ABSTRACT

Thailand is, presently, ranked sixth in the world in terms of rice production and second in terms of rice export. The market share is about 20 %. Besides being a staple food for the Thai people, rice is also very important to the Thai economy. It shared about 15% of agricultural gross domestic product (GDP) and ranked second after rubber in exporting value of agricultural products.

About half of the agricultural land of the country is devoted to rice growing and most of rice farmers are small famers. The average paddy planted area is only about 3 hectares per household. About 33 % of rice farmers are above 60 years old with the average age of 56 years.

the current agricultural policies of the Ministry of Agriculture and Cooperatives (MOAC) include establishing the rice restructuring plan in order to reduce the over rice production to match with the demand. The cost reduction and product quality improvement as well as value creation programs are emphasized. Niche market products such as organic rice, nutritious rice and geographical (GI) rice are also promoted. The area – based extension approach is adopted to implement the above policies. The government incentives provided include equipment, technology transfer, soft loans, direct payment and assistance in market linkages.

Keywords: Agricultural policies, restructuring plan, cost reduction, product quality improvement, value creation, niche market, organic rice, GI rice, area – based extension

INTRODUCTION

Thailand is still considered as an agricultural country even though the share of agricultural sector in the gross domestic product (GDP) has declined continuously. Presently, the agricultural sector contributes less than 10% to its national GDP l.However, majority of the people still live on farm in the rural areas and depend on agricultural activities for their source of livelihood. Agriculture provides food not only enough for domestic consumption but also has a surplus for export to earn a significant amount of foreign exchange for the country. Furthermore, most of the economic progress has been derived, directly or indirectly, from agricultural development. In the old days, for many Thai farmers, rice farming is a way of life for them. A small piece of land, whenever they have, most of them think first about growing rice for household consumption regardless of the prices they will receive. However, keeping rice for household consumption has been decreasing nowadays due to the change in harvesting practice from manual to combine machine which the farmers, generally, sell all their paddies immediately to the local assemblers right after harvest. Apart from being an important crop that has significant impact on the national economy, rice farming has also contributed much to the national culture. The royal ploughing ceremony is organized in May of every year. Due to the importance of rice and rice farmers, in 2009 the government has decided to designate the fifth of June of every year as the “National Rice and Rice Farmers Day”. This day was selected because in June 5, 1946 the late King Rama 8 together with the late King Rama 9 (then the brother of the King Rama 8) had visited the paddy field in Bangkhen district, Bangkok suburb and broadcasted rice seeds into the field. Furthermore, the rice farmers has always been recognized by the Thai people as “The Backbone of the Country”.

The Thai economy very much relies on its exports. The export earning constituted about 60 % of the total GDP. Agricultural exports share about 20 % of the total export value. Major agricultural exports in terms of value are rubber, rice, shrimp, processed fish, sugar and cassava, respectively. Many agricultural commodity exports are ranked first or very high on the list in terms of world market share.

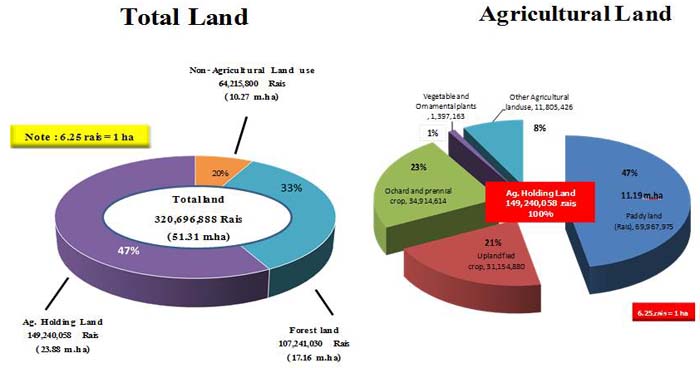

From the total land area of 320.7 million rais (51.3 mill. hectares), it can be categorized into 3 major groups as agricultural land which, in 2017 occupied about 23.9 million hectares or about 47 % of the total land area, the forest area covered about 17.2 million hectares or about 33 % and the rest are non – agricultural land which are used for housing, commercial and industrial purposes. For agricultural land, about 11.2 million hectares or about47 % of agricultural land are classified as paddy fields ).

In this paper, the relative importance of Thai rice to the country’s economy and to the world in terms of production and trade, Thai rice markets, characteristic of rice farmers and rice farming system will be presented. The government policies and activities implemented towards high value products will be also described.

Fig. 1. Land Use of Thailand 2017

Source: Office of Agricultural Economics (OAE)

RICE INDUSTRY IN THAILAND

Importance of Thai rice

In Thailand, rice is the most important crop in many aspects. It is a staple food for the Thai people and a major source of foreign exchange earning as well as a major source of employment. Rice production contributes about 15 % of its agricultural GDP which is the first in ranking among agricultural products. It ranked second after rubber in terms of export earnings.

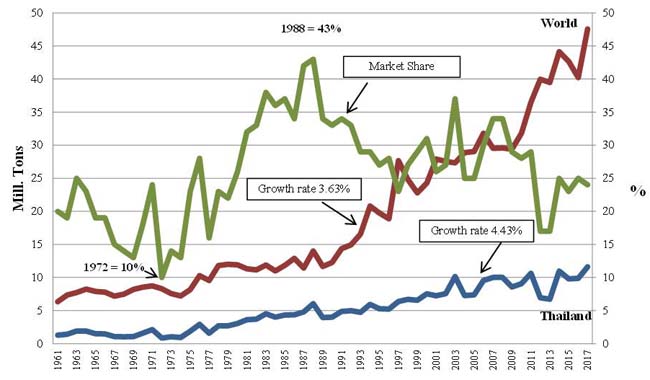

Thailand is currently ranked sixth in the world in rice production but constitutes only about 4 % of the world production. For export, Thailand is ranked second in rice export which have market share of about 24 % of the world rice trade. The world rice production and trade is shown in Table 1. However, for more than 30 years, Thailand used to consistently rank number one in rice export in the world until it lost its position to India and Vietnam in 2012. Over the last 50 years, the rice export from Thailand has increased from about 2 million tons to about 10 million tons with an average annual growth of about 4.4 %. During the same period, the world rice trade has increased from about 5 million tons to about 40 million tons with an average annual growth of about 3.6 %. However, the market share of Thai rice during this period has fluctuated from as low as 10 % to the highest point at more than 40 % (Fig. 2).

