ABSTRACT

This Paper underscores the significant role of government in the “Implementation and Enhancement of the Crop Insurance Program in the Philippines”.

From the perspective of the author, influenced by her readings and insights gained from various fora attended, the implementation and enhancement of the above cited program, is attributed to the following: (i) policy formulation and legislation; (ii) enabling policy environment; (iii) policy budget; and (iv) partnership. This paper also attempts to present the various fully subsidized rice insurance programs implemented by the Philippine Crop Insurance Corporation (PCIC), the rationale and implementing guidelines of each.

Like any program of national significance, the implementation of the above-program is not a stand-alone performance and responsibility of the Philippine Crop Insurance Corporation (PCIC) as the implementing agency, rather, it is the product of the interplay among legislators, implementers and partners and government institutions by way of integrating, synchronizing and mobilizing their actions, strategies and resources towards a common goal: building resilience in rice production and attaining Food Self Sufficiency in the country.

This paper also finds the government budget support through subsidies and appropriation as the key factor to the sustained implementation of an Agricultural Insurance Program in general and Crop Insurance Program in particular.

Keywords: climate change, academe, technocrats, global phenomena, guarantee fund, stabilize, mobilize, General Appropriation Act, fluctuations, mitigate, mechanism, innovative, government natural disaster, enhancement, policy legislation, policy environment, policy budget, partnership, legislators, implementers, government institutions, subsidies, synchronizing, mobilizing, strategies, resources, appropriation, resilience, sustained, key, collateral, investment, weather index-based, premium, weather adverse, mandate, capitalization, mainstream, vulnerable, subsistence, trigger, breach, multi-risk, operating policies, operating system procedure.

______________________________________

1Country Paper presented during the International Seminar on “Implementing and Improving Crop Natural Disaster Insurance Program” on June 13-17, 2016, Jeonju, Korea. Organized by the Food and Fertilizer Technology Center (FFTC) for the Asia and Pacific Region and the Rural Development Administration (RDA).

2Department Manager, Business Development and Marketing Department, Philippine Crop Insurance Corporation (PCIC) and Technical Focal Person UNDP-GEF-PCIC WIBI Mindanao Project: Scaling–up Risk Transfer Mechanisms for Climate Vulnerable Agriculture-based Communities in Mindanao. Email: pagaddu.rodelia@yahoo.com

INTRODUCTION

The Philippines is an archipelago nestled between a part of the Philippine Sea and West Pacific Sea located along the edge of the Pacific “Ring of Fire”. Inherent to its location, the Philippines has one of the highest exposures to natural hazards in the world.

A recent United Nations report identified the Philippines as the third most at risk to climate change events. According to another report released by environmental organization, German Watch- the Global Climate Risk Index 2015, which lists the most affected countries by weather related disturbances, like storms, floods and heat waves, based on the 2013 events, the Philippines is the top most vulnerable.

As an agricultural country, two-thirds of its population is directly or indirectly exposed to the impacts of climate change events. The country’s agricultural sector, composed of the rural poor is the most likely affected not only because its productivity and performance is dependent on weather, sustainability of water and remaining biological resources, but also because a significant portion of its population depends on it for food and livelihood.

In recent years, the world is a witness to the tremendous losses and damages wrought by extreme unpredictable weather conditions with the farmers, fishers and their children, prey to these unfortunate events of devastation, trapping them into the tunnel of poverty.

The above scenario must not be left unattended. Myrdal, Nobel Laureate in Economics attested, “it is in the agricultural sector that the battle for long- term economic development will be won or lost"3. Furthermore, if development is to take place and become self-sustaining, it will have to start in the rural areas in general and the agriculture sector in particular.

It is therefore in the above context that government and its instrumentalities consider as imperative today, the adoption of risks management schemes to spell the difference between a stagnated and a growing agri-based economy by building resilience in the country’s agricultural sector.

METHODOLOGY

To be able to attain the objectives of this study, the researcher employed the descriptive design. Analyses of various documents containing information on the Crop Insurance Program were undertaken. Primary and secondary data analyses were also carried out on the thirty five (35) years operational results of PCIC.

SCOPE AND LIMITATION

The term crop as used in this paper shall refer to “rice” only, in consideration of rice as the top staple crop of the Philippines and the only crop initially covered in the Crop Insurance Program.

______________________________________

3 Todaro, M. 1989. Economic Development in the Third World, New York. Pitun Publishing, Inc.

Development of the Crop Insurance Program in the Philippines

Climate change and variabilities is an increasing global phenomena getting the attention and concerned action among affected communities, policy legislators, program implementers, development technocrats, government and non-government sectors, academe and private counterparts the world over.

For its part, the Philippines, three decades and seven years ago, long before the global call on climate change, have included in its development framework the institution of a Crop Insurance System through the establishment of the Philippine Crop Insurance Corporation (PCIC).

Establishment of the Crop Insurance in the Philippines took off from the Agricultural Guarantee Fund (AGF) operationalized as an integral component of the Agrarian Reform Program implemented in 1972 which was intended to uplift the economic life of the farmer, through land and income distribution.

The Land Bank of the Philippines (LBP) administered the AGF to provide guarantee cover of up to 85% of the loan extended to small farmers. This guarantee scheme reinforced the supply of credit in the countryside, but failed to consider the demand side.

Guarantee mechanism only restructured the defaulted loan and did not grant a second loan to the affected farmer until the loan had been fully paid, thus, rendering the farmer borrower unproductive because of his failure to replant leading to perpetual indebtedness.

Cognizant of the weakness of the AGF scheme, the LBP as administrator, took the initiative to find ways and means to fill the gap by studying the feasibility of a crop insurance scheme that would insulate affected farmers from the vicious cycle of borrowing in order to plant, planting to be able to pay debt, and then borrow again to cover up losses and debts.

The study concluded that an all-risks crop insurance was feasible and was submitted to LBP Board of Directors who recommended to the President of the Philippines the creation and establishment of a crop insurance system. The committee reported the importance of implementing a crop insurance scheme as follows:

- Provide relief to rice producers from the heavy burden and loss caused by natural disasters and pests and diseases;

- Stabilizes the finances of lending institutions;

- Enhances farmers’ access to credit; and

- Serves as effective instruments for mobilizing funds from the farming community and trigger efforts to bring about self- sufficiency in staple food and intensified production initiatives.

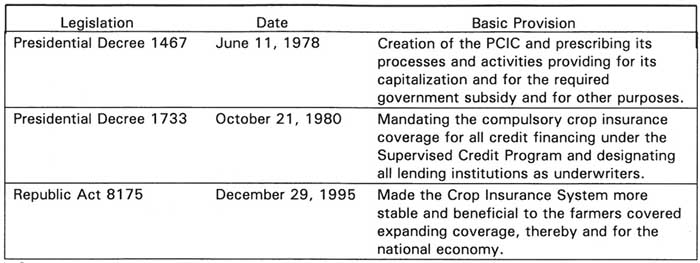

Creation of the PCIC

On June 11, 1978, the President of the Philippines, then Ferdinand E. Marcos, promulgated Presidential Decree (PD) 1467 creating the PCIC as the implementing agency of the country’s Crop Insurance Program (CIP).After the promulgation of the law, further studies were undertaken to operationalize the CIP by drawing up operating policies and operating systems and procedures.

