The emergence of new digital channel and technology has changed the way in which the agriculture sector generate revenue and improve performances (Mueller 2001, Canavari et al. 2010, Carpio et al. 2013). In the past five years, the internet has been used for buying and selling agricultural products in Thailand. However, the level of adoption of e-commerce among Thai farmers and SMEs in the agricultural sector are slow, compared with other sectors. Even though selling agricultural products through online channels enables farmers to eliminate intermediaries and leads to more benefit gain for farmers, most Thai farmers still preferred offline channels for agricultural products to online channels. Only a few SMEs and farmers, especially young smart farmers and farmers of specialty products (i.e. organic, natural, patricide free), applied to use digital channels.

According to the Electronics Transaction Development Agency (ETDA 2019a), two out of eight industries related to e-commerce for agricultural products, which were wholesale and retail industry and manufacturing industry (ETDA 2019a). The market value of e-commerce wholesale and retail industry was generally relied on SMEs, while manufacturing mostly generated by large enterprises. (Figure 1). For manufacturing industry[1], various agricultural and industrial products were processed and sell through digital channel including the B2C platform (61.38%) and the B2B platform (38.62%). However, data on the agricultural products in manufacturing industry was limited, thus this section mainly focused on e-commerce in wholesale and retail industry.

Figure 1. The types of enterprises in e-commerce for agricultural products

Source: Electronics Transaction Development Agency, 2019a

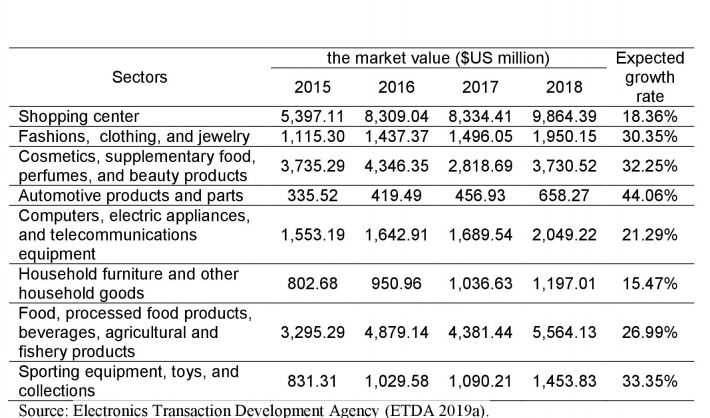

The leading e-commerce industry was wholesale and retail and categorized into eight sectors, which were shopping center (37.27%), food, beverages, agricultural and fishery products (21.02%), and cosmetics, supplementary food, and beauty products (14.09%) (Table 2). The market channel share of wholesale and retail industry was from the B2C platform (83.04%) and the B2B platform (16.96%). The market value of e-commerce of wholesale and retail industry in food, processed food, beverages, agriculture and fishery sector at $US 5,564.13 million was mainly generated by SMEs (94.7%) and large enterprises (5.31%) (ETDA 2019b). For SMEs, the most preferred channels for e-commerce was the social commerce (75.3%) followed by e-marketplace (23.9%) and brand websites (0.8%). Key driving factors of the growth of social commerce were messaging between consumers and businesses, creating added value to both sellers and buyers, costing low investments, rising access to the internet for consumers, operating easily with applications, offering e-payment with several payment gateways, and providing logistics services (Fruhling and Digman 2000, ETDA 2019b).

Table 2. The market value of e-commerce in wholesale and retail industry by sectors

