action plan 2023–2027. Ministry of Agriculture and Cooperatives.

Office of Agricultural Economics. (2024, December 19). Thailand’s agricultural GDP expected to shrink by 1.1% in 2024 before growing 1.8–2.8%; NESDC urged to adjust calculation ratio. InfoQuest. https://www.infoquest.co.th/2024/455013

Office of the National Economic and Social Development Council. (2023). Logistics cost trends and inventory holding in Thailand 2023–2024. Retrieved from https://www.nesdc.go.th

Office of the Permanent Secretary, Ministry of Transport. (2023). Thailand logistics industry report 2023. Retrieved from https://www.ditp.go.th/wp-content/uploads/2023/11/12_Logistics-Industry-in-Thailand.pdf

Office of Transport and Traffic Policy and Planning. (2009). Analysis of the cost structure of transport and logistics systems. Retrieved from https://www.otp.go.th/edureport/view?id=141Pakawachkrilers, K. (2022, September 5). Retail e-commerce to hit B4tn in 2025. Bangkok Post. https://www.bangkokpost.com/business/general/2377256/retail-e-commerce-to-hit-b4tn-in-2025

Ramingwong, S., Chaiprasit, S., & Kongsamut, P. (2024). Digital logistics for Thailand's agricultural competitiveness. Journal of Supply Chain and Logistics, 18(1), 22–41.

Sundram, P. (2023). Food security in ASEAN: progress, challenges and future. Frontiers in Sustainable Food Systems, 7. https://doi.org/10.3389/fsufs.2023.1260619

Sutthachaidee, W., Kuosuwan, B., & Kiranantawat, B. (2020). Pomelo export logistics process: modern factors of efficiency (the case of wiang kaen district, chiang rai province, Thailand). E3S Web of Conferences, 164, 3006. https://doi.org/10.1051/e3sconf/202016403006

Suvittawat, A. (2014). Competitiveness of Thai Entrepreneurs: Key Success Factors of Logistics Business Operations. Information Management and Business Review, 6(6), 280. https://doi.org/10.22610/imbr.v6i6.1126

Thailand Development Research Institute. (2023). Logistics development for agricultural export: Policy recommendations. Thailand Development Research Institute.

Trade Policy and Strategy Office. (2024). Development of logistics for agricultural trade. Retrieved from https://tpso.go.th/document/2406-0000000025

Trade Policy and Strategy Office. (2025). Agricultural trade report 2024. Ministry of Commerce, Thailand.

Trade Policy and Strategy Office. (2025, February 4). Commerce unveils record-breaking statistics: Thai agricultural exports in 2024 [Press release]. Trade Policy and Strategy Office, Ministry of Commerce. https://tpso.go.th/news/2502-0000000023

World Bank. (1985). Land ownership security and land values in rural Thailand (World Bank Report No. IDP 52). World Bank. Retrieved from https://documents1.worldbank.org/curated/en/389431468764960613/pdf/multi0page.pdf

World Bank. (2009). World Development Indicators: Exchange rates and prices. The World Bank. https://databank.worldbank.org/source/world-development-indicators

World Bank. (2018). Connecting to compete 2018: Trade logistics in the global economy – The Logistics Performance Index and its indicators. Washington, DC: World Bank Group.

World Bank. (2022). Enabling the business of agriculture 2022. World Bank Group.

Development of Thailand’s Agricultural Logistics Systems Toward ASEAN Regional Hub: Challenges and Policy Implications

ABSTRACT

This study investigates the evolving landscape and systemic challenges within Thailand's agricultural logistics, with a focus on impediments to efficiency and competitiveness. These include transportation inefficiencies, infrastructure deficits, and fragmented data management across various governmental bodies. The research assesses Thailand's potential to serve as a regional logistics center in ASEAN, aligning with the National Action Plan for Agricultural Logistics Development. The results indicate that despite advancements in infrastructure, significant challenges remain. These encompass elevated logistics expenditures, disjointed data infrastructures, limited logistical expertise among agricultural producers, and external disruptions to agricultural supply networks. Policy recommendations underscore the necessity of infrastructure investments in agriculturally significant regions, the adoption of digital logistics solutions, and the empowerment of farmers through knowledge enhancement. A strategic framework is proposed to synergize national and local strategies with academic research and private-sector involvement, to stimulate innovation, market adaptability, and competitive advantages.

