INTRODUCTION

With the increased demand for meat of bovine animals (beef and buffalo meat), Vietnamese producers need to be more strategic in their plans in order to be proficient to supply local demand. They also need to compete with foreign imports. Quantity of bovine meat per capita in Vietnam increased yearly by level of consumption. The Vietnam livestock industry has many weaknesses from production to marketing.

According to Chartsbin, Vietnam is on the world’s top 15 in terms of quantity of meat production as well as consumption. It annually produces 3.6 million tons and consumes 4.1 million tons of meat (every year, Vietnam must import meat to meet local demand). In terms of per capita consumption, Vietnam is at a low - average level of about 50 kg/person/year. However, compared to other countries in Southeast Asia, Vietnam is the second largest country with per capita meat consumption, followed by Malaysia (52.3 kg) and significantly higher than Philippines (33.6 kg), Thailand (25.8 kg) and Indonesia (11.6 kg).

Among the variety of meat types, pork, beef and poultry are considered important meats. Currently, Thailand has the potential for breeding and bovine feedlotting and processing. The country has the opportunities to export more bovine meat to the Vietnam market.

Livestock Products Overview and Demand of Bovine Meat in Vietnam

Vietnam livestock products overview

Livestock is an important economic sector of Vietnam, which creates supply of foodstuff for the Vietnamese people. The industry helps farmers to increase their income. For over a decade, the livestock industry has gradually shifted from small-scale production to bigger scale farms, with focus on ensuring food safety and minimizing environmental pollution.

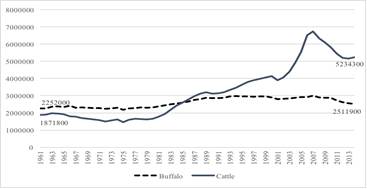

However, in recent years, the livestock sector in Vietnam has met many difficulties such as rising input costs (mainly as animal feed), output price instability, diseases, excessive use of prohibited substances and antibiotics, competition from imported meat products, and dependence on the feed source of foreign enterprises. Consequently, many farmers were affected and gone out of business. In a nutshell, the number of cattle in Vietnam has been increasing and is on an upward trend (Fig. 1).

Fig. 1. Number of Buffalo and Cattle in Vietnam (1961-2014)

Source: FAOSTAT (2016)

In general, the Vietnam livestock industry has many weaknesses as follows:

- Majority of feed inputs in Vietnam are imported, so the cost of production of feeds is high. In livestock production, with 65-70% of feeds cost shared. Compared with Thailand, price of animal feeds in Vietnam is higher than 10%.

- Ability to control diseases in livestock is not that effective. Foot-and-mouth disease (FMD) in cattle is still prevalent in Vietnam.

- Breeding of animal is also a weakness. The development of breeding animal quality in Vietnam is time-consuming.

- Poor organization of Vietnam livestock: production scale is minor and also not have vertical integration from production to marketing. Eighty-five percent of cattle in Vietnam is still in the category of small-scale farming.

- Manual slaughtering is still popular in Vietnam, leading to problems in food hygiene and safety, and reduction of value-added activities for livestock production. Now, around 20% of meat production are done in meat processing plants.

- The taxes for importing meat in Vietnam is high, however in 2018, the taxes for importing meat cutback will be 0% based on the rules of AFTA and TPP. Vietnam’s livestock industry will face many challenges, especially competition, from abroad.