E-commerce platforms in agricultural markets

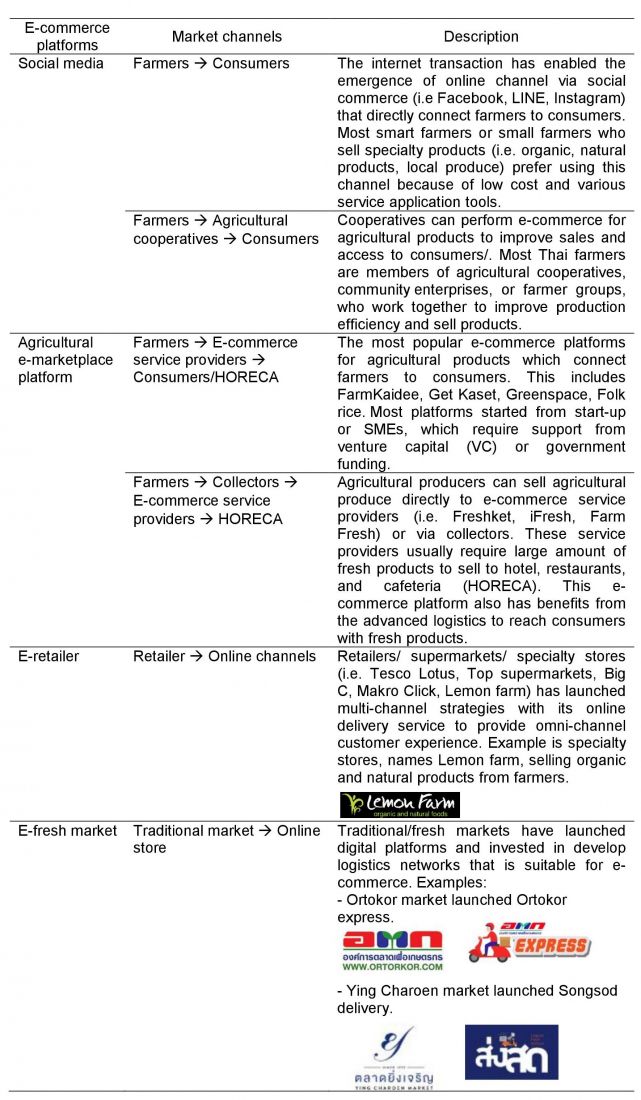

Digital platform has enabled larger visibility into both domestic and international supply chain of agricultural products (Mueller 2001, Hennessy et al. 2016). The relationship between sellers (i.e. farmers, agricultural cooperatives, and SMEs) and buyers are closer and more easily connected. In Thailand, agricultural products are available in six different market channels under four e-commerce platforms (Table 3). Four e-commerce platforms consist of social media, agricultural e-marketplace platform, e-retailers, and e-fresh market. The role of players in agri-food supply chain includes farmers, agricultural cooperatives, collectors, e-commerce providers, retailers, traditional markets, and end users. Another important player is logistic service providers, operating in two systems: on-demand delivery (i.e. Skootar, Lalamove) and third-party logistics (i.e. Kerry, Thailand post, FedEx, DHL). Financial service provider is also a key player in e-commerce platform. Two types of e-payments are payment gateway (i.e. 2C2P, PayPal, Omise, truemoney) and mobile payment (i.e. mobile banking).

Table 3. Market channels of e-commerce platforms for agricultural products

Source: author’s collection

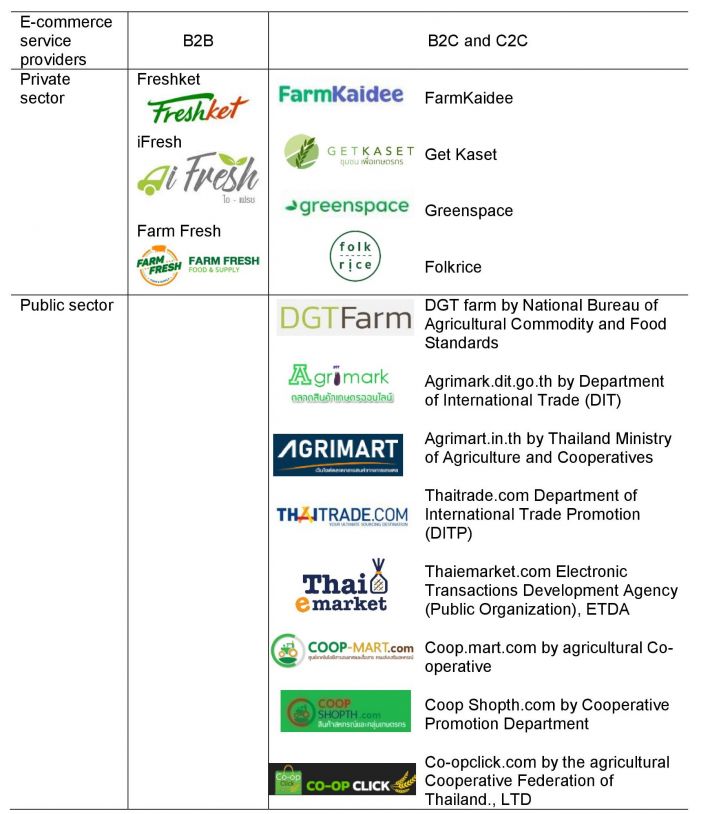

In recent years, a number of agricultural e-commerce services under B2B, B2C, and C2C platforms have been launched in Thailand (Table 4). These services provide farmers with new ways of selling their produce and reaching new buyers (Mueller 2000). One important move towards digital agricultural markets is being made by the government institution or public sector such as DGT farm created the e-marketing platform to match between farmers and consumers. With a great potential to e-commerce in agricultural sector, many e-commerce service providers by private sector have been established; however, most services are still in the start-up phase and require sources of funding and time to build up the business. For example, Get Kaset is C2C e-commerce service provider creating an online agricultural market to help farmers sell their agricultural products directly to customers at the fair price. Freshket is B2B e-marketplace platforms for fresh food suppliers and restaurants that help farmers/suppliers and restaurants buy/sell fresh products.