Keywords: Thailand agricultural logistics, infrastructure development, ASEAN regional hub, logistics policy

INTRODUCTION

Thailand's ambition to establish itself as a key ASEAN regional hub is contingent on the advancement and effectiveness of its agricultural logistics system. This requires a comprehensive analysis of the existing infrastructure, operational challenges, and technological integration within the country's agricultural supply chains. As ASEAN continues to pursue regional integration, the need for a resilient logistics sector to support the exchange of goods is becoming increasingly important, with the varying levels of development among Southeast Asian cities presenting both challenges and opportunities (Nguyen, 2020).

To effectively leverage regional integration, Thailand must strategically invest in its logistics infrastructure and cultivate a comprehensive understanding of trade routes and economic development within its agricultural logistics system. Agriculture remains a strategic sector in Thailand’s economy, providing a livelihood for a substantial portion of the population and serving as a major source of export revenue. In 2024, the export value of Thailand’s agricultural and agro-industrial products exceeded US$52 billion, constituting a significant percentage of the country’s total exports (Trade Policy and Strategy Office, 2025).

Thailand's leading agricultural exports demonstrate its rich natural resources and established agro-industrial capabilities. Likewise, processed agricultural products, including canned seafood, pet food, and refined sugar, reinforce the country's standing in global food supply networks.

However, despite robust global demand, the efficiency and resilience of Thailand’s agricultural export logistics system present ongoing challenges. Given that a significant portion of these exports is perishable, a highly coordinated cold chain, advanced warehousing, and effective multimodal transport systems are essential. Nevertheless, the country’s logistics remain heavily dependent on road transport, which accounted for 78.31% of total agricultural freight in 2023, while rail and water transport accounted for only 2.21% and 19.47%, respectively (National Economic and Social Development Council, 2024). This reliance on road transport increases logistics costs, limits scalability, and elevates the risk of delays and spoilage.

The COVID-19 pandemic exposed critical weaknesses within Thailand's cross-border agricultural logistics framework, most notably when rigorous health protocols precipitated delays at border checkpoints. These disruptions disproportionately affected the timely transit of perishable commodities, particularly at the Chinese border under the “Zero-COVID” strategy, resulting in elevated spoilage rates for fruit exports during peak harvesting periods and precipitating considerable financial detriments for both exporters and agricultural producers (Department of International Trade Promotion, 2023).

Furthermore, Thailand’s agricultural logistics infrastructure is characterized by fragmentation and a heterogeneous distribution of refrigerated storage and warehousing capabilities, which exacerbates post-harvest wastage (Office of Agricultural Economics, 2023). The assimilation of advanced information technology, automated systems, and comprehensive traceability mechanisms remains preliminary, especially amongst small and medium-sized enterprises operating within Thailand’s agri-business sector. Consequently, the fortification of logistics capabilities is paramount to sustaining export competitiveness, conforming to stringent international sanitary and phytosanitary regulations, and minimizing post-harvest losses.

Thailand stands to gain from multilateral initiatives like the GMS Cross-Border Transport Facilitation Agreement and ASEAN transport agreements by improving its connectivity, harmonizing transport regulations, and promoting multimodal logistics across borders. Simultaneously, the rapid expansion of Thailand's digital commerce, with e-commerce projections exceeding US$118.56 billion, driven by shifting consumer behaviors and the rise of meta-commerce (Pakawachkrilers, 2022), positions the nation as a prominent player in ASEAN B2C e-commerce. This encourages the adoption of digital channels among businesses, particularly small and medium-sized enterprises, thereby enhancing supply chain efficiency and fostering new economic opportunities for agricultural producers and community enterprises (Ilyas, Hu, & Wiwattanakornwong, 2020; Trade Policy and Strategy Office, 2025).

Ultimately, Thailand’s continued success in agricultural exports depends on its ability to enhance logistics infrastructure, invest in cold chain networks, develop human capital, and leverage regional cooperation to overcome structural inefficiencies. The findings of this study contribute to these national objectives by offering evidence-based insights to inform strategic planning and infrastructure investment, fostering a more competitive, sustainable, and integrated agricultural logistics system.