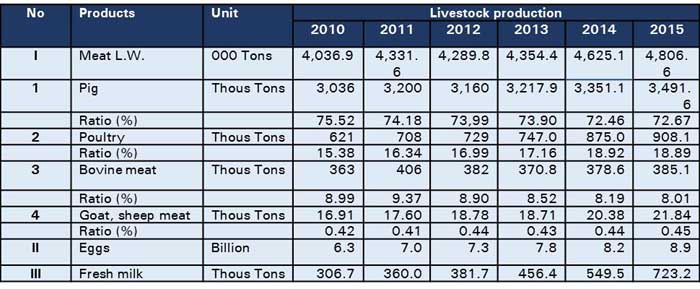

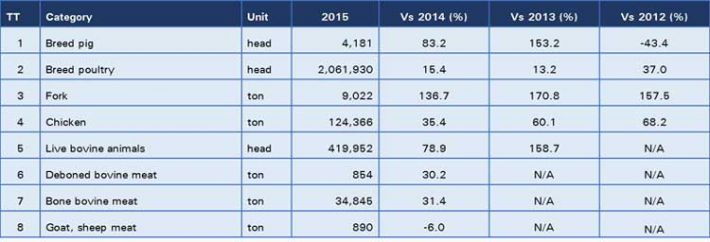

According to General Statistics Office of Vietnam (GSO-VN) in 2015, Vietnam has 2.58 million buffaloes; 5.18 million beef, increased 0.9% versus 2014. The number of buffaloes and cows continued to decline due to the decrease in their grazing area, low raising efficiency did not encourage farmers to invest. Table 1 shows the volume of livestock products in Vietnam for the past six years.

Table 1. Livestock products period 2010 – 2015 in Vietnam

Source: General Statistics Office of Vietnam (2016)

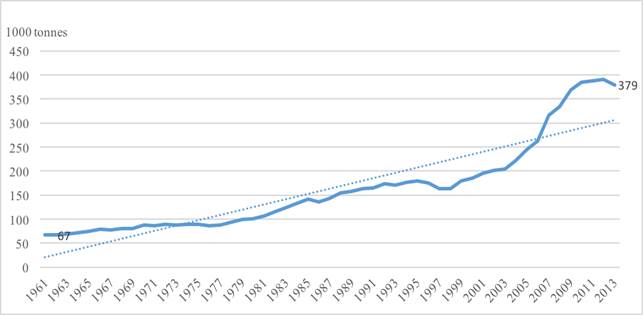

Conferring from U.S. Department of Agriculture, in 2016, demand of bovine meat in Vietnam was approximately 408,000 tons and bovine production in Vietnam is expected to reach 385,000 tons, and to meet the need to import at least 20,000 tons in 2014.

Food supply of bovine meat in Vietnam is shown in Fig. 2.

Fig. 2. Food supply of bovine meat in Vietnam from 1961-2013

Source: FAOSTAT (2016)

Demand of bovine meat in Vietnamese’s consumption

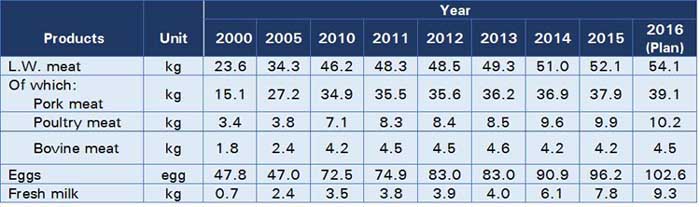

Rising demand for protein and the reduction of domestic beef supplies has placed Vietnam on the meat market map. However, meat consumption in Vietnam has risen significantly over the past decade and is expected to remain strong in the next five years. Average meat, egg, milk per capita per year in Vietnam during the period of 2000-2015 and its plan of 2016 are shown in Table 2.

Table 2. Average meat, egg, milk per capita per year in Vietnam

Source: General Statistics Office of Vietnam (2016)

The situation of imports of bovine meat

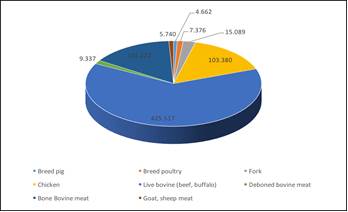

Vietnam has shown an improvement in the import of meat products since it joined the World Trade Organization (WTO) in 2007. With WTO trade agreements, the country has facilities to import. Vietnam’s livestock sector is not creating enough supply to meet its domestic demand. Besides, science and technology livestock production in this country is still considered poor and not comparable to many countries around the worlds. So imported meat products from overseas are considered inevitable to meet domestic demand. According to Vietnam Customs, Vietnam import value of live bovine was US$425.517 million in 2015 (Fig. 3).

Fig. 3. Vietnam import value of livestock products in 2015

Source: Vietnam Customs

Most of the beef consumed in Vietnam are derived from local cattle and live imports from Thailand, Laos and Cambodia, but the number of cattle imported from Australia has increased since 2010. The situation of imports of livestock products in Vietnam in 2015 is shown on Table 3.