On May 07, 1981, the CIP was launched. It was initially financed by the AGF which was transferred to the PCIC as part of the governments contribution to the PCIC Fund, thus, the funds provided to PCIC came from agrarian reform credit.

In order to make PCIC more responsive, the charter was amended by Presidential Decree 1733 on October 21, 1980. The law mandated that Crop Insurance be made compulsory for all lending institutions granting production loans for rice under the supervised credit programs of the government and the same shall act as PCIC underwriters. The law also provided for sanction for all lending institutions who did not comply.

Letter of Instruction No. 1242 was also signed and mandated PCIC to administer a Trust Fund amounting to $9.622 million to be given in tranches for three years to pay the claims of the Philippine National Bank and rural banks which participated in the Masagana 99 credit up to 85% program.

On December 29, 1995, Republic Act (RA) 1875was signed into law further amending PD 1467 to include provisions intended to make the Crop Insurance Program more stable and beneficial to the farmers. The following improvements are enumerated below:

- PCIC insurance operation was expanded to provide protection not only to crops but also non-crop agricultural assets and other areas of agriculture.

- The insurance capacity of PCIC was expanded as its capitalization was increased from $16.036 million to $42.762 million;

- The insurance coverage was expanded to include additional 20% of the cost of production inputs;

- Assures prompt payment of claims by considering claims completely documented and not acted upon within sixty (60) days from date of submission deemed approved;

- Provision of subsidies by the government to the subsistence farmers to bring the benefits of crop insurance within the reach of the farmers;

- Inclusion of three (3) farmer representatives in the PCIC Board of Directors to represent the farmers;

- Provision of a State Reserve Fund for catastrophic losses in the amount of $10.691 million;

- PCIC was attached to the Department of Agriculture for budgetary purposes

Overview of the Philippine Crop Insurance Corporation

The Philippine Crop Insurance Corporation is the country’s sole crop insurance provider. It is a Government-Owned and Controlled Corporation (GOCC) administratively under the Department of Agriculture (DA), mandated to help stabilize the income of agricultural producers and promote the flow of credit in the countryside by providing insurance protection particularly to the subsistence farmers and fishers against loss of their crops and non-crop agricultural assets on account of natural calamities such as typhoons, floods, droughts, earthquake and volcanic eruptions, plant pests and diseases, and/or other perils.

The insurance products sold by PCIC are rice, corn, high value crops, livestock, fisheries, non-crop agricultural assets, fisheries and aquaculture and credit and life term insurance.

As a GOCC, PCIC has a capital stock of $42.762 million which covers the corporation’s operating expenses. Through the General Appropriations Act (GAA), it receives premium subsidy from the government for and on behalf of the subsistence farmers. For the past five years, 2011-2015, PCIC posted a tremendous uptrend in its operation consistently matched with the increased budget it received from the GAA.

The importance of PCIC as the implementing arm of the Crop Insurance Program has become more concretized and defined with the intensified impacts of extreme weather events.

The Role of Crop Insurance in Agricultural Development

Experts are agreed that agricultural insurance has an important role in development and is essential in stabilizing financial fluctuations for those engaged in agriculture. Todaro (1989) pointed out that many programs to raise agricultural productivity among farmers have suffered because of failure to provide adequate insurance for both financial credit and physical stocks against the risks of crop shortfalls.

The following are the important roles of Crop Insurance:

- Provides protection to farmers’ investments and serves as a risk management/mitigating mechanism specially in the midst of climate change phenomena;

- Serves as a substitute or supplemental collateral to secure loans extended by lending institutions (LIs) like Land Bank of the Philippines (LBP), Local Government Units (LGUs), Rural Banks (RBs), Non-Government Organizations (NGOs) and Cooperatives, specially favouring farmers who have no properties that could serve as collateral;

- Promotes the flow of credit to the countryside by ensuring that borrowing farmers recover their farm investments through indemnities.

The Rice Insurance Program in the Philippines

Rice is the top staple crop of the Philippines. Back in 1981, at the initial implementation of the Crop Insurance Program, rice insurance was the only product in the market.

Rice insurance was availed either as a multi-risk cover or natural disaster cover only. Generally, about 95% of the total coverage availed, is under the multi-risk cover which covers all risks arising from natural disaster like typhoons, floods, earthquakes, tornadoes, droughts, volcanic eruptions and rice pests and diseases.

The period of cover for rice is variable depending on the maturity period of varieties planted, ranging from 100-130 days.

The amount of cover (AC) also varies on a per hectare basis in accordance with the technology adoption of the farmer with AC ranging from $534.75 to $1390.37 per hectare subject to the ceiling cover set by PCIC.

The premium rates also vary according to location, type of cover, planting season and risk classification of coverage.

The rice insurance helps the assured recover his actual farming investment on the insured farm at the time of loss. The assessment of damage on rice crops is ruled by established matrices, influenced by the stage of crop, cost of inputs applied at the time of loss and extent of damage incurred.

The rice insurance premium is costly. To make the premium cost affordable to the farmers, the government shares in the premium at 55% of the total premium.

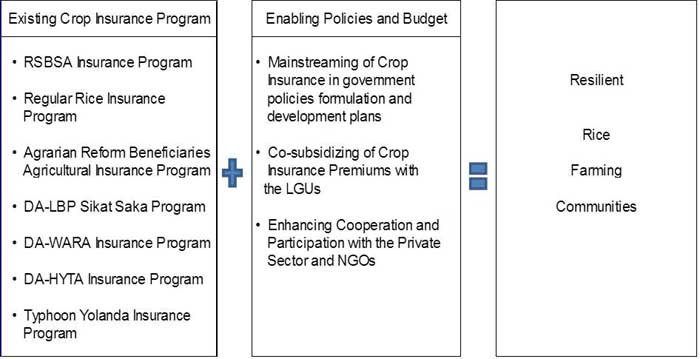

The PCIC Special Rice Insurance Programs

The PCIC is presently implementing two program classifications for its crop insurance products namely; regular program and special program. Under the regular program, the farmer pays his premium share and government shoulders about 55% through subsidy provision. The special program provides full (100%) premium subsidy making the crop insurance premium free of charge to the farmer and the lending institution. Premium payments for these special programs are allocated through the Fiscal Year General Appropriations Act.

The following are the PCIC Special Rice Insurance Programs:

- Registry System for the Basic Sectors in Agriculture (RSBSA) Agricultural Insurance Program (AIP)

The RSBSA-AIP is a full (100%) premium subsidy insurance program for all subsistence farmers listed in the RSBSA. The National Government appropriated to PCIC the sum of $21.381 million and $27.796 million premium subsidy fund pursuant to Fiscal Year (FY) 2014 GAA, Republic Act(RA) 10633 and FY 2015 GAA, RA 10651, to be used exclusively for the full (100) premium subsidy of RSBSA listed farmers.