ASEAN Context and Thailand’s Strategic Potential

The ASEAN region's significance in global agricultural trade and production is underpinned by its rich endowment of natural resources, amenable climatic conditions, and abundant labor supply, fostering the cultivation of diverse agricultural commodities. Thailand, under its founding membership in ASEAN, holds strategic advantages derived from its geographic location and well-developed multimodal transport infrastructure, enabling seamless connectivity with adjacent nations via terrestrial, fluvial, pipeline, and aerial routes. These synergistic geographical and infrastructural assets position Thailand favorably as a potential nucleus for agricultural logistics within the Southeast Asian region.

The Economic Significance of Agricultural Logistics

Agricultural logistics is a vital mechanism that enhances the competitiveness of agricultural products by managing all stages of the supply chain, including storage, transportation, processing, and distribution to end consumers. An efficient logistics system contributes to reducing production costs, preserving product quality, increasing value, and strengthening market confidence both domestically and internationally. According to the Office of Agricultural Economics (2024), Thailand has a total agricultural area of 23.64 million hectares, which accounts for 46.7% of the country’s total land area. The agricultural sector supports over 30 million people, with approximately 19.72 million engaged in agricultural labor and around 7.9 million farming households. Furthermore, data from the Trade Policy and Strategy Office (2025) indicates that Thailand’s total export value in 2024 reached US$300.53 billion, reflecting a 5.4% increase from the previous year. Exports of agricultural and agro-industrial products represented 17.36% of the total, amounting to US$52.19 billion, which is a 6.0% growth compared to 2023. These numbers highlight the strategic significance of the agricultural sector in Thailand’s economy, especially amid the challenges posed by geopolitical uncertainty, natural disasters, and increasing global competition.

Vision: Thailand as ASEAN’s Agricultural Logistics Hub

The Ministry of Agriculture and Cooperatives of Thailand has established an Action Plan for the Development of Agricultural Logistics Systems (2023–2027), with the strategic vision of positioning Thailand as a central agricultural logistics hub within ASEAN. This initiative is designed to cultivate extensive logistics infrastructure, build the capabilities of agricultural producers and agribusinesses, and promote the integration of advanced technologies and innovations. The primary objectives include decreasing logistics expenses and improving operational effectiveness throughout the agricultural supply chain, from production sites to consumers. Furthermore, the plan underscores the importance of cultivating human capital, reinforcing institutional proficiency in the agricultural domain, and fostering a competitive business environment for agriculture at both regional and global scales.

Objective of the Article

This study provides an in-depth examination of Thailand's agricultural logistics system, highlighting key structural challenges that undermine its efficiency and competitiveness. These challenges encompass transport inefficiencies, inadequacies in specialized infrastructure, and a lack of integrated data systems across relevant institutions. The feasibility of positioning Thailand as a central agricultural logistics hub within ASEAN is assessed, aligning with the national Action Plan for Agricultural Logistics Development (2023–2027), to inform policy development and strategic progress at the national level.

THEORY AND EMPIRICAL PERSPECTIVES

Logistics Cost Structure and Logistics Performance Index in Thailand

Thailand has consistently worked to improve its logistics system's competitiveness at both regional and global levels. The Logistics Performance Index, created by the World Bank, is a crucial macro-level indicator for assessing this advancement. This index includes elements such as infrastructure quality, tracking capabilities, timeliness, and the effectiveness of international shipments. Moreover, the composition of logistics costs as a proportion of GDP offers an empirical overview of the strengths, weaknesses, and patterns in the nation's logistics system.

Thailand’s logistics performance in Table 1 is captured in the LPI Global Rankings, where in 2018, the top five performing countries were Germany, Sweden, Belgium, Austria, and Japan. Thailand scored an average of 3.41, ranking 32nd globally and 2nd within the ASEAN region. The LPI assesses six core dimensions, including customs efficiency, infrastructure quality, international shipment competence, logistics service quality, tracking and tracing capabilities, and timeliness. Among these, Thailand performed strongly in timeliness (3.81) and tracking and tracing (3.47). However, customs procedures and infrastructure received the lowest scores, highlighting persistent vulnerabilities (Department of International Trade Promotion, 2023).

