Joo-Ho Song and Han-Phil Moon

Korea Rural Economic Institute(KREI), Hoigi, Seoul, South Korea

e-mail: jhsong@krei.re.kr

ABSTRACT

During the past 10 years since the signing of an FTA with Chile in 2002, Korea has signed 10 FTAs with 47 countries. As of July 2012, negotiations for FTAs are underway in Korea with 11 countries including China, Canada, Australia and New Zealand. For the agricultural sector which is expected to suffer damages due to the FTAs, the government has made a plan to compensate damages in the short term and improve agriculture`s competitiveness in the medium and long term. The Korean government introduced an FTA direct payment for damage compensation for some fruits right after KOR-CHILE FTA in 2004, the coverage of which has been expanded to all products after KOR-US FTA in 2012. The FTA Direct Payment for KOR-CHILE FTA has not been paid at all, but this year it is likely to be paid for some products for KOR-US FTA. However, whether to consider the share of FTA effects on the price drop to determine the payment rate remains to be solved. This first experience in paying FTA direct payment gave warning to the policy makers that compensation measures should be designed carefully.

Key Words: FTA, WTO, direct payment, compensation measure

INTRODUCTION

South Korea is one of the biggest beneficiaries of the multilateral trade system, of which the most typical example is the World Trade Organization (WTO), and the country is often quoted as a role model for having made economic progress through trade[1]. Recently, Korea has been actively seeking free trade agreements. The reason is that, amid the globally expanding regionalism, it hopes to minimize any damages it could suffer for being an outsider to the “FTA network” and actively respond to such challenges, while advancing the national systems in general and strengthening the economic competitiveness through proactive market opening and liberalization (MOFAT 2011). In promoting the FTAs, agricultural sector was considered as the weak point because Korean agriculture has relatively low competitiveness in the international market. Thus, the basic strategy for FTA is to maximize the benefit of free trade in industrial goods and to minimize the negative impact on agriculture.

During the past 10 years since the signing of an FTA with Chile in 2002, Korea has signed 10 FTAs with 47 countries. In addition to Chile, Korea signed an FTA with Singapore (November 2004), four Europe countries (EFTA, July 2005), 10 ASEAN members (April 2006), India (September 2008) and the US (originally signed in April 2007 but revised in December 2010 after renegotiation), 27 EU members (October 2009), Peru (August 2010) and Turkey (March 2012). The FTAs with these countries have already went into effect and the FTAs with Columbia (June 2012) is signed and yet to be ratified by their respective legislature.

As of August 2013, negotiations for FTAs are underway with China, Vietnam and Indonesia. Korea also joined RCEP (Regional Comprehensive Economic Partnership) that consisted of ASEAN +6 (China, Japan, Korea, Australia, New Zealand and India) countries and China-Japan-Korea FTA was launched May, 2013. The first official talk for an FTA with China began in May 2012, and the negotiation is being carried out in two phases. In the first phase, the two sides discuss the modality in goods, services, and investments sectors and especially how to deal with sensitive products. Only when the two sides agree on the modality will the second phase of negotiations begin[2] which will be single- undertaking.

Korea is trying to resume FTAs which already started but now suspended with Japan, Canada, Mexico, Australia, New Zealand, and the six countries of the Gulf Cooperation Council (GCC). Other than these countries, the countries with which Korea has concluded a joint research or is in the middle of creating favorable conditions are four countries of MERCOSUR, Israel, Malaysia and five countries in Middle America (MTIE, 2013).

Of the total amount of Korea's agricultural import (US$22billion, 2012), the share of trade with FTA partners including the US, EU, ASEAN, and Chile reached 50%. If the current talks for FTA come to fruition as planned, more than 90% of Korea's agricultural imports would be coming from FTA partners.

.jpg)

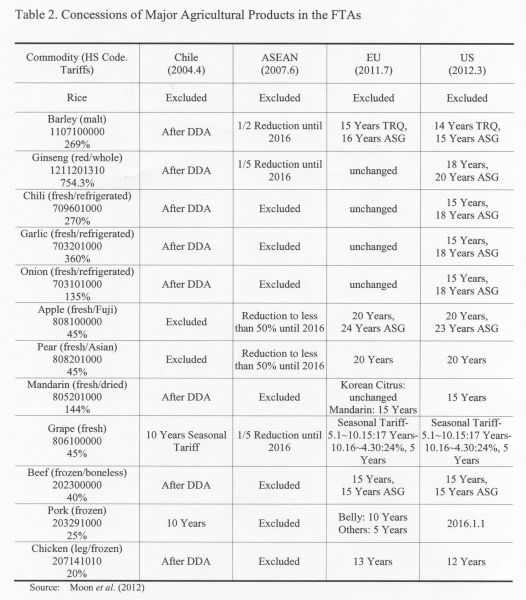

The average bound tariff rate of Korean agricultural products is 63.8%, and Korea has maintained the principle of seeking concession exemptions or partial market opening of major agricultural products in consideration of the unique position Korean agriculture holds in FTA negotiations. It is evaluated that in the case of FTAs with Chile and the ASEAN, which were concluded in the early days, and FTAs with countries that are not big exporters of agricultural products, the extent of market opening was considerably low. As for the tariffs on products that had little impact on the domestic market or those that the country already relied on to meet most of its demand, tariff concessions were made in such a way that tariffs could be abolished early.

However, in the case of the recently concluded Korea-US FTA, a relatively high level of concessions was made. Also, a similar result was obtained in the Korea-EU FTA, which was signed after the conclusion of negotiations with the US.

Korea excluded rice from the concessions list in all FTAs, and as for other sensitive products, it strived to minimize damages from the market opening through such means as retention of current tariffs, TRQ offers, introduction of seasonal tariffs, partial abolition of tariffs or extension of abolition period, and agreement on safeguards (ASG).