Table 4. E-commerce service providers for agricultural products

Source: author’s collection

Policy affecting e-commerce in agricultural markets

Common problems faced by Thai farmers are insufficient land, inadequate agriculture infrastructure, high costs of production inputs, lack of marketing skills, receiving unfair prices from middlemen or collectors, and aging farmers. Many Thai farmers could not receive enough revenue to cover their production costs. Risks in agricultural e-commerce for farmers and SMEs can divided into six issues: production risks, marketing risks, financial risks, legislation and policy risks, technology risks, and labor risks. For production risks, unstable weather conditions such as drought or rainfall, lack of efficient equipment and machinery, and damage due to pests and disease could be source of these risks. Marketing risks are prominent issues among Thai farmers, resulted from price instability, lack of knowledge on product pricing, data analysis, and operation, high level of competitive among similar products, low product and service quality, unattractive packaging, and ability to access to the market (Coble et al. 2018, Fecke et al. 2018). Financial risks came from limited access to financial institutions, funding sources, high input costs, and lack of adequate cash or credit. Legislation and policy risks associated with e-commerce tax uncertainty and the harmful effect by the government policy, which was inconsistent and short term implementation. Challenges on regulation for e-commerce would delay an investment decision on both domestic and cross-broader e-commerce. Technology risks resulted from less trust in e-payment, slow adoption in agricultural e-commerce platforms among farmers and SMEs, and the lack of national pooled data sharing and accessibility. Labor risks related to lack of skilled labor in information technology (IT), management, and negotiation; as well as moving toward the aging society of farmers.

Following problems and risks in agricultural e-commerce for farmers and SMEs, the government digitalized farmers and SMEs through online agricultural markets. Currently, the government policies directly affected the development of e-commerce.

- “Transform for SMEs 4.0” policy primarily focused on support the local communities and SME in agricultural sectors by enhancing market access and developing farmer’s business skills.

- The Ministry of Finance introduced e-payment in 2016 such as prompt-pay policy and standardized QR code payment to encourage Thai consumes to use e-payment and to enable digital payments with mobile phone. This benefits to SMEs and farmers to reduce transaction costs and close the sales.

- Four national e-commerce strategies have been implemented in 2017 including 1) enhance the entrepreneur by creating digital marketing skills and developing e-commerce products and standards 2) strengthen ecosystem for e-commerce by supporting cashless society and improve logistic network 3) improve the effectiveness of soft-infrastructure by making ease to access the pools of data 4) build trust in e-commerce market by ensuring consumer protection (ETDA 2018).

- The Office of SMEs Promotion (OSMEP) has collaborated work with Department of Agriculture extension and Bank of Agriculture and Agricultural Cooperatives (BAAC) launched “SMEs GO Online” campaign in 2019 to train SMEs on online marketing skills and entrepreneurship.

Challenges of e-commerce for agricultural products

Currently, the changes of technology and variety of digital platforms would enhance the farmer’s revenue and welfare. Moreover, the stakeholders in the agri-food chain would gain some benefits from providing fresher agricultural products to consumers, supporting directly to farmers, and expanding the market to both domestic and international markets (Fruhling and Digman 2000, Mueller 2001, Hennessy et al. 2016, Zapata et al. 2016). To shift tradition transaction to digital transaction in agricultural market, it is a long term process. In addition, the adoption of e-commerce on agricultural products are in an early stage, so several challenges are needed to be considered.

- The market structure of e-commerce for agricultural products in Thailand is considered as a monopolistic competition. A range of product differentiation is limited for agricultural products. New competitors are easily to enter the market, but need good operation and marketing skills and time to gain trust from the customers.

- Logistic infrastructure of Thailand ranked 41st in the world, of which the logistic infrastructure described as quality of trade and transport related infrastructure (i.e. poor road conditions, information technology) (World Bank 2018). In Thailand, logistic system faced heavy traffic, low levels of critical infrastructure in rural area, and high cost in cold chain system, leading to the logistical challenges of long delivery time and complex handling fresh produce.

- Most Thai consumers still preferred to buy agricultural products by themselves. Moreover, Thai consumers mostly relied on information on social media (i.e. product information, reviews) (Euromonitor International 2018). Therefore, quality control on physical appearance of products and the reliability for agricultural e-commerce are important.

- E-payment is one of the major challenges in the development of e-commerce. Even the number of e-commerce users was about 51.3% in 2018, but there were 42.7% who paid by using credit card (ETDA 2019a). Some consumers (6.8%) preferred not to purchase product and service online due to concern about frauds (ETDA 2019b). Lack of trust in digital payment has an impact on the adoption of e-commerce on agricultural products.

- Challenges on regulation for e-commerce including consumer protection, trade policy, tax policy, and environmental policy are uncertain. A lack of information causes economic loss and less opportunity for investment.

- A small number of Thai farmers and SMEs can adapt to digital channels. The government should encourage farmers and SMEs by training courses (i.e. e-commerce marketing, entrepreneurship, smart farmers, and technology application) and implementing a long term project (more than 2 years) to ensure that the online business of farmers or SMEs are well established. Moreover, the availability of funding sources, the development of co-creation among parties, and competition for new business model would create innovative start-up and potential e-commerce businesses.

