Introduction

Insurance is an instrument that is used to manage risks. In agriculture, insurance is a tool used to manage risks arising from the production of commodities, price variability, as well as climate and weather uncertainties. Risks from production is normally addressed by technological advances such as new varieties and other technological innovations. Risks arising out of price variability is generally addressed at the policy and market levels. The most important risk that is difficult to control is the risk against adverse weather conditions, or now also due to climate change.

In the Philippines, agricultural insurance is availed of by farmers also as a credit reduction mechanism, as a surrogate capital or substitute for physical capital (PICC, 2016). Lending institutions require agricultural insurance from farmer borrowers. Crop insurance facilitate credit access especially in formal lending institutions like the Land Bank of the Philippines.

This paper describes the current agricultural insurance system in the Philippines. The first section is a discussion of the legal framework for agricultural insurance programs by the government. The second section describes in detail the various agricultural insurance products and programs. The last section examines some of the issues besetting the Philippine agricultural insurance industry and the proposed legislations for the improvement of insurance delivery.

Legal framework of the agricultural insurance in the Philippines

The Philippine agricultural insurance is supervised by the Philippine Crop Insurance Corporation (PCIC), a government owned and controlled corporation under the Department of Agriculture. PCIC was created through Presidential Decree 1467 Creating the “Philippine Crop Insurance Corporation” Prescribing Its Powers and Activities, Providing for its Capitalization and for the Required Government Premium Subsidy and for Other Purposes,” and was passed into law in 1978. The main purpose of the insurance was “to provide insurance protection to farmers against losses arising from natural disasters, plant diseases and pest infestations initially for palay crops and later to other crops.” PD 1467 was later amended by Presidential Decree 1733 in 1980 and Republic Act 8175 An Act Further Amending Presidential Decree No. 1467, As Amended, Otherwise Known as the Charter of the Philippine Crop Insurance Corporation (PCIC) in Order to Make the Crop Insurance System More Stable and Beneficial to the Farmers Covered Thereby and for the National Economy, in 1995.

According to the laws, insurance of qualified farmers are against losses arising from natural calamities, plant diseases and pest infestations. Initially, the law stipulates that PCIC provide insurance coverage for rice crops, and has provisions for expansion to other crops as well as other non-agricultural assets such as machineries equipment, transport facilities and other related infrastructures. The laws mandate that the insurance shall cover the cost of production inputs, the value of the farmer's own labor and those of the members of his household, including the value of the labor of hired workers, and a portion of the expected yield, but excluding losses arising from “avoidable risks due to negligence, malfeasance or fraud committed by the insured or any member of his immediate farm household or employee or the failure of the insured to follow proven farm practices."

The PCIC is given the free hand to determine the premium rates, as well as the allocated sharing among farmers, lending institutions and the government. Only subsistence farmers cultivating not more than 7 hectares are covered by the government share of premium.

Types of Philippine agricultural insurance products and programs

Currently, there are seven insurance products and five insurance programs being administered and implemented by the PCIC. The seven insurance products are:

-

crop insurance for rice;

-

crop insurance for corn;

-

livestock insurance program;

-

fisheries insurance program;

-

non-crop agricultural asset insurance program;

-

high value commercial crop insurance; and

-

accident and dismemberment security scheme.

The five insurance programs are:

-

rice crop insurance for the Department of Agriculture weather adverse rice areas (WARA);

-

rice crop insurance for DA-LBP SIKAT SAKA program;

-

farmers and fishefolk listed in the registry system for basic sectors in agriculture (RSBSA);

-

agrarian reform beneficiaries (ARBs) participating in the agrarian production credit program (APCP) and credit assistance program for program beneficiaries development (CAP-PBD); and

-

for subsistence farmers and fisherfolk directly hit by typhoon Yolanda or Haiyan.

Insurance for crops

The agricultural insurance for rice was first offered in in 1981, followed by coverage for corn in 1982 and high value commercial crops (HVCC), starting in 1991 for tobacco and expanded in 1993 to cover other commodities.

Under these products, the objects of the insurance are the standing rice, corn, and HVCC. The insurance covers the cost of production of inputs including labor, plus an optional additional amount of cover of up to 20% of cover portion for rice and corn and 120% of the expected yield for HVCC.