Preliminary Estimation of FTA Impact on Agriculture

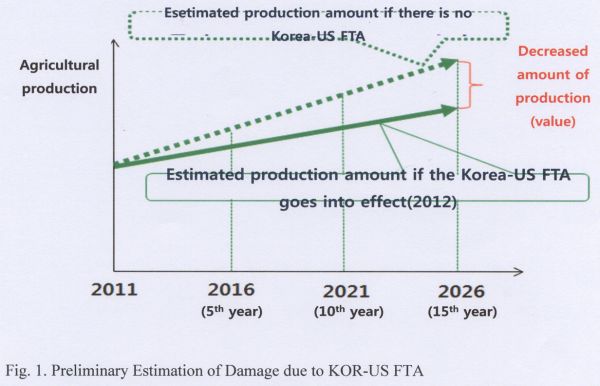

The amount of damage to the domestic agriculture that could result from the Korea-US FTA was estimated using the simulation model KASMO-2008 developed by the Korea Rural Economic Institute.

Using the data from 1980 to 2008, and under the premise that no Korea-US FTA was signed and that such a market condition continued, the amount of agricultural production was estimated for the period ending in 2026. With the amount set as the baseline, a policy simulation was made wherein the Korea-US FTA goes into effect on January 1, 2012, and a tariff reduction schedule was applied according to the concession agreement.

For each item on the concessions list, the following aspects were considered: 1) the substitution effect between the imported product and the domestic kind; 2) import substitution effect between the US and other countries; 3) demand substitution effect between commodities, and 4) competition effect in production for finite arable land.

The simulation results showed that if the Korea-US FTA goes into effect, agricultural production in Korea is estimated to decrease by Korean won 678.5 billion in the 5th year after the agreement's enforcement, Korean won 991.2 billon in the 10th year, and Korean won 1 trillion 235.4 billion in the 15th year. Damage is predicted to be big especially in the livestock sector. In the 15th year, the damage is estimated to be Korean won 443.8 billion in the case of beef, Korean won 208.5 billion in the case of pork, and Korean won 108.7 billion in the case of chicken (Choi, 2011).

Policy Response to FTAs : Compensation Measures

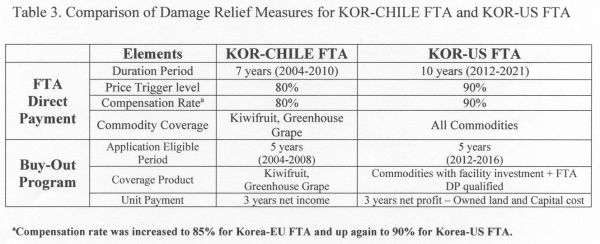

For the agricultural sector which is expected to suffer damages due to the FTA, the government has made a plan to compensate damages in the short term and improve agriculture's competitiveness in the medium and long term. For the first FTA with Chile, the Korean government introduced an FTA direct payment (FTA DP) for damage compensation and a buyout program for some fruits (kiwi and house-grown grape) which were expected to be affected mostly because Chile is a fruit exporter. The FTA DP was designed to be paid only when agricultural import from an FTA partner increases and subsequently the price falls. If the market price of a product in a given year is less than 80% of the average price (basis price) of three years in the past five years excluding the years with the highest and lowest price, then farmers are awarded 80% of the difference between the basis price and the market price. The requirement for the FTA DP is

(i) when the price in a given year falls below the basis price, and

(ii) when the total import volume and the import volume from the FTA partner in a given year exceed the basis volume, which is calculated as the Olympic average of the previous five years[3].

The support amount is calculated as follows:

* Support amount = cultivated area of the product× national average production amount per unit area × DP rate × adjustment factor

Here, DP rate = (basis price - price in the given year) × compensation rate (80%)

Basis price = three-year average excluding the highest and lowest price in the past five years×80%

Adjustment factor=policy variable for payment within the permitted range[4] set by the WTO

The compensation for business closure (buyout program) is limited to some fruits (kiwi, house-grown grape and peach) farms. The level of payment is three years worth of net income (=gross income – production cost – self-labor). The application period was five years from the start of the FTA.

There had not been strong resistance from the agricultural sector about subsequent FTAs until 2006 because the FTA partners for Korea during 2004-2006 were not big exporters or the concession level was not so high. However, KOR-US FTA in 2007 was different. Korea opened the domestic market for agricultural commodities except rice and the US is the biggest exporter of agricultural products. Thus, the Korean government augmented previous supplementary measures to soothe angry farmers such that the range of products for damage compensation shall be expanded to include all products (previously, only kiwis and green house-grown grapes were eligible for the direct payment and the buyout program was limited to kiwis, green house-grown grapes and peaches) that actually suffer damages and that the compensation rate, as well as the basis price, shall be increased to 90% from 80%. The improved measure is the result of embracing the farmers’ suggestion that the trigger level should be lowered in the National Assembly during the ratification process. But it caused many unexpected problems in determining the actual payment rate. The operation period of the direct payment for damage compensation is 10 years from the start of the FTA.

The compensation for business closure for KOR-US FTA becomes tougher compared with KOR-CHILE FTA. It is limited to those cases where facility investment is made for products that have met the requirements for direct payment, and the level of compensation is three years’ worth of net profit (= net income – cost of owned land and capital), which is lower than that of KOR-CHILE Buyout Program. The compensation period is five years from the start of the FTA. Such a change was taken to rectify the excessive support that was given to the producers of agricultural products, such as peach, that had not been directly affected by imports.

In addition, the direct payment for upland (non-rice) farming was newly introduced[5] by the Korean National Assembly, and it is expected to cause much difficulty in the implementation stage since it is not easy to confirm the target fields of each farm household and the administrative cost is very high. These modified FTA DP and buyout programs apply to all FTAs.

Evaluation of FTA Implementation and Compensation measures

Korea-Chile Agricultural Trade Trends

The trade amount of agricultural and livestock products between Korea and Chile has grown five-fold from US$50 million in 2003 when there was no free trade agreement between the two countries to US$250 million in 2010. The export amount of Korea's agricultural products and foods in 2010 was only US$900,000.