The eligiblefarmers to the RSBSA Program are the following:

- Farmers are registered in the RSBSA;

- Farmers are not receiving similar types of insurance subsidy from the local government;

- Farmers listed in the RSBSA have insurable interest on the farm submitted for coverage.

- DA-LBP Sikat Program

The DA Sikat Saka Program is the credit component of the Food Staples Sufficiency Program (FSSP) of the Department of Agriculture with Land Bank of the Philippines as the conduit.

The eligible farms must have an effective irrigation and functional drainage system with at least 0.50 hectare but not to exceed 5.0 hectares. The farm must not be within 200 meters to the nearest body of water or marshland, reached by regular transport system and within a generally peaceful area.

The amount of cover on a per hectare basis shall be up to the amount of loan granted by LBP subject to PCIC ceiling cover.

- Agrarian Production Credit Program and Credit Assistance Program for Program Beneficiaries Develoment (APCP-CAP-PBD)

The APCP-CAP-PBD are credit financingprograms being implemented by the Department of Agriculture (DA), Department of Agrarian Reform (DAR) and the Land Bank of the Philippines to provide credit to Agrarian Reform Beneficiaries (ARBs) at affordable cost, including development assistance and market support.

PCIC provides full (100%) premium subsidy for the cost of insurance coverage of ARBs participating in the programs. Rice crop is one of the crops covered. The eligible farmers are ARBs and their household members certified and endorsed by DAR.

- Crop Insurance Program for Subsistence Farmers and Fishers Directly Hit by Typhoon Yolanda

The Crop insurance Program for Typhoon Yolanda survivors is a full (100%) premium subsidy provided by PCIC for insurance coverage of the farm investments, including Accident and Dismemberment Security Scheme of subsistence farmers in certain areas hit by typhoon Yolanda (Haiyan). This program is in compliance with Malacañang Memo-Circular No. 59 dated November 26, 2013, to provide financial relief to farmers and fishers directly and adversely affected by typhoon Yolanda.

Those eligible for coverage are farmers certified by the Office of the Municipal/City Agriculturist or the Municipal Agrarian Officer and Provincial Agrarian Reform Officer as directly hit subsistence farmers.

- Da weather Adverse Rice Areas (WARA) Crop Insurance Program

The WARA Crop Insurance Program is a full (100%) premium subsidy program for subsistence farmers in areas affected by climate change.It is funded by the Department of Agriculture (DA). Qualified to the program are those subsistence farmers identified and verified by the DA-Regional Office to be located in climate change prone areas and areas with adverse agro-climatic conditions. This program was launched in 2012 synchronous with Sikat Saka Program.

- DA Rice High Yield Technology Adoption (HYTA) Crop Insurance Program

The DA-Rice HYTA Program is a full (100%) premium subsidy program for subsistence farmers participating in DA Rice High Yield Technology Adoption Program funded by the DA. This program promotes the use of high quality hybrid and inbred seeds and yield enhancing inputs to increase farm level productivity.

Farmers identified and listed by the DA as beneficiaries under the HYTA program are eligible for coverage.

PCIC Innovative Crop Insurance Products

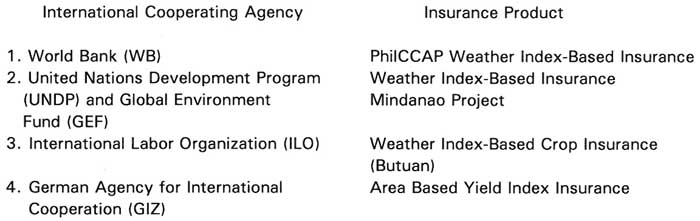

At present PCIC is piloting innovative crop insurance products in collaboration with international cooperating agencies as follows:

The Weather Index-Based Crop Insurance is insurance on the index formed from weather parameters, modified structurally to help the insured customers. The derivative product is structured in such a way that it reflects the actual losses of the insured. Usually, bad weather causes losses on the farms and the losses are prominent in case of a rainfed farm receiving inadequate rainfall.

The object of insurance shall be the weather index specific to the rice or corn crop on which the farmer has an insurable interest on. Insurance shall cover the cost of production inputs per Farm Plan and Budget subject to the cover ceiling as determined from time to time by the PCIC Board of Directors and shall be limited to the prescribed amount of cover appearing in the Certificate of Cover (CIC).

The Weather Index-Based Crop Insurance Products

1. Excess Rainfall Cover –An insurance coverage against excess rainfall. This occurs when the total rainfall in millimeter (mm) either two or more consecutive days or for a given growth stage period, is above the corresponding rainfall threshold of the crop, as the case maybe, and consequently breaches the indicated trigger/strike index.

2. Low rainfall Cover – when the total rainfall in millimeters (mm) either for 15 or more consecutive days (Rice only) or a given growth stage (Rice and Corn) is less than the corresponding indicated Trigger/Strike values.

Benefits of Weather Index-Based Insurance4

According to Ailon Capistrano, the lead of WIBI Mindanao Project- PhilRice Component on Index Development, the benefits of WIBI are the following:

1. Eliminates the dependence of insurer on manual assessment of losses which could be prone to inaccurate payouts due to subjectivity of the assessor because peril assessment is based purely from a data provided by a third party, the official weather bureau, Philippine Atmospheric, Geophysical and Astronomical Services Administration (PAGASA);

______________________________________

4Capistrano, Ailon, 2016, Lead, Index Development, WIBI Mindanao Project- PhilRice Component

2. Moral hazards among the insured is reduced if not eliminated even if the client was inclined to neglect his crop because payouts will still depend on the breached indices validated by a certified data of the PAGASA;

3. Adverse selection by the insurer can be avoided since the limiting criterion for potential WIBI enrollees would be the specified effective proximity of 20 km radius to the weather stations;

4. Higher re-insurance availability resulting to more farms covered by the insurer aside from reduction of operational costs;

5. Reduced claims response time resulting from an objective and simplified peril assessment and payout computation;

6. Improved transparency because the client themselves can personally assess their own claims if the third party data reference on index parameters are made public.