Table 3. Review the situation of imports of livestock products in Vietnam in 2015

Source: Vietnam Customs (2016)

Opportunities for Thai Livestock Exporting

Situation of Thailand’s bovine animals and new supply chain

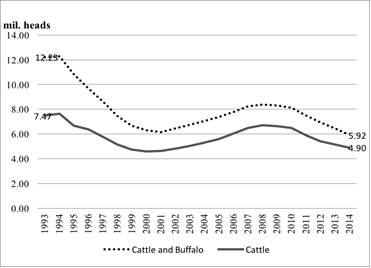

Thailand has a normal trend in decreasing cattle numbers from 1993 to 2014 (7.47 to 4.90 million heads) and decreasing buffalo numbers (4.75 to 1.02 million heads) according to FAOSTAT (2016). There have been previous incidents where agricultural mechanization replaced manual buffalo power. But other problems include debt, labor constraints, reduced grazing areas, and government policies that favor intensification of mono cropping. Overall, total bovine numbers have concentrated and are located in the Northeastern followed by the Central and the Northern Regions of the country. Bovine number in the North of Thailand is stabilized and developed. Number of head cattle and buffalo in Thailand is shown in Fig. 4.

Northeast Thailand, a large plateau of relatively infertile soils, is an area of traditional beef cattle farming. The region has undergone a rapid process of physical, social and economic change in the past 40 years. Clearing of forests during this period and the development of new infrastructure, particularly reading, has increased the level of human settlement and opened new agricultural areas for cropping.

Fig. 4. Number of head cattle and buffalo in Thailand from 1993-2014

Source: FAOSTAT (2016)

Thailand will be an agent between Australia and others countries. Following the Department of Agriculture and Food, Western Australia (DAFWA), there exists a new Supply Chain in Thailand, including:

- Live exports of feeder cattle with fattening and processing.

- Live Export of slaughter cattle with processing.

- Preliminary processing (e.g. carcass quarters/halves) in Australia with further processing in Thailand.

- Export of deboned beef from Australia.

With a range of competitive investment locations across Southeast Asia, the most suitable host country and specific site locations will ultimately depend on the needs and priorities of individual project proponents.

Australian Access into Thailand: Australia possesses tariff-free live cattle export into Thailand under the Thailand-Australia Free Trade Agreement (TAFTA). Conversely, processed beef imports are subjected to significant import tariffs (50% beef and 33% offal) enforced on imports beyond modest initial tariff-free quotas.

Opportunities export to Vietnam and ASIAN market

Thailand Access to Third Party Export Countries: Thailand possesses preferential access to regional beef markets through the ASEAN Economic Community (including Vietnam, Malaysia, Cambodia, Laos, and the Philippines) and the ASEAN-China Free Trade Agreement. Both country-level and facility level food health approvals will be required to permit beef exports into the lucrative Chinese market. Thailand has a strong reputation for quality as a food product exporter and is strategically positioning itself to supply growing regional food demand

Fig. 5. Beef and Veal Consumption Trends in some ASEAN countries, China and The World

Source: OECD (2015)

The Thailand beef industry is strategically placed in order to service growing Asian demand over the coming years. The development of a significant new supply chain utilizing modern processing and best practice management has the potential to drive significant industry development.

Table 4. Vietnam’s imports live bovine animals from Thailand

Source: trademap.org (2016)

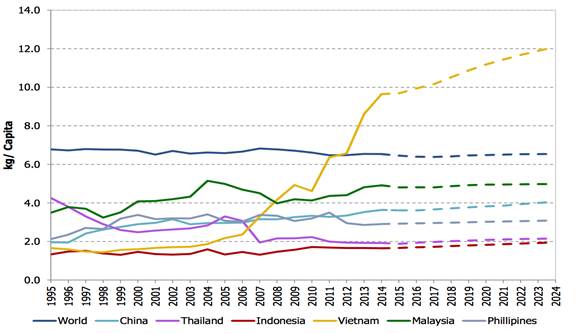

Elsewhere within the Association of South East Asian Nations (ASEAN) region (for countries with data available), Vietnam has recently experienced a surge in per capita consumption, driven by rising incomes and rising restaurant demand (Figure 5). Vietnamese data is also potentially influenced by rising cross-border trade to China.