After the entry into force of the Korea-Chile FTA, the annual growth rate of agricultural imports from Chile was very high at 20% on average. Especially in the case of Chilean fruits which are competitive in international markets, the growth rate reached 29%. The products that saw a big increase in import as a result of the FTA are grape, kiwifruit, wine, and pork. The share of each one of these Chilean fruits in the total imported fruit market also increased sharply (grape 70% share, kiwifruit 13%, wine 22%, and pork 16% share as of 2010).

The target products for direct payment in response to the Korea-Chile FTA are kiwifruit and greenhouse grapes. After the entry into force of the FTA, the amount of imported kiwifruit and grapes all increased, but the price of kiwifruit increased instead of decreasing, and in the case of grapes, the direct payment was not provided because it did not meet the requirement of more than 20% drop from the basis price even though the price fell.

Korea’s Agricultural Trade with EU and US.

Changes in the amount and price of imported agricultural products were observed in 2012. The Korea-EU FTA was effective from July 1, 2011, and Korea-US FTA went into effect on March 15, 2012. Thus, for the Korea- US FTA, the relevant data were adjusted considering the period of January 1 to March 14. In 2012, it looks like that the direct payment for damage compensation will not be implemented for most of the covered products because there is little product that meets all the three requirements, which are 1) increase in total amount of import, 2) increase in the amount of import from the FTA partner, and 3) price drop. If the import increase was mainly from non-FTA partners, then Direct Payment will not be paid even when the requirement 1) is met.

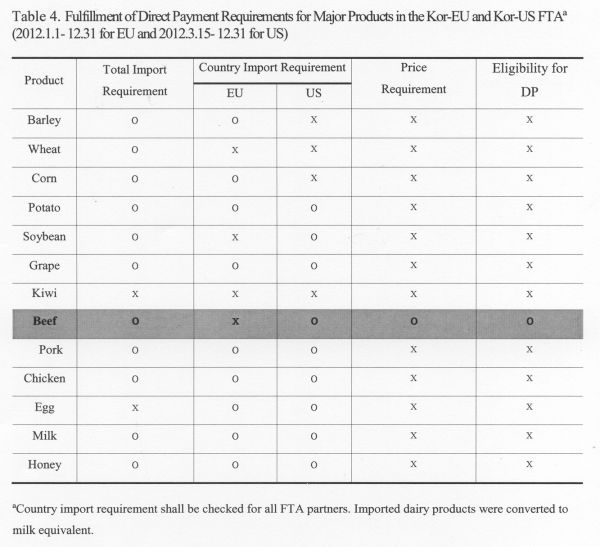

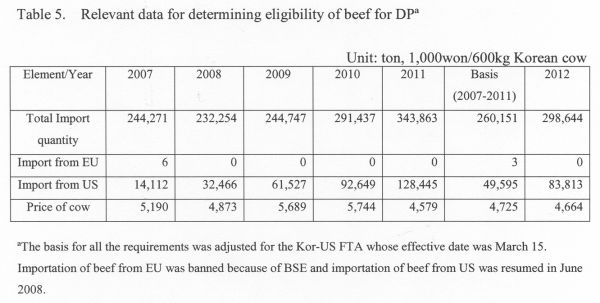

For major commodities in Table 4, most commodities satisfied the requirement of total import and the country import requirement. The exceptions are wheat, kiwi and eggs. In the case of wheat, the total import requirement was met, but that import increase was mainly from Brazil which is not an FTA partner. The total import requirement was not satisfied in the case of kiwi and eggs. However, even though most commodities satisfied both the total import and country import requirements, they could not meet the price drop requirement except for beef.

Thus, beef is the only eligible product for the FTA compensation direct payment in 2012.

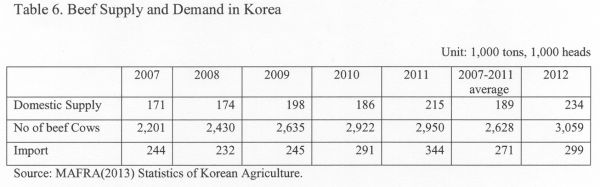

But when we scrutinize the case of beef, domestic supply in 2012 increased by 24% compared with the previous five-year (2007-2011) average and import quantity increased by only 10.3% compared with the previous five-year average. The impact of first year of Korea- US FTA was only 2.7% tariff reduction in beef (from 40% to 37.3%). Thus, it is most likely that the main reason of beef price drop in 2012 below the basis price level was due to the increase in domestic supply rather than import surge. Too many beef cows (3,059 thousand heads in 2012) resulted in the over-supply of domestic beef.

Determining the share of import impact on price drop.

The direct payment for beef can be calculated as follows.

DP rate = (basis price - price in the given year) × compensation rate (90%)

= (4,725,000 – 4,664,000) × 90% = 54,900/600 kg cow

But because it is hard to deny that the decrease in the beef price (actually cow price) in 2012 resulted mainly from the oversupply of domestic beef, the government decided to apply the share of the impact of import increase to the price drop to calculate the amount of DP to be paid. There are arguments on the DP rate whether to consider additionally the share of impact of import increase to price changes. In the relevant law, there is no regulation to calculate this share. Farmers’ groups and some politicians insist that the government should pay a full DP rate and should not segregate the impact of import increase and impact of domestic oversupply on price drop.

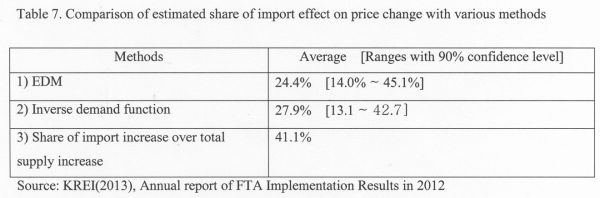

There can be several methods to calculate the share of the import impact on the price drop. First, one economically plausible way is to use the comparative static approach which is commonly known as EDM (Equilibrium Displacement Model). The partial equilibrium framework of the EDM involves linear approximation of changes in prices and quantities of inputs and outputs arising from exogenous changes. However, the EDM requires many parameters estimated including various elasticities, which are frequently criticized for its accuracy. The second method is to use a simple inverse demand function as follows: f(Pd ) = f(Qd , QIM) . where Pd is a domestic cow price, Qd is a demand for domestic beef, and QIM is a quantity of imported beef. The third way is to simply calculate the share of import increase over the total supply increase. This method is straightforward and easy to calculate. Thus the figure calculated will be unambiguous and will be a good method to persuade stakeholders. But this method implicitly adopts a too-strong assumption that price does not respond to demand but responds to only the supply side.