CONCLUSION

As digital platform has emerged, the e-commerce has applied to many industries. Online channel was slowly adapted to agricultural sector. Online agricultural markets create values for agri-food chain, support the use of digital platform to eliminate intermediaries, and help farmers sell their product at fair prices. In Thailand, B2C and C2C e-commerce platform played a major role in agricultural market. The value of Thailand’s e-commerce market was approximately $US 5,564.13 million in 2018. Major contribution to agricultural e-commerce came from SMEs where social commerce (i.e. Facebook and LINE) and e-marketplace were the top market channels for agricultural products. E-marketplace by the private sector has become increasingly dynamic. For the agricultural sector in Thailand, six market channels from farmers to end users were discussed with four e-commerce platform (social media, e-marketplace, e-retail, and e-fresh market). Increase in mobile connectivity has positively influenced the driving e-commerce in the agricultural sector. Even though some challenges to e-commerce for agricultural products have been improved (i.e. the digital infrastructure in the rural area), both current and new issues (i.e. long delivery time and complex handling fresh produce) need to be addressed. The logistical challenges of fresh produce and a small number of farmers’ adaption toward digital platform are significant issues. To succeed, agricultural e-commerce enterprises require scalable economy and sustainable business. The government should provide projects and funding to new farmers and SMEs to develop new business model for agricultural produce and promote the use of mobile internet and digital payment by end consumers. Moreover, creating the e-commerce ecosystem and building entrepreneurship environment would create a new opportunity and career to agricultural sectors.

REFERENCES

Canavari, M., Fritz, M., Hofstede, G.J., Matopoulos, A. and Vlachopoulou, M. 2010. The role of trust in the transition from traditional to electronic B2B relationships in agri-food chains. Computers and electronics in agriculture 70(2):321-327.

Carpio, C.E., Isengildina-Massa, O., Lamie, R.D. and Zapata, S.D. 2013. Does e-commerce help agricultural markets? The case of MarketMaker. Choices, 28(4), pp.1-7.

Coble, K.H., Mishra, A.K., Ferrell, S. and Griffin, T. 2018. Big data in agriculture: A challenge for the future. Applied Economic Perspectives and Policy, 40(1), pp.79-96.

Electronics Transaction Development Agency. 2018. National e-Commerce Strategy in Thailand, Office of Policy and Strategic Affairs, Electronic Transactions Development Agency, Ministry of Digital Economy and Society, Thailand. Available from https://www.etda.or.th/publishing-detail/national-e-commerce-strategy-in-thailand.html [Accessed 7 May 2019].

Electronics Transaction Development Agency. 2019a. The Value of E-Commerce Survey in Thailand 2018, Office of Policy and Strategic Affairs, Electronic Transactions Development Agency, Ministry of Digital Economy and Society, Thailand. Available from https://www.etda.or.th/publishing-detail/value-of-e-commerce-survey-in-thailand-2018.html [Accessed 4 June 2019].

Electronics Transaction Development Agency. 2019b. Thailand Internet User Profile 2018, Office of Policy and Strategic Affairs, Electronic Transactions Development Agency, Ministry of Digital Economy and Society, Thailand. Available from https://www.etda.or.th/publishing-detail/thailand-internet-user-profile-2018.html [Accessed 4 June 2019].

Euromonitor International 2018. Internet retailing in Thailand 2018. Available from https://www.euromonitor.com/internet-retailing-in-thailand/report [Accessed 4 May 2019].

Fecke, W., Danne, M. and Musshoff, O. 2018. E-commerce in agriculture–The case of crop protection product purchases in a discrete choice experiment. Computers and electronics in agriculture, 151, pp.126-135.

Fruhling, A.L. and Digman, L.A. 2000. The impact of electronic commerce on business-level strategies. Journal of Electronic Commerce Research, 1(1), p.13.

Hennessy, T., Läpple, D. and Moran, B. 2016. The digital divide in farming: a problem of access or engagement? Applied Economic Perspectives and Policy 38(3):474-491.

Mueller, R.A. 2000. Emergent E-commerce in Agriculture (No. 14). University of California, Agricultural Issues Center.

Mueller, R.A. 2001. E-commerce and entrepreneurship in agricultural markets. American Journal of Agricultural Economics, 83(5), pp.1243-1249.

NESDB. 2019. Gross Domestic Product Chain Volume Measures 1/2562, Office of the National Economic and Social Development Council (NESDB), Thailand. Available from https://www.nesdb.go.th/main.php?filename=QGDP_report [Accessed 5 April 2019].

OECD. 2019. Unpacking E-commerce: Business Models, Trends and Policies, Organization for Economic Co-Operation and Development (OECD) Publishing, Paris. Available from https://doi.org/10.1787/23561431-en [Accessed 25 June 2019].

OSMEP. 2018. Situation report of SMEs in 2017. The Office of SMEs Promotion (OSMEP), Thailand. Available from http://www.sme.go.th/th/download.php?modulekey=215&cid=0 [Accessed 25 June 2019].

World Bank. 2018. International LPI, Country score card: Thailand 2018. Available from https://lpi.worldbank.org/international/scorecard/radar/255/C/THA/2018#chartarea [Accessed 25 June 2019].