Selected Operational Highlights

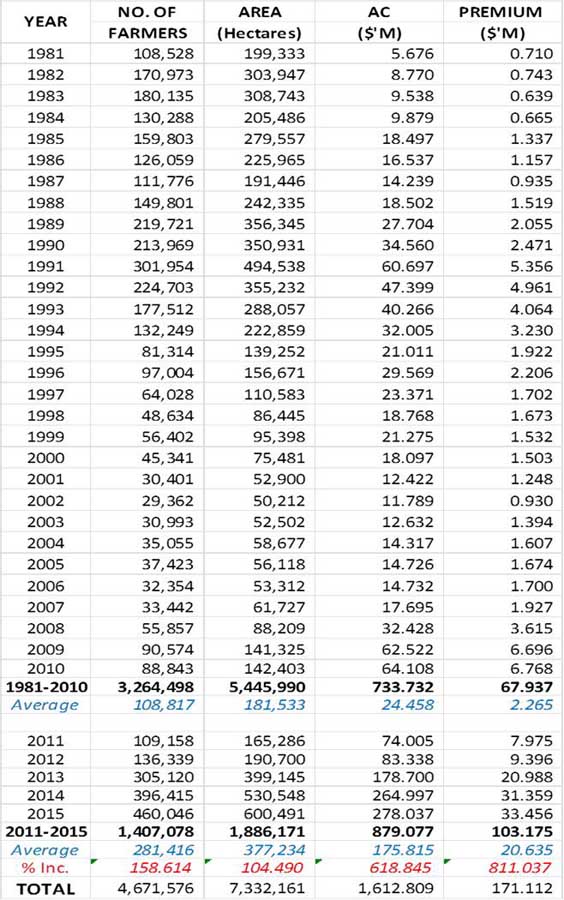

As shown in Table 2, there was a consistent increase on all the insurance performance parameters for crops from the period 2011- 2015. In terms of number of farmers, the average annual increase was 38.93%.

The highest increment was registered in 2013 at 123.8%. This remarkable increase was attributed to the implementation of the Agrarian Reform Beneficiaries (ARB’s) Agricultural Insurance Program (AIP) which infused $21.813 million from the Department of Agrarian Reform (DAR) to provide full premium subsidy for ARB’s.

The increase in 2012 was attributed to the implementation of the DA- Rice Programs namely; DA- Sikat Saka Program and DA- WARA Program.

In 2014, the Registry System for Basic Sectors in Agriculturewas launched with another $21.813 million budget from the 2014 General Appropriation Act for Fiscal Year 2014.

There was also a noted growth of coverage in 2015. This was due to the continued implementation of the RSBSA Program and the DA Rice Programs.

Table 3 shows that that the average number of farmers insured and the premiums paid from 2011-2015 were extremely higher (158%) and 811.037% respectively as compared to the average number of farmers and premiums paid from 1981-2010.

From 1981-2010, the government premium subsidy for the farmers insured were limited to the 55% of the total premium. This amount was to be collected by the PCIC annually. The remaining 45% was shouldered by the insured farmers themselves as a self-financed farmer and 27% if these were borrowing farmers.

Other Government Intervention for Crop Insurance Program

In order to create an environment that will further accelerate the adoption of the crop insurance program as a risk reduction and transfer mechanism, the following are cited:

1. Presidential Decree 1467, Section 14 provides for Inter-agency Linkage to promote and support the operations of the Corporation, all government departments, bureaus, offices, agencies and instrumentalities, national or local, all lending institutions, government or private now or hereafter engaged in the supervised credit program shall act as cooperating agencies of the Corporation , and for this purpose are directed to design their policies, programs, rules and regulations so as to attune and synchronize them with the objectives of PCIC.

2. Republic Act 9729 - Mainstreaming climate change in government policy formulation such that policies and measures that address climate change concerns are integrated in development/planning and sectoral decision making.

3. Republic Act 10121 – Otherwise known as the “Disaster Risk Reduction and Management Act of 2010”, specifically identified crop insurance as a disaster risk management strategy.

4. Climate Change Act of 2009 – The law mandated the Climate Change Commission to create an enabling environment for the design of relevant and appropriate risk-sharing and transfer instruments.

5. DA-Policy and Program Implementation for Climate Change – Committed that the crop insurance program shall pilot the weather-index based insurance and expand coverage to other agricultural fishery ventures.

6. Pending Legislation – The increase in the capitalization of PCIC from $44 million to $222 million.

PCIC Fund Provided by RA 8175

1. PCIC Equity. The authorized common stock to be subscribed by the National Government to PCIC is $32.072 million.

2. Government Premium Subsidy (GPS). The National Government subsidizes the pure risk premium for crop insurance coverage of the marginalized farmers.

3. State Reserve Fund. This is a fund for catastrophic losses in the amount of $106.906 million to be appropriated exclusively to address all losses in excess of risk premium.

Hand in hand with its policy formulation and legislation for the implementation and improvement of the crop insurance program is the support funding which are provided for in Republic Act 8175 under the following sections:

Section 6.3 of Republic Act 8175 provides that unreleased government premium subsidy for policies written from May 01, 1981 to December 29, 1995, shall be programmed for payment by government within a period of ten (10) years from 1995 and the yearly sums shall be included in the budgetary appropriations for submission to Congress in addition to the premium subsidy requirement for the fiscal year involved.

Section 6.4 – states that calamity funds earmarked by the Government shall include a certain percentage for crop insurance and shall be released to an administered by PCIC.

Section 6.5 – Ten percent (10%) of the net earnings of the Philippine Charity Sweepstakes Office (PCSO) from its lotto operation shall be earmarked by the Crop Insurance Program and said amount shall be directly remitted by PCSO to PCIC every six (6) months until amount of government subscription is fully paid.

PCIC Service Delivery Channels

The Crop Insurance products and services are delivered through its thirteen (13) Regional Offices and thirty-three (33) ProvincialExtension Offices nationwide manned by 247 able employees.

PCIC Linkages and Partnerships

With a very lean workforce at PCIC, it is essential for its effective and efficient delivery of service to establish linkage and partnerships.

The major insurance partner of PCIC is the Land Bank of the Philippines through its 37 Lending Centers and 72 Branch Offices.

The other partners are the following:

- Rural Bankers Association of the Philippine

- National Federation of Cooperatives

- Cooperative Rural Banks

- Micro-Finance Institutions

- Non-Government Organizations

- Finance Service Providers

- Farmers’ and Peoples’ Organizations

- Local Government Units

- Irrigators Associations

On the government side, PCIC linkages with the following:

- Department of Agriculture and its Regional Offices

- Department of Agrarian Reform

- National Irrigation Administration

- Bureau of Soils and Water Management

- Cooperative Development Authority

- Bureau of Animal Industry

- Philippine Carabao Center

- National Dairy Administration

- Philippine Council of Agriculture and Fisheries

- Philippine Coconut Authority

- Agricultural Training Institute

Further, PCIC accredits individual insurance solicitors and underwriters.

CONCLUSIONS

It is evident that the Philippines is on the top list of vulnerable countries to climate change events with two thirds of its population, the rural poor, situated in the agriculture sector exposed to risks and hazards.

Crop Insurance was identified as the effective risk management and transfer strategy to address the impacts of climate change, however, subsistence farmers could hardly afford actuarially determined premiums as evidenced in the low enrolment from the period 1981-2010 when 45% of the premiums were shouldered by the farmers.

Government should strengthen the Crop Insurance Program by passing into law the authority to increase the capitalization of PCIC from Php 2 billion to Php 10 billion pesos to be able to expand its service reach and penetration rate from 8% to 32%, thus, building resilience in agriculture.

REFERENCES

Braving the Uncertainties of Weather: 2013. “Situating Insurance within Climate Change Adaptation and Risk Reduction Strategies of the Philippines”, Climate Change Commission, Oxfam, Quezon City, Philippines.