The results of these three methods are summarized below. It seems there is no big difference between methods 1) and 2), and the result of method 3) also falls in the range of methods 1) and 2).

The Korean government announced that DP rate will be tentatively Korean won 13,396/600kg cow[6], using the result of method 1), but the final decision is still pending in National Assembly.

Other Issues related with DP

First, the law does not have limitation on eligible products, but for the convenience of implementation, the government decided that eligible commodities are limited to those whose price data are available and closely related with trade. Now 42 commodities are qualified for the FTA DP. Second, the substitution effects in consumption are not taken into consideration. As the implementation of FTAs progresses, the indirect effect on substitutable goods is also expected to grow in addition to the competition between imported products and domestic products. But since the current direct payment system requires two conditions (import increase and price drop) in a same commodity and because it does not take into account the indirect effect on substitute goods, some conflict is expected. The importation of bananas and mangoes, which are seldom produced domestically, increased and these surely had impact on domestic fruits, such as peaches and apples. But it is very difficult to gauge the impact accurately, thus the commodities that are not grown domestically are excluded from the FTA DP scheme. Third, for most sensitive products, the FTA effect is realized gradually for more than 10 years. For example, tariff of beef is 40% in Korea, and it becomes 0% after 15 years of KOR-US FTA. Therefore, the moving average price of 5 years’ Olympic average may not be appropriate to capture the long term effect of FTA. There is little chance to fulfill the 10% price drop requirement if moving average method were used. Rather, fixed basis price can better reflect the gradual reduction effect of tariff rate on domestic price.

CONCLUSION

FTAs with 47 countries including the US went into effect in Korea, and if the ongoing FTA talks with major countries (such as China) come into fruition with an agreement, then the effect of the market opening due to FTA is expected to exceed the effect of reaching an agreement in the WTO DDA talks (under the condition that Korea maintains the developing country status). Thus, the burden of further opening the market as a result of reaching an agreement at the DDA talks is expected to be low.

As far as the agricultural sector is concerned, the country already has the experience of taking measures to cope with an FTA. In the case of the Korea-Chile FTA, all the projects that were aimed at coping with the FTA were completed by 2010, and now the pressing task is to evaluate the effect and efficiency of the measures that were taken in the last seven years and reflect the results into future financial implementation. Although a partial evaluation was made for some projects, the overall effect is yet to be understood.

In consideration of FTA negotiations that are currently underway, i.e., Korea- China FTA and RCEP, as well as those that have already been concluded, a comprehensive plan is needed to minimize the inefficiency or the overlapping of the current and future complementary measures. In particular, it is necessary to improve the problems of complexity and inefficiency of the support system by switching to a comprehensive direct payment for income support that incorporates various direct payments (including the one for upland farming) and the direct payment for compensating the damage from FTA.

The direct payment for damage compensation may increase finance draining and can delay the restructuring aimed at improving competitiveness. Also, the compensation for business closure can cause an excessive exodus from farming. Therefore, the idea of expanding the project scale should be carefully evaluated.

If the increase in world market prices of agricultural products continues, together with domestic inflation, then the likelihood of carrying out the direct payment for damage compensation purpose during its 10-year operation period is rather low. International organizations like FAO and OECD forecast that the price rise of agricultural products will continue due to such factors as the instability of world grain production caused by climate change, increase in agricultural food consumption caused by the economic growth of developing countries, and the decline in the production of grains caused by the rising demand for bio-energy.

Moreover, since the tariff cuts on major agricultural products will be carried out over a period of more than 10 years (as outlined in the Korea-US FTA and Korea-EU FTA), it is highly unlikely that increase in imports will cause rapid drops in prices in the short term unless a special situation arises. In this case, even if the nominal income of farmers does not decrease, the real income is likely to fall when production costs rise. If the relative decline of farmers' income continues without the direct payment for damage compensation, it will be difficult to maintain an appropriate level of production base. Therefore, it is necessary to examine introducing a mechanism that would make up the decline in real income in the long term.

Meanwhile, as the implementation of FTAs progresses, the indirect effect on substitutable goods is also expected to grow in addition to the competition between imported products and domestic products. But since the current direct payment system requires two conditions (import increase and price drop) in a same commodity and because it does not take into account the indirect effect on substitute goods, some conflict is expected. In addition, various factors influence changes in the price of agricultural products, such as change in income and supply in addition to changes in the amount of imports. Therefore, the question of how to separate and measure these effects is also important tasks ahead.

In the case of the compensation for business closure, the farmers who received the compensation may switch to a different crop, and if so, then the existing farmers who have already been cultivating the crop will suffer damages as the supply increases. This is an example of the "balloon effect" where reduction in one side increases the other. Also, there could be the problem of inefficient distribution of resources if the farmer who received the compensation decides to cultivate the same crop again after a lapse of time. Therefore, further examination is needed to find solutions to such problems.

References

Choi, Sae-Kyun. 2011. The Impact and Future task of Korea- US FTA on Korean Agriculture. Agricultural Policy Focus, No. 4 (2011.12.22) (in Korean).

KREI (Korea Rural Economic Institute). 2013. Annual report of FTA Implementation Results in 2012 (in Korean).

MOFAT (Ministry of Foreign Affairs and Trade). 2011. Korea and FTAs. (http://www.fta.go.kr/new/ftakorea/policy.asp; Accessed 2 September 2013).

MTIE(Ministry of Trade, Industry and Energy). http://www.fta.go.kr/new2/ftakorea/ ftakorea2010.asp; Accessed 31 August 2013).