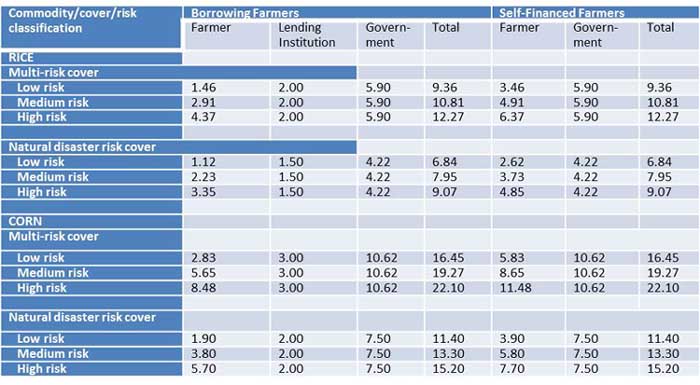

For rice and corn, the cover ceilings vary depending on the type of seeds used: for rice, PhP 41,000[3]/ha for inbred varieties, PhP 50,000/ha for seed production of inbred varieties as well as for commercial production (F1) of hybrid varieties, and PhP 65,000/ha for seed production of hybrid varieties. For corn, the cover ceilings are PhP 40,000/ha for hybrid varieties and PhP 28,000/ha for open-pollinated varieties. All farms using the National Seed Industry Council varieties are insurable. The period of cover is from seeding to harvesting. The premium rates vary depending on the region (location), season, and risk classification, and is shared by the farmer, lending institution and the government (Table 1).

For HVCC, crops such as abaca, “ampalaya”, asparagus, banana, cabbage, carrot, cassava, coconut, coffee, commercial trees, cotton, garlic, ginger, mango, mungbean, onion, papaya, peanut, pineapple, sugarcane, sweet potato, tobacco, tomato, water melon, white potato, and others are covered, subject to their feasibility. In contrast to rice and corn, the insurance premium for HVCC shall be market-rated and shall be borne solely by the farmer, and the premium rate ranging from 2% to 7% depending on the pre-coverage evaluation and other factors such as agro-climatic conditions, type of soil, terrain, and other location specific factors.

Table 1. National composite rates and premium sharing (%) for rice and corn insurance in the Philippines.

Source: PCIC, 2016.

The insurance covers risks as natural disasters such as typhoons, floods, drought, earthquakes, and volcanic eruptions, plant diseases, pests infestations and accidental fire for HVCC.

For the settlement of claims, verification and loss assessments are made by a team of adjusters who will assess the loss category and amount of indemnity. Insured farmers have a no-claim benefit of 10% of the farmer’s net premium shared paid for three consecutive crop seasons not subject of any claim.

Livestock insurance program

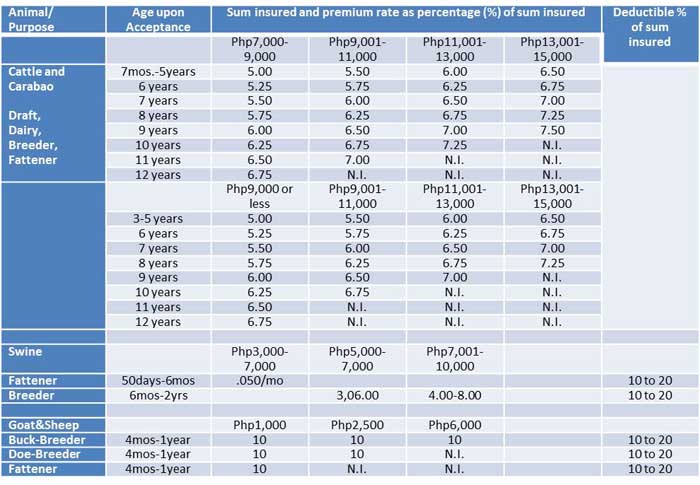

The livestock insurance program started in 1988 through a tie-up with Philippine Livestock Management Services Corporation. The insurance covers for livestock are for cattle, carabao, horse, swine, goat, poultry, and game fowls and animals, covering death due to accidents, diseases and other risks. The types of insurance covers include (1) non-commercial mortality insurance for cattle, carabao, horse, swine, goat and poultry; (2) commercial mortality insurance cover for cattle, carabao, horse, swine, goat and sheep, and poultry; (3) special cover for livestock dispersal; and (4) special cover for game fowls and animals such as fighting cocks and race horses.

The maximum total sum of insurance is less than PhP 110,000 per farmer or PhP 15,000 per head under the non-commercial mortality insurance and PhP110,000 under the commercial mortality insurance. The number of head that may be covered per farmer under non-commercial insurance are: two to 10 for cattle and carabao used for draft, dairy, breeder and fattener; two to 10 for horses used for draft; 20 to 25 for cattle and sheep used as breeder or fattener; two to 10 swine breeders and 7 to 20 swine fatteners. Under the commercial mortality insurance, the number of head are as follows: 11 and more (or at least 1 animal involving coverage of at least Php15,001) for cattle and carabao for draft, dairy, breeder or fattener; minimum of 11 horses for draft; minimum of 26 breeder or fattener goat or sheep; at least 26 swine breeder or at least 21 swine fattener; at least 5,000 broiler chicken, at least 1,000 pullets and layers of chicken and duck. The insurable age are as follows: 7 months to 5 years for cattle and carabao; three to five years for draft horses; four months to one year for goat and sheep; six months to two years for swine breeder; 50 days to 6 months for swine-fattener; 1 day to 8 weeks for broiler chicken, and 1 day to 75 weeks chicken pullets/layers and 12 to 63 weeks for duck pullets/layers. The sum insured and premium rate for commercial and non-commercial covers are listed in Tables 2 and 3.