The ASEAN Economic Community is creating a single market of over 600 million people. The creation of the ASEAN Economic Community enhances significant re-export opportunities for the new supply chain across the region.

Thailand has an established beef cattle industry that includes a well-developed feedlot sector. The Thai cattle industry incorporates local processing for the domestic market (just over 1 million head per annum), as well as significant feed lofting and live on-selling to surrounding Chinese and Association of South East Asian Nations (ASEAN) markets.

So SWOT analysis for Thai livestock exporting represent below:

Table 5. SWOT analysis and strategies for Thai livestock exporting to Vietnam market

CONCLUSION

Forecasts for 2019, reveal that total meat consumption in Vietnam will surpass the 4 million ton mark; accounting for nearly 65 % of total consumption, pork will still account for the largest share in the Vietnamese diet. However, significant growth is estimated at 3-5 % / year and is expected to open up promising prospects for the consumption of poultry meat and beef in the near future. However, this growth is not sufficient to meet market demand while supply and the stability of pork to meet domestic demand, supplies for beef and poultry meat could fall into serious shortages.

In the meantime, the potential for growing Thailand bovine exports to Vietnam remains high because of breeding, live bovine and bovine feedlotting and processing. A new supply chain from Australia exporting live feeder cattle to Thailand for fattening and processing possesses a number of advantages, including avoiding processed beef import quotas/tariffs and accessing low-cost feedlotting and processing labor within Thailand.

REFERECES

Agriculture, Forestry and Fishing. Statistical Data. General Statistics Office of Vietnam. https://www.gso.gov.vn

Review the situation of imports of livestock products in 2015. Vietnam Customs. Retrieved from http://www.customs.gov.vn/

Product: 0102 Live bovine animals. Bilateral trade between Viet Nam and Thailand. Bilateral trade between Viet Nam and Australia. Retrieved from http://www.trademap.org/

Retrieved from http://chartsbin.com/

Food Balance Sheets. FAOSTAT. Retrieved from http://fenix.fao.org/faostat/beta/en/#data/FBS

Meat consumption. OECD Data. Retrieved from https://data.oecd.org/agroutput/meat-consumption.htm

Production/Live Animals. FAOSTAT. Retrieved from http://faostat3.fao.org

New and innovative beef supply chains in Thailand. Prepared by AEC Group for the Department of Agriculture and Food, Western Australia (DAFWA)

|

Date submitted: Sept. 30, 2016

Reviewed, edited and uploaded: Oct. 5, 2016

|

Production of Bovine Meat in Vietnam – Opportunities for Exporting Thai Livestock

INTRODUCTION

With the increased demand for meat of bovine animals (beef and buffalo meat), Vietnamese producers need to be more strategic in their plans in order to be proficient to supply local demand. They also need to compete with foreign imports. Quantity of bovine meat per capita in Vietnam increased yearly by level of consumption. The Vietnam livestock industry has many weaknesses from production to marketing.

According to Chartsbin, Vietnam is on the world’s top 15 in terms of quantity of meat production as well as consumption. It annually produces 3.6 million tons and consumes 4.1 million tons of meat (every year, Vietnam must import meat to meet local demand). In terms of per capita consumption, Vietnam is at a low - average level of about 50 kg/person/year. However, compared to other countries in Southeast Asia, Vietnam is the second largest country with per capita meat consumption, followed by Malaysia (52.3 kg) and significantly higher than Philippines (33.6 kg), Thailand (25.8 kg) and Indonesia (11.6 kg).

Among the variety of meat types, pork, beef and poultry are considered important meats. Currently, Thailand has the potential for breeding and bovine feedlotting and processing. The country has the opportunities to export more bovine meat to the Vietnam market.

Livestock Products Overview and Demand of Bovine Meat in Vietnam

Vietnam livestock products overview

Livestock is an important economic sector of Vietnam, which creates supply of foodstuff for the Vietnamese people. The industry helps farmers to increase their income. For over a decade, the livestock industry has gradually shifted from small-scale production to bigger scale farms, with focus on ensuring food safety and minimizing environmental pollution.