Hilario, M.G.M., 2015, Braving the Uncertainties of Weather: “Weather Index-Based Insurance as Agriculture Risk Transfer Mechanism for Climate Change Adaptation and Risk Reduction in the Philippines”, p. 6.

Newsletter, 2016. WIBI Mindanao Project, “PhilRice Explains the Outstanding Benefits of Weather Index-Based Insurance”, pp. 2-3.

Presidential Decree 1467, 1978. “Creation of the Philippine Crop Insurance Corporation”.

Presidential Decree 1733, 1980.

Project Updates, 2015-001, WIBI Mindanao Project, “Scaling Up Risk Transfer Mechanisms for Climate Vulnerable Communities in Mindanao”, pp. 1-2.

Project Updates 2015-002, Mindanao Project, “Building Resilience To Climate and Economic Shocks Through Risk Transfer Mechanism and Diversified Livelihoods”, p. 2.

Revised Charter of the Philippine Crop Insurance Corporation Act of 1995, Republic Act 8175.

Rogelio N.C. et. al., 2014 “Coping with Extreme Climatic Events: Stories of Resiliency in the Philippines” p.2, SEARCA Knowledge Center on Climate Change.

Table1. Government Policy Legislations on the Creation of the Philippine Crop Insurance Corporationa

a The Government-Owned and Controlled Corporation mandated to provide insurance protection to the country’s agricultural producers, particularly the subsistence farmers, against: (1) Crop losses arising from natural calamities such as typhoons, floods, drought, earthquakes and volcanic eruptions as well as plant diseases and pest infestation; (2) Non-crop agricultural asset losses due to perils for which the asset has been insured against.

Table 2. Rice Insurance Coverage and Government Premium Subsidies from 2011 – 2015b

b Consolidated from PCIC Annual Reports for the period 2011-2015

c Implementation period of the PCIC fully subsidized premium subsidy pursuant to General Appropriations Acts (GAA) for Fiscal years 2014 and 2015 under Republic Acts 10633 and 10650, respectively.

d Implementation of the Agrarian Reform Beneficiaries (ARB) Agricultural Insurance Program (AIP) with $21.381 million fund from the GAA FY 2013.

Table 3. Comparative Crop Insurance Average Performance for the Period 1981-2010 and 2011-2015

.jpg)

Figure 1. Illustrates the consistent uptrend in the number of farmers enrolled in the crop insurance program during the implementation of fully

subsidized premium.

.jpg)

Figure 2. Consistent with Figure 1, Figure 2 shows increasing amount of insurance cover .

Figure 3. Shows increasing amount of insurance premium generated in the crop Insurance program for the Period 2011-2015.

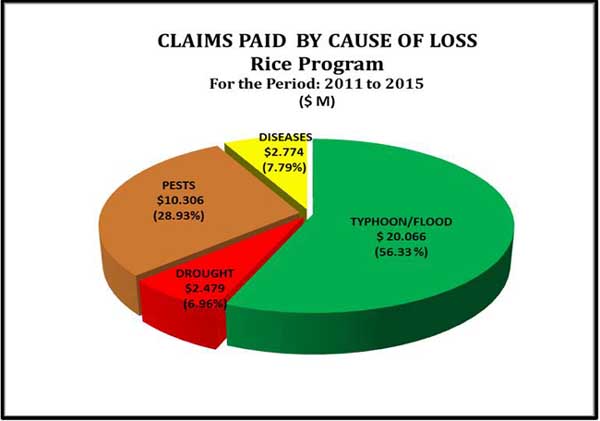

Figure 3. Indicates that the biggest portion of claims paid from 2011-2015 was due to natural disaster. 56.33% of the pie was paid to losses due to

Typhoon and flood, while 6.96% was paid to drought.

| Submitted as a country paper for the FFTC-RDA International Seminar on Implementing and Improving Crop Natural Disaster Insurance Program, June 14-16, 2016, Jeonju, Korea |

Government and its Role in the Implementation and Enhancement of the Crop Insurance Program in the Philippines1

ABSTRACT

This Paper underscores the significant role of government in the “Implementation and Enhancement of the Crop Insurance Program in the Philippines”.

From the perspective of the author, influenced by her readings and insights gained from various fora attended, the implementation and enhancement of the above cited program, is attributed to the following: (i) policy formulation and legislation; (ii) enabling policy environment; (iii) policy budget; and (iv) partnership. This paper also attempts to present the various fully subsidized rice insurance programs implemented by the Philippine Crop Insurance Corporation (PCIC), the rationale and implementing guidelines of each.

Like any program of national significance, the implementation of the above-program is not a stand-alone performance and responsibility of the Philippine Crop Insurance Corporation (PCIC) as the implementing agency, rather, it is the product of the interplay among legislators, implementers and partners and government institutions by way of integrating, synchronizing and mobilizing their actions, strategies and resources towards a common goal: building resilience in rice production and attaining Food Self Sufficiency in the country.

This paper also finds the government budget support through subsidies and appropriation as the key factor to the sustained implementation of an Agricultural Insurance Program in general and Crop Insurance Program in particular.

Keywords: climate change, academe, technocrats, global phenomena, guarantee fund, stabilize, mobilize, General Appropriation Act, fluctuations, mitigate, mechanism, innovative, government natural disaster, enhancement, policy legislation, policy environment, policy budget, partnership, legislators, implementers, government institutions, subsidies, synchronizing, mobilizing, strategies, resources, appropriation, resilience, sustained, key, collateral, investment, weather index-based, premium, weather adverse, mandate, capitalization, mainstream, vulnerable, subsistence, trigger, breach, multi-risk, operating policies, operating system procedure.

______________________________________

1Country Paper presented during the International Seminar on “Implementing and Improving Crop Natural Disaster Insurance Program” on June 13-17, 2016, Jeonju, Korea. Organized by the Food and Fertilizer Technology Center (FFTC) for the Asia and Pacific Region and the Rural Development Administration (RDA).

2Department Manager, Business Development and Marketing Department, Philippine Crop Insurance Corporation (PCIC) and Technical Focal Person UNDP-GEF-PCIC WIBI Mindanao Project: Scaling–up Risk Transfer Mechanisms for Climate Vulnerable Agriculture-based Communities in Mindanao. Email: pagaddu.rodelia@yahoo.com

INTRODUCTION

The Philippines is an archipelago nestled between a part of the Philippine Sea and West Pacific Sea located along the edge of the Pacific “Ring of Fire”. Inherent to its location, the Philippines has one of the highest exposures to natural hazards in the world.

A recent United Nations report identified the Philippines as the third most at risk to climate change events. According to another report released by environmental organization, German Watch- the Global Climate Risk Index 2015, which lists the most affected countries by weather related disturbances, like storms, floods and heat waves, based on the 2013 events, the Philippines is the top most vulnerable.

As an agricultural country, two-thirds of its population is directly or indirectly exposed to the impacts of climate change events. The country’s agricultural sector, composed of the rural poor is the most likely affected not only because its productivity and performance is dependent on weather, sustainability of water and remaining biological resources, but also because a significant portion of its population depends on it for food and livelihood.