Table 2. Sum insured and premium rate of livestock under non-commercial cover insurance in the Philippines.

Source: PCIC, 2016.

Notes: 1. For cattle, carabao, and horse: a. above premium rates are applicable for the first/initial coverage; b. for continued annual renewal of the policy (including those renewed within 30 days from the date of expiry, up to the age of 12 years), the assured shall be entitled to the premium rate similar to that of the first/initial coverage, based on the age the animal was first insured; and c. However, if the renewal of the policy was beyond 30 days after the expiry of the policy, the premium rate to be applied shall be based on the age of the animal upon acceptance of the last application. The coverage will be treated as if accepted for the first time.

2. For swine-breeder: premium rates shall depend on personnel handling and managing the animals including the presence of veterinary supervision or livestock inspector/technician, housing, animal husbandry practices, disease prevention and control program, and general health condition of the animals.

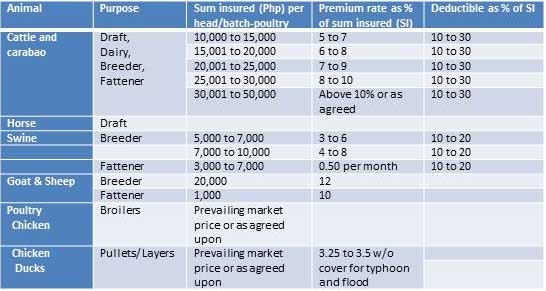

Table 3. Sum insured and premium rate of livestock under commercial cover insurance in the Philippines.

Source: PCIC, 2016

Notes: 1. The above premium rates are subject to change by PCIC.

2. The sum insured and premium rate for commercial cover of horse will be supplied by PCIC.

The risks covered by livestock mortality insurance includes diseases like liver fluke, verminous bronchitis, all other parasitic diseases, leptospirosis, swine enzootic pneumonia, colabacillosis, streptococcosis, tetanus, aflatoxicosis, cancerous diseases, footrot, rabies, poisoning, heat stroke, heart attack and all other diseases except those appearing in the exclusions in the policy. Also covered are accidental drowning, strangulation, snakebites and other events of accidental nature, except those caused by vehicular accidents; fire and lightning (not covered under commercial cover); dog bites for goats and sheep; and accidents arising from transport of animals to and from the farm and place of treatment. For poultry, which is under commercial cover, covered risks include catastrophic losses arising from death of birds due to accidents and/or diseases.

Extended coverage are also available for additional risks subject to some conditions such as inspection, vaccination of susceptible animals and maximum of 60% of sum insured only. The additions entail additional 0.25% of premium per desease of the sum insured. These diseases are, for cattle and carabao: anaplasmosis, anthrax, babesiosis, blackleg, contagious bovine pleuro-pneumonia, Johnne’s disease, hemorrhagic scepticemia, hoof and mouth disease, rinderpest, and tuberculosis. For swine, these are erysipelas, hog cholera, hoof and moth disease, salmonellosis and swine plague. In addition, for transport risk, a transport insurance cover is an option and is limited only to inland transport. For poultry, extended coverage is available for catastrophic losses arising from death due to diseases and epidemic subject to vaccination and inoculation of birds. Losses due to fire, lightning, typhoons and floods can also be covered for cattle, carabao and horses, subject to additional 0.50% premium.

Fisheries insurance program

The fisheries insurance program, pilot tested in 2011, protects fisherfolks against losses in harvested stock due to natural calamities or fortuitous events. Similar with the insurance for rice and corn, the insurance cover the cost of production inputs and the value of labor as per the farm budget plan which is required to be submitted. The period is from stocking up to harvest. The covered risk is limited cover for stock due to natural disasters and extended cover due to fortuitous events. The premium rates depend on the result of evaluation of the type as well as other factors such as agro-climatic conditions and terrain, among others. Individual fish farmers as well as cooperatives and organizations are eligible.

Non-crop agricultural asset insurance program

This program, initially offered in 1996, covers the non-crop agricultural assets, defined as machineries, equipment, transportation facilities and other related infrastructure directly or indirectly used in agricultural activities including production, marketing, processing, storage and distribution of goods and services.

There are three types of cover under this insurance: for fire and lightning cover, risks covered are warehouse risk for agricultural produce, machineries and equipment, industrial risks for processing of agricultural produce, poultry houses, pig pens stables and other similar structures, and other related infrastructure. Similar risks such as typhoons, flood, earthquake may be included in the insurance cover subject to approval by the PCIC. The premium rate is similar to the prevailing industry rates. Another type of insurance is the property floater for tractors, threshers, trailers, shallow tubewells, and other related farm machineries. The premium rate is based on the prevailing rate in the area, but not lower than one percent of the sum insured for initial coverage or the rate is expiring if renewal, subject to a minimum premium of Php 400 per policy. The third type is the commercial car insurance cover, with is for agricultural transport facilities/vehicles used for hauling agricultural products such as trucks and pick-ups. The premium is also based on the prevailing industry practice. The period of cover for all types is a maximum of one year.