Table 1. World rice production, exports and imports, 2017

|

Country

|

Production

|

Country

|

Exports

|

Country

|

Imports

|

|

(Mill. Tons)

|

(%)

|

(Mill. Tons)

|

(%)

|

(Mill. Tons)

|

(%)

|

|

China

|

144.95

|

30

|

India

|

12.3

|

26

|

China

|

5.5

|

12

|

|

India

|

110.15

|

23

|

Thailand

|

11.614

|

24

|

Nigeria

|

2.5

|

5

|

|

Indonesia

|

36.86

|

8

|

Vietnam

|

6.488

|

14

|

EU

|

1.875

|

4

|

|

Bangladesh

|

34.58

|

7

|

Pakistan

|

3.6

|

8

|

Iran

|

1.6

|

3

|

|

Vietnam

|

27.4

|

6

|

USA

|

3.384

|

7

|

Saudi Arabia

|

1.4

|

3

|

|

Thailand

|

19.2

|

4

|

Myanmar

|

3.2

|

7

|

Ivory Coast

|

1.35

|

3

|

|

Myanmar

|

12.65

|

3

|

Cambodia

|

1.15

|

2

|

Philippines

|

1.1

|

2

|

|

Philippines

|

11.69

|

2

|

Uruguay

|

1

|

2

|

Iraq

|

1.07

|

2

|

|

Brazil

|

8.38

|

2

|

Brazil

|

0.594

|

1

|

Malaysia

|

1

|

2

|

|

USA

|

7.12

|

1

|

Argentina

|

0.392

|

1

|

Indonesia

|

0.3

|

1

|

|

Others

|

73.8

|

15

|

Others

|

3.827

|

8

|

Others

|

29.854

|

63

|

|

World

|

486.78

|

100

|

World

|

47.549

|

100

|

World

|

47.549

|

100

|

Source: World Markets & Trade, USDA, February 2018

Fig. 2. Quantity of World Rice and Thai Rice Export and Market Share, 1961 – 2017

Source: IRRI and Thai Rice Exporters Association

Thai rice markets

In 2017, Benin is the biggest importer of Thai rice , followed by China and the United States, respectively (Table 2). Most of the Thai rice exports were white rice followed by Hommali Rice (Jasmine or fragrant rice) and parboiled rice, respectively (Table 2). The top ten customers of Thai rice by type of rice are shown in Table 3 Table 4 and Table 5.

In general, Thai rice is considered as a good quality rice which can be justified by the average FOB prices of major exporting countries such as India and Vietnam. The annual average of FOB prices for 5% white rice between 2012 and 2017 for Thailand, India and Vietnam is shown in Table 6. The FOB prices of Thailand are above the fob prices of both India and Vietnam while the FOB prices of India are higher than the FOB prices of Vietnam.

Table 2. Quantity and value of Thai rice exports by countries of destination and type of rice, 2017

|

Country of destination

|

Quantity

|

Value

(Mill. Baht)

|

Type of rice

|

Quantity

|

Value

|

|

(Ton)

|

(%)

|

(Ton)

|

(%)

|

(Ton)

|

(%)

|

|

Benin

|

1,811,164

|

16

|

23,114

|

White Rice

|

5,050,047

|

42

|

62,766

|

32

|

|

China

|

1,199,737

|

10

|

19,352

|

Hommali Rice

|

2,299,262

|

19

|

51,237

|

26

|

|

USA

|

503,517

|

4

|

13,368

|

Parboiled Rice

|

3,373,184

|

28

|

44,629

|

23

|

|

Republic of South Africa

|

775,175

|

7

|

10,502

|

Glutinous Rice

|

514,740

|

4

|

8,956

|

5

|

|

Cameroon

|

744,508

|

6

|

9,121

|

Pathumthani Rice

|

378,965

|

3

|

6,399

|

3

|

|

Bangladesh

|

550,119

|

5

|

7,081

|

Others

|

12,105

|

0

|

515

|

0

|

|

Ivory Coast

|

492,911

|

4

|

6,290

|

Sub – Total

|

11,628,303

|

97

|

174,502

|

90

|

|

Others

|

5,551,172

|

48

|

85,675

|

Rice Products

|

311,926

|

3

|

18,867

|

10

|

|

Total

|

11,628,303

|

100

|

174,503

|

Total

|

11,940,232

|

100

|

193,370

|

100

|

|

(5,817 Mill. US$)

|

(6,446 US$)

|

Source: Office of Agricultural Economics

Table 3. Thai rice markets by countries of destination for white rice and parboiled rice, 2017

|

Country of

destination

|

White rice

|

Country of

destination

|

Parboiled rice

|

|

(Ton)

|

(Mill. Baht)

|

(Ton)

|

(Mill. Baht)

|

|

China

|

606,358

|

7,493

|

Benin

|

1,314,492

|

17,165

|

|

Benin

|

478,572

|

5,624

|

Republic of South Africa

|

736,666

|

9,888

|

|

Mozambique

|

444,343

|

5,367

|

Bangladesh

|

537,209

|

6,914

|

|

Cameroon

|

450,989

|

5,167

|

Cameroon

|

251,988

|

3,347

|

|

Angola

|

389,656

|

5,109

|

Yemen Republic

|

146,210

|

1,928

|

|

Japan

|

335,812

|

4,167

|

Soviet (Russian)

|

39,079

|

536

|

|

Philippines

|

278,485

|

3,451

|

Algeria

|

36,178

|

474

|

|

Malaysia

|

254,834

|

3,221

|

Niger

|

30,331

|

405

|

|

Kenya

|

170,777

|

2,176

|

United Arab Emirates

|

27,831

|

389

|

|

Iran

|

143,123

|

1,881

|

Spain

|

21,747

|

353

|

|

Others

|

1,497,097

|

19,111

|

Others

|

231,454

|

3,229

|

|

Total

|

5,050,047

|

62,766

|

Total

|

3,373,184

|

44,629

|

|

(5,817 Mill. US$)