Moon, Hanphil., Choi, Seguin. 2012. The impact of FTA Proliferation and Future tasks in Korea. Paper presented at 2012 Agricultural Outlook in Korea. Korea Rural economic Institute. (in Korean).

OECD. 2012. The Impact of Regional Trade Agreement on Agricultural Trade. TAD/TC/CA/WP (2012) 2, May, 2012.

Regmi, Anita, Gehlhar, Mark., Wainio, John., Volrath, Thomas., Johnston, Paul., and Dathuria, Nitin. 2005. Market Access for High-Value Foods. Electronic Report from the Economic Research Service, USDA/ERS Report No. 840, February.

Zahniser, Steven, Zachary Crago 2009. NAFTA at 15: Building on Free Trade USDA/ERS WRS-09-03.

[1] The Degree of dependence on trade can be defined as (export amount + Import amount)/GDP. The Degree of dependence on trade in Korea was 96.7% in 2011, 18.7% in U.S. in 2009, 22.3% in Japan in 2009.

[2] In the first phase, the two sides will decide on how they can agree on sensitivity issues (i.e., tariff concession exemptions, longer reduction period, creation of new TRQs, etc.) and to what extent they will reflect the 'sensitivity.' It looks like as though the two sides will categorize the tariff lines into three tracks of concessions as adopted in the Korea-ASEAN FTA - that is, ‘normal’, ‘sensitive’, and ‘highly sensitive’ areas.

[3] But, for the FTA partner country import requirement, additional trigger level is applied to prevent frequent happening . For example, if the import share of a country for the product is less than 10%, the basis trigger level shall equal to 115% of import volume of previous five year Olympic average, which is similar to SSG trigger level in UR Agreement of Agriculture.

[4] Since the direct payment for damage compensation can be categorized as commodity specific subsidy, it should be operated within the total AMS or de-minimis.

[5] It was decided that starting from 2012, 400,000 won will be provided annually per ha as direct payment for upland farming of 19 products (wheat, bean, barley, corn, rye, millet, sorghum, buckwheat, other grains, red bean, mungbean, other pulses, bulky feed, peanut, sesame, chili, garlic).

[6] In Korea, some people raise cows to give birth to calves and sell them. Thus, calves are considered as a different product from cows and the payment rate is also calculated separately.

|

Submitted as a country paper for the FFTC-NACF International Seminar on Threats and Opportunities of the Free Trade Agreements in the Asian Region, Sept. 29 - Oct. 3, 2013, Seoul, Korea |

The Effects of FTAs and Compensation Measures in Korean Agriculture

Joo-Ho Song and Han-Phil Moon

Korea Rural Economic Institute(KREI), Hoigi, Seoul, South Korea

e-mail: jhsong@krei.re.kr

ABSTRACT

During the past 10 years since the signing of an FTA with Chile in 2002, Korea has signed 10 FTAs with 47 countries. As of July 2012, negotiations for FTAs are underway in Korea with 11 countries including China, Canada, Australia and New Zealand. For the agricultural sector which is expected to suffer damages due to the FTAs, the government has made a plan to compensate damages in the short term and improve agriculture`s competitiveness in the medium and long term. The Korean government introduced an FTA direct payment for damage compensation for some fruits right after KOR-CHILE FTA in 2004, the coverage of which has been expanded to all products after KOR-US FTA in 2012. The FTA Direct Payment for KOR-CHILE FTA has not been paid at all, but this year it is likely to be paid for some products for KOR-US FTA. However, whether to consider the share of FTA effects on the price drop to determine the payment rate remains to be solved. This first experience in paying FTA direct payment gave warning to the policy makers that compensation measures should be designed carefully.

Key Words: FTA, WTO, direct payment, compensation measure

INTRODUCTION

South Korea is one of the biggest beneficiaries of the multilateral trade system, of which the most typical example is the World Trade Organization (WTO), and the country is often quoted as a role model for having made economic progress through trade[1]. Recently, Korea has been actively seeking free trade agreements. The reason is that, amid the globally expanding regionalism, it hopes to minimize any damages it could suffer for being an outsider to the “FTA network” and actively respond to such challenges, while advancing the national systems in general and strengthening the economic competitiveness through proactive market opening and liberalization (MOFAT 2011). In promoting the FTAs, agricultural sector was considered as the weak point because Korean agriculture has relatively low competitiveness in the international market. Thus, the basic strategy for FTA is to maximize the benefit of free trade in industrial goods and to minimize the negative impact on agriculture.

During the past 10 years since the signing of an FTA with Chile in 2002, Korea has signed 10 FTAs with 47 countries. In addition to Chile, Korea signed an FTA with Singapore (November 2004), four Europe countries (EFTA, July 2005), 10 ASEAN members (April 2006), India (September 2008) and the US (originally signed in April 2007 but revised in December 2010 after renegotiation), 27 EU members (October 2009), Peru (August 2010) and Turkey (March 2012). The FTAs with these countries have already went into effect and the FTAs with Columbia (June 2012) is signed and yet to be ratified by their respective legislature.

As of August 2013, negotiations for FTAs are underway with China, Vietnam and Indonesia. Korea also joined RCEP (Regional Comprehensive Economic Partnership) that consisted of ASEAN +6 (China, Japan, Korea, Australia, New Zealand and India) countries and China-Japan-Korea FTA was launched May, 2013. The first official talk for an FTA with China began in May 2012, and the negotiation is being carried out in two phases. In the first phase, the two sides discuss the modality in goods, services, and investments sectors and especially how to deal with sensitive products. Only when the two sides agree on the modality will the second phase of negotiations begin[2] which will be single- undertaking.

Korea is trying to resume FTAs which already started but now suspended with Japan, Canada, Mexico, Australia, New Zealand, and the six countries of the Gulf Cooperation Council (GCC). Other than these countries, the countries with which Korea has concluded a joint research or is in the middle of creating favorable conditions are four countries of MERCOSUR, Israel, Malaysia and five countries in Middle America (MTIE, 2013).