In 2023, Thailand's logistics performance was ranked 34th among 139 countries, with a score of 3.5 out of 5.0, positioning it as the third-best performer in ASEAN, after Singapore and Malaysia. The nation's infrastructure efficiency was ranked 25th worldwide, indicating a moderate level of global competitiveness alongside notable structural constraints, especially in domestic connectivity and rural service delivery. The decline in Thailand’s ranking reflects relative stagnation compared to improvements in other countries, diminishing its competitive advantage in the global logistics sector.

Table 1. Comparison of country rankings and LPI scores in 2016 and 2018

Country

2016

2018

LPI score

Rank

LPI score

Rank

Germany

4.23

1

4.20

1

Sweden

4.20

3

4.05

2

Belgium

4.11

6

4.04

3

Austria

4.10

7

4.03

4

Japan

3.97

12

4.03

5

Thailand

3.26

45

3.41

32

Source: World Bank (2018)

Logistics expenses are a crucial determinant of total supply chain costs, thereby exerting considerable influence over the competitiveness of both individual enterprises and the broader national economy. As delineated by Ballou (2004), these costs are generally classified into transportation, inventory maintenance, and administrative categories. Each category is instrumental in shaping the operational effectiveness and strategic performance of supply chains.

According to Christopher (2016), strategic reduction of logistics costs can substantially improve an organization's competitive stance, impacting both pricing and the ability to meet consumer needs rapidly. This is especially relevant in the ASEAN Economic Community, where member countries are increasingly competing on cost.

In 2023, the Office of the National Economic and Social Development Council reported that Thailand's total logistics expenditure was approximately US$78.10 billion, representing 14.1% of the nation's GDP (Office of the National Economic and Social Development Council, 2024). Transportation activities constituted the most significant component of this cost, accounting for US$36.92 billion, or 6.7% of GDP. This highlights Thailand’s considerable reliance on road transport and its associated economic implications. Inventory holding costs amounted to US$35.34 billion, equivalent to 6.4% of GDP, indicating potential areas for improvement in warehousing practices, inventory management strategies, and overall supply chain synchronization. Administrative costs, while comparatively lower, still totaled US$5.81 billion, or 1.0% of GDP, encompassing expenses related to logistics planning, coordination efforts, and adherence to regulatory standards. Collectively, these statistics emphasize the imperative for comprehensive enhancements in infrastructure, digitalization initiatives, and logistics policies to foster a cost-efficient and competitive agricultural logistics sector in Figure 2.

Logistics costs in Thailand have shown an upward trend, primarily driven by increased inventory levels due to the slowdown in export activities and rising interest rates, which have significantly impacted financial costs for businesses (Office of Transport and Traffic Policy and Planning, 2023). These developments reflect underlying vulnerabilities in the financial management of supply chain operations, particularly for small and medium-sized enterprises (SMEs) that rely heavily on working capital for inventory financing.

Moreover, the country remains highly dependent on road transport, which accounts for 78.31% of total domestic freight movement. In contrast, rail and water transport remain underutilized, despite their potential for cost-efficiency and sustainability. This over-reliance on road transport underscores the structural imbalance in Thailand’s logistics system and highlights a critical weakness contributing to elevated logistics costs and limited resilience in supply chain networks in Table 2.

To mitigate these challenges, a strategic shift toward multimodal transport infrastructure and investment in alternative freight channels is essential for reducing total logistics costs and enhancing overall national competitiveness.

Table 2: Domestic freight transportation modes structure (Percent of total freight volume)

Year

Road

Water

Rail

Air

2022

79.48

18.55

1.96

0.01

2023

78.31

19.47

2.21

0.01

Source: Office of the National Economic and Social Development Council (2024)

Thailand's agricultural logistics sector is still grappling with considerable infrastructural deficits, most notably in warehousing, cold storage, and pre-cooling technologies. The inadequacy in both the availability and allocation of these critical resources impedes the preservation of agricultural product quality, thereby augmenting the total logistics expenditures (Office of the Permanent Secretary, Ministry of Transport, 2023).