|

(1,488 Mill. US$)

|

Source: Office of Agricultural Economics

Table 4. Thai rice markets by countries of destination for hommali rice (fragrant rice) and glutinous rice, 2017

|

Country of

destination

|

Hommali rice

(Fragrant rice)

|

Country of

destination

|

Glutinous rice

|

|

(Ton)

|

(Mill. Baht)

|

(Ton)

|

(Mill. Baht)

|

|

USA

|

457,234

|

12,224

|

China

|

249,566

|

4,040

|

|

China

|

301,822

|

7,109

|

Indonesia

|

102,775

|

1,719

|

|

Hong Kong

|

180,532

|

4,796

|

USA

|

19,244

|

547

|

|

Ivory Coast

|

266,890

|

3,594

|

Malaysia

|

17,256

|

326

|

|

Iran

|

120,313

|

2,463

|

Belgium

|

20,955

|

317

|

|

Canada

|

80,350

|

2,161

|

Vietnam

|

11,664

|

229

|

|

Singapore

|

66,666

|

1,943

|

Laos

|

11,650

|

202

|

|

Senegal

|

151,175

|

1,906

|

Japanese

|

8,674

|

177

|

|

Ghana

|

82,665

|

1,675

|

Philippines

|

9,130

|

162

|

|

Australia

|

44,725

|

1,255

|

Taiwan

|

8,512

|

161

|

|

Others

|

546,890

|

12,112

|

Others

|

55,314

|

1,077

|

|

Total

|

2,299,262

|

51,237

|

Total

|

514,740

|

8,956

|

|

(1,708 Mill. US$)

|

(298 Mill. US$)

|

Source: Office of Agricultural Economics

Table 5. Thai rice markets by countries of destination for Pathumthani rice (Fragrant rice) and Colored rice, 2017

|

Country of

destination

|

Pathumthani rice

(Fragrant rice)

|

Country of

destination

|

Colored rice

|

|

(Ton)

|

(Mill. Baht)

|

(Ton)

|

(Mill. Baht)

|

|

Ivory Coast

|

99,019

|

1,241

|

USA

|

2,309

|

116

|

|

China

|

41,372

|

678

|

Hong Kong

|

1,636

|

61

|

|

Singapore

|

25,716

|

593

|

Singapore

|

1,553

|

55

|

|

Hong Kong

|

25,059

|

502

|

Italy

|

1,386

|

54

|

|

Senegal

|

37,783

|

473

|

China

|

618

|

32

|

|

Ghana

|

21,589

|

412

|

Australia

|

496

|

29

|

|

USA

|

12,469

|

284

|

Canada

|

485

|

23

|

|

Israel

|

12,108

|

270

|

Netherlands

|

398

|

21

|

|

Netherlands

|

11,483

|

220

|

Malaysia

|

634

|

19

|

|

Taiwan

|

8,390

|

150

|

France

|

475

|

19

|

|

Others

|

83,978

|

1,576

|

Others

|

2,093

|

82

|

|

Total

|

378,965

|

6,399

|

Total

|

12,082

|

510

|

|

(213 Mill. US$)

|

(17 Mill. US$)

|

Source: Office of Agricultural Economics

Table 6. FOB Prices of rice of major exporting countries for white rice (5%), 2012 – 2017

|

Year

|

Thailand

(US$)

|

India

(US$)

|

Margin

(US$)

|

Vietnam

(US$)

|

Margin

(US$)

|

|

2012

|

575

|

434

|

141

|

432

|

143

|

|

2013

|

517

|

427

|

90

|

362

|

155

|

|

2014

|

423

|

420

|

3

|

415

|

8

|

|

2015

|

386

|

374

|

12

|

358

|

28

|

|

2016

|

397

|

368

|

29

|

359

|

38

|

|

2017

|

398

|

389

|

9

|

373

|

25

|

Source : Thai Rice Exporters Association

Thai rice farmers

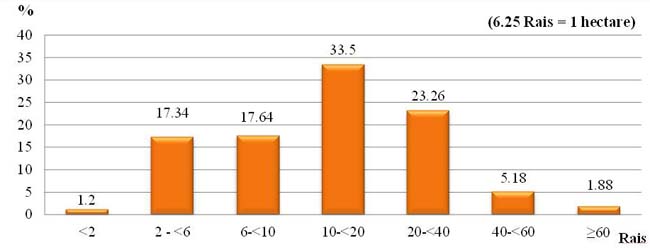

Although rice farming in Thailand is a major occupation and occupied about 50 % of the agricultural land, most farmers are still considered as small scale farmers in terms of farm size. About 70 % of the rice farmers have rice planted area less than 20 rais or 3.2 hectares

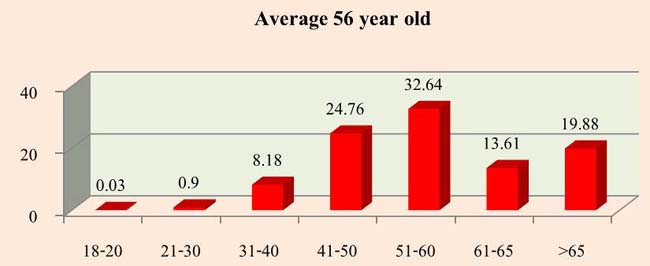

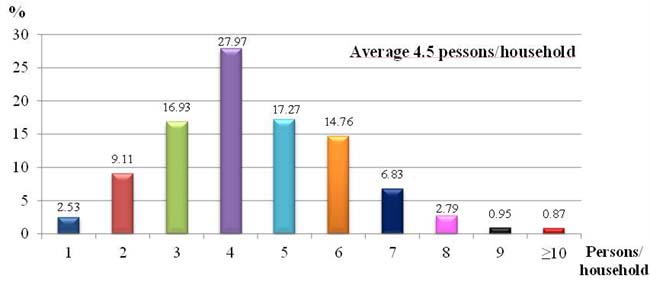

Regarding the age of the head of rice farms, it revealed that about 33 % of rice farmers are above 60 years with an average age of 56 years Most of rice farm households have 4 family members with theaverage members of 4.5 persons per household . As for the education level, about 80 % of the head of rice farms have finished their education up to primary school only.