In recent years, the world is a witness to the tremendous losses and damages wrought by extreme unpredictable weather conditions with the farmers, fishers and their children, prey to these unfortunate events of devastation, trapping them into the tunnel of poverty.

The above scenario must not be left unattended. Myrdal, Nobel Laureate in Economics attested, “it is in the agricultural sector that the battle for long- term economic development will be won or lost"3. Furthermore, if development is to take place and become self-sustaining, it will have to start in the rural areas in general and the agriculture sector in particular.

It is therefore in the above context that government and its instrumentalities consider as imperative today, the adoption of risks management schemes to spell the difference between a stagnated and a growing agri-based economy by building resilience in the country’s agricultural sector.

METHODOLOGY

To be able to attain the objectives of this study, the researcher employed the descriptive design. Analyses of various documents containing information on the Crop Insurance Program were undertaken. Primary and secondary data analyses were also carried out on the thirty five (35) years operational results of PCIC.

SCOPE AND LIMITATION

The term crop as used in this paper shall refer to “rice” only, in consideration of rice as the top staple crop of the Philippines and the only crop initially covered in the Crop Insurance Program.

______________________________________

3 Todaro, M. 1989. Economic Development in the Third World, New York. Pitun Publishing, Inc.

Development of the Crop Insurance Program in the Philippines

Climate change and variabilities is an increasing global phenomena getting the attention and concerned action among affected communities, policy legislators, program implementers, development technocrats, government and non-government sectors, academe and private counterparts the world over.

For its part, the Philippines, three decades and seven years ago, long before the global call on climate change, have included in its development framework the institution of a Crop Insurance System through the establishment of the Philippine Crop Insurance Corporation (PCIC).

Establishment of the Crop Insurance in the Philippines took off from the Agricultural Guarantee Fund (AGF) operationalized as an integral component of the Agrarian Reform Program implemented in 1972 which was intended to uplift the economic life of the farmer, through land and income distribution.

The Land Bank of the Philippines (LBP) administered the AGF to provide guarantee cover of up to 85% of the loan extended to small farmers. This guarantee scheme reinforced the supply of credit in the countryside, but failed to consider the demand side.

Guarantee mechanism only restructured the defaulted loan and did not grant a second loan to the affected farmer until the loan had been fully paid, thus, rendering the farmer borrower unproductive because of his failure to replant leading to perpetual indebtedness.

Cognizant of the weakness of the AGF scheme, the LBP as administrator, took the initiative to find ways and means to fill the gap by studying the feasibility of a crop insurance scheme that would insulate affected farmers from the vicious cycle of borrowing in order to plant, planting to be able to pay debt, and then borrow again to cover up losses and debts.

The study concluded that an all-risks crop insurance was feasible and was submitted to LBP Board of Directors who recommended to the President of the Philippines the creation and establishment of a crop insurance system. The committee reported the importance of implementing a crop insurance scheme as follows:

Creation of the PCIC

On June 11, 1978, the President of the Philippines, then Ferdinand E. Marcos, promulgated Presidential Decree (PD) 1467 creating the PCIC as the implementing agency of the country’s Crop Insurance Program (CIP).After the promulgation of the law, further studies were undertaken to operationalize the CIP by drawing up operating policies and operating systems and procedures.

On May 07, 1981, the CIP was launched. It was initially financed by the AGF which was transferred to the PCIC as part of the governments contribution to the PCIC Fund, thus, the funds provided to PCIC came from agrarian reform credit.

In order to make PCIC more responsive, the charter was amended by Presidential Decree 1733 on October 21, 1980. The law mandated that Crop Insurance be made compulsory for all lending institutions granting production loans for rice under the supervised credit programs of the government and the same shall act as PCIC underwriters. The law also provided for sanction for all lending institutions who did not comply.

Letter of Instruction No. 1242 was also signed and mandated PCIC to administer a Trust Fund amounting to $9.622 million to be given in tranches for three years to pay the claims of the Philippine National Bank and rural banks which participated in the Masagana 99 credit up to 85% program.

On December 29, 1995, Republic Act (RA) 1875was signed into law further amending PD 1467 to include provisions intended to make the Crop Insurance Program more stable and beneficial to the farmers. The following improvements are enumerated below:

Overview of the Philippine Crop Insurance Corporation

The Philippine Crop Insurance Corporation is the country’s sole crop insurance provider. It is a Government-Owned and Controlled Corporation (GOCC) administratively under the Department of Agriculture (DA), mandated to help stabilize the income of agricultural producers and promote the flow of credit in the countryside by providing insurance protection particularly to the subsistence farmers and fishers against loss of their crops and non-crop agricultural assets on account of natural calamities such as typhoons, floods, droughts, earthquake and volcanic eruptions, plant pests and diseases, and/or other perils.

The insurance products sold by PCIC are rice, corn, high value crops, livestock, fisheries, non-crop agricultural assets, fisheries and aquaculture and credit and life term insurance.

As a GOCC, PCIC has a capital stock of $42.762 million which covers the corporation’s operating expenses. Through the General Appropriations Act (GAA), it receives premium subsidy from the government for and on behalf of the subsistence farmers. For the past five years, 2011-2015, PCIC posted a tremendous uptrend in its operation consistently matched with the increased budget it received from the GAA.

The importance of PCIC as the implementing arm of the Crop Insurance Program has become more concretized and defined with the intensified impacts of extreme weather events.

The Role of Crop Insurance in Agricultural Development

Experts are agreed that agricultural insurance has an important role in development and is essential in stabilizing financial fluctuations for those engaged in agriculture. Todaro (1989) pointed out that many programs to raise agricultural productivity among farmers have suffered because of failure to provide adequate insurance for both financial credit and physical stocks against the risks of crop shortfalls.

The following are the important roles of Crop Insurance:

The Rice Insurance Program in the Philippines

Rice is the top staple crop of the Philippines. Back in 1981, at the initial implementation of the Crop Insurance Program, rice insurance was the only product in the market.

Rice insurance was availed either as a multi-risk cover or natural disaster cover only. Generally, about 95% of the total coverage availed, is under the multi-risk cover which covers all risks arising from natural disaster like typhoons, floods, earthquakes, tornadoes, droughts, volcanic eruptions and rice pests and diseases.

The period of cover for rice is variable depending on the maturity period of varieties planted, ranging from 100-130 days.

The amount of cover (AC) also varies on a per hectare basis in accordance with the technology adoption of the farmer with AC ranging from $534.75 to $1390.37 per hectare subject to the ceiling cover set by PCIC.

The premium rates also vary according to location, type of cover, planting season and risk classification of coverage.

The rice insurance helps the assured recover his actual farming investment on the insured farm at the time of loss. The assessment of damage on rice crops is ruled by established matrices, influenced by the stage of crop, cost of inputs applied at the time of loss and extent of damage incurred.

The rice insurance premium is costly. To make the premium cost affordable to the farmers, the government shares in the premium at 55% of the total premium.