Pre-cooling systems, essential for rapidly decreasing the temperature of newly harvested agricultural products, are critical in maintaining produce quality and prolonging shelf life. Nevertheless, numerous areas, mainly rural and small-scale agricultural regions, lack adequate pre-cooling infrastructure. The Office of the National Economic and Social Development Council (2023) indicates that current logistics infrastructure cannot sustain effective distribution, as cold storage and temperature-controlled warehousing are predominantly located in urban centers or commercial provinces.

The uneven distribution of resources in Thailand's logistics infrastructure results in significant inventory holding and transportation costs. Thailand's inventory holding costs in 2023 reached US$35.34 billion, accounting for 6.4% of the GDP, a 7.4% increase from the previous year (Office of the National Economic and Social Development Council, 2023). This trend reflects upstream logistics system inefficiencies and highlights structural bottlenecks.

Ballou (2004) and Christopher (2016) highlight the critical role of efficient warehousing and cold chain systems in ensuring the global competitiveness of agricultural supply chains. Inadequate infrastructure can lead to product degradation, reduced export values, and increased spoilage risks, thereby impeding Thailand's agricultural trade potential.

Furthermore, the volume of road freight in Thailand experienced a decline from 460.3 million tons in 2022 to 428.4 million tons in 2023, reflecting a slowdown in both domestic economic activity and export demand. These trends underscore the imperative for strategic investments in agricultural logistics infrastructure, particularly given the sector's susceptibility to external financial shocks.

In terms of policy, forecasts suggest a reduction in the logistics costs-to-GDP ratio to 13.4–13.8% in 2024 (Office of Agricultural Economics, 2024), driven by economic recovery, growth in domestic consumption, and the optimization of infrastructure investments. Despite the continued presence of high costs, governmental efforts are aimed at promoting multimodal transport development, particularly shifting freight from road to rail.

Additionally, there are ongoing initiatives to establish interoperable data standards across logistics systems, which will provide a basis for Thailand’s transition to smart logistics. Nevertheless, in comparison to regional competitors, Thailand's logistics system remains limited. Ongoing challenges such as protracted infrastructure development, fluctuating logistics costs, and external factors like global oil prices, economic uncertainties, and pandemic-related disruptions continue to hinder the sector’s efficiency and long-term competitiveness.

Conceptual Underpinnings of Agricultural Logistics in Thailand

Agricultural logistics is integral to the management of the agricultural supply chain, involving the strategic planning, execution, and oversight of the movement of raw materials, products, and associated data to ensure efficient, transparent, and traceable storage, transportation, and delivery of agricultural goods to end consumers. The fundamental goal of agricultural logistics is to minimize costs, reduce post-harvest losses, maintain product quality, and ensure timely delivery, which is particularly critical for perishable goods (Johnson et al., 2015).

Agricultural logistics is an integral component of farming, encompassing activities such as seed procurement, cultivation, crop management, harvesting, and delivery to collection points, processing facilities, or cooperative organizations. Each stage incurs explicit and implicit logistical expenses. Effective agricultural logistics systems rely on robust infrastructure, advanced technology, and sound management practices to ensure seamless operations from production to market. Thailand's strategic location in Southeast Asia, with its shared borders and extensive coastlines, positions it as a key transit point for agricultural goods within ASEAN and beyond (Sundram, 2023).

Therefore, agricultural logistics is a pivotal factor in bolstering the competitive edge of both farmers and agribusinesses. This holds particularly true in modern agricultural markets, where efficiency, accuracy, and transparency are paramount for ensuring the seamless transit of products from production sites to consumers. Effective management of logistics activities exerts a direct influence on the competitiveness of agricultural products within both domestic and regional markets, where logistics costs, including transportation, warehousing, and administrative expenses, serve as key indicators of overall logistics performance.

According to the Thai Ministry of Agriculture and Cooperatives, logistics costs constitute a substantial proportion of agricultural product sales. Specifically, pineapple logistics costs average 10.41% of total sales, oil palm 8.89%, white rice 8.59%, and jasmine rice 6.90%. These percentages surpass international benchmarks, where developed nations typically aim for levels below 5% of GDP (World Bank, 2023). These elevated costs are indicative of inefficiencies, including superfluous transportation steps, unproductive labor practices, and a deficiency in technological support.