Fig. 3. Percentage of farms by size of rice planted area, 2014/15

Source : Office of Agricultural Economics

Fig. 4. Age Distribution of rice farm household head, 2011/12

Source : Socio-economic Survey of Rice Farmers, 2011/12, Agricultural Research Development Agency

Fig. 5. Family members of rice farm households, 2011/12

Source : Socio-economic Survey of Rice Farmers, 2011/12, Agricultural Research Development Agency

Rice farming system in Thailand

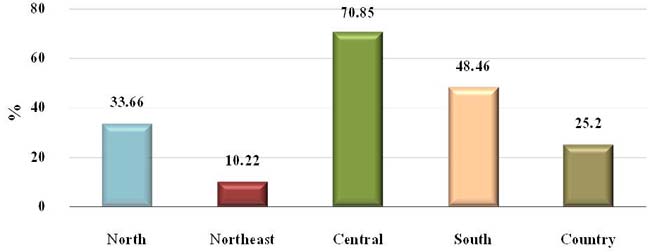

There are four rice ecosystems in Thailand. The rainfed lowland is the largest area which constitutes about 72 % of the total paddy field and mainly located in the northeastern region. The second ecosystem is the irrigated lowland with a share about 20 % of the total paddy area and mostly located in the central plain. The other two ecosystems are deep water and upland rice with a share about 5 % and 3 %, respectively. The irrigated planted areas are varied from one region to the others with the average of about 25 % of the total rice planted area in the country. The highest percentage is in the central region, which have irrigated areas of about 70 %. The lowest This is one of the reasons that make the national average of rice yield in Thailand to be very low. The other reason is that most of the varieties planted are the native variety which generally have very low yield. However, these varieties are very good in quality such as Hommali, RD15 and RD6 (Glutinous rice) which are all fragrant rice.

Fig. 6. Percentage of irrigated rice planted area by region, 2014/15

Source: Office of Agricultural Economics (OAE)

Typically, there are two main seasons for rice growing in the country, wet season rice and dry season rice. For the purpose of statistical data collection to avoid double counts, the definitions of wet and dry season rice as defined by OAE are given as follows:

Wet – season rice which is sometimes called major rice refers to the rice grown during the wet season which is May to October except in the eastern coast provinces of the southern region, namely, Nakhon Si Thammarat, Phatthalung, Songkhla, Pattani, Yala and Narathiwat where the wet – season rice is grown during 16 June to 28 February of the following year.

Dry – season rice which is sometimes called second rice refers to the rice grown duiring the dry season which is some time between November and April of the following year except in the above 6 provinces which the dry – season rice is grown during 1 March to 15 June. Most of the second rice areas are in the irrigated area in the central plain.

However, the actual rice season can be varied from year to year depending on the weather condition. In irrigated areas, there is no specific season and farmers may grow rice as many as 3 times a year or 5 times in 2 years.

Rice supply chain in Thailand

In general, rice trade in Thailand is a free market system with many buyers and sellers. However, during the 2011 – 2013 period the free market system has collapsed due to the change in government policy by adopting rice pledging scheme which offered very high mortgage prices compared to the market prices. Thus, most of the paddy produced are channeled to the government pledging scheme. The rice mills could not operate efficiently and many of them became storage of the rice stock of the government. The agricultural cooperatives could not collect the paddy from its numbers to carry out their business.

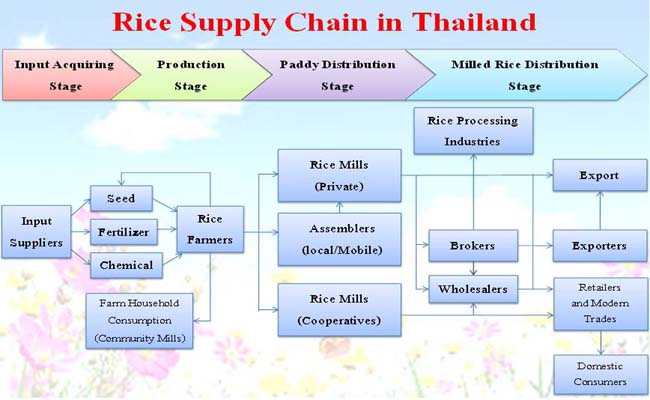

There are four major stages along the rice supply chain in Thailand which include input acquiring, production, paddy distribution and milled rice distribution. The important inputs used in rice production are seeds, fertilizers and chemicals (insecticides and herbicides).For seeds, most farmers obtained seeds from seed dealers in the local areas. However, some farmers use their own seeds produced by themselves on farms. The use of their own seeds which is now very limited due to the change in harvesting method from manual to combine machine. Community Rice Centers (CRC) which produced seeds for farmers by farmers are also another seed providers in the community. For fertilizers and chemicals, most farmers buy from local dealers which sometimes also give some technical advice and credit to their customers.

Right after harvest, farmers may sell their paddies to the local assemblers or sometimes mobile (ad hoc) assemblers which usually come from other provinces during the peak of the harvesting period. Some farmers may sell it directly to the rice mills in the nearby areas. This is because most of the rice farmers have no drying facilities and no storage. However, some famers may keep some of their paddies for household consumption and for seeds in the next season. The paddies that the farmers kept for household consumption will be milled by small rice mills in the village when it is needed.

After the paddy is milled, most of the millers sell their milled rice to rice exporters through rice brokers. Generally, the big buyers such as exporters and wholesalers will ask the broker to collect milled rice which specify the quantity and the quality (grade) of rice for them. Besides collecting rice, the brokers will also provide credit to buyers by advancing some or all of the amount of money required to buy rice from the millers. In return, brokers will receive a commission about 0.6 – 0.75 % from buyers for their services. For some millers, which have full facilities such as color sorter and packaging machines, they may sell rice directly to buyers such as wholesalers, exporters and oversea importers.