The PCIC Special Rice Insurance Programs

The PCIC is presently implementing two program classifications for its crop insurance products namely; regular program and special program. Under the regular program, the farmer pays his premium share and government shoulders about 55% through subsidy provision. The special program provides full (100%) premium subsidy making the crop insurance premium free of charge to the farmer and the lending institution. Premium payments for these special programs are allocated through the Fiscal Year General Appropriations Act.

The following are the PCIC Special Rice Insurance Programs:

The RSBSA-AIP is a full (100%) premium subsidy insurance program for all subsistence farmers listed in the RSBSA. The National Government appropriated to PCIC the sum of $21.381 million and $27.796 million premium subsidy fund pursuant to Fiscal Year (FY) 2014 GAA, Republic Act(RA) 10633 and FY 2015 GAA, RA 10651, to be used exclusively for the full (100) premium subsidy of RSBSA listed farmers.

The eligiblefarmers to the RSBSA Program are the following:

The DA Sikat Saka Program is the credit component of the Food Staples Sufficiency Program (FSSP) of the Department of Agriculture with Land Bank of the Philippines as the conduit.

The eligible farms must have an effective irrigation and functional drainage system with at least 0.50 hectare but not to exceed 5.0 hectares. The farm must not be within 200 meters to the nearest body of water or marshland, reached by regular transport system and within a generally peaceful area.

The amount of cover on a per hectare basis shall be up to the amount of loan granted by LBP subject to PCIC ceiling cover.

The APCP-CAP-PBD are credit financingprograms being implemented by the Department of Agriculture (DA), Department of Agrarian Reform (DAR) and the Land Bank of the Philippines to provide credit to Agrarian Reform Beneficiaries (ARBs) at affordable cost, including development assistance and market support.

PCIC provides full (100%) premium subsidy for the cost of insurance coverage of ARBs participating in the programs. Rice crop is one of the crops covered. The eligible farmers are ARBs and their household members certified and endorsed by DAR.

The Crop insurance Program for Typhoon Yolanda survivors is a full (100%) premium subsidy provided by PCIC for insurance coverage of the farm investments, including Accident and Dismemberment Security Scheme of subsistence farmers in certain areas hit by typhoon Yolanda (Haiyan). This program is in compliance with Malacañang Memo-Circular No. 59 dated November 26, 2013, to provide financial relief to farmers and fishers directly and adversely affected by typhoon Yolanda.

Those eligible for coverage are farmers certified by the Office of the Municipal/City Agriculturist or the Municipal Agrarian Officer and Provincial Agrarian Reform Officer as directly hit subsistence farmers.

The WARA Crop Insurance Program is a full (100%) premium subsidy program for subsistence farmers in areas affected by climate change.It is funded by the Department of Agriculture (DA). Qualified to the program are those subsistence farmers identified and verified by the DA-Regional Office to be located in climate change prone areas and areas with adverse agro-climatic conditions. This program was launched in 2012 synchronous with Sikat Saka Program.

The DA-Rice HYTA Program is a full (100%) premium subsidy program for subsistence farmers participating in DA Rice High Yield Technology Adoption Program funded by the DA. This program promotes the use of high quality hybrid and inbred seeds and yield enhancing inputs to increase farm level productivity.

Farmers identified and listed by the DA as beneficiaries under the HYTA program are eligible for coverage.

PCIC Innovative Crop Insurance Products

At present PCIC is piloting innovative crop insurance products in collaboration with international cooperating agencies as follows:

The Weather Index-Based Crop Insurance is insurance on the index formed from weather parameters, modified structurally to help the insured customers. The derivative product is structured in such a way that it reflects the actual losses of the insured. Usually, bad weather causes losses on the farms and the losses are prominent in case of a rainfed farm receiving inadequate rainfall.

The object of insurance shall be the weather index specific to the rice or corn crop on which the farmer has an insurable interest on. Insurance shall cover the cost of production inputs per Farm Plan and Budget subject to the cover ceiling as determined from time to time by the PCIC Board of Directors and shall be limited to the prescribed amount of cover appearing in the Certificate of Cover (CIC).

The Weather Index-Based Crop Insurance Products

1. Excess Rainfall Cover –An insurance coverage against excess rainfall. This occurs when the total rainfall in millimeter (mm) either two or more consecutive days or for a given growth stage period, is above the corresponding rainfall threshold of the crop, as the case maybe, and consequently breaches the indicated trigger/strike index.

2. Low rainfall Cover – when the total rainfall in millimeters (mm) either for 15 or more consecutive days (Rice only) or a given growth stage (Rice and Corn) is less than the corresponding indicated Trigger/Strike values.

Benefits of Weather Index-Based Insurance4

According to Ailon Capistrano, the lead of WIBI Mindanao Project- PhilRice Component on Index Development, the benefits of WIBI are the following:

1. Eliminates the dependence of insurer on manual assessment of losses which could be prone to inaccurate payouts due to subjectivity of the assessor because peril assessment is based purely from a data provided by a third party, the official weather bureau, Philippine Atmospheric, Geophysical and Astronomical Services Administration (PAGASA);

______________________________________

4Capistrano, Ailon, 2016, Lead, Index Development, WIBI Mindanao Project- PhilRice Component

2. Moral hazards among the insured is reduced if not eliminated even if the client was inclined to neglect his crop because payouts will still depend on the breached indices validated by a certified data of the PAGASA;

3. Adverse selection by the insurer can be avoided since the limiting criterion for potential WIBI enrollees would be the specified effective proximity of 20 km radius to the weather stations;

4. Higher re-insurance availability resulting to more farms covered by the insurer aside from reduction of operational costs;

5. Reduced claims response time resulting from an objective and simplified peril assessment and payout computation;

6. Improved transparency because the client themselves can personally assess their own claims if the third party data reference on index parameters are made public.

Selected Operational Highlights

As shown in Table 2, there was a consistent increase on all the insurance performance parameters for crops from the period 2011- 2015. In terms of number of farmers, the average annual increase was 38.93%.

The highest increment was registered in 2013 at 123.8%. This remarkable increase was attributed to the implementation of the Agrarian Reform Beneficiaries (ARB’s) Agricultural Insurance Program (AIP) which infused $21.813 million from the Department of Agrarian Reform (DAR) to provide full premium subsidy for ARB’s.

The increase in 2012 was attributed to the implementation of the DA- Rice Programs namely; DA- Sikat Saka Program and DA- WARA Program.

In 2014, the Registry System for Basic Sectors in Agriculturewas launched with another $21.813 million budget from the 2014 General Appropriation Act for Fiscal Year 2014.

There was also a noted growth of coverage in 2015. This was due to the continued implementation of the RSBSA Program and the DA Rice Programs.

Table 3 shows that that the average number of farmers insured and the premiums paid from 2011-2015 were extremely higher (158%) and 811.037% respectively as compared to the average number of farmers and premiums paid from 1981-2010.

From 1981-2010, the government premium subsidy for the farmers insured were limited to the 55% of the total premium. This amount was to be collected by the PCIC annually. The remaining 45% was shouldered by the insured farmers themselves as a self-financed farmer and 27% if these were borrowing farmers.