Accident and dismemberment security scheme

One unique feature of the agricultural insurance in the Philippines is the accident and dismemberment security scheme offered to agricultural producers, fisherfolks and other stakeholders, preferably with existing agricultural insurance, covering death or dismemberment due to accident. These are term insurance packages opened in 2005. Other family members are also eligible. Two types of insurance plans are available: individual and group plan for ages 15 and 70 years old, and family plan, for 12 years to 70 years old. Insurance is for one year. Covered risks are death due to accident, loss of body parts due to accident.

Special insurance programs

The Rice Crop Insurance for the DA Weather Adverse Areas (WARA) Insurance Program aims to encourage farmers in climate change-affected areas to produce rice. For farms to be eligible, these must be duly identified and verified by the DA. Standard premium rates in the area shall apply, and the amount of cover is PhP 10,000/ha.

-

The Rice Corp Insurance for DA-LBP SIKAT SAKA Program is a free insurance for subsistence farmers participating in the DA-LBP Sikat-Saka Program (SSP) in 45 major rice producing provinces in the country. This is a credit component of the Food Staples Sufficiency Program of the DA, where LBP is the lending conduit. The amount of cover is up to the amount of loan granted by the LBP.

-

The Agricultural Insurance Program for farmers and fisherfolks listed in the registry system for basic sectors in agriculture (RSBSA) is an insurance for farmers listed in the registry who are not receiving any other subsidy for similar types of insurance, and most importantly have insurable interest in the farm. The amount of cover is equal to the actual amount of loan for borrowing farmers or a maximum of PhP 20,000 per hectare for rice and corn insurance programs or for other insurance programs, the amount of cover is computed in accordance with guidelines and procedures subject to limits of coverage per farmer/fisherfolk as specified in the program. This program was implemented for insurance policies incepting from January 1 2015 to December 31, 2015.

-

The Agricultural Insurance for Agrarian Reform Beneficiaries (ARBs) participating in the Agrarian Production Credit Program (APCP) and Credit Assistance Program for Program Beneficiaries Development (CAP-PBD) is a 100% premium subsidy for the cost of insurance coverage of the participating ARBs in the financing programs implemented by the DA, DAR and LBP. The insurance covers all the regular insurance products implemented by the PCIC.

-

Finally, the agricultural insurance program for subsistence farmers and fisherfolks directly hit by typhoon Yolanda or Haiyan is a full premium subsidy provided by the PCIC for insurance coverage of farm investments and Accident and Dismemberment Security Scheme in areas directly hit by the typhoon. These are the areas in Region 6, 7 and 8. The amount of cover is equal to the actual amount of loan for borrowing farmers or a maximum of Php 20,000 per hectare for rice and corn insurance programs or for other insurance programs, the amount of cover is computed in accordance with guidelines and procedures subject to limits of coverage per farmer/fisherfolk as specified in the program.

Issues on Agricultural Insurance Programs

Most of the insurance programs described earlier are subsidized by the government. In the sharing of premium among the farmer, lending institution and the government, the latter that pays the highest as indicated in the premium sharing in Table 1. Even with this scenario, the insurance penetration ratio remained low especially for rice and corn insurance programs.

A study by Reyes et al. (2015) found the following issues surrounding the agricultural insurance in the country: low awareness among farmers on the insurance lines of the PICC and their terms and conditions, the issue on the assessment of the damages when claiming indemnity, the low penetration rates particularly for rice and corn insurance. Operational issues were also noted, among them the ad hoc nature of implementing the special insurance programs which tended to have discontinuous funding.

Issues on high administrative and operating costs that constrained the profitability of PICC were also noted by the study conducted by the Congressional Policy and Budget Research Department (2013). Other issues included funding deficiencies that affect the operations of the PCIC that lead to unpaid government equity share and under-delivered or undelivered premium subsidies.

Conclusions and policy implications

Agriculture has been subjected to risks arising from problems related to production, prices and natural disasters. Risk management has been a key concern to farmers, hence, agricultural insurance in the country has been established and supported through policies that created the Philippine Crop Insurance Corporation. The policies have clearly stipulated the provision of insurance, an instrument to manage risk, to protect the farmers against losses from natural calamities, plant diseases and pests infestations. The insurance that originally covered staple foods such as rice and corn was expanded to include livestock, fisheries, non-crop agricultural assets, high value commercial crops and accident and dismemberment security scheme.

While the government provides for various insurance windows for the farmers and pays the highest fee in the premium sharing of insurance, there were issues that impede the availment of insurance in agriculture. Policies are then created to further strengthen and improve the provisions of agricultural insurance in the country.

To strengthen PCIC, efforts are being made to amend or revise the agricultural insurance law in the country. Some of the bills filed in Philippine Congress are:

-

An Act Further Amending Presidential Decree No. 1467, As Amended, Otherwise Known As The Charter of the Philippine Crop Insurance Corporation, In Order To Expand And Improve Agricultural Insurance In The Philippines And Promote Small Agricultural Producers Resilience to Climate Change. The salient features of the bill are the inclusion of reinsurance arrangement with agricultural cooperatives and other agricultural organizations.