For the domestic market, the milled rice is usually distributed via the wholesalers who bought rice from rice millers and sell it to the retailers around the country and to the modern trade stores or supermarkets as a small rice pack (mainly 5 kg/pack). Some of the milled rice are sold to the rice processing industries for further processing activities to make food and non-food products and sell it in both domestic and oversea markets. However, the secondary or sophisticated rice products are still produced in limited amount compared to the primary products such as regular milled rice. The current rice supply chain in Thailand is shown in Fig. 7.

Fig. 7. Rice supply chain in Thailand

The market structure and flow of rice in Thailand is very dynamic because of the many changes in government policies such as change from income warrantee scheme to pledging scheme due to the change in political party which controlled the government administration. The paddy central markets are no longer in existence and the future market is not anymore active in the trading of rice.

CURRENT AGRICULTURAL POLICES OF MOAC

The current policies of the Ministry of Agricultural and Cooperatives (MOAC) that are related to the high value products development can be summarized as follows.

Production policies

1) Establish the restructuring plan in order to reduce the over production to match with the demand.

For rice crop, the existing growing areas are classified into two major zones, suitable areas and unsuitable areas. For suitable areas, improvement of efficiency of production and quality of the products will be emphasized. Moreover, the second rice have to be reduced and changed to other cash crops or green manure crops or left idle during the dry season. For unsuitable area, mixed farming or change to other activities will be promoted by providing the farmers with some incentives.

2) Reduce cost of production and improve quality of products.

The appropriate technologies will be transferred to the rice farmers extensively. The good agricultural practices (GAPs) for rice farming are encouraged and certified.

3) Promote value-added products.

The training courses and equipment and other incentives will be provided. The government supports include packaging equipment and branding development.

Marketing policies

- The market driven strategy will be emphasized.

Production target will be set up to match with the demand before planting time.

- Promote business matching and e – market platforms establishment.

These activities include establishing farmers’ markets in the rural communities, facilitating in price negotiation with the local millers as well as organizing the training courses on how to develop e-market platforms.

- Promote niche market products.

Rice for niche markets include organic rice, geographical indication (GI) rice, nutritious rice, colored rice, native varieties rice and rice for food processing industry.

Targets

- All products have to be safety products in 2022.

- 60 % of all products are organic products in 2027.

Approach

- The area – based extension approach will be adopted to implement the above policies.

The paddy fields of each small farmer in the neighborhood are consolidated to make it look similar to a large farm while the ownership remains unchanged. The objectives of the area-based extension system are to make the promoting target areas to achieve economy of scale in order to increase the bargaining power of farmers. Thus, the cost of production for each small farmer in the area will be reduced while the price received by the farmers will be increased. In doing so, it is also very convenient for government officials to transfer site specific technology to the farmers in the areas and assist them in linking with the buyers. In addition, the area – based approach will facilitate the integration of work among different departments to further improve the efficiency and productivity of rice farming.The farmers’ organization for farmers in the particular large farm will be set up, it’s not yet existing, and the farm manager will be appointed to operate each big farm.

- Local leaning center for each commodity will be established and strengthened.

The best practice farm in each district will be selected to be a local learning center for farmers in each commodity which include rice crop.

CONCLUSION AND RECOMMENDATION

Thai rice is very important nationally and globally. It is a major source of export earning for the country and a major source of rice supply to feed the world. However, Thai rice farmers are still very poor compared to other occupations in the agricultural sector. Most of them are small farmers and are very old. It is very clear that the government wanted to promote high value products for export instead of primary products such as milled rice as usual to avoid competition from other exporting countries. In practice, however, the action taken by the government to further development and enhancing the secondary products business is very limited especially for small farmers and startup business. More researches and investments by the government in the field of value – added product development are needed. Furthermore, the farmers’ organizations and its network should also be established and strengthened especially in developing and operating high value products business. Agro – tourism should also be promoted for people as consumers to visit rice farms and observe rice cultural practices and value – added activities under the concept “Know producer, Know quality”.

|

(Submitted as a paper for the International Seminar on “Promoting Rice Farmers’ Market through value-adding Activities”, June 6-7, 2018, Kasetsart University, Thailand)

|

Thailand’s Rice Industry and Current Policies towards High Value Rice Products

ABSTRACT

Thailand is, presently, ranked sixth in the world in terms of rice production and second in terms of rice export. The market share is about 20 %. Besides being a staple food for the Thai people, rice is also very important to the Thai economy. It shared about 15% of agricultural gross domestic product (GDP) and ranked second after rubber in exporting value of agricultural products.

About half of the agricultural land of the country is devoted to rice growing and most of rice farmers are small famers. The average paddy planted area is only about 3 hectares per household. About 33 % of rice farmers are above 60 years old with the average age of 56 years.

the current agricultural policies of the Ministry of Agriculture and Cooperatives (MOAC) include establishing the rice restructuring plan in order to reduce the over rice production to match with the demand. The cost reduction and product quality improvement as well as value creation programs are emphasized. Niche market products such as organic rice, nutritious rice and geographical (GI) rice are also promoted. The area – based extension approach is adopted to implement the above policies. The government incentives provided include equipment, technology transfer, soft loans, direct payment and assistance in market linkages.

Keywords: Agricultural policies, restructuring plan, cost reduction, product quality improvement, value creation, niche market, organic rice, GI rice, area – based extension

INTRODUCTION

Thailand is still considered as an agricultural country even though the share of agricultural sector in the gross domestic product (GDP) has declined continuously. Presently, the agricultural sector contributes less than 10% to its national GDP l.However, majority of the people still live on farm in the rural areas and depend on agricultural activities for their source of livelihood. Agriculture provides food not only enough for domestic consumption but also has a surplus for export to earn a significant amount of foreign exchange for the country. Furthermore, most of the economic progress has been derived, directly or indirectly, from agricultural development. In the old days, for many Thai farmers, rice farming is a way of life for them. A small piece of land, whenever they have, most of them think first about growing rice for household consumption regardless of the prices they will receive. However, keeping rice for household consumption has been decreasing nowadays due to the change in harvesting practice from manual to combine machine which the farmers, generally, sell all their paddies immediately to the local assemblers right after harvest. Apart from being an important crop that has significant impact on the national economy, rice farming has also contributed much to the national culture. The royal ploughing ceremony is organized in May of every year. Due to the importance of rice and rice farmers, in 2009 the government has decided to designate the fifth of June of every year as the “National Rice and Rice Farmers Day”. This day was selected because in June 5, 1946 the late King Rama 8 together with the late King Rama 9 (then the brother of the King Rama 8) had visited the paddy field in Bangkhen district, Bangkok suburb and broadcasted rice seeds into the field. Furthermore, the rice farmers has always been recognized by the Thai people as “The Backbone of the Country”.