Other Government Intervention for Crop Insurance Program

In order to create an environment that will further accelerate the adoption of the crop insurance program as a risk reduction and transfer mechanism, the following are cited:

1. Presidential Decree 1467, Section 14 provides for Inter-agency Linkage to promote and support the operations of the Corporation, all government departments, bureaus, offices, agencies and instrumentalities, national or local, all lending institutions, government or private now or hereafter engaged in the supervised credit program shall act as cooperating agencies of the Corporation , and for this purpose are directed to design their policies, programs, rules and regulations so as to attune and synchronize them with the objectives of PCIC.

2. Republic Act 9729 - Mainstreaming climate change in government policy formulation such that policies and measures that address climate change concerns are integrated in development/planning and sectoral decision making.

3. Republic Act 10121 – Otherwise known as the “Disaster Risk Reduction and Management Act of 2010”, specifically identified crop insurance as a disaster risk management strategy.

4. Climate Change Act of 2009 – The law mandated the Climate Change Commission to create an enabling environment for the design of relevant and appropriate risk-sharing and transfer instruments.

5. DA-Policy and Program Implementation for Climate Change – Committed that the crop insurance program shall pilot the weather-index based insurance and expand coverage to other agricultural fishery ventures.

6. Pending Legislation – The increase in the capitalization of PCIC from $44 million to $222 million.

PCIC Fund Provided by RA 8175

1. PCIC Equity. The authorized common stock to be subscribed by the National Government to PCIC is $32.072 million.

2. Government Premium Subsidy (GPS). The National Government subsidizes the pure risk premium for crop insurance coverage of the marginalized farmers.

3. State Reserve Fund. This is a fund for catastrophic losses in the amount of $106.906 million to be appropriated exclusively to address all losses in excess of risk premium.

Hand in hand with its policy formulation and legislation for the implementation and improvement of the crop insurance program is the support funding which are provided for in Republic Act 8175 under the following sections:

Section 6.3 of Republic Act 8175 provides that unreleased government premium subsidy for policies written from May 01, 1981 to December 29, 1995, shall be programmed for payment by government within a period of ten (10) years from 1995 and the yearly sums shall be included in the budgetary appropriations for submission to Congress in addition to the premium subsidy requirement for the fiscal year involved.

Section 6.4 – states that calamity funds earmarked by the Government shall include a certain percentage for crop insurance and shall be released to an administered by PCIC.

Section 6.5 – Ten percent (10%) of the net earnings of the Philippine Charity Sweepstakes Office (PCSO) from its lotto operation shall be earmarked by the Crop Insurance Program and said amount shall be directly remitted by PCSO to PCIC every six (6) months until amount of government subscription is fully paid.

PCIC Service Delivery Channels

The Crop Insurance products and services are delivered through its thirteen (13) Regional Offices and thirty-three (33) ProvincialExtension Offices nationwide manned by 247 able employees.

PCIC Linkages and Partnerships

With a very lean workforce at PCIC, it is essential for its effective and efficient delivery of service to establish linkage and partnerships.

The major insurance partner of PCIC is the Land Bank of the Philippines through its 37 Lending Centers and 72 Branch Offices.

The other partners are the following:

On the government side, PCIC linkages with the following:

Further, PCIC accredits individual insurance solicitors and underwriters.

CONCLUSIONS

It is evident that the Philippines is on the top list of vulnerable countries to climate change events with two thirds of its population, the rural poor, situated in the agriculture sector exposed to risks and hazards.

Crop Insurance was identified as the effective risk management and transfer strategy to address the impacts of climate change, however, subsistence farmers could hardly afford actuarially determined premiums as evidenced in the low enrolment from the period 1981-2010 when 45% of the premiums were shouldered by the farmers.

Government should strengthen the Crop Insurance Program by passing into law the authority to increase the capitalization of PCIC from Php 2 billion to Php 10 billion pesos to be able to expand its service reach and penetration rate from 8% to 32%, thus, building resilience in agriculture.

REFERENCES

Braving the Uncertainties of Weather: 2013. “Situating Insurance within Climate Change Adaptation and Risk Reduction Strategies of the Philippines”, Climate Change Commission, Oxfam, Quezon City, Philippines.

Hilario, M.G.M., 2015, Braving the Uncertainties of Weather: “Weather Index-Based Insurance as Agriculture Risk Transfer Mechanism for Climate Change Adaptation and Risk Reduction in the Philippines”, p. 6.

Newsletter, 2016. WIBI Mindanao Project, “PhilRice Explains the Outstanding Benefits of Weather Index-Based Insurance”, pp. 2-3.

Presidential Decree 1467, 1978. “Creation of the Philippine Crop Insurance Corporation”.

Presidential Decree 1733, 1980.

Project Updates, 2015-001, WIBI Mindanao Project, “Scaling Up Risk Transfer Mechanisms for Climate Vulnerable Communities in Mindanao”, pp. 1-2.

Project Updates 2015-002, Mindanao Project, “Building Resilience To Climate and Economic Shocks Through Risk Transfer Mechanism and Diversified Livelihoods”, p. 2.

Revised Charter of the Philippine Crop Insurance Corporation Act of 1995, Republic Act 8175.

Rogelio N.C. et. al., 2014 “Coping with Extreme Climatic Events: Stories of Resiliency in the Philippines” p.2, SEARCA Knowledge Center on Climate Change.

Table1. Government Policy Legislations on the Creation of the Philippine Crop Insurance Corporationa

a The Government-Owned and Controlled Corporation mandated to provide insurance protection to the country’s agricultural producers, particularly the subsistence farmers, against: (1) Crop losses arising from natural calamities such as typhoons, floods, drought, earthquakes and volcanic eruptions as well as plant diseases and pest infestation; (2) Non-crop agricultural asset losses due to perils for which the asset has been insured against.

Table 2. Rice Insurance Coverage and Government Premium Subsidies from 2011 – 2015b

b Consolidated from PCIC Annual Reports for the period 2011-2015

c Implementation period of the PCIC fully subsidized premium subsidy pursuant to General Appropriations Acts (GAA) for Fiscal years 2014 and 2015 under Republic Acts 10633 and 10650, respectively.

d Implementation of the Agrarian Reform Beneficiaries (ARB) Agricultural Insurance Program (AIP) with $21.381 million fund from the GAA FY 2013.

Table 3. Comparative Crop Insurance Average Performance for the Period 1981-2010 and 2011-2015

Figure 1. Illustrates the consistent uptrend in the number of farmers enrolled in the crop insurance program during the implementation of fully

subsidized premium.

Figure 2. Consistent with Figure 1, Figure 2 shows increasing amount of insurance cover .

Figure 3. Shows increasing amount of insurance premium generated in the crop Insurance program for the Period 2011-2015.

Figure 3. Indicates that the biggest portion of claims paid from 2011-2015 was due to natural disaster. 56.33% of the pie was paid to losses due to

Typhoon and flood, while 6.96% was paid to drought.