However, in recent years, the livestock sector in Vietnam has met many difficulties such as rising input costs (mainly as animal feed), output price instability, diseases, excessive use of prohibited substances and antibiotics, competition from imported meat products, and dependence on the feed source of foreign enterprises. Consequently, many farmers were affected and gone out of business. In a nutshell, the number of cattle in Vietnam has been increasing and is on an upward trend (Fig. 1).

Fig. 1. Number of Buffalo and Cattle in Vietnam (1961-2014)

Source: FAOSTAT (2016)

In general, the Vietnam livestock industry has many weaknesses as follows:

According to General Statistics Office of Vietnam (GSO-VN) in 2015, Vietnam has 2.58 million buffaloes; 5.18 million beef, increased 0.9% versus 2014. The number of buffaloes and cows continued to decline due to the decrease in their grazing area, low raising efficiency did not encourage farmers to invest. Table 1 shows the volume of livestock products in Vietnam for the past six years.

Table 1. Livestock products period 2010 – 2015 in Vietnam

Source: General Statistics Office of Vietnam (2016)

Conferring from U.S. Department of Agriculture, in 2016, demand of bovine meat in Vietnam was approximately 408,000 tons and bovine production in Vietnam is expected to reach 385,000 tons, and to meet the need to import at least 20,000 tons in 2014.

Food supply of bovine meat in Vietnam is shown in Fig. 2.

Fig. 2. Food supply of bovine meat in Vietnam from 1961-2013

Source: FAOSTAT (2016)

Demand of bovine meat in Vietnamese’s consumption

Rising demand for protein and the reduction of domestic beef supplies has placed Vietnam on the meat market map. However, meat consumption in Vietnam has risen significantly over the past decade and is expected to remain strong in the next five years. Average meat, egg, milk per capita per year in Vietnam during the period of 2000-2015 and its plan of 2016 are shown in Table 2.

Table 2. Average meat, egg, milk per capita per year in Vietnam

Source: General Statistics Office of Vietnam (2016)

The situation of imports of bovine meat

Vietnam has shown an improvement in the import of meat products since it joined the World Trade Organization (WTO) in 2007. With WTO trade agreements, the country has facilities to import. Vietnam’s livestock sector is not creating enough supply to meet its domestic demand. Besides, science and technology livestock production in this country is still considered poor and not comparable to many countries around the worlds. So imported meat products from overseas are considered inevitable to meet domestic demand. According to Vietnam Customs, Vietnam import value of live bovine was US$425.517 million in 2015 (Fig. 3).

Fig. 3. Vietnam import value of livestock products in 2015

Source: Vietnam Customs

Most of the beef consumed in Vietnam are derived from local cattle and live imports from Thailand, Laos and Cambodia, but the number of cattle imported from Australia has increased since 2010. The situation of imports of livestock products in Vietnam in 2015 is shown on Table 3.

Table 3. Review the situation of imports of livestock products in Vietnam in 2015

Source: Vietnam Customs (2016)

Opportunities for Thai Livestock Exporting

Situation of Thailand’s bovine animals and new supply chain

Thailand has a normal trend in decreasing cattle numbers from 1993 to 2014 (7.47 to 4.90 million heads) and decreasing buffalo numbers (4.75 to 1.02 million heads) according to FAOSTAT (2016). There have been previous incidents where agricultural mechanization replaced manual buffalo power. But other problems include debt, labor constraints, reduced grazing areas, and government policies that favor intensification of mono cropping. Overall, total bovine numbers have concentrated and are located in the Northeastern followed by the Central and the Northern Regions of the country. Bovine number in the North of Thailand is stabilized and developed. Number of head cattle and buffalo in Thailand is shown in Fig. 4.

Northeast Thailand, a large plateau of relatively infertile soils, is an area of traditional beef cattle farming. The region has undergone a rapid process of physical, social and economic change in the past 40 years. Clearing of forests during this period and the development of new infrastructure, particularly reading, has increased the level of human settlement and opened new agricultural areas for cropping.