The Thai economy very much relies on its exports. The export earning constituted about 60 % of the total GDP. Agricultural exports share about 20 % of the total export value. Major agricultural exports in terms of value are rubber, rice, shrimp, processed fish, sugar and cassava, respectively. Many agricultural commodity exports are ranked first or very high on the list in terms of world market share.

From the total land area of 320.7 million rais (51.3 mill. hectares), it can be categorized into 3 major groups as agricultural land which, in 2017 occupied about 23.9 million hectares or about 47 % of the total land area, the forest area covered about 17.2 million hectares or about 33 % and the rest are non – agricultural land which are used for housing, commercial and industrial purposes. For agricultural land, about 11.2 million hectares or about47 % of agricultural land are classified as paddy fields ).

In this paper, the relative importance of Thai rice to the country’s economy and to the world in terms of production and trade, Thai rice markets, characteristic of rice farmers and rice farming system will be presented. The government policies and activities implemented towards high value products will be also described.

Fig. 1. Land Use of Thailand 2017

Source: Office of Agricultural Economics (OAE)

RICE INDUSTRY IN THAILAND

Importance of Thai rice

In Thailand, rice is the most important crop in many aspects. It is a staple food for the Thai people and a major source of foreign exchange earning as well as a major source of employment. Rice production contributes about 15 % of its agricultural GDP which is the first in ranking among agricultural products. It ranked second after rubber in terms of export earnings.

Thailand is currently ranked sixth in the world in rice production but constitutes only about 4 % of the world production. For export, Thailand is ranked second in rice export which have market share of about 24 % of the world rice trade. The world rice production and trade is shown in Table 1. However, for more than 30 years, Thailand used to consistently rank number one in rice export in the world until it lost its position to India and Vietnam in 2012. Over the last 50 years, the rice export from Thailand has increased from about 2 million tons to about 10 million tons with an average annual growth of about 4.4 %. During the same period, the world rice trade has increased from about 5 million tons to about 40 million tons with an average annual growth of about 3.6 %. However, the market share of Thai rice during this period has fluctuated from as low as 10 % to the highest point at more than 40 % (Fig. 2).

Table 1. World rice production, exports and imports, 2017

Country

Production

Country

Exports

Country

Imports

(Mill. Tons)

(%)

(Mill. Tons)

(%)

(Mill. Tons)

(%)

China

144.95

30

India

12.3

26

China

5.5

12

India

110.15

23

Thailand

11.614

24

Nigeria

2.5

5

Indonesia

36.86

8

Vietnam

6.488

14

EU

1.875

4

Bangladesh

34.58

7

Pakistan

3.6

8

Iran

1.6

3

Vietnam

27.4

6

USA

3.384

7

Saudi Arabia

1.4

3

Thailand

19.2

4

Myanmar

3.2

7

Ivory Coast

1.35

3

Myanmar

12.65

3

Cambodia

1.15

2

Philippines

1.1

2

Philippines

11.69

2

Uruguay

1

2

Iraq

1.07

2

Brazil

8.38

2

Brazil

0.594

1

Malaysia

1

2

USA

7.12

1

Argentina

0.392

1

Indonesia

0.3

1

Others

73.8

15

Others

3.827

8

Others

29.854

63

World

486.78

100

World

47.549

100

World

47.549

100

Source: World Markets & Trade, USDA, February 2018

Fig. 2. Quantity of World Rice and Thai Rice Export and Market Share, 1961 – 2017

Source: IRRI and Thai Rice Exporters Association

Thai rice markets

In 2017, Benin is the biggest importer of Thai rice , followed by China and the United States, respectively (Table 2). Most of the Thai rice exports were white rice followed by Hommali Rice (Jasmine or fragrant rice) and parboiled rice, respectively (Table 2). The top ten customers of Thai rice by type of rice are shown in Table 3 Table 4 and Table 5.

In general, Thai rice is considered as a good quality rice which can be justified by the average FOB prices of major exporting countries such as India and Vietnam. The annual average of FOB prices for 5% white rice between 2012 and 2017 for Thailand, India and Vietnam is shown in Table 6. The FOB prices of Thailand are above the fob prices of both India and Vietnam while the FOB prices of India are higher than the FOB prices of Vietnam.

Table 2. Quantity and value of Thai rice exports by countries of destination and type of rice, 2017

Country of destination

Quantity

Value

(Mill. Baht)

Type of rice

Quantity

Value

(Ton)

(%)

(Ton)

(%)

(Ton)

(%)

Benin

1,811,164

16

23,114

White Rice

5,050,047

42

62,766

32

China

1,199,737

10

19,352

Hommali Rice

2,299,262

19

51,237

26

USA

503,517

4

13,368

Parboiled Rice

3,373,184

28

44,629

23

Republic of South Africa

775,175

7

10,502

Glutinous Rice

514,740

4

8,956

5

Cameroon

744,508

6

9,121

Pathumthani Rice

378,965

3

6,399

3

Bangladesh

550,119

5

7,081

Others

12,105

0

515

0

Ivory Coast

492,911

4

6,290

Sub – Total

11,628,303

97

174,502

90

Others

5,551,172

48

85,675

Rice Products

311,926

3

18,867

10

Total

11,628,303

100

174,503

Total

11,940,232

100

193,370

100

(5,817 Mill. US$)

(6,446 US$)

Source: Office of Agricultural Economics

Table 3. Thai rice markets by countries of destination for white rice and parboiled rice, 2017

Country of

destination

White rice

Country of

destination

Parboiled rice

(Ton)