Of the total amount of Korea's agricultural import (US$22billion, 2012), the share of trade with FTA partners including the US, EU, ASEAN, and Chile reached 50%. If the current talks for FTA come to fruition as planned, more than 90% of Korea's agricultural imports would be coming from FTA partners.

The average bound tariff rate of Korean agricultural products is 63.8%, and Korea has maintained the principle of seeking concession exemptions or partial market opening of major agricultural products in consideration of the unique position Korean agriculture holds in FTA negotiations. It is evaluated that in the case of FTAs with Chile and the ASEAN, which were concluded in the early days, and FTAs with countries that are not big exporters of agricultural products, the extent of market opening was considerably low. As for the tariffs on products that had little impact on the domestic market or those that the country already relied on to meet most of its demand, tariff concessions were made in such a way that tariffs could be abolished early.

However, in the case of the recently concluded Korea-US FTA, a relatively high level of concessions was made. Also, a similar result was obtained in the Korea-EU FTA, which was signed after the conclusion of negotiations with the US.

Korea excluded rice from the concessions list in all FTAs, and as for other sensitive products, it strived to minimize damages from the market opening through such means as retention of current tariffs, TRQ offers, introduction of seasonal tariffs, partial abolition of tariffs or extension of abolition period, and agreement on safeguards (ASG).

Preliminary Estimation of FTA Impact on Agriculture

The amount of damage to the domestic agriculture that could result from the Korea-US FTA was estimated using the simulation model KASMO-2008 developed by the Korea Rural Economic Institute.

Using the data from 1980 to 2008, and under the premise that no Korea-US FTA was signed and that such a market condition continued, the amount of agricultural production was estimated for the period ending in 2026. With the amount set as the baseline, a policy simulation was made wherein the Korea-US FTA goes into effect on January 1, 2012, and a tariff reduction schedule was applied according to the concession agreement.

For each item on the concessions list, the following aspects were considered: 1) the substitution effect between the imported product and the domestic kind; 2) import substitution effect between the US and other countries; 3) demand substitution effect between commodities, and 4) competition effect in production for finite arable land.

The simulation results showed that if the Korea-US FTA goes into effect, agricultural production in Korea is estimated to decrease by Korean won 678.5 billion in the 5th year after the agreement's enforcement, Korean won 991.2 billon in the 10th year, and Korean won 1 trillion 235.4 billion in the 15th year. Damage is predicted to be big especially in the livestock sector. In the 15th year, the damage is estimated to be Korean won 443.8 billion in the case of beef, Korean won 208.5 billion in the case of pork, and Korean won 108.7 billion in the case of chicken (Choi, 2011).

Policy Response to FTAs : Compensation Measures

For the agricultural sector which is expected to suffer damages due to the FTA, the government has made a plan to compensate damages in the short term and improve agriculture's competitiveness in the medium and long term. For the first FTA with Chile, the Korean government introduced an FTA direct payment (FTA DP) for damage compensation and a buyout program for some fruits (kiwi and house-grown grape) which were expected to be affected mostly because Chile is a fruit exporter. The FTA DP was designed to be paid only when agricultural import from an FTA partner increases and subsequently the price falls. If the market price of a product in a given year is less than 80% of the average price (basis price) of three years in the past five years excluding the years with the highest and lowest price, then farmers are awarded 80% of the difference between the basis price and the market price. The requirement for the FTA DP is

(i) when the price in a given year falls below the basis price, and

(ii) when the total import volume and the import volume from the FTA partner in a given year exceed the basis volume, which is calculated as the Olympic average of the previous five years[3].

The support amount is calculated as follows:

* Support amount = cultivated area of the product× national average production amount per unit area × DP rate × adjustment factor

Here, DP rate = (basis price - price in the given year) × compensation rate (80%)

Basis price = three-year average excluding the highest and lowest price in the past five years×80%

Adjustment factor=policy variable for payment within the permitted range[4] set by the WTO

The compensation for business closure (buyout program) is limited to some fruits (kiwi, house-grown grape and peach) farms. The level of payment is three years worth of net income (=gross income – production cost – self-labor). The application period was five years from the start of the FTA.

There had not been strong resistance from the agricultural sector about subsequent FTAs until 2006 because the FTA partners for Korea during 2004-2006 were not big exporters or the concession level was not so high. However, KOR-US FTA in 2007 was different. Korea opened the domestic market for agricultural commodities except rice and the US is the biggest exporter of agricultural products. Thus, the Korean government augmented previous supplementary measures to soothe angry farmers such that the range of products for damage compensation shall be expanded to include all products (previously, only kiwis and green house-grown grapes were eligible for the direct payment and the buyout program was limited to kiwis, green house-grown grapes and peaches) that actually suffer damages and that the compensation rate, as well as the basis price, shall be increased to 90% from 80%. The improved measure is the result of embracing the farmers’ suggestion that the trigger level should be lowered in the National Assembly during the ratification process. But it caused many unexpected problems in determining the actual payment rate. The operation period of the direct payment for damage compensation is 10 years from the start of the FTA.

The compensation for business closure for KOR-US FTA becomes tougher compared with KOR-CHILE FTA. It is limited to those cases where facility investment is made for products that have met the requirements for direct payment, and the level of compensation is three years’ worth of net profit (= net income – cost of owned land and capital), which is lower than that of KOR-CHILE Buyout Program. The compensation period is five years from the start of the FTA. Such a change was taken to rectify the excessive support that was given to the producers of agricultural products, such as peach, that had not been directly affected by imports.

In addition, the direct payment for upland (non-rice) farming was newly introduced[5] by the Korean National Assembly, and it is expected to cause much difficulty in the implementation stage since it is not easy to confirm the target fields of each farm household and the administrative cost is very high. These modified FTA DP and buyout programs apply to all FTAs.