Fig. 4. Number of head cattle and buffalo in Thailand from 1993-2014

Source: FAOSTAT (2016)

Thailand will be an agent between Australia and others countries. Following the Department of Agriculture and Food, Western Australia (DAFWA), there exists a new Supply Chain in Thailand, including:

With a range of competitive investment locations across Southeast Asia, the most suitable host country and specific site locations will ultimately depend on the needs and priorities of individual project proponents.

Australian Access into Thailand: Australia possesses tariff-free live cattle export into Thailand under the Thailand-Australia Free Trade Agreement (TAFTA). Conversely, processed beef imports are subjected to significant import tariffs (50% beef and 33% offal) enforced on imports beyond modest initial tariff-free quotas.

Opportunities export to Vietnam and ASIAN market

Thailand Access to Third Party Export Countries: Thailand possesses preferential access to regional beef markets through the ASEAN Economic Community (including Vietnam, Malaysia, Cambodia, Laos, and the Philippines) and the ASEAN-China Free Trade Agreement. Both country-level and facility level food health approvals will be required to permit beef exports into the lucrative Chinese market. Thailand has a strong reputation for quality as a food product exporter and is strategically positioning itself to supply growing regional food demand

Fig. 5. Beef and Veal Consumption Trends in some ASEAN countries, China and The World

Source: OECD (2015)

The Thailand beef industry is strategically placed in order to service growing Asian demand over the coming years. The development of a significant new supply chain utilizing modern processing and best practice management has the potential to drive significant industry development.

Table 4. Vietnam’s imports live bovine animals from Thailand

Source: trademap.org (2016)

Elsewhere within the Association of South East Asian Nations (ASEAN) region (for countries with data available), Vietnam has recently experienced a surge in per capita consumption, driven by rising incomes and rising restaurant demand (Figure 5). Vietnamese data is also potentially influenced by rising cross-border trade to China.

The ASEAN Economic Community is creating a single market of over 600 million people. The creation of the ASEAN Economic Community enhances significant re-export opportunities for the new supply chain across the region.

Thailand has an established beef cattle industry that includes a well-developed feedlot sector. The Thai cattle industry incorporates local processing for the domestic market (just over 1 million head per annum), as well as significant feed lofting and live on-selling to surrounding Chinese and Association of South East Asian Nations (ASEAN) markets.

So SWOT analysis for Thai livestock exporting represent below:

Table 5. SWOT analysis and strategies for Thai livestock exporting to Vietnam market

CONCLUSION

Forecasts for 2019, reveal that total meat consumption in Vietnam will surpass the 4 million ton mark; accounting for nearly 65 % of total consumption, pork will still account for the largest share in the Vietnamese diet. However, significant growth is estimated at 3-5 % / year and is expected to open up promising prospects for the consumption of poultry meat and beef in the near future. However, this growth is not sufficient to meet market demand while supply and the stability of pork to meet domestic demand, supplies for beef and poultry meat could fall into serious shortages.

In the meantime, the potential for growing Thailand bovine exports to Vietnam remains high because of breeding, live bovine and bovine feedlotting and processing. A new supply chain from Australia exporting live feeder cattle to Thailand for fattening and processing possesses a number of advantages, including avoiding processed beef import quotas/tariffs and accessing low-cost feedlotting and processing labor within Thailand.

REFERECES

Agriculture, Forestry and Fishing. Statistical Data. General Statistics Office of Vietnam. https://www.gso.gov.vn

Review the situation of imports of livestock products in 2015. Vietnam Customs. Retrieved from http://www.customs.gov.vn/

Product: 0102 Live bovine animals. Bilateral trade between Viet Nam and Thailand. Bilateral trade between Viet Nam and Australia. Retrieved from http://www.trademap.org/

Retrieved from http://chartsbin.com/

Food Balance Sheets. FAOSTAT. Retrieved from http://fenix.fao.org/faostat/beta/en/#data/FBS

Meat consumption. OECD Data. Retrieved from https://data.oecd.org/agroutput/meat-consumption.htm

Production/Live Animals. FAOSTAT. Retrieved from http://faostat3.fao.org

New and innovative beef supply chains in Thailand. Prepared by AEC Group for the Department of Agriculture and Food, Western Australia (DAFWA)

Date submitted: Sept. 30, 2016

Reviewed, edited and uploaded: Oct. 5, 2016