-

An Act Strengthening the Philippine Crop Insurance Corporation System by Expanding Its Program Coverage, Increasing Its Funding Source and Imposing Heavier Penalties on Spurious Claims, Amending Presidential Decree No. 1467, As Amended, Otherwise Known As The Charter Of The Philippine Crop Insurance Corporation (PCIC). The proposed law authorizes PICC to seek all funding sources, including earmarked funding from revenue generating institutions like PCSO and the PAGCOR. It also proposes the inclusion of the Secretary of Department of Agrarian Reform in the Board of Directors.

-

An Act Establishing The State Agricultural Guarantee And Insurance Protection Funds (SAGIP Funds), Creating the State Agricultural Guarantee and Insurance Protection Corporation (SAGIPCo), Defining Its Objectives, Powers, Functions, Providing Funds Therefore And For Other Purposes. The provisions include creation of the State Agricultural Guarantee and Insurance Protection Corporation (SAGIPCo) to provide social security services to farmers/fisherfolk such as like crop insurance, loan guarantee, life insurance among others. The bill also provides that the PCIC’s and Quedancor’s operations will be integrated into the SAGIPCo.

-

An Act Further Amending Presidential Decree No. 1467, Otherwise Known as the Philippine Crop Insurance Corporation Decree and Republic Act No. 8175, Otherwise Known As The Revised Charter Of The Philippine Crop Insurance Corporation (PCIC) to include agro-forestry crops and forest plantations, as well as non-crop agricultural insurance for forest plantation machineries and related infrastructures.

-

An Act Providing For A More Comprehensive Protection Program Against Loss of Lives And Properties Due To Natural Disasters And Similar Acts of Nature, Amending Presidential Decree No. 1467 Otherwise Known As The Charter Of The “Philippine Crop Insurance Corporation” To Embody The Elaborations Within Its Powers And Responsibilities, Providing Funds Therefor, Changing Its Corporate Name To “Philippine Catastrophe Insurance and Reinsurance Corporation” And For Other Purposes. The proposed bill aims to provide insurance/reinsurance protection to participating persons and develop and implement guarantee programs and such other collateral substitute schemes as may be necessary to encourage banks and other institutional sources of funds to lend to small entrepreneurs.

-

An Act Authorizing the Grant of a Full Crop Insurance Coverage to Qualified Beneficiaries of the Comprehensive Agrarian Reform Program Amending for the Purpose Section 14 of R.A. 9700 Otherwise Known as the “Comprehensive Agrarian Reform Program Extension with Reforms” aims to provide full cost of insurance to the qualified beneficiaries of the Comprehensive Agrarian Reform Program. Other amendments include authorize PCIC to insure government properties belonging to agencies/bureaus in agri-fisheries sector, authorizing PCIC to engage in reinsurance of agri-fisheries risks and compulsory insurance coverage of all government financed-projects in the agri-fisheries sector.

References

Mamhot P.C.T. and Bangsal, N.V. 2012. Review of the Philippine Crop Insurance: Key Challenges and Prospects. Congressional Policy and Budget Research Department. House of Representatives. Congress of the Philippines. Quezon City, Philippines.

Philippine Corp Insurance Corporation. 2016. www.pcic.gov.ph. Accessed April 1, 2016.

Reyes M.R. 2015. Review of Design and Implementation of the Agricultural Insurance Programs of the Philippine Corp Insurance Corporation. Discussion Paper Series No. 2015-07. Philippine Institute for Development Studies. Makati City, Philippines.

|

Date submitted: April 27, 2016

Reviewed, edited and uploaded: April 28, 2016

|

[1] Policy paper submitted to the Food and Fertilizer Technology Center (FFTC) for the Asian and Pacific Region for the project titled “Asia-Pacific Information Platform in Agricultural Policy”. Policy papers, as corollary outputs of the project, describe pertinent Philippine laws and regulations on agriculture, aquatic and natural resources.

[2] Senior Science Research Specialist, Socio-Economics Research Division-Philippine Council for Agriculture, Aquatic and Natural Resources Research and Development (SERD-PCAARRD) of the Department of Science and Technology (DOST), Los Baños, Laguna, Philippines.

Agricultural Insurance in the Philippines

Introduction

Insurance is an instrument that is used to manage risks. In agriculture, insurance is a tool used to manage risks arising from the production of commodities, price variability, as well as climate and weather uncertainties. Risks from production is normally addressed by technological advances such as new varieties and other technological innovations. Risks arising out of price variability is generally addressed at the policy and market levels. The most important risk that is difficult to control is the risk against adverse weather conditions, or now also due to climate change.

In the Philippines, agricultural insurance is availed of by farmers also as a credit reduction mechanism, as a surrogate capital or substitute for physical capital (PICC, 2016). Lending institutions require agricultural insurance from farmer borrowers. Crop insurance facilitate credit access especially in formal lending institutions like the Land Bank of the Philippines.