Evaluation of FTA Implementation and Compensation measures

Korea-Chile Agricultural Trade Trends

The trade amount of agricultural and livestock products between Korea and Chile has grown five-fold from US$50 million in 2003 when there was no free trade agreement between the two countries to US$250 million in 2010. The export amount of Korea's agricultural products and foods in 2010 was only US$900,000.

After the entry into force of the Korea-Chile FTA, the annual growth rate of agricultural imports from Chile was very high at 20% on average. Especially in the case of Chilean fruits which are competitive in international markets, the growth rate reached 29%. The products that saw a big increase in import as a result of the FTA are grape, kiwifruit, wine, and pork. The share of each one of these Chilean fruits in the total imported fruit market also increased sharply (grape 70% share, kiwifruit 13%, wine 22%, and pork 16% share as of 2010).

The target products for direct payment in response to the Korea-Chile FTA are kiwifruit and greenhouse grapes. After the entry into force of the FTA, the amount of imported kiwifruit and grapes all increased, but the price of kiwifruit increased instead of decreasing, and in the case of grapes, the direct payment was not provided because it did not meet the requirement of more than 20% drop from the basis price even though the price fell.

Korea’s Agricultural Trade with EU and US.

Changes in the amount and price of imported agricultural products were observed in 2012. The Korea-EU FTA was effective from July 1, 2011, and Korea-US FTA went into effect on March 15, 2012. Thus, for the Korea- US FTA, the relevant data were adjusted considering the period of January 1 to March 14. In 2012, it looks like that the direct payment for damage compensation will not be implemented for most of the covered products because there is little product that meets all the three requirements, which are 1) increase in total amount of import, 2) increase in the amount of import from the FTA partner, and 3) price drop. If the import increase was mainly from non-FTA partners, then Direct Payment will not be paid even when the requirement 1) is met.

For major commodities in Table 4, most commodities satisfied the requirement of total import and the country import requirement. The exceptions are wheat, kiwi and eggs. In the case of wheat, the total import requirement was met, but that import increase was mainly from Brazil which is not an FTA partner. The total import requirement was not satisfied in the case of kiwi and eggs. However, even though most commodities satisfied both the total import and country import requirements, they could not meet the price drop requirement except for beef.

Thus, beef is the only eligible product for the FTA compensation direct payment in 2012.

But when we scrutinize the case of beef, domestic supply in 2012 increased by 24% compared with the previous five-year (2007-2011) average and import quantity increased by only 10.3% compared with the previous five-year average. The impact of first year of Korea- US FTA was only 2.7% tariff reduction in beef (from 40% to 37.3%). Thus, it is most likely that the main reason of beef price drop in 2012 below the basis price level was due to the increase in domestic supply rather than import surge. Too many beef cows (3,059 thousand heads in 2012) resulted in the over-supply of domestic beef.

Determining the share of import impact on price drop.

The direct payment for beef can be calculated as follows.

DP rate = (basis price - price in the given year) × compensation rate (90%)

= (4,725,000 – 4,664,000) × 90% = 54,900/600 kg cow

But because it is hard to deny that the decrease in the beef price (actually cow price) in 2012 resulted mainly from the oversupply of domestic beef, the government decided to apply the share of the impact of import increase to the price drop to calculate the amount of DP to be paid. There are arguments on the DP rate whether to consider additionally the share of impact of import increase to price changes. In the relevant law, there is no regulation to calculate this share. Farmers’ groups and some politicians insist that the government should pay a full DP rate and should not segregate the impact of import increase and impact of domestic oversupply on price drop.

There can be several methods to calculate the share of the import impact on the price drop. First, one economically plausible way is to use the comparative static approach which is commonly known as EDM (Equilibrium Displacement Model). The partial equilibrium framework of the EDM involves linear approximation of changes in prices and quantities of inputs and outputs arising from exogenous changes. However, the EDM requires many parameters estimated including various elasticities, which are frequently criticized for its accuracy. The second method is to use a simple inverse demand function as follows: f(Pd ) = f(Qd , QIM) . where Pd is a domestic cow price, Qd is a demand for domestic beef, and QIM is a quantity of imported beef. The third way is to simply calculate the share of import increase over the total supply increase. This method is straightforward and easy to calculate. Thus the figure calculated will be unambiguous and will be a good method to persuade stakeholders. But this method implicitly adopts a too-strong assumption that price does not respond to demand but responds to only the supply side.

The results of these three methods are summarized below. It seems there is no big difference between methods 1) and 2), and the result of method 3) also falls in the range of methods 1) and 2).

The Korean government announced that DP rate will be tentatively Korean won 13,396/600kg cow[6], using the result of method 1), but the final decision is still pending in National Assembly.

Other Issues related with DP

First, the law does not have limitation on eligible products, but for the convenience of implementation, the government decided that eligible commodities are limited to those whose price data are available and closely related with trade. Now 42 commodities are qualified for the FTA DP. Second, the substitution effects in consumption are not taken into consideration. As the implementation of FTAs progresses, the indirect effect on substitutable goods is also expected to grow in addition to the competition between imported products and domestic products. But since the current direct payment system requires two conditions (import increase and price drop) in a same commodity and because it does not take into account the indirect effect on substitute goods, some conflict is expected. The importation of bananas and mangoes, which are seldom produced domestically, increased and these surely had impact on domestic fruits, such as peaches and apples. But it is very difficult to gauge the impact accurately, thus the commodities that are not grown domestically are excluded from the FTA DP scheme. Third, for most sensitive products, the FTA effect is realized gradually for more than 10 years. For example, tariff of beef is 40% in Korea, and it becomes 0% after 15 years of KOR-US FTA. Therefore, the moving average price of 5 years’ Olympic average may not be appropriate to capture the long term effect of FTA. There is little chance to fulfill the 10% price drop requirement if moving average method were used. Rather, fixed basis price can better reflect the gradual reduction effect of tariff rate on domestic price.

CONCLUSION

FTAs with 47 countries including the US went into effect in Korea, and if the ongoing FTA talks with major countries (such as China) come into fruition with an agreement, then the effect of the market opening due to FTA is expected to exceed the effect of reaching an agreement in the WTO DDA talks (under the condition that Korea maintains the developing country status). Thus, the burden of further opening the market as a result of reaching an agreement at the DDA talks is expected to be low.