Zapata, S.D., Isengildina-Massa, O., Carpio, C.E. and Lamie, R.D. 2016. Does E-Commerce Help Farmers’ Markets? Measuring the Impact of MarketMaker. Journal of Food Distribution Research, 47(856-2016-58222), pp.1-18.

|

Date submitted: July 22, 2019

Reviewed, edited and uploaded: August 12, 2019

|

[1] Manufacturing industry consists of food products, beverages, textile, leather, paper, rubber, wood products, basic pharmaceutical products, primary metal products, non-metallic products (i.e. glass products, clay building materials, cement), and furniture.

E-commerce of Agricultural Products in Thailand

ABSTRACT

With the emergence of digital channels and growing e-commerce across industries in Thailand, the e-commerce for the agricultural sector has gradually emerged. Digital platforms can enable farmers to overcome agricultural problems throughout the value chain from upstream to downstream. Farmers and SMEs can sell agricultural products directly to e-commerce service providers, retailers, and consumers, leading to increased efficiency of the agri-food supply chain and generating greater revenue, as well as a better relationship between buyers and sellers. The B2C and C2C e-commerce platforms are prominent business models for agricultural products. The market value of agricultural e-commerce mainly contributed from small and medium enterprises (SMEs) where social commerce (i.e. facebook and LINE) and e-marketplace were top preferred market channels. Agricultural e-commerce service providers can be a direct positive influence on driving digital adoption among farmers. The government pushed the shift in the agricultural sector toward online channel with “Thailand 4.0” policy, “Transform for SMEs 4.0” policy, and national e-commerce strategies, which provided support on the development of digital platform and digital marketing skills on SMEs and farmers, as well as, improved the digital infrastructure and built the digital network in the rural area. To shift traditional commerce toward e-commerce in agricultural market, building digital ecosystem and entrepreneurship environment, as well as enhancing farmers and SMEs to adopt digital channels are suggested.

Keywords: e-commerce, ecosystem, digital platform, agricultural products, SMEs, Thailand

INTRODUCTION

E-commerce in Thailand

E-commerce is defined as the transactions between buyer and seller via the internet (Fruhling and Digm 2000, Mueller 2000, OECD 2019). With the highly urbanized population and hectic lifestyles, Thailand is one of the world’s fastest growing e-commerce markets. The value of Thailand’s e-commerce market amounted to US$101.59 billion[1] in 2018 with the growth rate at 14% annually on average (ETDA 2019a). The total e-commerce enterprises in Thailand was 644,071 enterprises, which can be divided based on the market value into small and medium enterprises or SMEs (33.73%) and large enterprises (76.45%). E-commerce transactions involved three types of partners: consumers, business, and government with six combinations of platforms, of which four are considered important platforms in Thailand: business-to-business (B2B); business-to-consumers (B2C); consumer-to-consumer (C2C), and business-to-government (B2G) transactions[2]. In 2018, the B2B platform carried the highest value of the e-commerce market (54.36%) followed by the B2C platform (27.47%)[3], and the B2G platform (18.17%) (ETDA 2019a). The e-commerce market of B2B and B2C platforms can be divided into eight economic industries including wholesale and retail (31.84%), accommodation service (24.58%), manufacturing (20.89%), information and communication (16.15%), transportation (4.89%), art and entertainment (1.13%), other service business, (0.40%), and insurance (0.13%).

In Thailand, e-commerce has been applied in many business sectors, especially retail, service, and financial industries. There are two main e-commerce players in Thailand including Lazada (B2C platform) and Shopee (B2C platform and C2C platform). In 2017, internet users in Thailand was reported at 45.2 million with mobile penetration rate at 88.25, giving that one Thai person penetrates the mobile phone number more than one number (ETDA 2019b). One of driving factors was the government policy, names “Net pracharat” project, which aimed to improve the digital infrastructure in the rural area. Another driver is the shift of consumer lifestyle to digital life such as buying products and services, communicating via social media, watching movies, ordering food delivery, and surfing product information (ETDA 2019b). The number of mobile internet users continues to grow year-by-year, especially using for accessing social media. The top five social media platforms in Thailand are YouTube, Facebook, Line, Messenger, and Instagram. In general, four different e-commerce platforms in Thailand can be categorized into four channels as follows:

Both internal and external factors play prominent roles in the rapid growth of e-commerce in Thailand (ETDA 2019a). For internal factors, more digital platforms are offered to consumers; as well as, some enterprises have more experiences in digital platforms and are able to apply different digital marketing strategies to each platform. The rise of the internet through mobile connectivity and increasing role of mobile networks has become the key in improving the e-commerce. For external factors, the government policy on digital economy, “Thailand 4.0” provided support on the development of the digital infrastructure, as well as built the digital connectivity and internet network in the rural area. Boosting digital ecosystem and giving buyers and sellers a more convenient way to make transactions via digital platforms would shift traditional commerce toward e-commerce. Therefore, the growing popularity of e-commerce has created opportunities for all types of businesses including SMEs and small farmers in the agri-food sector.