(Mill. Baht)

(Ton)

(Mill. Baht)

China

606,358

7,493

Benin

1,314,492

17,165

Benin

478,572

5,624

Republic of South Africa

736,666

9,888

Mozambique

444,343

5,367

Bangladesh

537,209

6,914

Cameroon

450,989

5,167

Cameroon

251,988

3,347

Angola

389,656

5,109

Yemen Republic

146,210

1,928

Japan

335,812

4,167

Soviet (Russian)

39,079

536

Philippines

278,485

3,451

Algeria

36,178

474

Malaysia

254,834

3,221

Niger

30,331

405

Kenya

170,777

2,176

United Arab Emirates

27,831

389

Iran

143,123

1,881

Spain

21,747

353

Others

1,497,097

19,111

Others

231,454

3,229

Total

5,050,047

62,766

Total

3,373,184

44,629

(5,817 Mill. US$)

(1,488 Mill. US$)

Source: Office of Agricultural Economics

Table 4. Thai rice markets by countries of destination for hommali rice (fragrant rice) and glutinous rice, 2017

Country of

destination

Hommali rice

(Fragrant rice)

Country of

destination

Glutinous rice

(Ton)

(Mill. Baht)

(Ton)

(Mill. Baht)

USA

457,234

12,224

China

249,566

4,040

China

301,822

7,109

Indonesia

102,775

1,719

Hong Kong

180,532

4,796

USA

19,244

547

Ivory Coast

266,890

3,594

Malaysia

17,256

326

Iran

120,313

2,463

Belgium

20,955

317

Canada

80,350

2,161

Vietnam

11,664

229

Singapore

66,666

1,943

Laos

11,650

202

Senegal

151,175

1,906

Japanese

8,674

177

Ghana

82,665

1,675

Philippines

9,130

162

Australia

44,725

1,255

Taiwan

8,512

161

Others

546,890

12,112

Others

55,314

1,077

Total

2,299,262

51,237

Total

514,740

8,956

(1,708 Mill. US$)

(298 Mill. US$)

Source: Office of Agricultural Economics

Table 5. Thai rice markets by countries of destination for Pathumthani rice (Fragrant rice) and Colored rice, 2017

Country of

destination

Pathumthani rice

(Fragrant rice)

Country of

destination

Colored rice

(Ton)

(Mill. Baht)

(Ton)

(Mill. Baht)

Ivory Coast

99,019

1,241

USA

2,309

116

China

41,372

678

Hong Kong

1,636

61

Singapore

25,716

593

Singapore

1,553

55

Hong Kong

25,059

502

Italy

1,386

54

Senegal

37,783

473

China

618

32

Ghana

21,589

412

Australia

496

29

USA

12,469

284

Canada

485

23

Israel

12,108

270

Netherlands

398

21

Netherlands

11,483

220

Malaysia

634

19

Taiwan

8,390

150

France

475

19

Others

83,978

1,576

Others

2,093

82

Total

378,965

6,399

Total

12,082

510

(213 Mill. US$)

(17 Mill. US$)

Source: Office of Agricultural Economics

Table 6. FOB Prices of rice of major exporting countries for white rice (5%), 2012 – 2017

Year

Thailand

(US$)

India

(US$)

Margin

(US$)

Vietnam

(US$)

Margin

(US$)

2012

575

434

141

432

143

2013

517

427

90

362

155

2014

423

420

3

415

8

2015

386

374

12

358

28

2016

397

368

29

359

38

2017

398

389

9

373

25

Source : Thai Rice Exporters Association

Thai rice farmers

Although rice farming in Thailand is a major occupation and occupied about 50 % of the agricultural land, most farmers are still considered as small scale farmers in terms of farm size. About 70 % of the rice farmers have rice planted area less than 20 rais or 3.2 hectares

Regarding the age of the head of rice farms, it revealed that about 33 % of rice farmers are above 60 years with an average age of 56 years Most of rice farm households have 4 family members with theaverage members of 4.5 persons per household . As for the education level, about 80 % of the head of rice farms have finished their education up to primary school only.

Fig. 3. Percentage of farms by size of rice planted area, 2014/15

Source : Office of Agricultural Economics

Fig. 4. Age Distribution of rice farm household head, 2011/12

Source : Socio-economic Survey of Rice Farmers, 2011/12, Agricultural Research Development Agency

Fig. 5. Family members of rice farm households, 2011/12

Source : Socio-economic Survey of Rice Farmers, 2011/12, Agricultural Research Development Agency

Rice farming system in Thailand

There are four rice ecosystems in Thailand. The rainfed lowland is the largest area which constitutes about 72 % of the total paddy field and mainly located in the northeastern region. The second ecosystem is the irrigated lowland with a share about 20 % of the total paddy area and mostly located in the central plain. The other two ecosystems are deep water and upland rice with a share about 5 % and 3 %, respectively. The irrigated planted areas are varied from one region to the others with the average of about 25 % of the total rice planted area in the country. The highest percentage is in the central region, which have irrigated areas of about 70 %. The lowest This is one of the reasons that make the national average of rice yield in Thailand to be very low. The other reason is that most of the varieties planted are the native variety which generally have very low yield. However, these varieties are very good in quality such as Hommali, RD15 and RD6 (Glutinous rice) which are all fragrant rice.

Fig. 6. Percentage of irrigated rice planted area by region, 2014/15

Source: Office of Agricultural Economics (OAE)

Typically, there are two main seasons for rice growing in the country, wet season rice and dry season rice. For the purpose of statistical data collection to avoid double counts, the definitions of wet and dry season rice as defined by OAE are given as follows:

Wet – season rice which is sometimes called major rice refers to the rice grown during the wet season which is May to October except in the eastern coast provinces of the southern region, namely, Nakhon Si Thammarat, Phatthalung, Songkhla, Pattani, Yala and Narathiwat where the wet – season rice is grown during 16 June to 28 February of the following year.

Dry – season rice which is sometimes called second rice refers to the rice grown duiring the dry season which is some time between November and April of the following year except in the above 6 provinces which the dry – season rice is grown during 1 March to 15 June. Most of the second rice areas are in the irrigated area in the central plain.