This paper describes the current agricultural insurance system in the Philippines. The first section is a discussion of the legal framework for agricultural insurance programs by the government. The second section describes in detail the various agricultural insurance products and programs. The last section examines some of the issues besetting the Philippine agricultural insurance industry and the proposed legislations for the improvement of insurance delivery.

Legal framework of the agricultural insurance in the Philippines

The Philippine agricultural insurance is supervised by the Philippine Crop Insurance Corporation (PCIC), a government owned and controlled corporation under the Department of Agriculture. PCIC was created through Presidential Decree 1467 Creating the “Philippine Crop Insurance Corporation” Prescribing Its Powers and Activities, Providing for its Capitalization and for the Required Government Premium Subsidy and for Other Purposes,” and was passed into law in 1978. The main purpose of the insurance was “to provide insurance protection to farmers against losses arising from natural disasters, plant diseases and pest infestations initially for palay crops and later to other crops.” PD 1467 was later amended by Presidential Decree 1733 in 1980 and Republic Act 8175 An Act Further Amending Presidential Decree No. 1467, As Amended, Otherwise Known as the Charter of the Philippine Crop Insurance Corporation (PCIC) in Order to Make the Crop Insurance System More Stable and Beneficial to the Farmers Covered Thereby and for the National Economy, in 1995.

According to the laws, insurance of qualified farmers are against losses arising from natural calamities, plant diseases and pest infestations. Initially, the law stipulates that PCIC provide insurance coverage for rice crops, and has provisions for expansion to other crops as well as other non-agricultural assets such as machineries equipment, transport facilities and other related infrastructures. The laws mandate that the insurance shall cover the cost of production inputs, the value of the farmer's own labor and those of the members of his household, including the value of the labor of hired workers, and a portion of the expected yield, but excluding losses arising from “avoidable risks due to negligence, malfeasance or fraud committed by the insured or any member of his immediate farm household or employee or the failure of the insured to follow proven farm practices."

The PCIC is given the free hand to determine the premium rates, as well as the allocated sharing among farmers, lending institutions and the government. Only subsistence farmers cultivating not more than 7 hectares are covered by the government share of premium.

Types of Philippine agricultural insurance products and programs

Currently, there are seven insurance products and five insurance programs being administered and implemented by the PCIC. The seven insurance products are:

The five insurance programs are:

Insurance for crops

The agricultural insurance for rice was first offered in in 1981, followed by coverage for corn in 1982 and high value commercial crops (HVCC), starting in 1991 for tobacco and expanded in 1993 to cover other commodities.

Under these products, the objects of the insurance are the standing rice, corn, and HVCC. The insurance covers the cost of production of inputs including labor, plus an optional additional amount of cover of up to 20% of cover portion for rice and corn and 120% of the expected yield for HVCC.

For rice and corn, the cover ceilings vary depending on the type of seeds used: for rice, PhP 41,000[3]/ha for inbred varieties, PhP 50,000/ha for seed production of inbred varieties as well as for commercial production (F1) of hybrid varieties, and PhP 65,000/ha for seed production of hybrid varieties. For corn, the cover ceilings are PhP 40,000/ha for hybrid varieties and PhP 28,000/ha for open-pollinated varieties. All farms using the National Seed Industry Council varieties are insurable. The period of cover is from seeding to harvesting. The premium rates vary depending on the region (location), season, and risk classification, and is shared by the farmer, lending institution and the government (Table 1).

For HVCC, crops such as abaca, “ampalaya”, asparagus, banana, cabbage, carrot, cassava, coconut, coffee, commercial trees, cotton, garlic, ginger, mango, mungbean, onion, papaya, peanut, pineapple, sugarcane, sweet potato, tobacco, tomato, water melon, white potato, and others are covered, subject to their feasibility. In contrast to rice and corn, the insurance premium for HVCC shall be market-rated and shall be borne solely by the farmer, and the premium rate ranging from 2% to 7% depending on the pre-coverage evaluation and other factors such as agro-climatic conditions, type of soil, terrain, and other location specific factors.

Table 1. National composite rates and premium sharing (%) for rice and corn insurance in the Philippines.

Source: PCIC, 2016.

The insurance covers risks as natural disasters such as typhoons, floods, drought, earthquakes, and volcanic eruptions, plant diseases, pests infestations and accidental fire for HVCC.

For the settlement of claims, verification and loss assessments are made by a team of adjusters who will assess the loss category and amount of indemnity. Insured farmers have a no-claim benefit of 10% of the farmer’s net premium shared paid for three consecutive crop seasons not subject of any claim.

Livestock insurance program

The livestock insurance program started in 1988 through a tie-up with Philippine Livestock Management Services Corporation. The insurance covers for livestock are for cattle, carabao, horse, swine, goat, poultry, and game fowls and animals, covering death due to accidents, diseases and other risks. The types of insurance covers include (1) non-commercial mortality insurance for cattle, carabao, horse, swine, goat and poultry; (2) commercial mortality insurance cover for cattle, carabao, horse, swine, goat and sheep, and poultry; (3) special cover for livestock dispersal; and (4) special cover for game fowls and animals such as fighting cocks and race horses.