The development of e-commerce for agricultural products

The 2017 Gross Domestic Production (GDP) of agriculture sector in Thailand accounted for 8.7% of the total GDP at US$498 billion, while the rest was generated from non-agriculture sectors (NESDB 2018). For the contribution to the economy based on the enterprise size, small enterprises (SE) contributed 30% of GDP, medium enterprise (ME)[1] contributed 12.4% of GDP, and the large enterprises (LE) contributed 43% of GDP. Two sectors related to agricultural products were the trade & repairs and manufacturing, which were mainly generated by SMEs or the total of SE and ME (Table 1). In the traditional agri-food supply chain, farmers sell agricultural products through four channels: 1) direct sales, 2) farmer groups, community enterprises, agricultural cooperatives, 3) SMEs, and 4) middlemen or collectors where SMEs consists of the private/public enterprises registered as individual or juristic persons or community enterprises in which these enterprises operate under four economic activities: manufacturing, services, retail, and wholesale (OSMEP 2018). The majority of Thai farmers sold their agricultural products to middleman at farmgate prices, which was lower than the market prices. Examples of direct sales through offline channels are traditional markets or wet markets, flee market, wholesale market, and physical stores. Each channel has potential for e-commerce to disrupt the traditional transactions, especially selling through middlemen or collectors where e-commerce can create new links between farmers and consumers to bypass intermediaries.

The emergence of new digital channel and technology has changed the way in which the agriculture sector generate revenue and improve performances (Mueller 2001, Canavari et al. 2010, Carpio et al. 2013). In the past five years, the internet has been used for buying and selling agricultural products in Thailand. However, the level of adoption of e-commerce among Thai farmers and SMEs in the agricultural sector are slow, compared with other sectors. Even though selling agricultural products through online channels enables farmers to eliminate intermediaries and leads to more benefit gain for farmers, most Thai farmers still preferred offline channels for agricultural products to online channels. Only a few SMEs and farmers, especially young smart farmers and farmers of specialty products (i.e. organic, natural, patricide free), applied to use digital channels.

According to the Electronics Transaction Development Agency (ETDA 2019a), two out of eight industries related to e-commerce for agricultural products, which were wholesale and retail industry and manufacturing industry (ETDA 2019a). The market value of e-commerce wholesale and retail industry was generally relied on SMEs, while manufacturing mostly generated by large enterprises. (Figure 1). For manufacturing industry[1], various agricultural and industrial products were processed and sell through digital channel including the B2C platform (61.38%) and the B2B platform (38.62%). However, data on the agricultural products in manufacturing industry was limited, thus this section mainly focused on e-commerce in wholesale and retail industry.

Figure 1. The types of enterprises in e-commerce for agricultural products

Source: Electronics Transaction Development Agency, 2019a

The leading e-commerce industry was wholesale and retail and categorized into eight sectors, which were shopping center (37.27%), food, beverages, agricultural and fishery products (21.02%), and cosmetics, supplementary food, and beauty products (14.09%) (Table 2). The market channel share of wholesale and retail industry was from the B2C platform (83.04%) and the B2B platform (16.96%). The market value of e-commerce of wholesale and retail industry in food, processed food, beverages, agriculture and fishery sector at $US 5,564.13 million was mainly generated by SMEs (94.7%) and large enterprises (5.31%) (ETDA 2019b). For SMEs, the most preferred channels for e-commerce was the social commerce (75.3%) followed by e-marketplace (23.9%) and brand websites (0.8%). Key driving factors of the growth of social commerce were messaging between consumers and businesses, creating added value to both sellers and buyers, costing low investments, rising access to the internet for consumers, operating easily with applications, offering e-payment with several payment gateways, and providing logistics services (Fruhling and Digman 2000, ETDA 2019b).

Table 2. The market value of e-commerce in wholesale and retail industry by sectors

E-commerce platforms in agricultural markets

Digital platform has enabled larger visibility into both domestic and international supply chain of agricultural products (Mueller 2001, Hennessy et al. 2016). The relationship between sellers (i.e. farmers, agricultural cooperatives, and SMEs) and buyers are closer and more easily connected. In Thailand, agricultural products are available in six different market channels under four e-commerce platforms (Table 3). Four e-commerce platforms consist of social media, agricultural e-marketplace platform, e-retailers, and e-fresh market. The role of players in agri-food supply chain includes farmers, agricultural cooperatives, collectors, e-commerce providers, retailers, traditional markets, and end users. Another important player is logistic service providers, operating in two systems: on-demand delivery (i.e. Skootar, Lalamove) and third-party logistics (i.e. Kerry, Thailand post, FedEx, DHL). Financial service provider is also a key player in e-commerce platform. Two types of e-payments are payment gateway (i.e. 2C2P, PayPal, Omise, truemoney) and mobile payment (i.e. mobile banking).