As far as the agricultural sector is concerned, the country already has the experience of taking measures to cope with an FTA. In the case of the Korea-Chile FTA, all the projects that were aimed at coping with the FTA were completed by 2010, and now the pressing task is to evaluate the effect and efficiency of the measures that were taken in the last seven years and reflect the results into future financial implementation. Although a partial evaluation was made for some projects, the overall effect is yet to be understood.

In consideration of FTA negotiations that are currently underway, i.e., Korea- China FTA and RCEP, as well as those that have already been concluded, a comprehensive plan is needed to minimize the inefficiency or the overlapping of the current and future complementary measures. In particular, it is necessary to improve the problems of complexity and inefficiency of the support system by switching to a comprehensive direct payment for income support that incorporates various direct payments (including the one for upland farming) and the direct payment for compensating the damage from FTA.

The direct payment for damage compensation may increase finance draining and can delay the restructuring aimed at improving competitiveness. Also, the compensation for business closure can cause an excessive exodus from farming. Therefore, the idea of expanding the project scale should be carefully evaluated.

If the increase in world market prices of agricultural products continues, together with domestic inflation, then the likelihood of carrying out the direct payment for damage compensation purpose during its 10-year operation period is rather low. International organizations like FAO and OECD forecast that the price rise of agricultural products will continue due to such factors as the instability of world grain production caused by climate change, increase in agricultural food consumption caused by the economic growth of developing countries, and the decline in the production of grains caused by the rising demand for bio-energy.

Moreover, since the tariff cuts on major agricultural products will be carried out over a period of more than 10 years (as outlined in the Korea-US FTA and Korea-EU FTA), it is highly unlikely that increase in imports will cause rapid drops in prices in the short term unless a special situation arises. In this case, even if the nominal income of farmers does not decrease, the real income is likely to fall when production costs rise. If the relative decline of farmers' income continues without the direct payment for damage compensation, it will be difficult to maintain an appropriate level of production base. Therefore, it is necessary to examine introducing a mechanism that would make up the decline in real income in the long term.

Meanwhile, as the implementation of FTAs progresses, the indirect effect on substitutable goods is also expected to grow in addition to the competition between imported products and domestic products. But since the current direct payment system requires two conditions (import increase and price drop) in a same commodity and because it does not take into account the indirect effect on substitute goods, some conflict is expected. In addition, various factors influence changes in the price of agricultural products, such as change in income and supply in addition to changes in the amount of imports. Therefore, the question of how to separate and measure these effects is also important tasks ahead.

In the case of the compensation for business closure, the farmers who received the compensation may switch to a different crop, and if so, then the existing farmers who have already been cultivating the crop will suffer damages as the supply increases. This is an example of the "balloon effect" where reduction in one side increases the other. Also, there could be the problem of inefficient distribution of resources if the farmer who received the compensation decides to cultivate the same crop again after a lapse of time. Therefore, further examination is needed to find solutions to such problems.

References

Choi, Sae-Kyun. 2011. The Impact and Future task of Korea- US FTA on Korean Agriculture. Agricultural Policy Focus, No. 4 (2011.12.22) (in Korean).

KREI (Korea Rural Economic Institute). 2013. Annual report of FTA Implementation Results in 2012 (in Korean).

MOFAT (Ministry of Foreign Affairs and Trade). 2011. Korea and FTAs. (http://www.fta.go.kr/new/ftakorea/policy.asp; Accessed 2 September 2013).

MTIE(Ministry of Trade, Industry and Energy). http://www.fta.go.kr/new2/ftakorea/ ftakorea2010.asp; Accessed 31 August 2013).

Moon, Hanphil., Choi, Seguin. 2012. The impact of FTA Proliferation and Future tasks in Korea. Paper presented at 2012 Agricultural Outlook in Korea. Korea Rural economic Institute. (in Korean).

OECD. 2012. The Impact of Regional Trade Agreement on Agricultural Trade. TAD/TC/CA/WP (2012) 2, May, 2012.

Regmi, Anita, Gehlhar, Mark., Wainio, John., Volrath, Thomas., Johnston, Paul., and Dathuria, Nitin. 2005. Market Access for High-Value Foods. Electronic Report from the Economic Research Service, USDA/ERS Report No. 840, February.

Zahniser, Steven, Zachary Crago 2009. NAFTA at 15: Building on Free Trade USDA/ERS WRS-09-03.

[1] The Degree of dependence on trade can be defined as (export amount + Import amount)/GDP. The Degree of dependence on trade in Korea was 96.7% in 2011, 18.7% in U.S. in 2009, 22.3% in Japan in 2009.

[2] In the first phase, the two sides will decide on how they can agree on sensitivity issues (i.e., tariff concession exemptions, longer reduction period, creation of new TRQs, etc.) and to what extent they will reflect the 'sensitivity.' It looks like as though the two sides will categorize the tariff lines into three tracks of concessions as adopted in the Korea-ASEAN FTA - that is, ‘normal’, ‘sensitive’, and ‘highly sensitive’ areas.

[3] But, for the FTA partner country import requirement, additional trigger level is applied to prevent frequent happening . For example, if the import share of a country for the product is less than 10%, the basis trigger level shall equal to 115% of import volume of previous five year Olympic average, which is similar to SSG trigger level in UR Agreement of Agriculture.

[4] Since the direct payment for damage compensation can be categorized as commodity specific subsidy, it should be operated within the total AMS or de-minimis.

[5] It was decided that starting from 2012, 400,000 won will be provided annually per ha as direct payment for upland farming of 19 products (wheat, bean, barley, corn, rye, millet, sorghum, buckwheat, other grains, red bean, mungbean, other pulses, bulky feed, peanut, sesame, chili, garlic).

[6] In Korea, some people raise cows to give birth to calves and sell them. Thus, calves are considered as a different product from cows and the payment rate is also calculated separately.