The maximum total sum of insurance is less than PhP 110,000 per farmer or PhP 15,000 per head under the non-commercial mortality insurance and PhP110,000 under the commercial mortality insurance. The number of head that may be covered per farmer under non-commercial insurance are: two to 10 for cattle and carabao used for draft, dairy, breeder and fattener; two to 10 for horses used for draft; 20 to 25 for cattle and sheep used as breeder or fattener; two to 10 swine breeders and 7 to 20 swine fatteners. Under the commercial mortality insurance, the number of head are as follows: 11 and more (or at least 1 animal involving coverage of at least Php15,001) for cattle and carabao for draft, dairy, breeder or fattener; minimum of 11 horses for draft; minimum of 26 breeder or fattener goat or sheep; at least 26 swine breeder or at least 21 swine fattener; at least 5,000 broiler chicken, at least 1,000 pullets and layers of chicken and duck. The insurable age are as follows: 7 months to 5 years for cattle and carabao; three to five years for draft horses; four months to one year for goat and sheep; six months to two years for swine breeder; 50 days to 6 months for swine-fattener; 1 day to 8 weeks for broiler chicken, and 1 day to 75 weeks chicken pullets/layers and 12 to 63 weeks for duck pullets/layers. The sum insured and premium rate for commercial and non-commercial covers are listed in Tables 2 and 3.

Table 2. Sum insured and premium rate of livestock under non-commercial cover insurance in the Philippines.

Source: PCIC, 2016.

Notes: 1. For cattle, carabao, and horse: a. above premium rates are applicable for the first/initial coverage; b. for continued annual renewal of the policy (including those renewed within 30 days from the date of expiry, up to the age of 12 years), the assured shall be entitled to the premium rate similar to that of the first/initial coverage, based on the age the animal was first insured; and c. However, if the renewal of the policy was beyond 30 days after the expiry of the policy, the premium rate to be applied shall be based on the age of the animal upon acceptance of the last application. The coverage will be treated as if accepted for the first time.

2. For swine-breeder: premium rates shall depend on personnel handling and managing the animals including the presence of veterinary supervision or livestock inspector/technician, housing, animal husbandry practices, disease prevention and control program, and general health condition of the animals.

Table 3. Sum insured and premium rate of livestock under commercial cover insurance in the Philippines.

Source: PCIC, 2016

Notes: 1. The above premium rates are subject to change by PCIC.

2. The sum insured and premium rate for commercial cover of horse will be supplied by PCIC.

The risks covered by livestock mortality insurance includes diseases like liver fluke, verminous bronchitis, all other parasitic diseases, leptospirosis, swine enzootic pneumonia, colabacillosis, streptococcosis, tetanus, aflatoxicosis, cancerous diseases, footrot, rabies, poisoning, heat stroke, heart attack and all other diseases except those appearing in the exclusions in the policy. Also covered are accidental drowning, strangulation, snakebites and other events of accidental nature, except those caused by vehicular accidents; fire and lightning (not covered under commercial cover); dog bites for goats and sheep; and accidents arising from transport of animals to and from the farm and place of treatment. For poultry, which is under commercial cover, covered risks include catastrophic losses arising from death of birds due to accidents and/or diseases.

Extended coverage are also available for additional risks subject to some conditions such as inspection, vaccination of susceptible animals and maximum of 60% of sum insured only. The additions entail additional 0.25% of premium per desease of the sum insured. These diseases are, for cattle and carabao: anaplasmosis, anthrax, babesiosis, blackleg, contagious bovine pleuro-pneumonia, Johnne’s disease, hemorrhagic scepticemia, hoof and mouth disease, rinderpest, and tuberculosis. For swine, these are erysipelas, hog cholera, hoof and moth disease, salmonellosis and swine plague. In addition, for transport risk, a transport insurance cover is an option and is limited only to inland transport. For poultry, extended coverage is available for catastrophic losses arising from death due to diseases and epidemic subject to vaccination and inoculation of birds. Losses due to fire, lightning, typhoons and floods can also be covered for cattle, carabao and horses, subject to additional 0.50% premium.

Fisheries insurance program

The fisheries insurance program, pilot tested in 2011, protects fisherfolks against losses in harvested stock due to natural calamities or fortuitous events. Similar with the insurance for rice and corn, the insurance cover the cost of production inputs and the value of labor as per the farm budget plan which is required to be submitted. The period is from stocking up to harvest. The covered risk is limited cover for stock due to natural disasters and extended cover due to fortuitous events. The premium rates depend on the result of evaluation of the type as well as other factors such as agro-climatic conditions and terrain, among others. Individual fish farmers as well as cooperatives and organizations are eligible.

Non-crop agricultural asset insurance program

This program, initially offered in 1996, covers the non-crop agricultural assets, defined as machineries, equipment, transportation facilities and other related infrastructure directly or indirectly used in agricultural activities including production, marketing, processing, storage and distribution of goods and services.