Table 3: Transport cost by product and mode (USD per ton-kilometer)

Product

Road (USD)

Rail (USD)

Water (USD)

Rice

0.05

0.03

0.02

Cassava

0.05

0.03

0.02

Sugar

0.05

0.03

0.02

Rubber

0.05

0.02

0.01

Soybean Oil

0.08

-

-

Fuel Oil

0.07

0.03

0.02

Plastic Pellets

0.07

-

-

Hot Rolled Steel

0.04

-

0.02

Construction Steel

0.05

-

0.02

Cement

0.04

0.03

0.02

Drinking Water

0.06

-

0.02

Consumer Goods

0.05

-

-

Average

0.05

0.03

0.02

Remark: According to World Bank/IMF data, the average exchange rate in 2008 was 1 USD = 33.36 THB (World Bank, 2009)

Source: Office of Transport and Traffic Policy and Planning (2009)

Beyond transportation, logistics costs for agricultural products in Thailand also extend to storage and sales-related activities. The Office of Transport and Traffic Policy and Planning (2009) emphasized that while road transport represents the highest direct cost, the overall burden on farmers and producers also arises from limited post-harvest storage capacity and reliance on intermediaries in marketing channels. These weaknesses increase spoilage, reduce efficiency, and add to final consumer prices. Thus, logistics costs are not confined to transport alone but are distributed across three interrelated sectors such as post-production storage, transportation, and sales indicating that comprehensive strategies are required to improve efficiency throughout the agricultural supply chain in Table 3.

Logistics performance is evaluated using perception and satisfaction indices, such as the Industrial Logistics Performance Index, which the Logistics Bureau developed under the Department of Primary Industries and Mines, Ministry of Industry. The Ministry of Agriculture and Cooperatives has recently conducted studies to assess agricultural logistics costs for rice, oil palm, and pineapple across 13 provinces. These studies employed surveys and data management systems to analyze logistics performance across three dimensions.

Nonetheless, persistent challenges impede progress, notably farmers' restricted understanding of logistics, the geographical scattering of production, and insufficient infrastructure to achieve sustained cost efficiencies. Strategic investment in technology, product aggregation mechanisms, and collaborative networks is therefore essential to the advancement of agricultural logistics, facilitating Thailand's aspirations to establish itself as a prominent logistics hub within ASEAN.

IMPLEMENTATION

Alignment with National Strategic Plans

The development of Thailand’s agricultural logistics system is guided by the 20-Year National Strategy (2018–2037), which prioritizes enhancing national competitiveness through reduced logistics costs and improved transport efficiency in the agricultural sector. This overarching strategy has been operationalized through specific frameworks, such as the National Logistics Development Plan and the Agricultural Logistics Action Plan (2023–2027). These plans provide clearly defined strategic objectives and measurable indicators designed to drive long-term improvements in Thailand’s agricultural economy.

Development Planning for the 2023–2027 Agricultural Logistics Initiative

The 2023–2027 Agricultural Logistics Plan resulted from a collaborative effort involving the Office of Agricultural Economics, the Ministry of Agriculture and Cooperatives, representatives from both public and private sectors, and academic institutions. The planning methodology encompassed an analysis of actual logistical scenarios within the agricultural domain, the compilation of expert perspectives, an evaluation of sectoral requirements, and the formulation of a practically oriented action plan. The plan is dedicated to improving logistical efficacy and cost reduction, thereby facilitating access for farmers and entrepreneurs to superior logistics services, alongside the localized execution of the plan. This integrated strategy ensures alignment with national development goals and cultivates resilience within the agricultural sector.

Stakeholders and Participation Mechanism

A comprehensive stakeholder engagement strategy is integral to the plan, including farmers, community enterprises, cooperatives, logistics service providers, academics, and government agencies. It promotes public discussions, brainstorming forums, public hearings, and survey data collection, which inform the formulation of actionable strategies. It also fosters inter-agency collaboration to achieve sustainable logistics development.

Objectives, Indicators, and Key Activities