Table 3. Market channels of e-commerce platforms for agricultural products

Source: author’s collection

In recent years, a number of agricultural e-commerce services under B2B, B2C, and C2C platforms have been launched in Thailand (Table 4). These services provide farmers with new ways of selling their produce and reaching new buyers (Mueller 2000). One important move towards digital agricultural markets is being made by the government institution or public sector such as DGT farm created the e-marketing platform to match between farmers and consumers. With a great potential to e-commerce in agricultural sector, many e-commerce service providers by private sector have been established; however, most services are still in the start-up phase and require sources of funding and time to build up the business. For example, Get Kaset is C2C e-commerce service provider creating an online agricultural market to help farmers sell their agricultural products directly to customers at the fair price. Freshket is B2B e-marketplace platforms for fresh food suppliers and restaurants that help farmers/suppliers and restaurants buy/sell fresh products.

Table 4. E-commerce service providers for agricultural products

Source: author’s collection

Policy affecting e-commerce in agricultural markets

Common problems faced by Thai farmers are insufficient land, inadequate agriculture infrastructure, high costs of production inputs, lack of marketing skills, receiving unfair prices from middlemen or collectors, and aging farmers. Many Thai farmers could not receive enough revenue to cover their production costs. Risks in agricultural e-commerce for farmers and SMEs can divided into six issues: production risks, marketing risks, financial risks, legislation and policy risks, technology risks, and labor risks. For production risks, unstable weather conditions such as drought or rainfall, lack of efficient equipment and machinery, and damage due to pests and disease could be source of these risks. Marketing risks are prominent issues among Thai farmers, resulted from price instability, lack of knowledge on product pricing, data analysis, and operation, high level of competitive among similar products, low product and service quality, unattractive packaging, and ability to access to the market (Coble et al. 2018, Fecke et al. 2018). Financial risks came from limited access to financial institutions, funding sources, high input costs, and lack of adequate cash or credit. Legislation and policy risks associated with e-commerce tax uncertainty and the harmful effect by the government policy, which was inconsistent and short term implementation. Challenges on regulation for e-commerce would delay an investment decision on both domestic and cross-broader e-commerce. Technology risks resulted from less trust in e-payment, slow adoption in agricultural e-commerce platforms among farmers and SMEs, and the lack of national pooled data sharing and accessibility. Labor risks related to lack of skilled labor in information technology (IT), management, and negotiation; as well as moving toward the aging society of farmers.

Following problems and risks in agricultural e-commerce for farmers and SMEs, the government digitalized farmers and SMEs through online agricultural markets. Currently, the government policies directly affected the development of e-commerce.

Challenges of e-commerce for agricultural products

Currently, the changes of technology and variety of digital platforms would enhance the farmer’s revenue and welfare. Moreover, the stakeholders in the agri-food chain would gain some benefits from providing fresher agricultural products to consumers, supporting directly to farmers, and expanding the market to both domestic and international markets (Fruhling and Digman 2000, Mueller 2001, Hennessy et al. 2016, Zapata et al. 2016). To shift tradition transaction to digital transaction in agricultural market, it is a long term process. In addition, the adoption of e-commerce on agricultural products are in an early stage, so several challenges are needed to be considered.

CONCLUSION

As digital platform has emerged, the e-commerce has applied to many industries. Online channel was slowly adapted to agricultural sector. Online agricultural markets create values for agri-food chain, support the use of digital platform to eliminate intermediaries, and help farmers sell their product at fair prices. In Thailand, B2C and C2C e-commerce platform played a major role in agricultural market. The value of Thailand’s e-commerce market was approximately $US 5,564.13 million in 2018. Major contribution to agricultural e-commerce came from SMEs where social commerce (i.e. Facebook and LINE) and e-marketplace were the top market channels for agricultural products. E-marketplace by the private sector has become increasingly dynamic. For the agricultural sector in Thailand, six market channels from farmers to end users were discussed with four e-commerce platform (social media, e-marketplace, e-retail, and e-fresh market). Increase in mobile connectivity has positively influenced the driving e-commerce in the agricultural sector. Even though some challenges to e-commerce for agricultural products have been improved (i.e. the digital infrastructure in the rural area), both current and new issues (i.e. long delivery time and complex handling fresh produce) need to be addressed. The logistical challenges of fresh produce and a small number of farmers’ adaption toward digital platform are significant issues. To succeed, agricultural e-commerce enterprises require scalable economy and sustainable business. The government should provide projects and funding to new farmers and SMEs to develop new business model for agricultural produce and promote the use of mobile internet and digital payment by end consumers. Moreover, creating the e-commerce ecosystem and building entrepreneurship environment would create a new opportunity and career to agricultural sectors.

REFERENCES

Canavari, M., Fritz, M., Hofstede, G.J., Matopoulos, A. and Vlachopoulou, M. 2010. The role of trust in the transition from traditional to electronic B2B relationships in agri-food chains. Computers and electronics in agriculture 70(2):321-327.

Carpio, C.E., Isengildina-Massa, O., Lamie, R.D. and Zapata, S.D. 2013. Does e-commerce help agricultural markets? The case of MarketMaker. Choices, 28(4), pp.1-7.