There are three types of cover under this insurance: for fire and lightning cover, risks covered are warehouse risk for agricultural produce, machineries and equipment, industrial risks for processing of agricultural produce, poultry houses, pig pens stables and other similar structures, and other related infrastructure. Similar risks such as typhoons, flood, earthquake may be included in the insurance cover subject to approval by the PCIC. The premium rate is similar to the prevailing industry rates. Another type of insurance is the property floater for tractors, threshers, trailers, shallow tubewells, and other related farm machineries. The premium rate is based on the prevailing rate in the area, but not lower than one percent of the sum insured for initial coverage or the rate is expiring if renewal, subject to a minimum premium of Php 400 per policy. The third type is the commercial car insurance cover, with is for agricultural transport facilities/vehicles used for hauling agricultural products such as trucks and pick-ups. The premium is also based on the prevailing industry practice. The period of cover for all types is a maximum of one year.

Accident and dismemberment security scheme

One unique feature of the agricultural insurance in the Philippines is the accident and dismemberment security scheme offered to agricultural producers, fisherfolks and other stakeholders, preferably with existing agricultural insurance, covering death or dismemberment due to accident. These are term insurance packages opened in 2005. Other family members are also eligible. Two types of insurance plans are available: individual and group plan for ages 15 and 70 years old, and family plan, for 12 years to 70 years old. Insurance is for one year. Covered risks are death due to accident, loss of body parts due to accident.

Special insurance programs

The Rice Crop Insurance for the DA Weather Adverse Areas (WARA) Insurance Program aims to encourage farmers in climate change-affected areas to produce rice. For farms to be eligible, these must be duly identified and verified by the DA. Standard premium rates in the area shall apply, and the amount of cover is PhP 10,000/ha.

Issues on Agricultural Insurance Programs

Most of the insurance programs described earlier are subsidized by the government. In the sharing of premium among the farmer, lending institution and the government, the latter that pays the highest as indicated in the premium sharing in Table 1. Even with this scenario, the insurance penetration ratio remained low especially for rice and corn insurance programs.

A study by Reyes et al. (2015) found the following issues surrounding the agricultural insurance in the country: low awareness among farmers on the insurance lines of the PICC and their terms and conditions, the issue on the assessment of the damages when claiming indemnity, the low penetration rates particularly for rice and corn insurance. Operational issues were also noted, among them the ad hoc nature of implementing the special insurance programs which tended to have discontinuous funding.

Issues on high administrative and operating costs that constrained the profitability of PICC were also noted by the study conducted by the Congressional Policy and Budget Research Department (2013). Other issues included funding deficiencies that affect the operations of the PCIC that lead to unpaid government equity share and under-delivered or undelivered premium subsidies.

Conclusions and policy implications

Agriculture has been subjected to risks arising from problems related to production, prices and natural disasters. Risk management has been a key concern to farmers, hence, agricultural insurance in the country has been established and supported through policies that created the Philippine Crop Insurance Corporation. The policies have clearly stipulated the provision of insurance, an instrument to manage risk, to protect the farmers against losses from natural calamities, plant diseases and pests infestations. The insurance that originally covered staple foods such as rice and corn was expanded to include livestock, fisheries, non-crop agricultural assets, high value commercial crops and accident and dismemberment security scheme.

While the government provides for various insurance windows for the farmers and pays the highest fee in the premium sharing of insurance, there were issues that impede the availment of insurance in agriculture. Policies are then created to further strengthen and improve the provisions of agricultural insurance in the country.

To strengthen PCIC, efforts are being made to amend or revise the agricultural insurance law in the country. Some of the bills filed in Philippine Congress are:

References

Mamhot P.C.T. and Bangsal, N.V. 2012. Review of the Philippine Crop Insurance: Key Challenges and Prospects. Congressional Policy and Budget Research Department. House of Representatives. Congress of the Philippines. Quezon City, Philippines.

Philippine Corp Insurance Corporation. 2016. www.pcic.gov.ph. Accessed April 1, 2016.

Reyes M.R. 2015. Review of Design and Implementation of the Agricultural Insurance Programs of the Philippine Corp Insurance Corporation. Discussion Paper Series No. 2015-07. Philippine Institute for Development Studies. Makati City, Philippines.

Date submitted: April 27, 2016

Reviewed, edited and uploaded: April 28, 2016

[1] Policy paper submitted to the Food and Fertilizer Technology Center (FFTC) for the Asian and Pacific Region for the project titled “Asia-Pacific Information Platform in Agricultural Policy”. Policy papers, as corollary outputs of the project, describe pertinent Philippine laws and regulations on agriculture, aquatic and natural resources.

[2] Senior Science Research Specialist, Socio-Economics Research Division-Philippine Council for Agriculture, Aquatic and Natural Resources Research and Development (SERD-PCAARRD) of the Department of Science and Technology (DOST), Los Baños, Laguna, Philippines.

[3] 1 US$ = PhP 42.00