However, the actual rice season can be varied from year to year depending on the weather condition. In irrigated areas, there is no specific season and farmers may grow rice as many as 3 times a year or 5 times in 2 years.

Rice supply chain in Thailand

In general, rice trade in Thailand is a free market system with many buyers and sellers. However, during the 2011 – 2013 period the free market system has collapsed due to the change in government policy by adopting rice pledging scheme which offered very high mortgage prices compared to the market prices. Thus, most of the paddy produced are channeled to the government pledging scheme. The rice mills could not operate efficiently and many of them became storage of the rice stock of the government. The agricultural cooperatives could not collect the paddy from its numbers to carry out their business.

There are four major stages along the rice supply chain in Thailand which include input acquiring, production, paddy distribution and milled rice distribution. The important inputs used in rice production are seeds, fertilizers and chemicals (insecticides and herbicides).For seeds, most farmers obtained seeds from seed dealers in the local areas. However, some farmers use their own seeds produced by themselves on farms. The use of their own seeds which is now very limited due to the change in harvesting method from manual to combine machine. Community Rice Centers (CRC) which produced seeds for farmers by farmers are also another seed providers in the community. For fertilizers and chemicals, most farmers buy from local dealers which sometimes also give some technical advice and credit to their customers.

Right after harvest, farmers may sell their paddies to the local assemblers or sometimes mobile (ad hoc) assemblers which usually come from other provinces during the peak of the harvesting period. Some farmers may sell it directly to the rice mills in the nearby areas. This is because most of the rice farmers have no drying facilities and no storage. However, some famers may keep some of their paddies for household consumption and for seeds in the next season. The paddies that the farmers kept for household consumption will be milled by small rice mills in the village when it is needed.

After the paddy is milled, most of the millers sell their milled rice to rice exporters through rice brokers. Generally, the big buyers such as exporters and wholesalers will ask the broker to collect milled rice which specify the quantity and the quality (grade) of rice for them. Besides collecting rice, the brokers will also provide credit to buyers by advancing some or all of the amount of money required to buy rice from the millers. In return, brokers will receive a commission about 0.6 – 0.75 % from buyers for their services. For some millers, which have full facilities such as color sorter and packaging machines, they may sell rice directly to buyers such as wholesalers, exporters and oversea importers.

For the domestic market, the milled rice is usually distributed via the wholesalers who bought rice from rice millers and sell it to the retailers around the country and to the modern trade stores or supermarkets as a small rice pack (mainly 5 kg/pack). Some of the milled rice are sold to the rice processing industries for further processing activities to make food and non-food products and sell it in both domestic and oversea markets. However, the secondary or sophisticated rice products are still produced in limited amount compared to the primary products such as regular milled rice. The current rice supply chain in Thailand is shown in Fig. 7.

Fig. 7. Rice supply chain in Thailand

The market structure and flow of rice in Thailand is very dynamic because of the many changes in government policies such as change from income warrantee scheme to pledging scheme due to the change in political party which controlled the government administration. The paddy central markets are no longer in existence and the future market is not anymore active in the trading of rice.

CURRENT AGRICULTURAL POLICES OF MOAC

The current policies of the Ministry of Agricultural and Cooperatives (MOAC) that are related to the high value products development can be summarized as follows.

Production policies

1) Establish the restructuring plan in order to reduce the over production to match with the demand.

For rice crop, the existing growing areas are classified into two major zones, suitable areas and unsuitable areas. For suitable areas, improvement of efficiency of production and quality of the products will be emphasized. Moreover, the second rice have to be reduced and changed to other cash crops or green manure crops or left idle during the dry season. For unsuitable area, mixed farming or change to other activities will be promoted by providing the farmers with some incentives.

2) Reduce cost of production and improve quality of products.

The appropriate technologies will be transferred to the rice farmers extensively. The good agricultural practices (GAPs) for rice farming are encouraged and certified.

3) Promote value-added products.

The training courses and equipment and other incentives will be provided. The government supports include packaging equipment and branding development.

Marketing policies

Production target will be set up to match with the demand before planting time.

These activities include establishing farmers’ markets in the rural communities, facilitating in price negotiation with the local millers as well as organizing the training courses on how to develop e-market platforms.

Rice for niche markets include organic rice, geographical indication (GI) rice, nutritious rice, colored rice, native varieties rice and rice for food processing industry.

Targets

Approach

The paddy fields of each small farmer in the neighborhood are consolidated to make it look similar to a large farm while the ownership remains unchanged. The objectives of the area-based extension system are to make the promoting target areas to achieve economy of scale in order to increase the bargaining power of farmers. Thus, the cost of production for each small farmer in the area will be reduced while the price received by the farmers will be increased. In doing so, it is also very convenient for government officials to transfer site specific technology to the farmers in the areas and assist them in linking with the buyers. In addition, the area – based approach will facilitate the integration of work among different departments to further improve the efficiency and productivity of rice farming.The farmers’ organization for farmers in the particular large farm will be set up, it’s not yet existing, and the farm manager will be appointed to operate each big farm.

The best practice farm in each district will be selected to be a local learning center for farmers in each commodity which include rice crop.

CONCLUSION AND RECOMMENDATION

Thai rice is very important nationally and globally. It is a major source of export earning for the country and a major source of rice supply to feed the world. However, Thai rice farmers are still very poor compared to other occupations in the agricultural sector. Most of them are small farmers and are very old. It is very clear that the government wanted to promote high value products for export instead of primary products such as milled rice as usual to avoid competition from other exporting countries. In practice, however, the action taken by the government to further development and enhancing the secondary products business is very limited especially for small farmers and startup business. More researches and investments by the government in the field of value – added product development are needed. Furthermore, the farmers’ organizations and its network should also be established and strengthened especially in developing and operating high value products business. Agro – tourism should also be promoted for people as consumers to visit rice farms and observe rice cultural practices and value – added activities under the concept “Know producer, Know quality”.

(Submitted as a paper for the International Seminar on “Promoting Rice Farmers’ Market through value-adding Activities”, June 6-7, 2018, Kasetsart University, Thailand)