Coble, K.H., Mishra, A.K., Ferrell, S. and Griffin, T. 2018. Big data in agriculture: A challenge for the future. Applied Economic Perspectives and Policy, 40(1), pp.79-96.

Electronics Transaction Development Agency. 2018. National e-Commerce Strategy in Thailand, Office of Policy and Strategic Affairs, Electronic Transactions Development Agency, Ministry of Digital Economy and Society, Thailand. Available from https://www.etda.or.th/publishing-detail/national-e-commerce-strategy-in-thailand.html [Accessed 7 May 2019].

Electronics Transaction Development Agency. 2019a. The Value of E-Commerce Survey in Thailand 2018, Office of Policy and Strategic Affairs, Electronic Transactions Development Agency, Ministry of Digital Economy and Society, Thailand. Available from https://www.etda.or.th/publishing-detail/value-of-e-commerce-survey-in-thailand-2018.html [Accessed 4 June 2019].

Electronics Transaction Development Agency. 2019b. Thailand Internet User Profile 2018, Office of Policy and Strategic Affairs, Electronic Transactions Development Agency, Ministry of Digital Economy and Society, Thailand. Available from https://www.etda.or.th/publishing-detail/thailand-internet-user-profile-2018.html [Accessed 4 June 2019].

Euromonitor International 2018. Internet retailing in Thailand 2018. Available from https://www.euromonitor.com/internet-retailing-in-thailand/report [Accessed 4 May 2019].

Fecke, W., Danne, M. and Musshoff, O. 2018. E-commerce in agriculture–The case of crop protection product purchases in a discrete choice experiment. Computers and electronics in agriculture, 151, pp.126-135.

Fruhling, A.L. and Digman, L.A. 2000. The impact of electronic commerce on business-level strategies. Journal of Electronic Commerce Research, 1(1), p.13.

Hennessy, T., Läpple, D. and Moran, B. 2016. The digital divide in farming: a problem of access or engagement? Applied Economic Perspectives and Policy 38(3):474-491.

Mueller, R.A. 2000. Emergent E-commerce in Agriculture (No. 14). University of California, Agricultural Issues Center.

Mueller, R.A. 2001. E-commerce and entrepreneurship in agricultural markets. American Journal of Agricultural Economics, 83(5), pp.1243-1249.

NESDB. 2019. Gross Domestic Product Chain Volume Measures 1/2562, Office of the National Economic and Social Development Council (NESDB), Thailand. Available from https://www.nesdb.go.th/main.php?filename=QGDP_report [Accessed 5 April 2019].

OECD. 2019. Unpacking E-commerce: Business Models, Trends and Policies, Organization for Economic Co-Operation and Development (OECD) Publishing, Paris. Available from https://doi.org/10.1787/23561431-en [Accessed 25 June 2019].

OSMEP. 2018. Situation report of SMEs in 2017. The Office of SMEs Promotion (OSMEP), Thailand. Available from http://www.sme.go.th/th/download.php?modulekey=215&cid=0 [Accessed 25 June 2019].

World Bank. 2018. International LPI, Country score card: Thailand 2018. Available from https://lpi.worldbank.org/international/scorecard/radar/255/C/THA/2018#chartarea [Accessed 25 June 2019].

Zapata, S.D., Isengildina-Massa, O., Carpio, C.E. and Lamie, R.D. 2016. Does E-Commerce Help Farmers’ Markets? Measuring the Impact of MarketMaker. Journal of Food Distribution Research, 47(856-2016-58222), pp.1-18.

Date submitted: July 22, 2019

Reviewed, edited and uploaded: August 12, 2019

[1] Manufacturing industry consists of food products, beverages, textile, leather, paper, rubber, wood products, basic pharmaceutical products, primary metal products, non-metallic products (i.e. glass products, clay building materials, cement), and furniture.

[1] The definition of small enterprises (SE) and medium enterprise (ME) is categorized by the number of employees and the total value of fixed asset (excluding land) (OSMEP 2018).

[1] The exchange rate on 10 July 2019 is THB 31.01 = US$1. Source: Bank of Thailand (2019).

[2] The definition of business-to-business (B2B) is a type of commerce transaction existing between businesses in the private sector, in which the private sector means e-commerce operators registered as juristic persons and intending to do businesses between one another. The business consists of small and medium enterprises (SMEs) (an annual revenue is less than US$1.61 million) and large enterprises (an annual revenue is equal or more than US$1.61 million). The definition of business-to-consumer (B2C) is a type of commerce transaction existing between businesses in the private/public sector and the private sector, in which the private sector means e-Commerce operators registered as individual or juristic persons and intending to do businesses between one another. The definition of consumer-to-consumer (C2C) is a type of commerce transaction existing between individuals. The definition of business-to-consumer (B2G) is a type of commerce transaction existing between the private and public sectors under two approaches: e-market and e-bidding (ETDA 2019a).

[3] Note that the annual report by the Electronics Transaction Development Agency (ETDA) did not report the data on C2C platform separated from B2C platform.